Embed Size (px)

Citation preview

Country Profile 2006

Kazakhstan This Country Profile is a reference work, analysing the country�s history, politics, infrastructure and economy. It is revised and updated annually. The Economist Intelligence Unit�s Country Reports analyse current trends and provide a two-year forecast.

The full publishing schedule for Country Profiles is now available on our website at www.eiu.com/schedule The Economist Intelligence Unit 26 Red Lion Square London WC1R 4HQ United Kingdom

The Economist Intelligence Unit

The Economist Intelligence Unit is a specialist publisher serving companies establishing and managing operations across national borders. For over 50 years it has been a source of information on business developments, economic and political trends, government regulations and corporate practice worldwide.

The Economist Intelligence Unit delivers its information in four ways: through its digital portfolio, where the latest analysis is updated daily; through printed subscription products ranging from newsletters to annual reference works; through research reports; and by organising seminars and presentations. The firm is a member of The Economist Group.

London The Economist Intelligence Unit 26 Red Lion Square London WC1R 4HQ United Kingdom Tel: (44.20) 7576 8000 Fax: (44.20) 7576 8500 E-mail: [email protected]

New York The Economist Intelligence Unit The Economist Building 111 West 57th Street New York NY 10019, US Tel: (1.212) 554 0600 Fax: (1.212) 586 0248 E-mail: [email protected]

Hong Kong The Economist Intelligence Unit 60/F, Central Plaza 18 Harbour Road Wanchai Hong Kong Tel: (852) 2585 3888 Fax: (852) 2802 7638 E-mail: [email protected]

Website: www.eiu.com

Electronic delivery This publication can be viewed by subscribing online at www.store.eiu.com

Reports are also available in various other electronic formats, such as CD-ROM, Lotus Notes, online databases and as direct feeds to corporate intranets. For further information, please contact your nearest Economist Intelligence Unit office

Copyright © 2006 The Economist Intelligence Unit Limited. All rights reserved. Neither this publication nor any part of it may be reproduced, stored in a retrieval system, or transmitted in any form or by any means, electronic, mechanical, photocopying, recording or otherwise, without the prior permission of The Economist Intelligence Unit Limited.

All information in this report is verified to the best of the author's and the publisher's ability. However, the Economist Intelligence Unit does not accept responsibility for any loss arising from reliance on it.

ISSN 1364-3541

Symbols for tables �n/a� means not available; ��� means not applicable

Printed and distributed by Patersons Dartford, Questor Trade Park, 151 Avery Way, Dartford, Kent DA1 1JS, UK.

TUR

KM

EN

ISTA

N

UZB

EK

ISTA

N

TAJI

KIS

TAN

KYR

GYZ

RE

P.

CH

INA

RU

SS

IA

IRA

N

© T

he

Eco

no

mis

t In

tell

igen

ce U

nit

Lim

ited

20

06

CASP

IAN

SEA

AR

AL

SEA

Alm

aty

Alm

aty

Alm

aty

Sem

eySe

mey

(Sem

ipal

atin

sk)

(Sem

ipal

atin

sk)

Sem

ey(S

emip

alat

insk

)

Pav

lod

arP

avlo

dar

Pav

lod

ar

Turk

esta

nTu

rkes

tan

Shym

kSh

ymke

nt

ent

Shym

ken

t

Lep

syLe

psy

Ru

dn

yR

ud

ny

Kar

agan

dy(

Kar

agan

da)

Kar

agan

dy(

Kar

agan

da)

Kar

agan

dy(

Kar

agan

da)

Osk

emen

Osk

emen

(Ust

-Kam

enog

orsk

)(U

st-K

amen

ogor

sk)

Osk

emen

(Ust

-Kam

enog

orsk

)

AST

AN

AA

STA

NA

AST

AN

A

Pet

rop

aP

etro

pav

lovs

kvl

ovsk

Pet

rop

avlo

vsk

Lep

sy

Akt

og

ayA

kto

gay

Aya

gu

zA

yag

uz

Aya

go

z

Zyry

ano

vsk

Len

ino

go

rsk

Akt

og

ay

Bal

khas

hB

alkh

ash

Bal

khas

h

L. B

alk

ha

sh

Ka

pch

aga

ysko

ye R

es.L.L.

Ala

kol

Ala

kol

L. A

lako

l

L. Z

ays

an

L. S

elet

yten

iz

L. T

engi

zL.

Ten

giz

L. T

engi

z

L. S

asy

kko

lL.

Sa

sykk

ol

L. S

asy

kko

l

Akt

au

Fort

Sh

evch

enko

No

vyy

Uze

n

Bey

neu

Aty

rau

Akt

ob

eA

kto

be

(Akt

yub

insk

)(A

ktyu

bin

sk)

Akt

ob

e(A

ktyu

bin

sk)

Kar

abu

tak

Aks

Aks

ayayU

rals

kU

rals

kU

rals

kA

ksay

Uil

Mak

atM

akat

Mak

at

Alg

a Emb

a Chel

kar

Ara

lsk

nsk

nsk

No

voka

zali

nsk

Kyz

ylo

rda

Ary

sA

rys

Ary

s

Turk

esta

nTa

raz

Shu

Tald

yko

rgan

Tald

yko

rgan

Tald

yko

rgan

Kap

chag

ayK

apch

agay

Kap

chag

ay

Pan

filo

van

filo

vPa

nfi

lov

Chig

anak

Ku

stan

ayK

ust

anay

Ku

stan

ayR

ud

ny

Atb

asar

Atb

asar

Ark

alyk

Ark

alyk

Atb

asar

Ark

alyk

Tem

irta

u

Ab

ayK

arka

rali

nsk

Kar

kara

lin

skK

arka

rali

nsk

Ekib

astu

zEk

ibas

tuz

Ekib

astu

z

Ko

ksh

etau

Ko

ksh

etau

Ko

ksh

etau

Turg

ay

Dzh

ezka

zgan

Dzh

etyg

ara

Dzh

etyg

ara

Dzh

etyg

ara

Shch

uch

insk

Ka

za

kh

Up

lan

ds

Ka

za

kh

Up

lan

ds

Be

tp

ak

da

la

Ca

spia

n

De

pre

ssio

n

To

rgh

ay

Pla

tea

u

Ust

yu

rtP

late

au

KA

ZA

KH

STA

NK

AZ

AK

HS

TAN

KA

ZA

KH

STA

N

Irtysh

R.

Syrda r

yaR.

Emba

R.

Ural R.

0 k

m10

02

00

30

05

00

0 m

iles

100

30

02

00

40

0

July

20

06

Mai

n r

ailw

ay

Mai

n r

oad

Inte

rnat

ion

al b

ou

nd

ary

Mai

n a

irp

ort

Cap

ital

Maj

or

tow

n

Oth

er t

ow

n

Country Profile 2006 www.eiu.com © The Economist Intelligence Unit Limited 2006

Comparative economic indicators, 2005

Gross domestic product(US$ bn)

Sources: Economist Intelligence Unit estimates; national sources.

0 20 40 60 80 100 120 140

TajikistanKyrgyz Republic

MoldovaArmenia

MacedoniaGeorgia

TurkmenistanAlbania

Bosnia and HercegovinaUzbekistanAzerbaijan

EstoniaLatvia

LithuaniaSerbia and Montenegro

BulgariaBelarus

SloveniaCroatia

SlovakiaKazakhstan

UkraineRomaniaHungary

Czech RepublicPolandRussia

Gross domestic product(% change, year on year)

Sources: Economist Intelligence Unit estimates; national sources.

-2 0 2 4 6 8 10 12 14 16

Kyrgyz RepublicUkrainePoland

SloveniaMacedonia

RomaniaHungary

CroatiaBosnia and Hercegovina

BulgariaAlbania

TurkmenistanCzech Republic

SlovakiaSerbia and Montenegro

RussiaTajikistan

UzbekistanMoldova

LithuaniaBelarusGeorgia

KazakhstanEstonia

LatviaArmenia

Azerbaijan

0 2 4 6 8 10 12 14 16

MacedoniaArmenia

Czech RepublicPoland

AlbaniaSloveniaSlovakia

LithuaniaCroatia

HungaryEstonia

Bosnia and HercegovinaBulgaria

Kyrgyz RepublicLatvia

UzbekistanTajikistan

KazakhstanGeorgia

RomaniaAzerbaijan

BelarusTurkmenistan

MoldovaRussia

UkraineSerbia and Montenegro

Consumer prices(% change, year on year)

Sources: Economist Intelligence Unit estimates; national sources.

Gross domestic product per head(US$ '000)

Sources: Economist Intelligence Unit estimates; national sources.

0 2 4 6 8 10 12 14 16 18

TajikistanUzbekistan

Kyrgyz RepublicMoldova

TurkmenistanGeorgia

AzerbaijanArmeniaUkraine

Bosnia and HercegovinaSerbia and Montenegro

MacedoniaAlbaniaBelarus

BulgariaKazakhstan

RomaniaRussiaLatvia

LithuaniaPolandCroatia

SlovakiaEstonia

HungaryCzech Republic

Slovenia763.6

26.4

303.2

0.0

Kazakhstan 1

© The Economist Intelligence Unit Limited 2006 www.eiu.com Country Profile 2006

Contents

Kazakhstan

3 Basic data

4 Politics 4 Political background 5 Recent political developments 9 Constitution, institutions and administration 10 Political forces 14 International relations and defence

17 Resources and infrastructure 17 Population 18 Education 19 Health 20 Natural resources and the environment 21 Transport, communications and the Internet 22 Energy provision

23 The economy 23 Economic structure 24 Economic policy 26 Economic performance 27 Regional trends

27 Economic sectors 27 Agriculture 28 Mining and semi-processing 31 Manufacturing 31 Construction 32 Financial services 33 Other services

33 The external sector 33 Trade in goods 35 Invisibles and the current account 36 Capital flows and foreign debt 37 Foreign reserves and the exchange rate

39 Regional overview 39 Membership of organisations

43 Appendices 43 Sources of information 44 Reference tables 44 Population 45 Labour force 45 Energy production 46 State budget

2 Kazakhstan

Country Profile 2006 www.eiu.com © The Economist Intelligence Unit Limited 2006

46 Money supply 47 Interest rates 47 Gross domestic product 47 Nominal gross domestic product by expenditure 48 Real gross domestic product by expenditure 48 Prices and earnings 48 Main trading partners 49 Main composition of trade 49 Balance of payments, IMF series 50 External debt, World Bank series 50 Foreign reserves 50 Exchange rates

Kazakhstan 3

© The Economist Intelligence Unit Limited 2006 www.eiu.com Country Profile 2006

Kazakhstan

Basic data

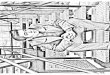

2,717,300 sq km

15,219,300 (January 1st 2006 estimate)

The capital was moved from Almaty to Astana (formerly Akmola) on December 10th 1997

Population in !000 (1999 census)

Almaty 1,129 Karaganda 437 Shymkent 360 Astana 313 Ust-Kamenogorsk 311 Pavlodar 301 Semipalatinsk 270 Petropavlovsk 204

Continental. Average temperature in Astana in winter: -18°C; in summer: 20°C. Average temperature in Almaty in winter: -8°C; in summer: 22°C

Kazakh is the state language. Russian is the most widely spoken language and is the de facto language of administration

Metric system

Tenge. Average exchange rate in 2005: Tenge132.88:US$1; exchange rate on June 29th 2006: Tenge119.21:US$1

Calendar year

6 hours ahead of GMT; 5 hours ahead of GMT in Western Kazakhstan

January 1st (New Year); March 8th (Women!s Day); March 21st-22nd (Novruz); May 1st (Unification holiday); May 9th (Victory Day); August 30th (Constitution Day); October 25th (Republic Day), December 16th (Independence Day)

Total area

Population

Main towns

Climate

Languages

Weights and measures

Currency

Fiscal year

Public holidays

Time

4 Kazakhstan

Country Profile 2006 www.eiu.com © The Economist Intelligence Unit Limited 2006

Politics

Kazakhstan has been ruled by one man since its independence from the Soviet Union in 1991: Nursultan Nazarbayev, the current president and formerly the first secretary of the Communist Party of the Kazakh Soviet Socialist Republic. Kazakhstan has had a series of different parliaments, two constitutions, frequent constitutional amendments and long periods during which Mr Nazarbayev has ruled by decree. Since 1995 Mr Nazarbayev has steadily increased his control over Kazakhstan!s political structures, which has allowed him to secure re-election several times, the most recent presidential election being in December 2005. He has benefited from two flawed referendums, in April and August 1995, that cancelled the presidential election planned for 1996 and introduced a new constitution enhancing his powers. Mr Nazarbayev!s supporters won virtually all of the seats in the new bicameral parliament following the legislative election held in December 1995.

In October 1998 Mr Nazarbayev brought forward the presidential election, originally planned for the end of 2000, to January 10th 1999. Along with constitutional changes introduced at the same time, Mr Nazarbayev in effect became president for life. With his main rival barred from standing, Mr Nazarbayev was comfortably re-elected in January 1999 and his supporters won a flawed parliamentary election in October 1999. On June 27th 2000 he granted himself immunity from prosecution. Mr Nazarbayev has also appointed members of his family to prominent positions.

Political background

Modern Kazakhstan!s history is closely linked to that of Russia. In 1730 a request by one of the three Kazakh tribal confederations for Russian protection from external attack led to the gradual subordination of the Kazakhs to the Russian empire. There was relatively slow Russian immigration into what is now Kazakhstan before the 1930s. However, considerable anti-Russian resentment had built up by the early 20th century"especially following Russia!s violent crushing of Kazakh resistance to conscription into the Tsarist army in 1916. When Tsarist Russia collapsed in 1917, Kazakh nationalists declared an autonomous Kazakh government in the east of the country. Defeat by the Bolsheviks in 1920, however, led to integration into the Russian Federation as an autonomous Kazakh republic, followed by the establishment of the Kazakh Soviet Socialist Republic as a separate and full union republic in 1936.

Communism had a disastrous effect on the mainly nomadic Kazakhs, who were forcibly sedentarised during Soviet rule. During the 1930s the number of Kazakhs dropped from 4m to 3m as a result of starvation, emigration and purges. Throughout the Stalinist era Kazakhstan became a dumping-ground for unwanted ethnic groups, deported en masse to the republic. Russian immigration picked up substantially. Until the 1950s Russians dominated the republic both numerically and politically. However, although they continued to be subservient to Moscow, Kazakhs succeeded in gradually increasing their political power locally, especially under Dinmukhamed Kunayev, the first

Russian protection leads to Russian colonisation

Kazakhstan 5

© The Economist Intelligence Unit Limited 2006 www.eiu.com Country Profile 2006

secretary of the Kazakh Communist Party (1962-86), who was a close friend of Leonid Brezhnev, general secretary of the Communist Party of the Soviet Union (CPSU). At the same time the urban Kazakh population became increasingly Russified.

The rule of Mr Kunayev, who allowed corruption to flourish, ended when he was sacked in December 1986 by the Soviet leader Mikhail Gorbachev. Mr Kunayev was replaced by an ethnic Russian experienced in fighting corruption, Gennady Kolbin. Fearing a return to Russian domination, thousands of young Kazakhs demonstrated on the streets of the then capital, Alma-Ata (now Almaty), provoking a violent crackdown by the Soviet authorities.

Nursultan Nazarbayev, an ethnic Kazakh, replaced Mr Kolbin in 1989. Fearing a backlash from the large Russian minority, and recognising the republic!s economic dependence on Russia, Mr Nazarbayev opposed independence. In a fraudulent referendum in March 1991, the vote came out overwhelmingly in favour of remaining part of the Soviet Union. However, Kazakhstan found itself involuntarily cast adrift when Russia, Belarus and Ukraine left the Soviet Union to form the Commonwealth of Independent States (CIS) on December 8th 1991. On December 16th 1991 Kazakhstan became the last republic to leave the Soviet Union, having been one of the last to make its local language the official state language. Mr Nazarbayev was the only candidate in the first presidential election, held in December 1991, and he won 95% of the vote"a result reminiscent of elections during the Soviet period.

Recent political developments

Since Kazakhstan became independent in 1991 Mr Nazarbayev!s main objective has been to retain power. As part of this strategy he has been careful to distance himself from specific policies, and has used the office of the prime minister as a focus for public discontent. The first prime ministers of independent Kazakhstan were thus blamed for unpopular or unsuccessful policies: Sergei Tereshchenko was removed in October 1994, Akezhan Kazhegeldin in October 1997 and Nurlan Balgimbayev in October 1999. The then foreign minister, Kasymzhomart Tokayev, succeeded Mr Balgimbayev only to be demoted back to foreign minister in January 2002.

While still prime minister, Mr Tokayev had been weakened by a fracturing of the cabinet in November 2001 during which a reformist faction formed a new political party, the Democratic Choice of Kazakhstan (DVK). The ministers who formed the DVK not only wanted a less centralised system of government, but also seem to have wanted to undermine Mr Tokayev, who at the time looked like a possible successor to Mr Nazarbayev. Since then Mr Nazarbayev has appointed prime ministers who have been loyal and whose main task has been to contain conflicts within the elite while repressing the opposition. Mr Tokayev was replaced in January 2002 by Imangali Tasmagambetov, whose administration sent prominent opposition politicians from the DVK to jail, following trials of dubious fairness.

Kazakhstan is at first reluctant to leave the Soviet Union

Prime ministers take the blame for policy failures

6 Kazakhstan

Country Profile 2006 www.eiu.com © The Economist Intelligence Unit Limited 2006

Under Mr Tasmagambetov, the taboo against public discussion of corruption in the elite was enforced with great vigour, and independent journalists were harassed. Mr Tasmagambetov also introduced a highly restrictive law on political parties that aimed to prevent most opposition movements from even registering, let alone competing in elections. The June 2002 law made onerous demands that in order to register a party had to have at least 50,000 members (the previous level required was 3,000), with a minimum of 700 members in each of Kazakhstan!s 14 provinces"including the Astana and Almaty regions. Parties also had to have contested two successive legislative elections.

However, Mr Tasmagambetov!s loyalty did not guarantee effectiveness, and the then prime minister mishandled relations with Kazakhstan!s parliament"despite this body!s being dominated by Nazarbayev supporters. As a result, he was replaced in June 2003 by another Nazarbayev loyalist, Danial Akhmetov. Under Mr Akhmetov the government has rhetorically begun to advocate opening up the political system, but in practice repression of dissent has been stepped up. The main aim of official politics during 2004 was to clamp down on the media and ensure that pro-government parties won the election to the lower house of parliament, the Majilis. Mr Akhmetov!s attempt to bring in a restrictive media code failed following considerable foreign pressure and domestic criticism. The authorities instead resorted to indirect methods, such as libel suits in the government-controlled courts and tax investigations to curb the press.

The election to the Majilis in September and October 2004 was neither free nor fair. In an attempt to create the semblance of a contested election, the authorities formed ten electoral blocs, all of which supported Mr Nazarbayev. The opposition formed two electoral blocs, the Ak Zhol (Bright Path) party, led by moderate former officials, and a bloc that brought together the more radical DVK and the Communist Party of Kazakhstan (KPK). Although the authorities had, under foreign pressure, allowed the DVK and the KPK to contest the election, a government-controlled court banned the DVK in December 2004 after it called for civil disobedience in the event of electoral manipulation. The opposition managed to gain just one seat for the Ak Zhol party. The extent of electoral manipulation proved too much for the outgoing Majilis speaker, Zharmakhan Tuyakbay, a member of the main pro-presidential party, Otan. Mr Tuyakbay resigned all his official positions in protest against the electoral fraud, and joined the opposition.

Politics in 2005 was dominated by the need to secure Mr Nazarbayev!s re-election in an atmosphere of considerable tension. On the external front the changes of leadership in Ukraine in December 2004 and in the Kyrgyz Republic in March 2005 created considerable nervousness in Central Asia. Partly in response to these events, Mr Nazarbayev took steps to buy off any potential popular unrest, most notably through large increases in public-sector wages, student stipends and pensions.

The government resorted to other tried-and-tested tactics to prevent the opposition from mounting a credible challenge and to make the president!s re-election a formality. The authorities co-opted some members of the opposition

Clamping down on opposition is the current priority

Parliamentary election in 2004 is flawed

December 2005 secures another resounding re-election

Kazakhstan 7

© The Economist Intelligence Unit Limited 2006 www.eiu.com Country Profile 2006

into the government and, through a Constitutional Council ruling, brought the presidential election forward from the originally scheduled date of December 2006 to December 2005 on the basis of a constitutional ambiguity. The length of the presidential term is set at seven years by article 41 of the constitution. Article 41 thus meant that Mr Nazarbayev!s term ended in January 2006. However, article 94 of the constitution states that presidential elections are to be held on the first Sunday of December after the expiration of the presidential term. This would have meant December 2006, in effect giving Mr Nazarbayev almost another year in office.

The administration presumably decided that holding the election at the end of 2005 carried fewer risks to Mr Nazarbayev!s position than waiting until the end of 2006. The election was duly brought forward, and Mr Nazarbayev secured an overwhelming victory of 91%, although international observers viewed the election as flawed. His only significant rival, Mr Tuyakbay, suffered considerable personal harassment during his campaign and in the event obtained a marginal share of the vote.

Presidential election results, Dec 4th 2005 (% of total)

Nursultan Nazarbayev 91.15

Zharmakhan Tuyakbay 6.61Alikhan Baymenov 1.61Yerasil Abylkasymov 0.34

Mels Yeleusov 0.28

Source: Central Electoral Commission.

Important recent events

April-August 1995

Two flawed referendums result in the cancellation of the presidential election planned for 1996 (keeping Nursultan Nazarbayev in power until December 2000) and the approval of a new authoritarian constitution, which received 89% of the vote.

October 1998

Parliament moves the presidential election forward by one year, to January 1999, and extends the presidential term from five to seven years.

January 1999

Mr Nazarbayev is re-elected with 80% of the vote.

October 1999

Mr Nazarbayev!s supporters win the parliamentary election, which is heavily criticised by international monitors.

November 2001

The formation of a new political movement within the government, the Democratic Choice of Kazakhstan (DVK), causes a political crisis.

March-May 2002

The government crushes the DVK, arresting its leaders and forcing it to split. Independent media outlets also come under attack. The government is forced to

8 Kazakhstan

Country Profile 2006 www.eiu.com © The Economist Intelligence Unit Limited 2006

admit that Mr Nazarbayev held US$1bn in Swiss bank accounts, although it claims that the money has been repatriated.

July 2002

Mr Nazarbayev signs into effect a new law on political parties that would close down most opposition movements, and the DVK!s two most prominent leaders are sentenced to prison on charges of corruption and abuse of office.

March 2004

During pre-trial hearings in the US concerning a corruption scandal over 1990s oil deals, Mr Nazarbayev is formally named as one of the officials to whom a US businessman, James Giffen, is charged with making illegal payments.

September/October 2004

Kazakhstan holds a flawed parliamentary election in which the opposition manages to win just one out of 77 seats.

November 2005

A prominent opposition figure, Zamanbek Nurkadilov, is found dead in his home in Almaty, the former capital. The official verdict is suicide but his widow and the opposition claim foul play.

December 2005

A flawed presidential election delivers a 91% victory for Mr Nazarbayev.

February 2006

Another opposition leader, Altynbek Sarsenbayev, is found dead. The politician, his bodyguard and his driver had been executed outside Almaty. The deaths were almost immediately blamed on Yerzhan Utembayev, chief of staff of the speaker of the Senate (the upper house of parliament), Nurtay Abykayev.

July 2006

The two main pro-presidential parties, Otan (Fatherland, headed by Mr Nazarbayev) and Asar (All Together; led by the president!s daughter Dariga Nazarbayeva) agree to merge.

Within Kazakhstan, top-level corruption is a taboo issue and the government launched a furious campaign of harassment in response to opposition publications and TV stations reporting foreign coverage of corruption allegations in Kazakhstan during 2002. To an extent the government has been its own worst enemy on the corruption issue, and its attempt to use charges of corruption against its enemies has backfired. In 1997-98 the government claimed that former prime minister Mr Kazhegeldin, who quarrelled with Mr Nazarbayev and went into exile, had property in Belgium and Swiss bank accounts. This prompted an investigation in both countries concerned, contributing to the unfolding of a scandal involving allegations of bribery surrounding several major oil deals between Kazakhstan and US companies in the mid-1990s.

When Mr Tasmagambetov became prime minister one of his main priorities was to deal with the possible effects of the scandal. He oversaw a harsh crackdown on dissent and the harassment of any independent media that discussed the corruption allegations. Despite this, in April 2002 he was forced

Corruption causes unease in government circles

Kazakhstan 9

© The Economist Intelligence Unit Limited 2006 www.eiu.com Country Profile 2006

to admit publicly that the government had indeed kept money in Swiss bank accounts in the mid-1990s, arguing that the accounts had been opened as an emergency fund in case of economic shocks.

"Kazakhgate"

A corruption scandal surrounding oil deals in the mid-1990s, widely referred to as "Kazakhgate", has dogged the government since it began in 1998, and in 2003 it resulted in the jailing of a US businessman, James Giffen, who runs a New York-based firm called Mercator Corporation. Mr Giffen has been indicted under the US Foreign Corrupt Practices Act (FCPA). The US government alleges that in the mid-1990s Mr Giffen paid US$78m in bribes to two high-ranking Kazakh officials in order to secure oil deals in the country. The US has also charged Mr Giffen with tax fraud. The two Kazakh officials in the case were initially only referred to as KO1 and KO2, but in March 2004 they were named as the president of Kazakhstan, Nursultan Nazarbayev, and a former prime minister, Nurlan Balgimbayev. Mr Nazarbayev has denied all connection to the case, describing the bribery allegations as "an insinuation, a provocation and a set-up". One former executive of the US oil company Mobil (now ExxonMobil), J Bryan Williams, pleaded guilty to tax evasion in New York in September 2003 and received a sentence of three years and ten months in prison. He was also ordered to pay a fine of US$25,000 and an additional US$3.5m in tax. Mr Williams had received a US$7m payment for helping to insert Mobil into Tengizchevroil (TCO)"the joint venture led by the US!s Chevron that is exploiting the giant onshore Tengiz and Korolev fields in western Kazakhstan"of which US$2m was reported to have come from the government of Kazakhstan. ExxonMobil has denied knowledge of the illegal payments. Mr Williams first began receiving payments in 1993 and worked for Mobil until 1998.

Mr Nazarbayev has proved relatively tolerant of moderate nationalist groups representing Kazakhstan!s large Russian minority (30% of the population in 2001), despite a programme of "Kazakhisation" that the government launched in the initial post-independence period"which removed Russians from many important posts. Since 1994 this nationalist drive has been curbed, in part because of criticism from both Russia and the US but also because of the loss of skilled workers"most of whom are ethnic Russians. Attempts to encourage learning of the Kazakh language have been consistently scaled back. For instance, whereas Kazakhstan!s 1993 constitution established Kazakh as the official state language, relegated Russian to the status of a "language of inter-ethnic communication""the second official language"and defined Kazakhstan as an ethnic state, the 1995 constitution dropped its predecessor!s definition of the country as a Kazakh state.

Constitution, institutions and administration

Kazakhstan has had two constitutions since independence. The first, approved in January 1993, accorded the president wide-ranging powers. The second constitution, approved in August 1995, entrenched the president!s dominance, notably by abolishing the post of vice-president. In October 1998 parliament further strengthened Mr Nazarbayev!s hold on power. With only one vote

Inter-ethnic relations have been calm

Presidential power is enshrined in the constitution

10 Kazakhstan

Country Profile 2006 www.eiu.com © The Economist Intelligence Unit Limited 2006

against, it abolished the maximum age limit and the two-term limit for the presidency, and extended the presidential term of office from five to seven years. Mr Nazarbayev can now stay in power indefinitely. To deter opposition groups from boycotting elections, parliament also abolished the requirement for a minimum 50% turnout to make elections valid.

On paper, the constitution guarantees full human rights, freedom of conscience and social justice. In practice, however, civil rights remain fragile. Organised opposition groups face constant pressure from the security forces. Both the police and the judiciary are corrupt and subject to political interference. The president has personally appointed a Constitutional Council to replace the more independent Constitutional Court. Corporate law remains poorly developed and enforced.

Four important institutions exist in Kazakhstan: the presidency, the cabinet, the National Bank of Kazakhstan (NBK, the central bank) and the Committee for National Security (KNB, the successor to the KGB). Compared with other institutions, the NBK enjoys a high degree of respect, mainly as a result of its successful fight against inflation and its attempts to stabilise the economy in the aftermath of the August 1998 financial crisis in Russia. The NBK was led by Grigory Marchenko, a well-regarded reformer (see Economic sectors: Financial services), until January 2004, when he was replaced by his deputy, Anvar Saidenov. The security forces, led by the KNB, curb political opposition through legal harassment and occasional violence and imprisonment.

The presidency is the most powerful of these bodies. Mr Nazarbayev dictates policy, even though officially policy implementation is the responsibility of the government and its ministries. They in turn face little opposition in pushing legislation through a parliament lacking any real power. The presidential administration also deals with most major foreign investments and foreign policy issues. Weak administration and corruption have hampered the implementation of reforms. Administrative reform is unlikely because corruption plays an important role in maintaining the cohesion of the political elite in Kazakhstan.

Political forces

The key political force in Kazakhstan is the president, Mr Nazarbayev, and his closest advisors. The president!s inner circle tends to change, but few dare to question his authority or his position. Mr Nazarbayev is treated as being above politics or criticism, and any personal attacks on him or his integrity are generally not tolerated. As most real politics in Kazakhstan occurs behind closed doors, it is hard to delineate who the key forces within Mr Nazarbayev!s circle are. An important figure within the presidential entourage is the speaker of the Senate (the upper house of parliament), Nurtay Abykayev. Mr Abykayev is a vital figure in Kazakhstan!s political arrangement because, as Senate speaker, he is constitutionally next in line to take over the president!s functions in the event that Mr Nazarbayev were suddenly incapacitated. Various members of Mr Nazarbayev!s family also hold positions of great influence.

Policymaking rests with the president

President is the main political force

Kazakhstan 11

© The Economist Intelligence Unit Limited 2006 www.eiu.com Country Profile 2006

The emergence of several pro-presidential parties in recent years nonetheless suggests that conflicts within the elite have increased. Mr Nazarbayev usually attempts to restrain such tensions by ensuring that those who are forced to leave government"whether owing to personality clashes or poor performance"have a continued career in business or as advisors. However, the problem for Mr Nazarbayev is that although none are questioning his position, many are jostling to position themselves for the eventual succession. Furthermore, although the chances of a strictly dynastic succession in Kazakhstan have diminished, such a move cannot be ruled out altogether.

The political fortunes of the president!s eldest daughter, Dariga Nazarbayeva, have waxed and waned in recent years. Ms Nazarbayeva entered politics in October 2003 when she launched the Asar (All Together) party. Despite the considerable restrictions on registering political parties laid out in the 2002 law on political parties, Asar apparently managed to sign up 172,000 members before its founding congress in February 2004. The opposition devoted considerable attention to thwarting Ms Nazarbayeva during the 2004 election to the lower house of parliament, the Majilis. However, Asar proved to have less backing than observers initially thought, obtaining four seats in parliament. Instead, the main pro-presidential party, Otan (Fatherland), increased its representation in the 77-seat Majilis from 24 seats to 42 seats.

Ms Nazarbayeva!s husband, Rakhat Aliyev, has also had mixed fortunes in recent years. In November 2001 he was forced to resign as deputy head of the KNB, after parliament reportedly turned against him. Mr Aliyev was then appointed Kazakhstan!s ambassador to Austria. However, after some three years in Austria, he was brought back to become first deputy foreign minister in July 2005, suggesting he was back in favour.

The fortunes of this faction nonetheless appeared to take another turn for the worse after Ms Nazarbayeva publicly called for Mr Abykayev!s resignation in the wake of the murder of a prominent opposition figure. This attack on a figure so close to the president was indicative of factional jockeying for position within the elite: Mr Abykayev reportedly has links to another powerful faction, centred on Mr Nazarbayev!s other son-in-law, Timur Kulibayev"first vice-president of the state-owned oil and gas company, Kazmunaigaz. Mr Kulibayev!s support in the oil industry gives him considerable leverage over politics, and he is also considered a strong contender for the eventual succession.

Factional in-fighting was also at play in a government campaign to introduce a new media law and strengthen state control over media outlets, which was widely seen as targeting Ms Nazarbayeva!s holding in the Khabar TV and radio agency. Mz Nazarbayeva suffered a further setback in July 2006, when the two main pro-presidential parties, Otan and Asar, agreed to unite. Although the move was portrayed as a merger by both parties"and was ostensibly mooted by Asar"it more closely resembles the absorption by the president!s party of that of his daughter. Although Ms Nazarbayeva will be a deputy leader of the new party, the president will continue to head it and senior Otan figures will retain their prominent roles. In one respect the merger could be seen as Ms Nazarbayeva!s "return to the fold" following her recent criticisms of figures close to the

President's family all seek to succeed him

12 Kazakhstan

Country Profile 2006 www.eiu.com © The Economist Intelligence Unit Limited 2006

president. However, it could also be a blow to her hopes of succeeding her father, as it removes her independent political base.

Kazakhstan!s political parties, whether pro-government or opposition, have little impact on politics and have questionable membership rolls. Pro-Nazarbayev parties claim to have combined memberships of close to 1m members. The main political party, Otan, boasts membership of 300,000; following its absorption of Asar it will claim a membership of over half a million. For comparison, in the UK"a country with a population four times that of Kazakhstan"the two largest political parties have memberships of around 350,000. Other pro-Nazarbayev parties also claim very high membership. The Party of Patriots of Kazakhstan"which won no parliamentary seats"claims 170,000 members. The Aul (Village) Social Democratic Party of Kazakhstan claims 150,000 members, and the Ruhaniyat (Spirituality) Party claims 75,000 members. Yet despite their large claimed membership, neither Aul nor Ruhaniyat won any seats in the Majilis. By contrast, the electoral bloc of the pro-government Agrarian Party and the Civic Party, known as the AIST bloc, won the second-largest number of seats, despite being largely unknown.

Majilis election, Sep 19th and Oct 3rd 2004 (turnout 56.49%)

Party Constituency seats PR seats Total seatsPro-government Otan Party 35 7 42AIST bloc 10 1 11Asar Party 3 1 4Democratic Party 1 0 1Independents 18 0 18

Opposition Ak Zhol 0 1 1

Source: Central Electoral Commission.

The authorities have proved themselves adept at breaking up and neutralising opposition parties. Within months of its formation the DVK split in two, with a less radical faction led by Uraz Dzhandosov"a former first deputy prime minister and noted economic reformer"breaking off to become the Ak Zhol (Bright Path) party. Then, in April 2005, Mr Dzhandosov and others split away from Ak Zhol to form Nagyz Ak Zhol (True Bright Path). Although the opposition now contains a number of talented and highly capable former government officials, it is ineffective, poorly funded and"whenever it coalesces"subject to legal pressure and occasional physical harassment. Previous opposition parties formed by disgruntled officials, such as Azamat (Citizenship), have split and failed in the past.

The longest-standing opposition party is the Communist Party of Kazakhstan (KPK). The government encouraged a split in the KPK during 2004 to prevent the party from becoming a viable opposition force. Partly as a result of this, the KPK"in principle a long-standing opponent of a liberal reform agenda"formed an electoral alliance with the DVK. This bloc was subject to considerable official harassment and failed to gain a single seat.

Party membership rolls are suspect

Opposition has lacked cohesiveness

Kazakhstan 13

© The Economist Intelligence Unit Limited 2006 www.eiu.com Country Profile 2006

Attempts to create a broad opposition front have repeatedly failed. The opposition!s most recent attempt to coalesce was in forming an umbrella movement under the name "For a Fair Kazakhstan""bringing together Nagyz Ak Zhol, the now banned DVK and the KPK"in order to support Mr Tuyakbay as its candidate against Mr Nazarbayev in the 2005 presidential election. A new party, Alga! (Forward!), was founded in August 2005 by former members of the DVK, but this party was denied formal registration in 2006.

Two prominent opposition leaders, Zamanbek Nurkadilov and Altynbek Sarsenbayev, died violently shortly after one another, fuelling speculation that the deaths were organised by state officials at the highest level. In November 2005 Mr Nurkadilov was found dead from gunshot wounds in his home in Almaty, the former capital, and the official verdict was suicide. Mr Sarsenbayev, however, was clearly murdered, together with his driver and bodyguard"in February 2006 the bodies were found shot dead outside Almaty with their hands tied behind their backs. The official investigation concluded that Mr Abykayev!s chief of staff, Yerzhan Utembayev, had ordered the killing as a personal revenge over an insult. The official explanation that Mr Sarsenbayev was killed by rogue officials for personal reasons failed to satisfy the opposition, which found the authorities overly keen to wrap up the Sarsenbayev case.

There are small numbers of extremists, Russian nationalists, Kazakh nationalists and Islamic fundamentalists. These groups are marginal and are under government surveillance. A small number of Kazakh citizens have joined al-Qaida, and have been involved in terrorist attacks in neighbouring Uzbekistan and fought with al-Qaida in Afghanistan. There is no popular basis for Islamic fundamentalism outside of the small, poor, rural ethnic Kazakh communities in southern Kazakhstan.

Main political figures

Nursultan Nazarbayev

The president, Mr Nazarbayev, originally came to power in 1989 as the first secretary of the Communist Party of the Kazakh Soviet Socialist Republic. He is adept at keeping disparate ethnic groups in balance, and has allowed a measure of economic reform, as well as considerable foreign investment. However, corrupt practices have flourished under his administration. In 1999 it was revealed that Mr Nazarbayev had a Swiss bank account, and in 2000 a series of offshore companies were also discovered to be under his control. Mr Nazarbayev is an erratic administrator who has failed to implement a number of structural economic changes. Although there is evidence of elite discontent with his rule, Mr Nazarbayev remains in command.

Dariga Nazarbayeva

Ms Nazarbayeva is the eldest of the president!s three daughters. With a background in the media since 1994, she has a significant holding in the principal TV and radio agency in Kazakhstan, Khabar, and is president of the Eurasian Centre for Strategic Research. These media connections, and extensive charity work, have given her a high public profile and a political influence disproportionate to her official

Radical parties are small and weak

Opposition suffers major blows

14 Kazakhstan

Country Profile 2006 www.eiu.com © The Economist Intelligence Unit Limited 2006

responsibilities. Ms Nazarbayeva made a late entry into active politics in October 2003, when she formed a pro-presidential party, Asar. The party performed worse than expected in the election to the Majilis (the lower house of parliament) in 2004, and in 2006 it was merged into the president!s party, Otan. Her husband, Rakhat Aliyev, fell from favour in November 2001 and was appointed ambassador to Austria, although in July 2005 he was brought back to Kazakhstan and given a new post in the government.

Danial Akhmetov

Mr Akhmetov was appointed prime minister in June 2003. Originally from Pavlodar, he is a long-standing ally of Mr Nazarbayev. Mr Akhmetov was governor of Pavlodar province in 1993-97, after which he was transferred to the governorship of the Northern Kazakhstan province. He was then deputy prime minister until 2001, when he was sent back to Pavlodar to tighten control over the region, which had become a focus of dissent against the government. Following Mr Akhmetov!s appointment there were few signs of further unrest in the region.

Nurtay Abykayev

Mr Abykayev has been Mr Nazarbayev!s right-hand man since the latter came to power in 1989. He was chief of Mr Nazarbayev!s staff from 1989 to 1995, and was appointed as Kazakhstan!s first ambassador to the UK in 1995. In 1996 he returned to the presidential administration, and was head of the National Security Committee (KNB) in 1998-2000. In 2000 he became deputy foreign minister, before being made speaker of the Senate (the upper house of parliament) in 2004. He is widely considered to be Mr Nazarbayev!s closest ally, and according to the constitution he would take over in the event of the president!s sudden incapacity.

Galymzhan Zhakiyanov

Governor of Pavlodar region until Mr Nazarbayev dismissed him in November 2001 after he helped to found the Democratic Choice of Kazakhstan (DVK), Mr Zhakiyanov is currently serving a seven-year prison term following a flawed trial in July-August 2002. In August 2004 he was moved from prison into house arrest, after repeated domestic and international demands for his release"particularly in view of the fact that he has a long-standing heart condition and suffered a heart attack while in prison. He was released in January 2006, after the presidential election, and could play a key role in keeping the increasingly besieged opposition parties together. However, it remains to be seen whether his time in prison has weakened him personally or diminished his leadership skills

International relations and defence

Mr Nazarbayev makes the key decisions over foreign policy, and the rhetorical priority in foreign relations is regional co-operation schemes. Mr Nazarbayev has ceaselessly championed integration of the former Soviet republics as well as regional co-operation and free trade in Central Asia. In reality, however, such schemes have proved ineffective, serving only to divert some categories of trade through tariff distortions. Similarly, Mr Nazarbayev!s desire to reconstruct the economic space of the former Soviet Union has also failed.

Regional co-operation plans have largely failed

Kazakhstan 15

© The Economist Intelligence Unit Limited 2006 www.eiu.com Country Profile 2006

The Commonwealth of Independent States (CIS) customs union (comprising Kazakhstan, the Kyrgyz Republic, Tajikistan, Belarus and Russia) was renamed the Eurasian Economic Community (Eurasec) in October 2000, with the aim of creating a more formal economic bloc between some former Soviet republics. In reality, Eurasec is not proving any more effective than its predecessor, which served only to insulate exporters from tackling hard-currency markets and encourage them to buy some inputs at higher prices than might be available without the customs union!s external tariff. Indeed, the new grouping gives more weight to Russia"with four votes out of ten, compared with its equal footing in the customs union. For Kazakhstan, which is now largely a crude oil exporter, Eurasec is of little relevance, as most Kazakh oil is sold to hard-currency markets.

Kazakhstan is also a member of the Central Asian Economic Community, which was renamed the Central Asian Co-operation Organisation (CACO) in January 2002, in an attempt to give the grouping renewed impetus. However, in reality it scarcely functions. The CACO is the latest in a line of failed attempts at regional co-operation in Central Asia. The fundamental sticking-points are the lack of complementarity between the Central Asian economies and Uzbekistan!s desire to be the regional leader"which Kazakhstan has consistently resisted. Bilateral tensions over the poorly demarcated border with Uzbekistan flared in 2000 but have broadly been resolved, and the two sides are now working jointly to delineate the border. Suspicions between the two countries, however, remain.

Kazakhstan!s main external ally and security guarantor is Russia. Despite some early tensions over the treatment of the Russian minority in Kazakhstan, relations are good"and to an extent facilitated Kazakhstan!s decision to assist the US in the counter-terrorism operations that followed the attacks on the US in September 2001. Kazakhstan has offered the US overflight rights and the right to land aircraft in Kazakhstan for counter-terrorism operations. The US is giving Kazakhstan increased military assistance"although the amount is insignificant. Kazakhstan was quick to co-operate in part to avoid being upstaged by Uzbekistan, which is strategically better placed. Kazakhstan has hinted that it might withdraw its support in the light of ongoing corruption investigations in the US, but this appears unlikely. Kazakhstan, like Russia, has been a substantial beneficiary of the US defeat of the Taliban in Afghanistan in late 2001, and has an interest in maintaining good relations with the US.

After independence the government had been initially uneasy about China!s long-term intentions in Central Asia, but in 1995 Kazakhstan joined a regional anti-terrorism grouping including Russia and China"that has since been renamed the Shanghai Co-operation Organisation (SCO)"to co-ordinate anti-Islamist and anti-separatist activities. The government is now actively encouraging Chinese investment in the oil sector, in part to decrease its dependence on large Western oil firms. In May 2004 Mr Nazarbayev and his Chinese counterpart, Hu Jintao, signed an agreement on the construction of a 1,240-km pipeline from Atasu in central Kazakhstan to Xinjiang, the Chinese

Relations with Russia are far closer than ties to the US

Relations with China improve

16 Kazakhstan

Country Profile 2006 www.eiu.com © The Economist Intelligence Unit Limited 2006

region that lies on Kazakhstan!s eastern border. China!s role in the Kazakh oil sector has since expanded slowly but steadily.

Kazakhstan inherited a large but crumbling Soviet arsenal and considerable armed forces, including nuclear weapons. However, Kazakhstan was a nuclear power in name only. These nuclear weapons were in practice under full Russian control and by April 1995 were withdrawn from the country, with Kazakhstan co-operating fully in its own disarmament. The army is poorly organised, badly equipped and inefficiently led. Few Kazakhs held commissions in the Soviet armed forces, being instead mostly assigned to unarmed construction battalions. Recognising the state of its defences, the government wants to increase defence spending, and in both 2001 and 2002 defence expenditure was raised to 1% of GDP. Spending on public order is around twice this level.

The Soviet government had moved many of its weapons to Kazakhstan to avoid the limits imposed by the 1990 Conventional Forces in Europe (CFE) treaty. In particular, Kazakhstan inherited a well-equipped air force. Kazakhstan!s air force has 164 combat aircraft, including 43 MiG-31s and 40 MiG-29s. Average annual flying time is 100 hours, half of the NATO minimum, compared with just 25 hours a year in 1999. Another 75 combat aircraft are in storage. According to the International Institute for Strategic Studies (IISS), Kazakhstan also has 650 T-72 tanks and 280 T-62s. The navy has 15 fighting vessels in the Caspian Sea.

Defence forces, 2006 (no of troops)

Total military 65,800 Army 46,800 Air force 19,000Paramilitary 34,500 Internal Security Troops (under interior ministry control) 20,000 Border Guards (under Interior Ministry control) 12,000 Marine Border Guards 3,000 Presidential Guard 2,000 Government Guard 500

Source: International Institute for Strategic Studies, The Military Balance, 2005/2006.

Security risk

Armed conflict

After independence, Kazakhstan moved quickly to settle the border dispute with China and has sought to demarcate its borders with its former Soviet neighbours (Russia, the Kyrgyz Republic, Turkmenistan and Uzbekistan). There was some tension in relations with Uzbekistan following Uzbek attempts to mark the frontier unilaterally, but in September 2002 a final delimitation deal was signed between the two countries. Nevertheless, there could be some skirmishes along the Uzbek-Kazakh border, where local inhabitants disagree with the official partition. The dispute over the legal status of the Caspian Sea is unlikely to lead to armed conflict involving Kazakhstan, given that the country has settled its claims on the Caspian with Russia and Azerbaijan. Iran has threatened the use of force against Azerbaijan to assert its claims in the Caspian, but any such conflict is unlikely to draw in Kazakhstan.

Armed forces are under-resourced

Kazakhstan 17

© The Economist Intelligence Unit Limited 2006 www.eiu.com Country Profile 2006

Terrorism

There is little risk of domestic terrorism. Although there has been some Islamist activity in southern Kazakhstan, there is little threat of local Islamists turning violent. The majority of Kazakhs are secular, and opposition to the government is mostly peaceful. The rapid US and Afghan defeat of the Taliban regime in Afghanistan and the weakening of the Islamic Movement of Uzbekistan (IMU)"the main insurgent group in former Soviet Central Asia"have reduced the danger of Islamist terrorism in Kazakhstan and the region. The government presents the spread of Islamic extremism as the main security threat in the region, but this is largely a justification for increasingly harsh measures against domestic political dissent.

Civil unrest

There is little serious civil unrest, largely because of the effectiveness of the secret police and the government!s success in keeping the vast majority of the population isolated from the political process. As a consequence, although demonstrations sometimes take place in protest against specific issues"such as pension arrears, for example"they tend to be localised and short-lived. The government does not hesitate to use the police against dissenters, and is generally quite effective in its harassment of opposition figures and activists who are deemed to be too prominent.

Crime

Although there are no reliable statistics on petty crime, foreign visitors have often been the victims of robberies, especially on road and rail transport. However, in the large urban centres, Astana and Almaty, rising economic prosperity appears to have lessened the risks specific to foreigners. Some precautions are still advisable: there have been several instances where foreigners have been met at the airport by someone purporting to have been sent to meet them and subsequently robbed"showing that passenger lists are not always kept confidential. The police are ineffective and in some cases involved with the criminals. The extortion of bribes from motorists is commonplace.

Drug smuggling and organised crime

Kazakhstan!s location as a transit point from Central Asia to Russia, as well as its long and often open borders, make it an ideal transit point for drug smugglers and people traffickers. The ineffectiveness of the police and customs service at preventing the abuse of Kazakh territory for such criminal enterprises contrasts with their zealous application of trade regulations and surveillance"and the regular stopping of vehicles carrying legitimate goods. The security services have ensured that organised crime has steered well clear of attempting to gain a foothold in the oil and gas sector, which is the domain of the ruling elite.

Resources and infrastructure

Population

Kazakhstan had a population density of just 5.6 inhabitants per sq km at the beginning of 2006. Most of the population lives in the north-east and south-east, whereas the central and western provinces"the latter being where most oilfields are located"are sparsely populated. According to the 1999 census, Kazakhstan!s population was 14.9m, and had fallen by around 1% annually since the previous census in 1989. However, after two more years of decline, the

Population is on a trend of decline

18 Kazakhstan

Country Profile 2006 www.eiu.com © The Economist Intelligence Unit Limited 2006

population started to grow again as of 2002, reaching 15.2m at the start of 2006, 1% higher than a year earlier.

One principal reason for the decline in population that Kazakhstan experienced over the 1990s was emigration. Between 1989 and 1999 the ethnic Russian population fell by 1.5m, and 500,000 ethnic Germans"more than half of the ethnic German population"also left Kazakhstan. As a result of their higher birth rate and the mass emigration of minorities, by 1999 ethnic Kazakhs had become a majority in the country for the first time since the 1920s. Years of strong economic growth since 2000 have reversed migratory trends in Kazakhstan, and net migration turned positive for the first time in 2004. Kazakhstan is attracting migrants from its poorer neighbours in Central Asia and from China. Net migration has turned strongly positive in 2005, thanks to large scale immigration from Uzbekistan. Departures for Russia have slowed considerably.

Net migration (no. of people, year-end)

1999 -8,3002000 -7,3002001 -5,900

2002 -4,2002003 -8,300

2004 2,8002005 22,668

Source: Statistics Agency of the Republic of Kazakhstan.

Also as a result of past emigration, the overall proportion of the population aged over 60 is relatively low, at around 10%, since the average age of ethnic Kazakhs is much younger than that of other nationalities in the republic. Consequently, roughly three times as many ethnic Kazakhs are entering the workforce as are leaving it. Nevertheless, ethnic Kazakhs"with larger and younger families"are the most likely to suffer from poverty in Kazakhstan. This is partly because ethnic Kazakhs often live in rural areas, predominantly in the south, whereas ethnic Russians prevail in the industrialised north. The poorest area is the mainly ethnic Kazakh province of southern Kazakhstan, with the lowest per-capita income in 2005"half that of the national average and one-fifth that of the wealthiest province, oil-rich Atyrau. Poverty has nevertheless declined fairly rapidly in recent years, owing to rapid real GDP growth. According to the Statistics Agency of the Republic of Kazakhstan (SARK), the share of the population living below the poverty line (US$35/month) has fallen from over 28% in 2001 to below 10% in 2005.

Education

Russians and other ethnic minorities in Kazakhstan dominated science and technology studies during the Soviet period, and since independence their mass emigration has depleted Kazakhstan!s skills base. Literacy remains high, at 97.5%, according to the 1999 census (the latest available data), with the World Bank putting the literacy rate among the population aged over 15 at 99.5%. The number of students enrolled in higher education has risen steadily from

Post-Soviet educational system is in decline

Kazakh population is young

Kazakhstan 19

© The Economist Intelligence Unit Limited 2006 www.eiu.com Country Profile 2006

440,700 in 2000/01 to 747,100 in 2004/05. However, in primary education the situation appears to be deteriorating, with the number of pupils enrolled in day schools falling from 3.2m in 2000/01 to just under 3m in 2004/05. Moreover, educational standards are declining, owing in part to a lack of resources. Spending on education was 3.5% of GDP in 2005, compared with 3.9% of GDP in 1999. The president, Nursultan Nazarbayev, has made repeated calls in recent years for increased state investment in education.

Some private educational establishments have been set up, to an extent filling the gaps created by the deterioration in the public system. However, even though private education has seen a steady increase"growing from 137 establishments in 1996 to 521 in 2004"the sector is still insignificant, accounting for only just over 5% of all educational establishments in 2004, and taking in less than 10% of all students. Nevertheless, the higher quality of private-sector secondary education compared with the state system is clear from the fact that enrolment in private institutions increases with the level of education. Whereas private primary schools take in only around 7% of all schoolchildren, private higher education establishments account for 46% of the student population at that level.

Health

As with education, the quality of healthcare provision declined sharply after independence, owing to a reduction in funding and the emigration of many doctors and specialists. However, Kazakhstan!s main health indicators appear to suggest that the sector turned the corner in 2000, and have shown small but steady improvements since then. The number of doctors per 10,000 inhabitants recovered from 49 in 2000 to nearly 55 in 2004, and the number of hospital beds per 10,000 inhabitants has been stable at 77 in 2004-05 after falling to 72 in 2000. That the health sector is still underfunded is nevertheless evident in the fact that the government spent around 2.5% of GDP on healthcare in 2005, compared with an OECD average of over 7%. The effects of the oil boom have yet to be felt in the healthcare sector.

Officially, healthcare is provided free of charge and on the basis of need. However, given the shortage of resources, in practice"as elsewhere in Central Asia"a bribe helps to jump the queue and secure better treatment. Financial constraints are also causing a shift away from expensive in-patient care in hospitals towards out-patient care. The government is trying to bring in a system of compulsory health insurance, but this will only have an effect in the medium term. In the meantime the state-run health service is struggling to afford imported medical supplies. Money in the healthcare system tends to be spent on wages, at the expense of new equipment.

Some aspects of public health provision have collapsed, resulting in small outbreaks of typhoid, cholera and diphtheria. The situation is particularly worrying in the south of the country, where poor living conditions and the lack of funding for rural healthcare have led to a spread of tuberculosis. This disease is also a severe problem in Kazakhstan!s prisons. A serious public health issue concerns the environmentally degraded region surrounding the shrinking Aral

Health provision is improving slowly

Diseases and radiation are serious health risks

20 Kazakhstan

Country Profile 2006 www.eiu.com © The Economist Intelligence Unit Limited 2006

Sea, where the life expectancy of the population is lower than in most other areas of Kazakhstan and where pulmonary problems are widespread. There are, however, indications that the sea level in the Aral is slowly rising again thanks to a dam construction project funded by the World Bank, which was completed in August 2005. Although it is impossible to revive the sea fully, a higher sea level should reverse part of the environmental damage. The effects of radiation from years of Soviet nuclear testing in the north of the country at Semipalatinsk"underground as of the 1960s but atmospheric until then"are potentially serious but their extent is as yet unclear.

In July 2005 the Kazakh authorities reported outbreaks of avian influenza (or bird flu) among poultry in Pavlodar region, and other reports from the Russian authorities confirmed that bird flu is spreading from its original location in South-east Asia north- and westwards into Mongolia and Siberia. The outbreaks in Kazakhstan and Russia have been attributed to contact between domestic birds and wild waterfowl via shared water resources. There have been reports of the virus in East Kazakhstan, Akmola and Northern Kazakhstan. Kazakhstan!s large geographical size and small population have led officials to remain sanguine about the possibility of an epidemic among humans. However, the rapid spread of the virus in Russia could help bird flu to spread to more of Kazakhstan!s border regions.

Natural resources and the environment

Kazakhstan has a large endowment of oil, and to a lesser extent gas reserves. The Statistical Review of World Energy, published by BP (UK), estimates total Kazakh proven reserves at the end of 2005 at 79.6bn barrels of oil, or 3.3% of world reserves. By comparison, Saudi Arabia possessed 264.2bn barrels in proven reserves at the end of 2005, equivalent to 22% of the world total. At the end of 2005 Kazakhstan had 1.7% of world gas reserves, totalling 3trn cu metres, as well as large deposits of coal"31.3bn tonnes in reserves, equal to 3.4% of world reserves. It also has deposits of chrome, lead, tungsten, copper, zinc and iron ore, as well as several large gold deposits, including the Vasilkovskoye mine with around 7m oz of gold.

In addition to the damage caused by Soviet-era heavy industry, Kazakhstan has inherited two grave environmental problems. First, the area around Semipalatinsk (near the eastern border of the country) acted as the Soviet Union!s nuclear test site for many years, and has been heavily contaminated by radioactivity, the long-term impact of which remains unclear"in part because the Soviet authorities covered the issue up and suppressed data. Second, the Aral Sea, whose shoreline Kazakhstan shares with Uzbekistan, is drying up rapidly because of the excessive and inefficient use of the two rivers that feed it, the Syrdarya and the Amudarya (Oxus and Jaxartes), for cotton production in Central Asia. The remainder of the Aral Sea is contaminated by the overuse of fertilisers and pesticides, and the exposed bed of the former sea is a dustbowl affecting the health of those living near it. The desiccation of the Aral Sea has also caused the former island of Vozrozhdensky to become a peninsula"although sea levels are now reportedly rising after the construction of a dam

Kazakhstan is rich in mineral resources

Radiation and drought are the main environmental problems

Avian influenza could pose new health threat

Kazakhstan 21

© The Economist Intelligence Unit Limited 2006 www.eiu.com Country Profile 2006

funded by the World Bank. This island was a Soviet-era biological testing site. These problems have caused major water supply shortages and precipitated the near-collapse of the Kazakh fishing industry.

Transport, communications and the Internet

Kazakhstan faces two key infrastructure challenges. First, the country needs to plan decades ahead for oil and gas export pipelines and seek the necessary foreign investment to fund these pipelines. In addition, as Kazakhstan has no access to the high seas, the government needs the political consent of other states for the construction of these pipelines. Moreover, two of Kazakhstan!s possible future pipeline routes, Russia and Iran, are potential competitors in global energy markets. Both countries are likely to question the legality and environmental wisdom of proposals to build an oil export pipeline under the Caspian Sea from Aktau in western Kazakhstan to Baku, the capital of Azerbaijan. The purpose of this pipeline would be to allow Kazakhstan to pump oil directly into the newly opened oil pipeline that takes oil from Baku to the Turkish Mediterranean oil terminal of Ceyhan. Second, Kazakhstan!s size"five times that of France"and population distribution mean that maintaining an integrated national communications infrastructure is costly. The main economic activity, oil, is in the west of the country, close to the Caspian Sea, whereas the bulk of the population lives in the central, southern and eastern provinces.

Rail is a vital form of freight transport in Kazakhstan. The state-owned railway monopoly, Kazakhstan Temir Zholy (Kazakhstan Railways), is currently engaged in a three-year, US$1bn upgrade programme funded by foreign lending. Passenger rail services are loss-making but are being spun off into a separate corporate entity from the more viable cargo transport business. The railway infrastructure is poor. Kazakhstan has a railway density of only 5.5 km per 1,000 sq km, compared with 50-100 km in advanced European economies. Even in the Commonwealth of Independent States (CIS) railway density tends to be in the range of 23-37 km per 1,000 sq km.

Kazakhstan has 14,203 km of 1.52m-gauge railway lines, of which 4,802 km are double-track lines but only 3,997 km are electrified. New lines are planned to shorten the journey between western China and central Russia, a journey that has to cross Kazakhstan, which would therefore bring higher invisibles earnings on the balance of payments. Reform and restructuring of the railways is, however, a slow process and is not expected to be completed until towards the end of the decade at the earliest.

The road infrastructure is also in need of rehabilitation. Kazakhstan has 90,018 km of roads, of which 84,112 km (93%) are paved. Ownership of passenger cars is rising rapidly thanks to the oil boom, but remains low at less than 10 per 100 inhabitants. Illicit imports of second-hand or stolen cars make up a significant part of the market.

Given Kazakhstan!s size and population distribution, the development of civil aviation could be expected to have been a policy priority. Instead, commercial

Size poses a significant transport problem

Transport links need massive investment

Aviation has suffered from political in-fighting

22 Kazakhstan

Country Profile 2006 www.eiu.com © The Economist Intelligence Unit Limited 2006

aviation became mired in a political battle for control of the sector. The state-owned airline"known first as Kazakhstan Airlines and then as Air Kazakhstan"suffered as a result, and was eventually declared bankrupt in 2004. Its rival, Air Astana, then took over all the former national carrier!s most profitable routes and is now the country!s main operator. Deputies in the previous parliament accused the government of forcing Air Kazakhstan!s bankruptcy in order to favour Air Astana.

The new national carrier is benefiting from the authorities! determination to promote the new capital, Astana. In early 2005 the government announced that foreign carriers would be forced to switch all of their flights from the former capital, Almaty, to Astana. This caused an outcry among international airline operators, and the government offered a compromise in July. Airlines will be allowed to continue to serve Almaty if at least one flight from each foreign destination flies into Astana. Almaty remains Kazakhstan!s commercial capital and its population is more than twice that of Astana.

As tends to be the case in emerging markets, mobile telephony has grown rapidly despite its relatively high cost, whereas fixed-line telephony has languished. According to the World Bank, there were 35.1 fixed-line and mobile telephone subscribers per 100 inhabitants in 2004, up from 13.7 per 100 inhabitants in 2000. According to government figures, mobile subscribers in 2004 numbered 18 per 100 inhabitants"up by 200% from 2001"and there were 15 landlines per 100 inhabitants. In developed countries landline penetration is usually at least 40 per 100 inhabitants, and in the western countries of the former Soviet Union it is over 20 per 100 inhabitants. Internet use in Kazakhstan was 26.7 per 1,000 inhabitants in 2004 according to the World Bank, up from 6.7 per 1,000 inhabitants in 2000. Although this is a reasonable level of Internet usage by Central Asian standards, access to the Internet in Kazakhstan remains a minority privilege"often of those working for the government, who have access at work. Limited salaries make the cost of computers and Internet connections prohibitive for most people.

Energy provision

Kazakhstan is in the early stages of becoming a substantial energy producer, but for the moment the country still imports a portion of its energy requirement. Over time, much of this is likely to be produced domestically, thereby obviating the need for imports. Domestic oil consumption is around 260,000 barrels/day. Under half of Kazakhstan!s electricity requirement comes from importing electricity from Russia. Given that 83% of all associated gas in Kazakhstan from oil production is still flared off"despite government regulations banning flaring"there is ample feedstock for gas-fired power stations. For the moment, Kazakhstan still buys gas from Uzbekistan for southern Kazakhstan. However, the government is now developing small local fields in southern Kazakhstan to eliminate the need for imported gas from Uzbekistan.

Kazakhstan!s energy transmission and distribution systems are being rehabilitated after years of Soviet-era neglect. The electricity grid is receiving assistance from the World Bank and the European Bank for Reconstruction and

Kazakhstan still imports electricity and gas

Mobile telephony is growing rapidly

Kazakhstan 23

© The Economist Intelligence Unit Limited 2006 www.eiu.com Country Profile 2006

Development (EBRD). Regional electricity companies are scheduled for privatisation. However, past experience suggests that the likely success of these utilities! privatisation is questionable. For instance, in 2000 the government in effect forced Tractebel (Belgium)"which ran the Almaty electricity utility"to leave the country. Tractebel had successfully turned the Almaty electricity company around by slashing delinquency rates of over 75% to around 13%. However, following the April 1999 devaluation the government froze electricity prices to control inflation, and the ensuing dispute with Tractebel led the Belgian company to leave Kazakhstan.

The economy

Economic structure Main economic indicators, 2005 (Actual unless otherwise indicated)

Real GDP growth (%) 9.4

Consumer price inflation (av; %) 7.6

Current-account balance (US$ m) -485.7

Exchange rate (av; Tenge:US$) 132.9

Population (m) 15.2

External debt (year-end; US$ m) 41,541a

a Economist Intelligence Unit estimates.

Source: Economist Intelligence Unit, CountryData.

Before independence in 1991 Kazakhstan!s specialised role in the Soviet economy was focused on wheat production, metallurgy and mineral extraction. In turn, Kazakhstan could count on a captive market for its goods"regardless of their quality"and on a steady supply of underpriced energy and other cheap inputs. With the break-up of the Soviet Union, this centrally planned system collapsed, causing a steep fall in output in Kazakhstan"the Central Asian economy most closely linked to Russia. The post-independence recession thus wiped out a number of industrial subsectors, such as consumer goods. Industry shrank from over 31% of GDP in 1992 to just 21% of GDP in 1996. By 2000 industry had become the main sector again, with a 33% share of GDP, almost exclusively attributable to an investment-led oil boom, as a result of which oil now accounts for over half of industrial output. The only other significant sector in the Kazakh economy is the semi-processing of metals and steel production, both of which are relatively labour-intensive but which are concentrated in a handful of firms. This sector also recovered rapidly from the post-Soviet collapse thanks to foreign investment.

The construction sector is very dependent on the oil sector, and has expanded gradually as a share of GDP in tandem with investment in oil. The rest of the economy comprises a small-scale but rapidly growing services sector, and a large, inefficient and labour-intensive agricultural sector"the largest employer but an increasingly irrelevant exporter. In 2005 agriculture!s share of GDP was less than 7%"down from 23% in 1992"and food products accounted for less than 3% of exports. Because of the growth of the oil sector and the likely real

Soviet collapse severs chains of production

Other sectors are weak, and subordinate to oil

24 Kazakhstan

Country Profile 2006 www.eiu.com © The Economist Intelligence Unit Limited 2006

appreciation of the currency, in the long term the agricultural sector will need to be subsidised heavily if it is to survive.

Thanks to foreign participation, the quality of investment in the economy is far superior to that of the Soviet era and has recovered following a post-independence collapse. However, the vast majority of foreign investment is destined to the extraction of mineral resources, with other sectors suffering from under-investment. Foreign investment into oil extraction accounted for around one-quarter of total investment inflows in 2005.

Data collection still suffers from methodological shortcomings, in part owing to a lack of resources. The statistics agency no longer has the influence over enterprises and ministries that it enjoyed in the Soviet period, making data collection difficult. Its problems are particularly evident in the lack of consistent expenditure data on the national accounts. The data are incomplete and difficult to obtain, and their release is far from timely.

Comparative economic indicators, 2005 Kazakhstana Russiaa Uzbekistan b Chinaa Ukrainea