Sustainable Mobility : 100 Investment Ideas

3 Document non contractuel, strictement limité à l’usage privé du destinataire, les informations fournies dans ce document proviennent de sources dignes de foi mais ne

peuvent être garanties. Les appréciations formulées reflètent notre opinion à la date de publication et sont donc susceptibles d’être révisées ultérieurement

ODDO SECURITIES

Jean-Philippe Desmartin

+33 (0)1 44 51 81 89 - [email protected]

S. Thévoux-Chabuel

+33 (0)1 44 51 84 31 - [email protected]

With the participation of sector analysts

SUSTAINALYTICS

Jean-Florent Helfre

+31 20 205 00 11 - [email protected]

Arne Philipp Klug

+49 69 33 29 65 62 - [email protected]

Laurence Loubières

+1 416 861 0403 - ext.25 - [email protected]

SRI Wednesday 5 October 2011

Sustainable mobility: 100 investment ideas This thematic study carried out in partnership with Oddo Securities, the leading

independent brokerage in France, aims to provide an overview of mobility: both

physical (transport) and virtual. The study examines the ESG challenges, risks and

opportunities presented by sustainable mobility as well as 100 investment ideas

(worldwide coverage) combining buoyant positioning (batteries, rail) and a best-in-

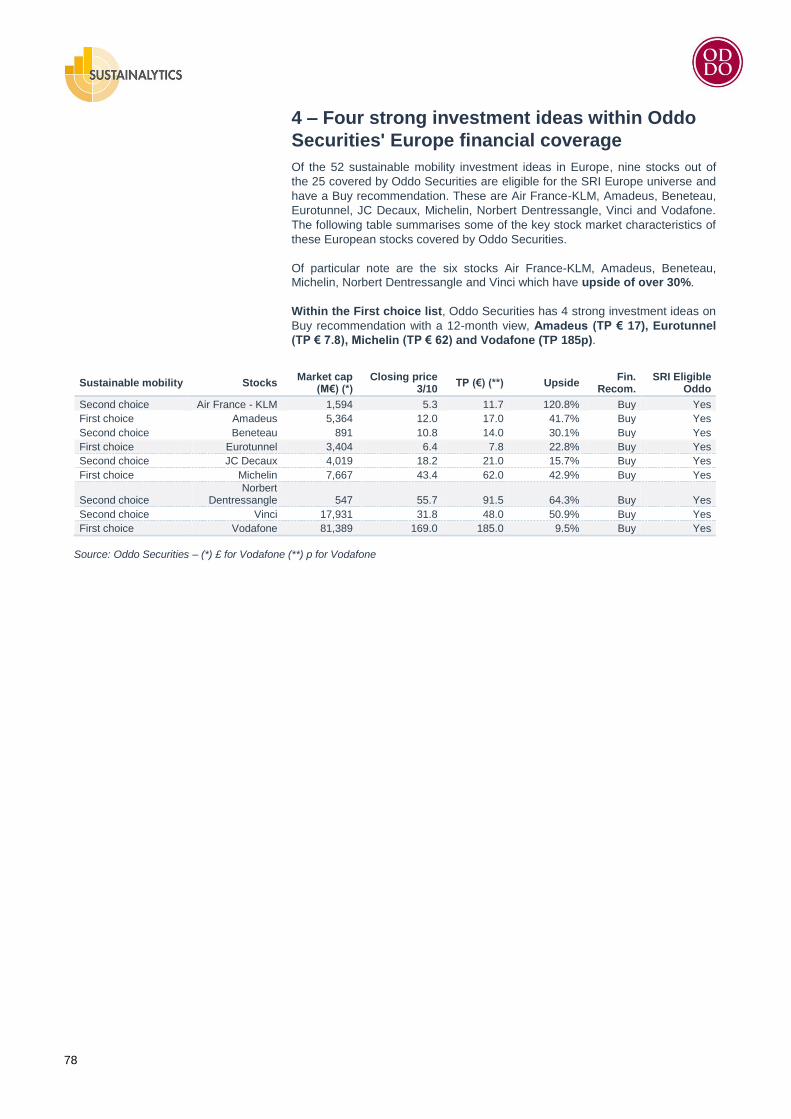

class approach. Within its European financial coverage, Oddo Securities has 4 strong

investment ideas on Buy recommendation with a 12-month view, Amadeus (TP € 17),

Eurotunnel (TP € 7.8), Michelin (TP € 62) and Vodafone (TP 185p).

By sustainable mobility we mean the "ability to meet the needs of a society to

move freely, gain access, communicate, trade and establish relationships without

sacrificing other essential human or ecological values today or in the future".

Therefore, the challenges are enormous.

This study considers the ESG challenges associated with different types of

transport (air, rail, maritime and road transport) distinguishing between freight and

passenger transport on which a distinction has also been drawn between

developed and emerging countries. It also looks at the major alternatives offered

by virtual mobility and e-substitution.

We have also addressed the dynamics (global village, hyper-mobility,

urbanisation), areas for improvement/risks (air pollution, climate change,

congestion, noise, peak oil, land take, road safety) and environmental and social

opportunities (batteries, second-generation biofuels, public transport, rail, virtual

mobility) associated with sustainable mobility which are many and complex. Oddo

Securities proposes an ESG allocation (overweight, neutral and underweight) for

25 mobility positionings with regards to sustainable development.

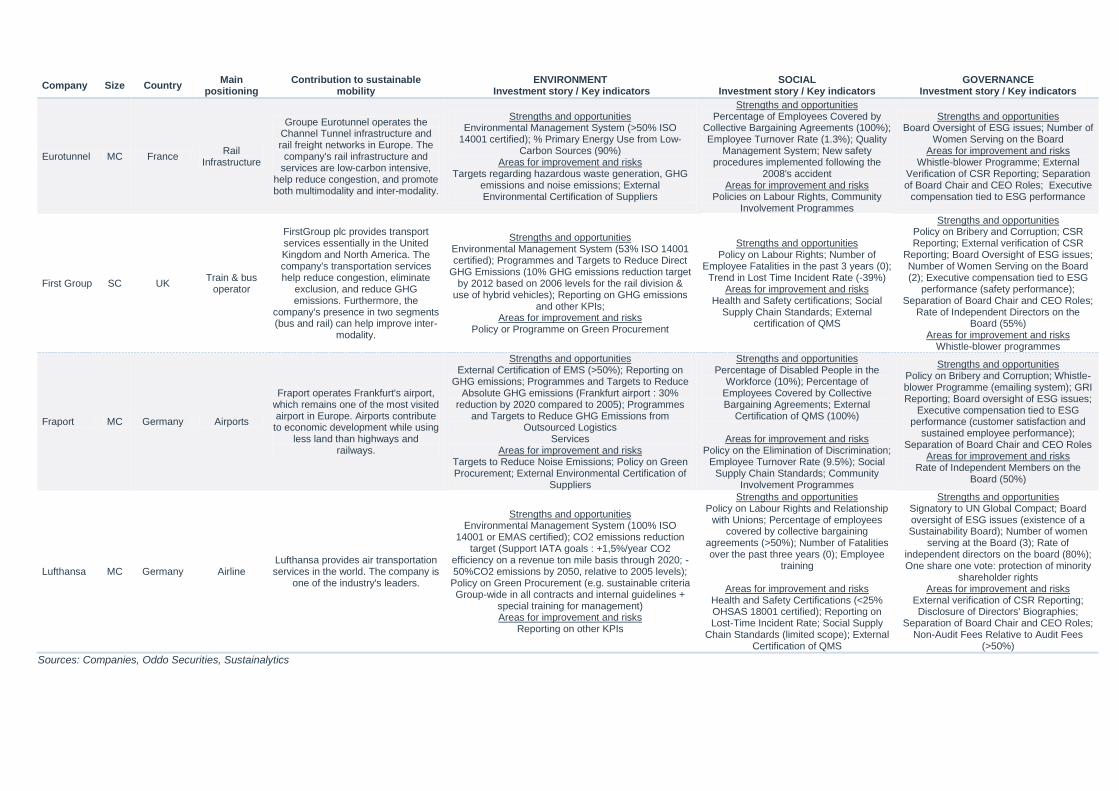

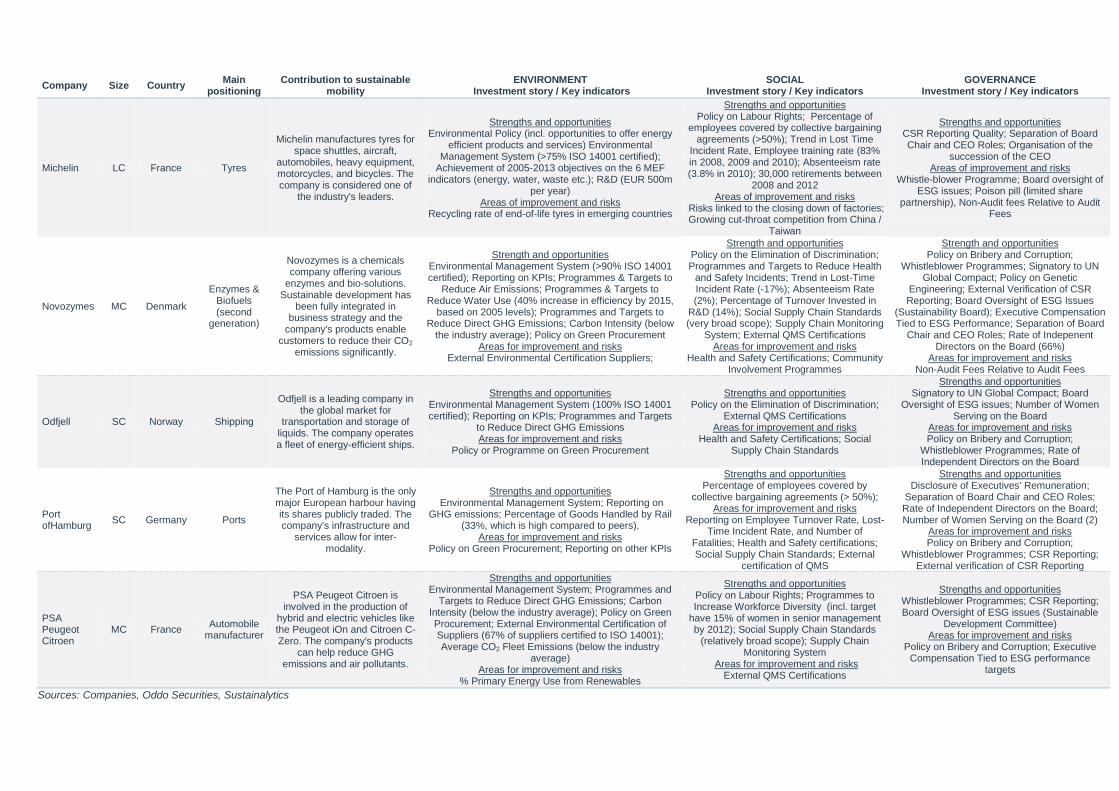

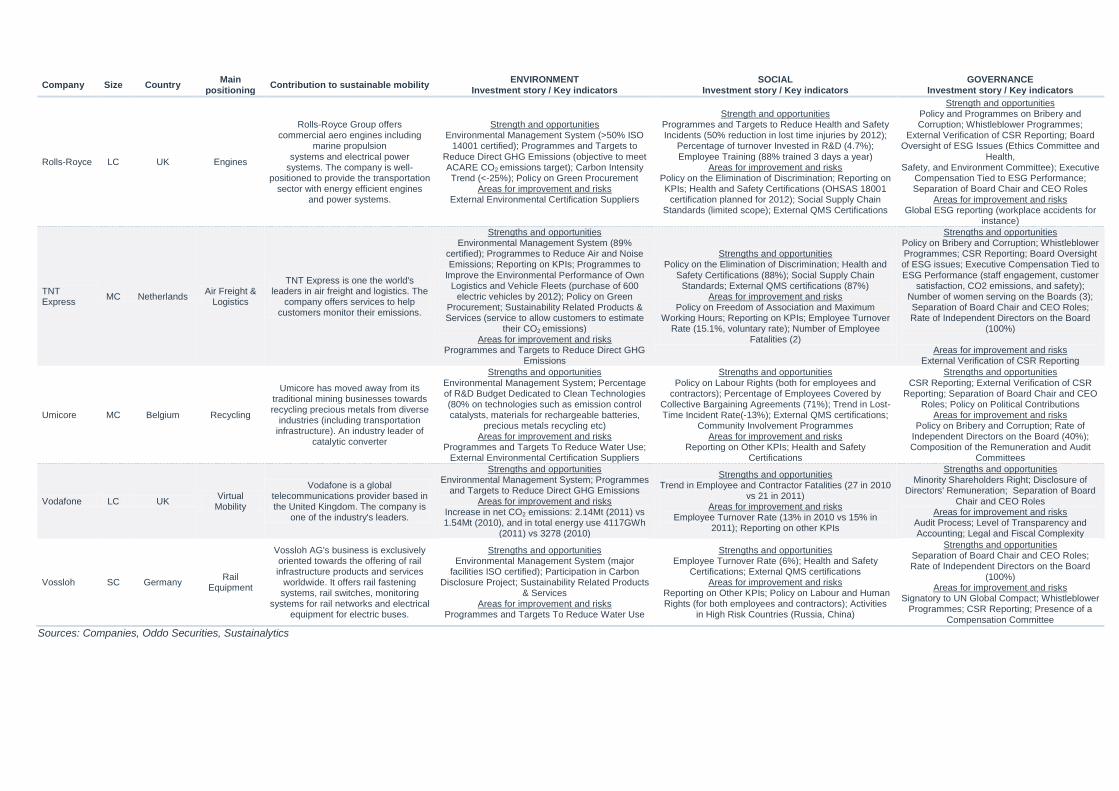

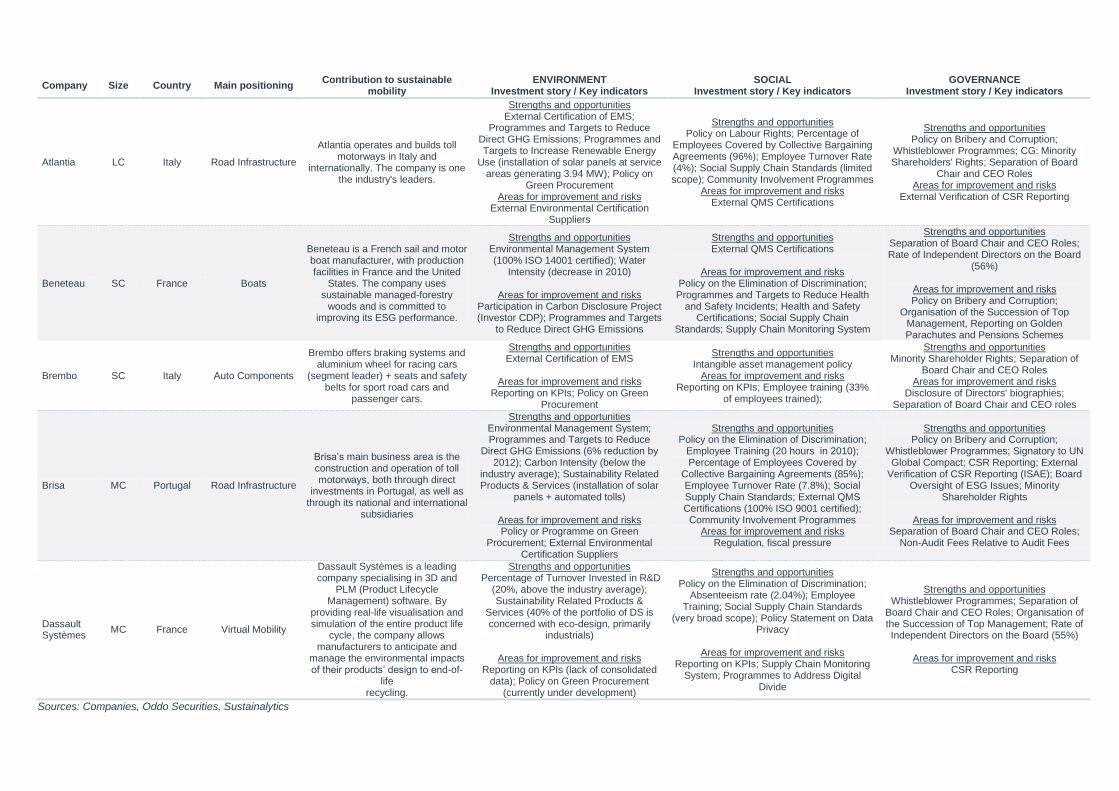

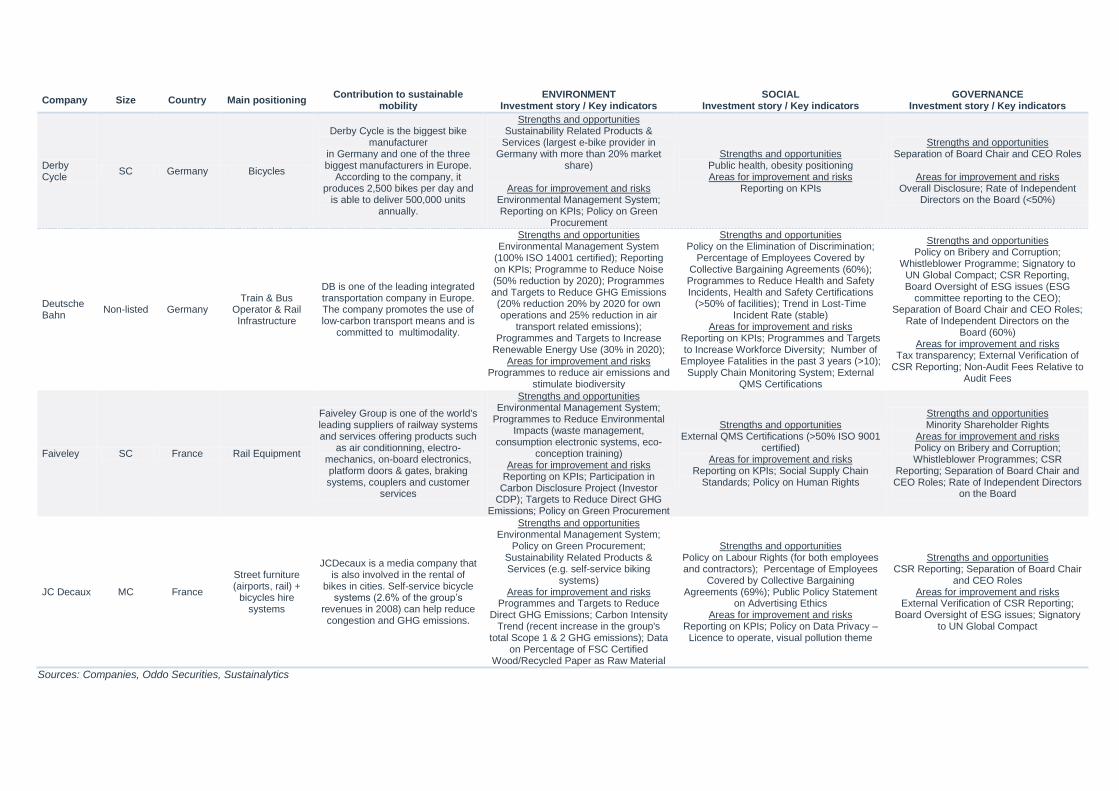

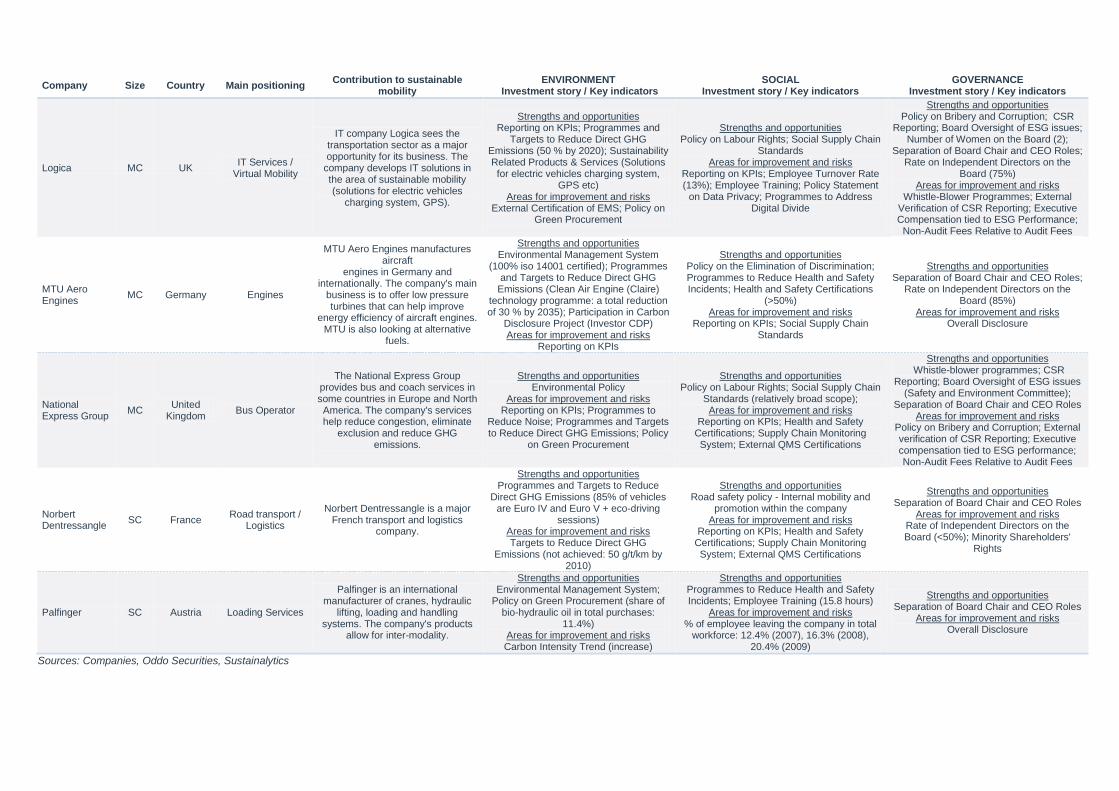

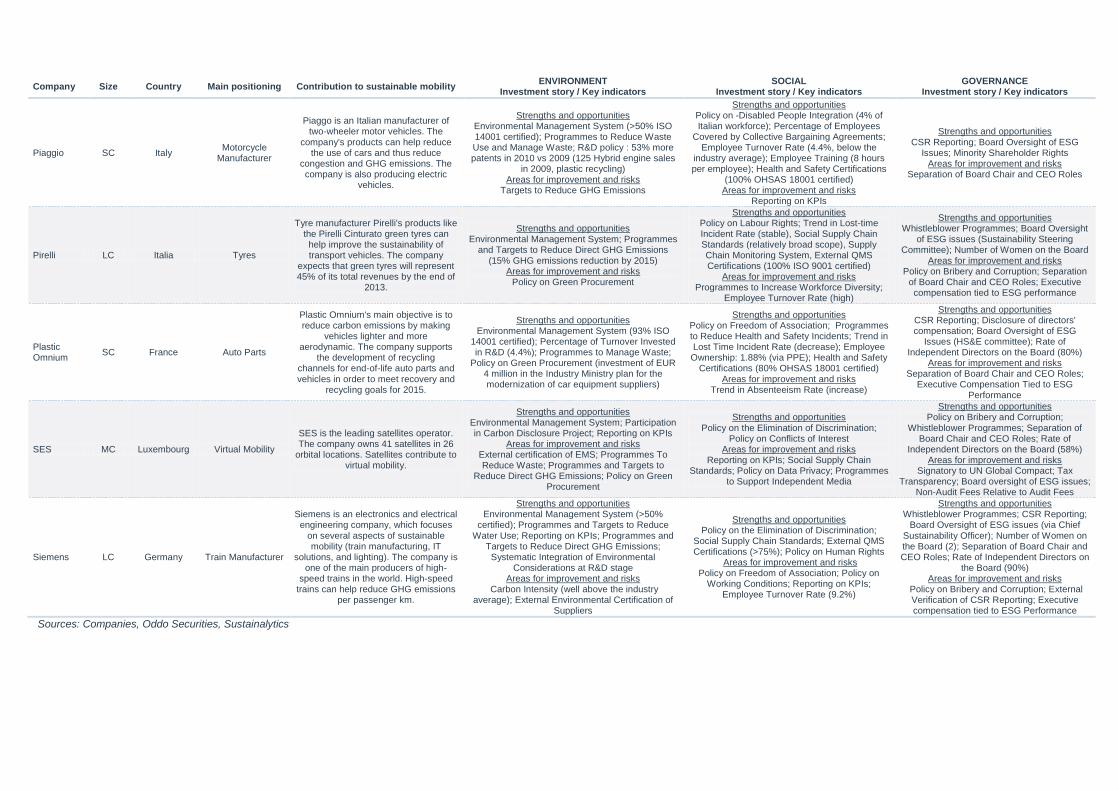

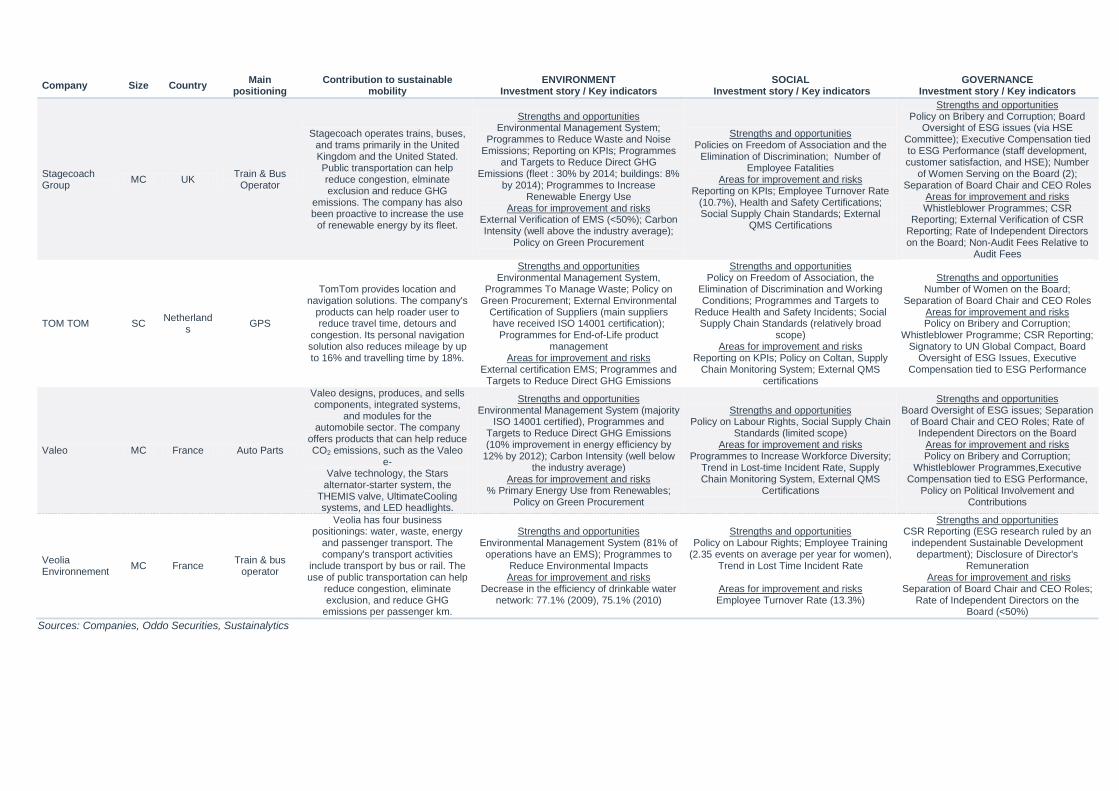

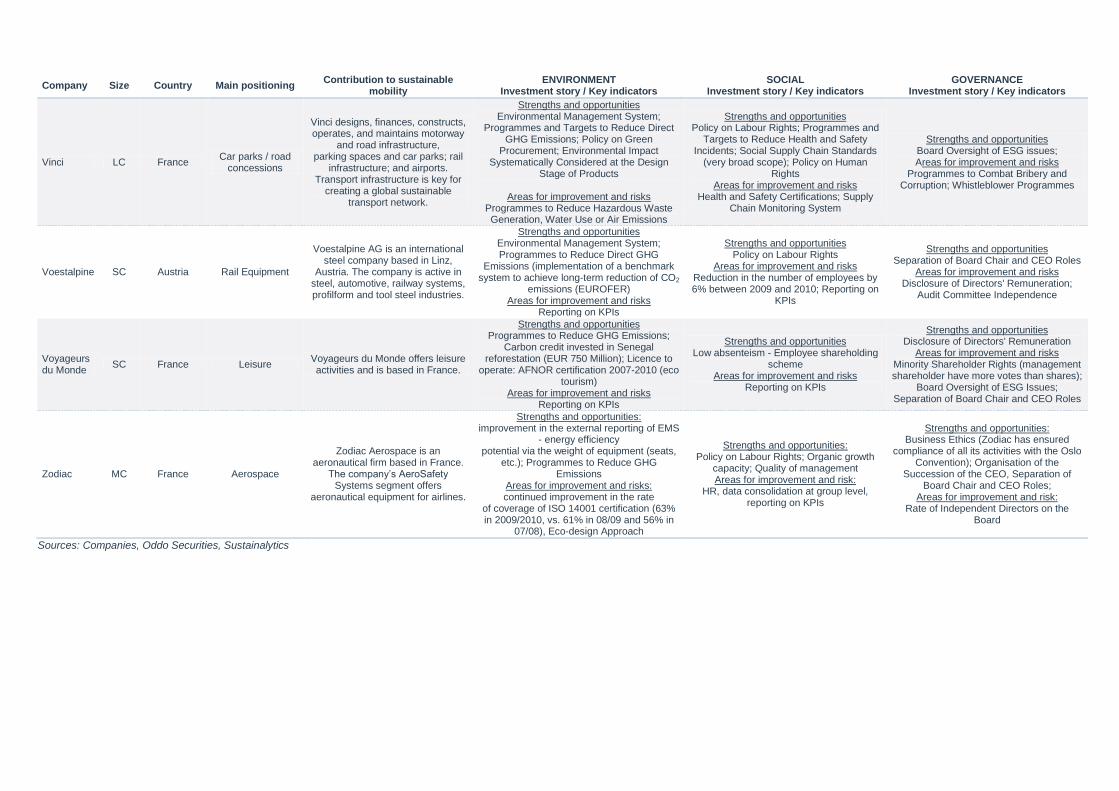

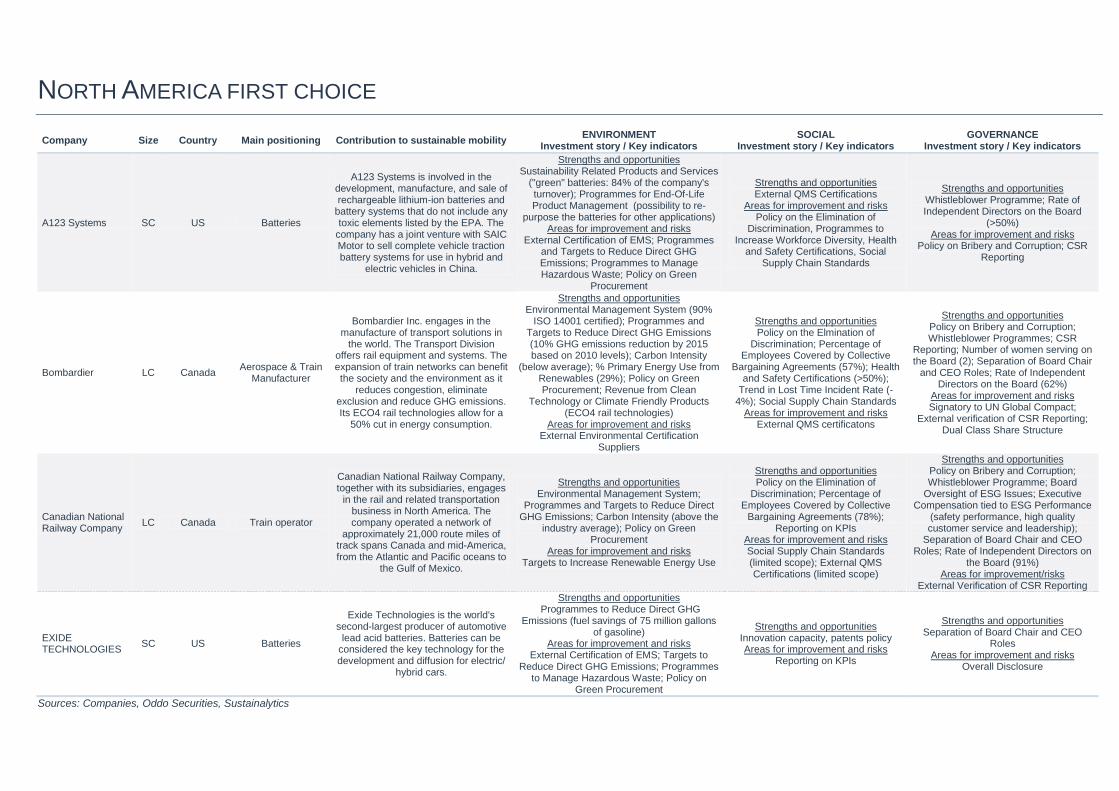

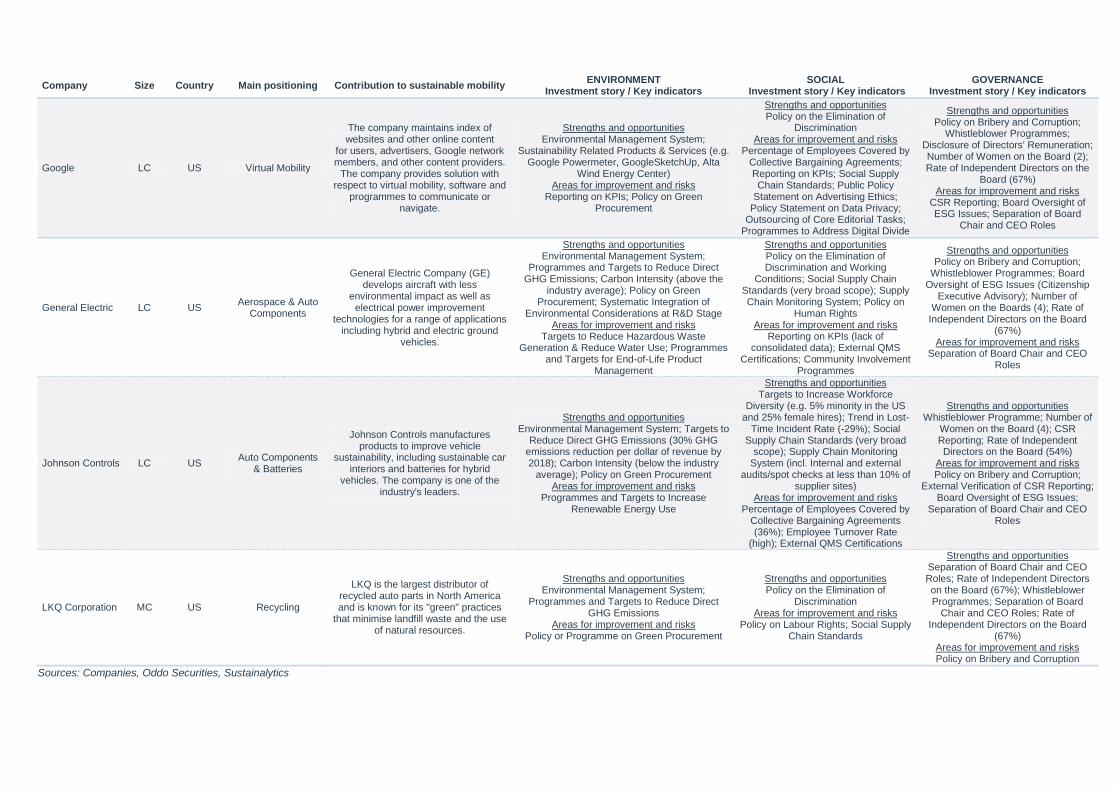

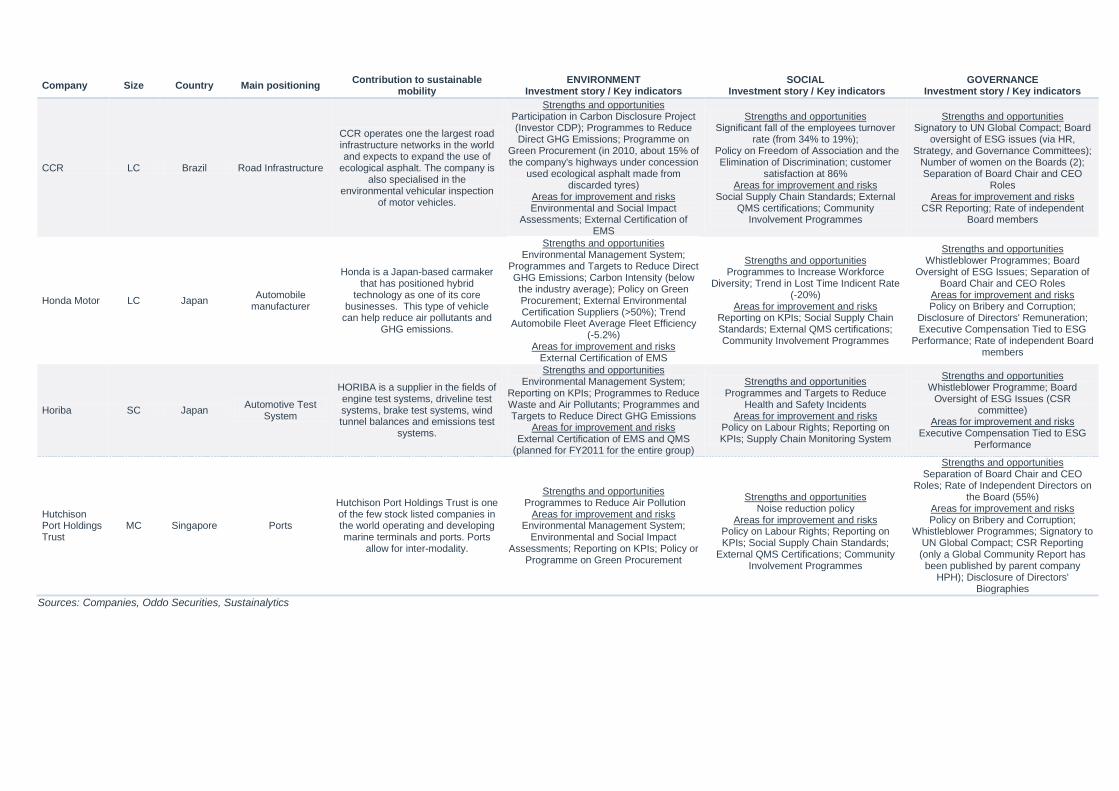

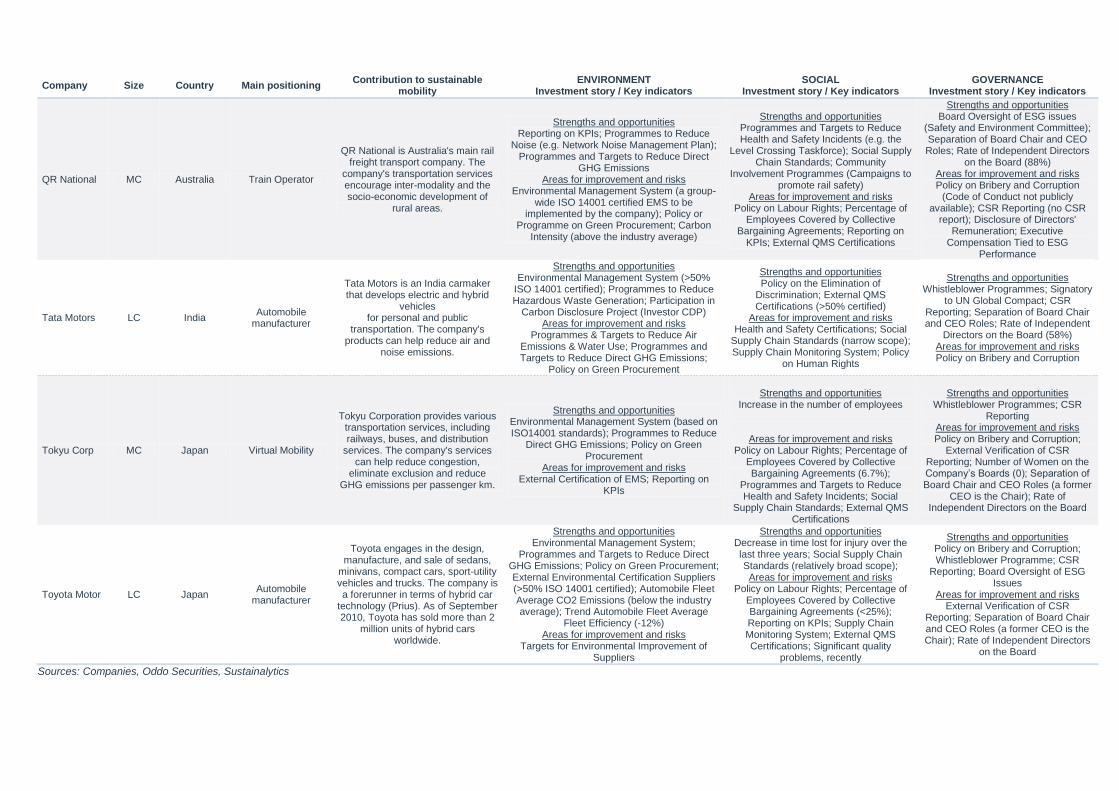

The 100 investment ideas proposed by Oddo Securities and Sustainalytics, cover

Europe (52 stocks), North America (29 stocks) and the rest of the world (19

stocks). These ideas are presented in the appendices in the form of an ESG

SWOT analysis.

The companies identified cover traditional transport business models (airlines, car

makers, shipping) as well as emerging business models (batteries, biofuels) and

businesses in recovery (bicycles, rail).

Within its European financial coverage, Oddo Securities has 4 strong investment

ideas on Buy recommendation with a 12-month view, Amadeus (TP € 17),

Eurotunnel (TP € 7.8), Michelin (TP € 62) and Vodafone (TP 185p).

4 Document non contractuel, strictement limité à l’usage privé du destinataire, les informations fournies dans ce document proviennent de sources dignes de foi mais ne

peuvent être garanties. Les appréciations formulées reflètent notre opinion à la date de publication et sont donc susceptibles d’être révisées ultérieurement

The information herein has been obtained from sources that Sustainalytics believes to be reliable. However, Sustainalytics does not guarantee its accuracy or completeness. Copyright © 2011 Sustainalytics. All rights reserved. No portion of this material may be reproduced in any form without the expressed written permission of Sustainalytics.

This publication is exclusively intended for Oddo & Cie‘s customers; it is sent by way of information and cannot be divulged to a third party without the prior consent of Oddo & Cie.

This document is not and should not be construed as an offer to sell or the solicitation of an offer to purchase or subscribe for any investment.

This research has been prepared in accordance with regulatory provisions designed to promote the independence of investment research.

While all reasonable effort has been made to ensure that the information contained is not untrue or misleading at the time of publication, no representation is made as to its accuracy or completeness and it should not be relied upon as such.

Past performances offer no guarantee as to future performances.

All opinions expressed in the present document reflect the current context and which is subject to change without notice.

Oddo & Cie is licensed by the Comité de Contrôle Prudentiel (ACP) and regulated by the Autorité des Marchés Financiers (AMF).

This research has been prepared in accordance with regulatory provisions designed to promote the independence of investment research.

―Chinese walls‖ (information barrier) have been implemented to avert the unauthorised dissemination of confidential information and to prevent and manage situations of conflict of interest.

At the time of publication of this document, Oddo & Cie and/or one of its subsidiaries may have a conflict of interest with the issuer mentioned.

In particular, it may be the case that Oddo & Cie and/or one of its subsidiaries is acting or intends to act in the next twelve months as an injector of liquidity, market maker, advisor or investment bank for one of the companies mentioned in the present publication.

Distribution to U.S. Investors: Notice to US Investors: This report is issued solely to major US institutional investors pursuant to SEC Rule 15a-6. Oddo Securities Corp. MEMBER: NASD / SIPC is distributing this document in the United States of America and, in connection there with, accepts responsibility for its contents. Any US customer wishing to effect transactions in any securities referred to herein or options there on should do so only by contacting a representative of Oddo Securities Corp. and not one of its overseas affiliates, including the producer of the research, Oddo et Cie.

Contact Info

Oddo Securities Corp. MEMBER: NASD/SIPC (U.S.INVESTORS)

A wholly owned subsidiary of Oddo et Cie

Patrick Oddoux President, Oddo Securities Corp. (NewYork),

150 East 52nd Street NewYork,

New York 10022

212-481-4002

The disclosures of all companies mentioned in this document may be consulted on Oddo & Cie‘s research site.

Our stock market recommendations Our stock market recommendations reflect the RELATIVE performance expected for each stock on a 12-month timeframe.

Buy: performance expected to exceed that of the benchmark index, sectoral (large caps) or other (small and mid caps).

Neutral: performance expected to to be comparable to that of the benchmark index, sectoral (large caps) or other (small and mid caps).

Reduce: performance expected to fall short of that of the benchmark index, sectoral (large caps) or other (small and mid caps).

5 Document non contractuel, strictement limité à l’usage privé du destinataire, les informations fournies dans ce document proviennent de sources dignes de foi mais ne

peuvent être garanties. Les appréciations formulées reflètent notre opinion à la date de publication et sont donc susceptibles d’être révisées ultérieurement

Contents

Sustainable Mobility - definitions, challenges and prospects 6

Transport vs. mobility, sustainability and sustainable mobility - What do we mean?

Mobility and its dynamics over the long term: towards Hypermobility

Overview of passenger and freight transport worldwide

Global trends of mobility

The revolution in motion: the new paradigms of mobility

Issues of mobility - The Unbearable Lightness of mobility today? 31

Environmental issues

Social issues

Sustainable mobility is a source of opportunities that go far beyond the transportation sector 50

Infrastructure companies

Manufacturers

Component producers in the world

Energy providers

Renewable electricity: towards more consolidation

Ticketing, leasing and self-service systems

Virtual Mobility

100 investment ideas 75

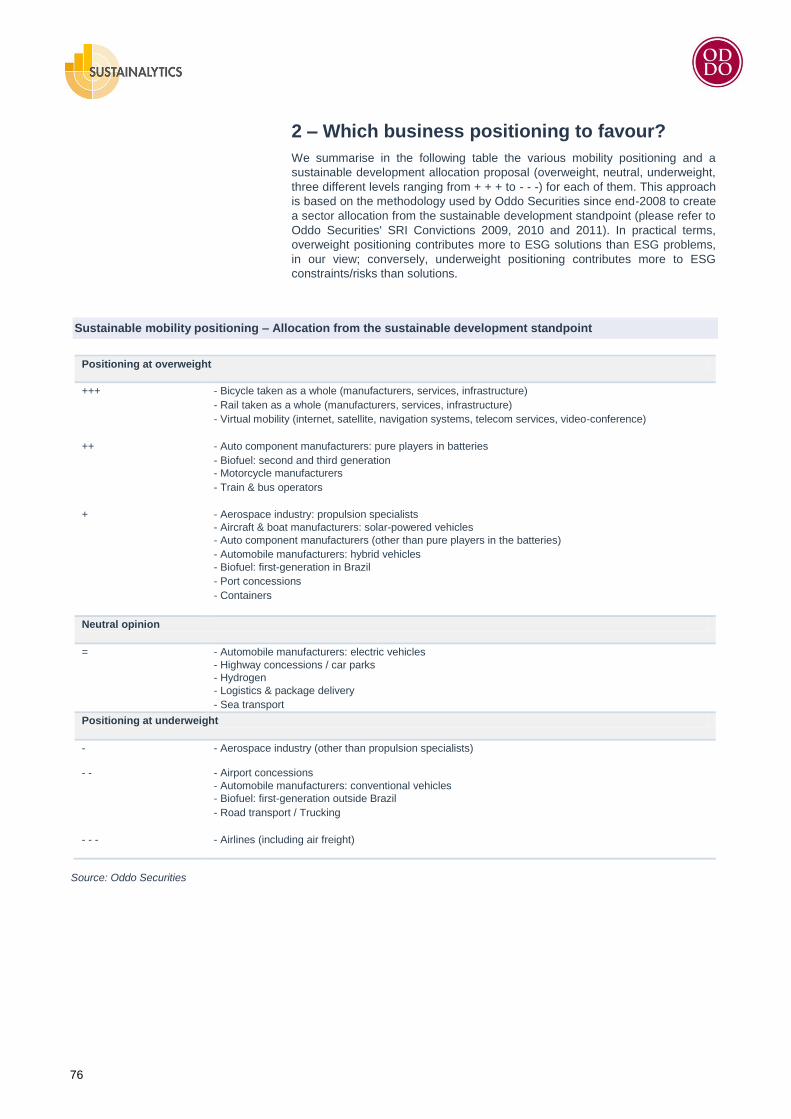

1 – Preliminary comments

2 – Which business positioning to favour?

3 – Sustainable mobility: 100 investment ideas

4 – Four strong investment ideas within Oddo Securities' Europe financial coverage

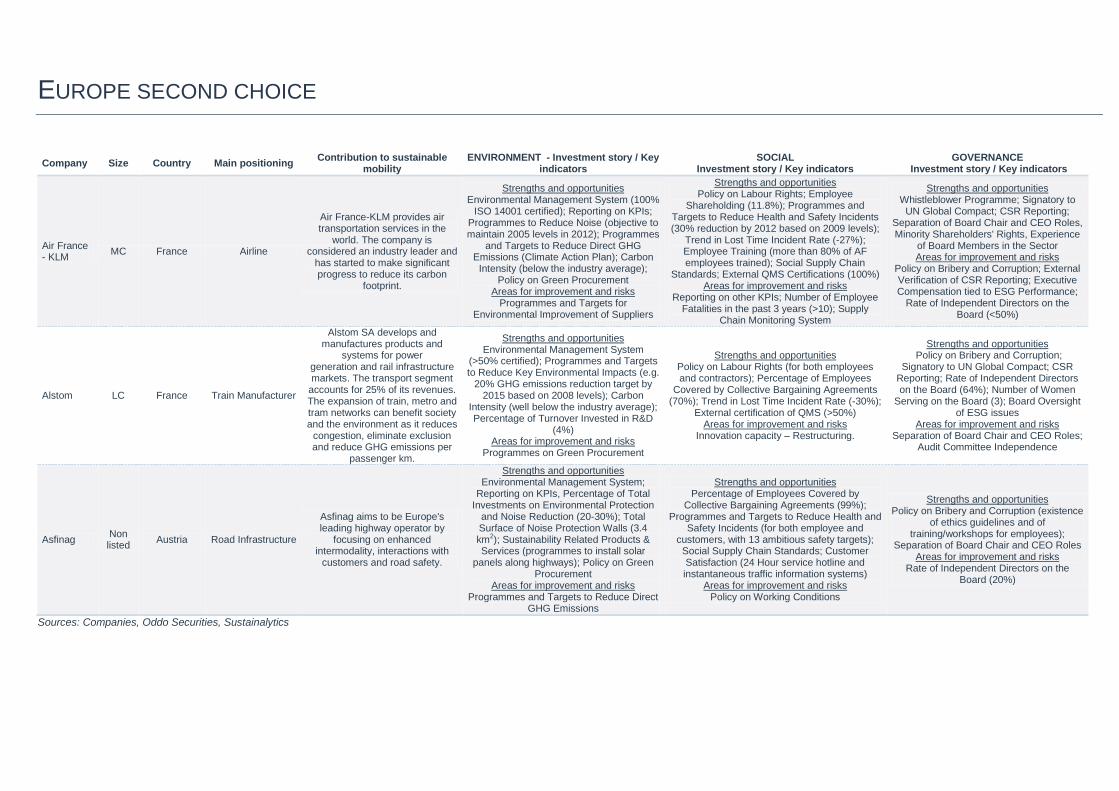

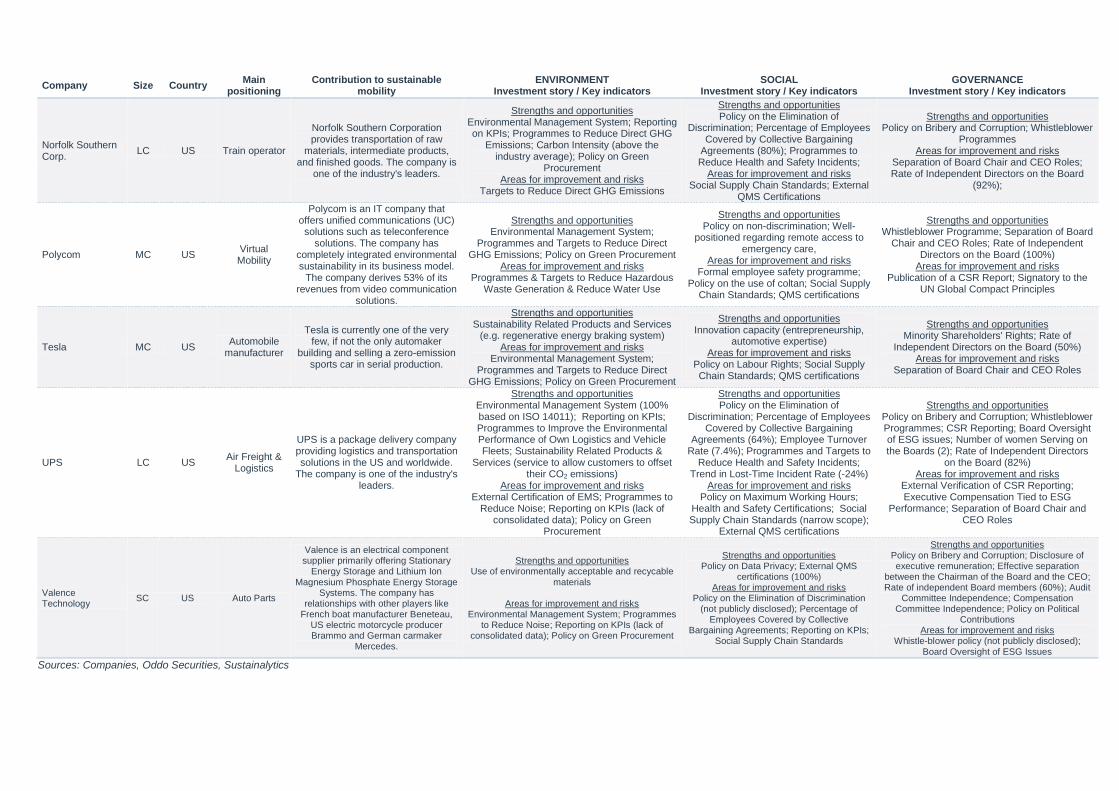

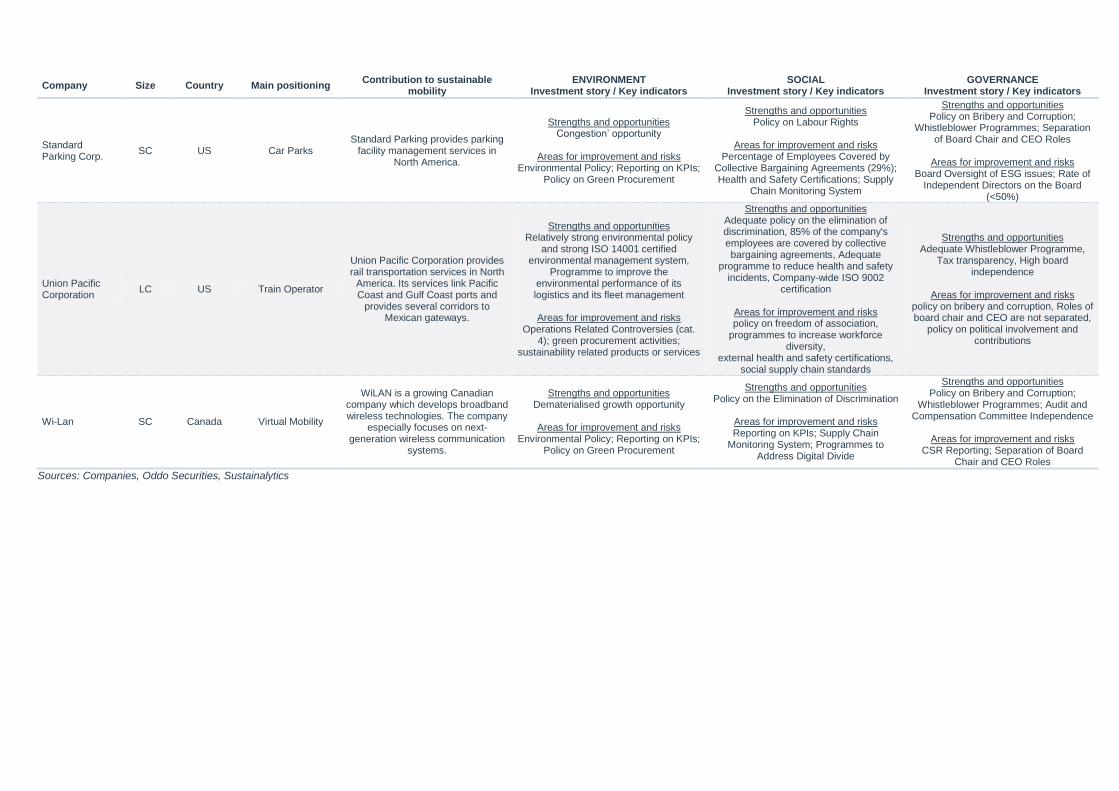

Europe first choice 79

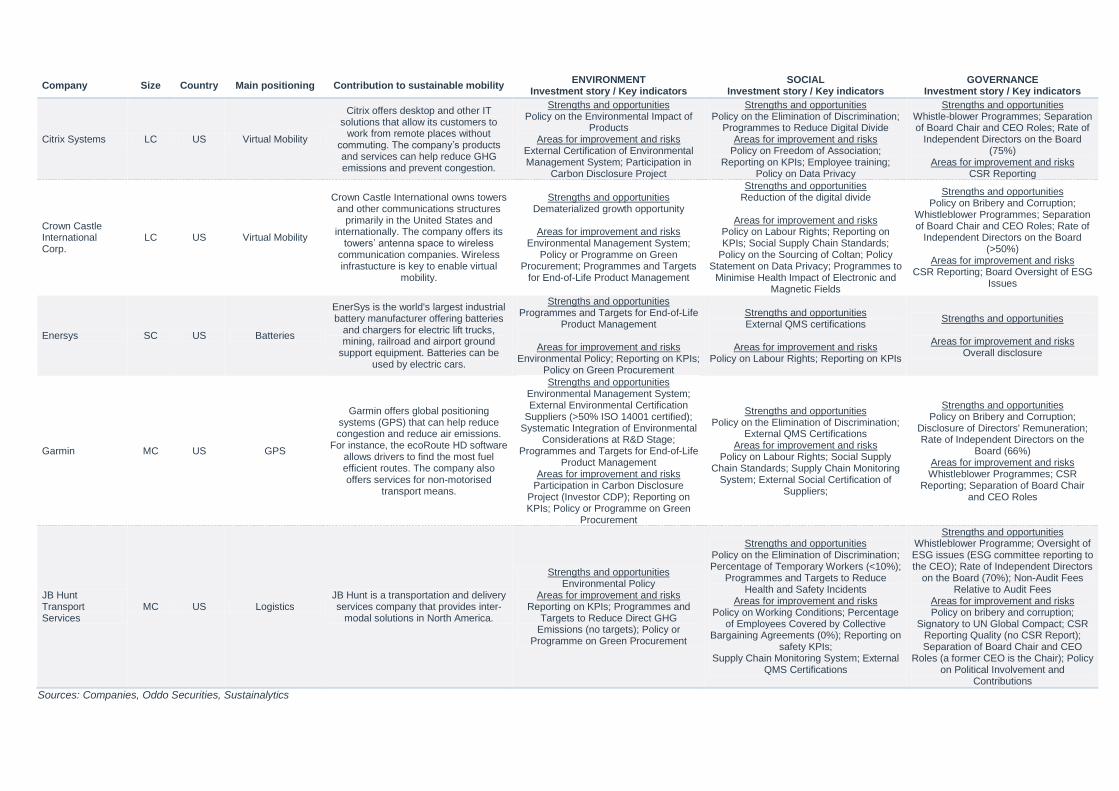

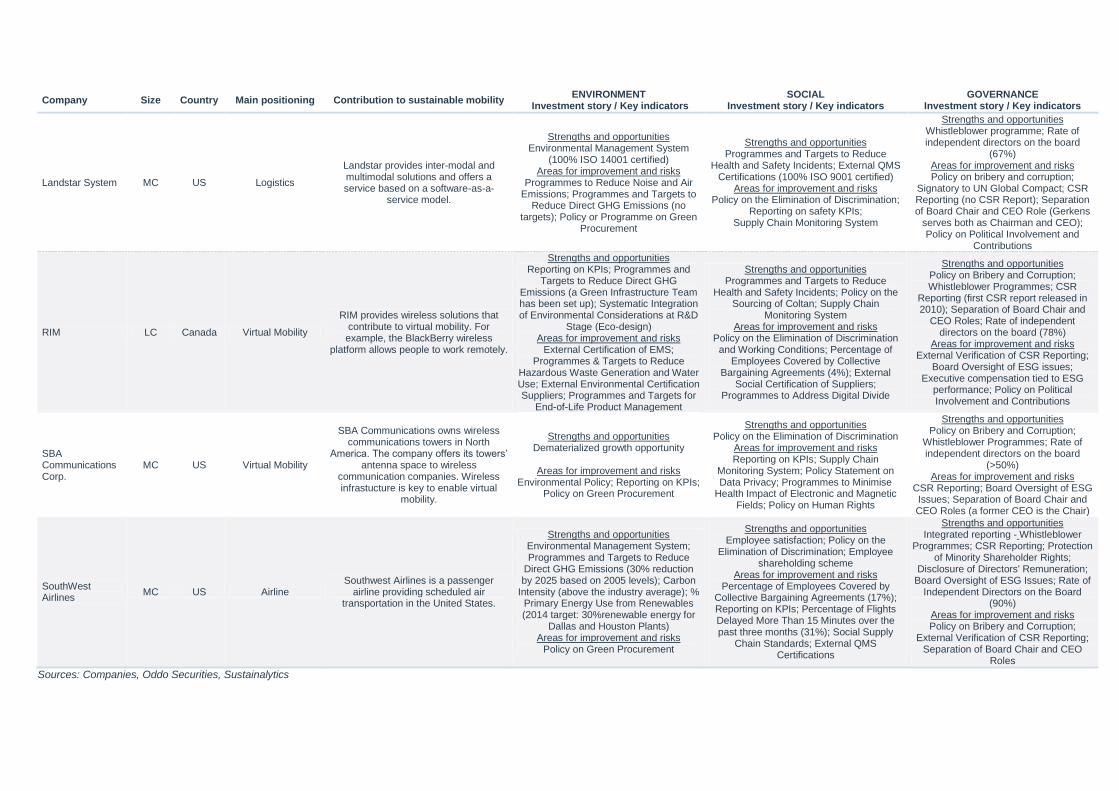

Europe second choice 83

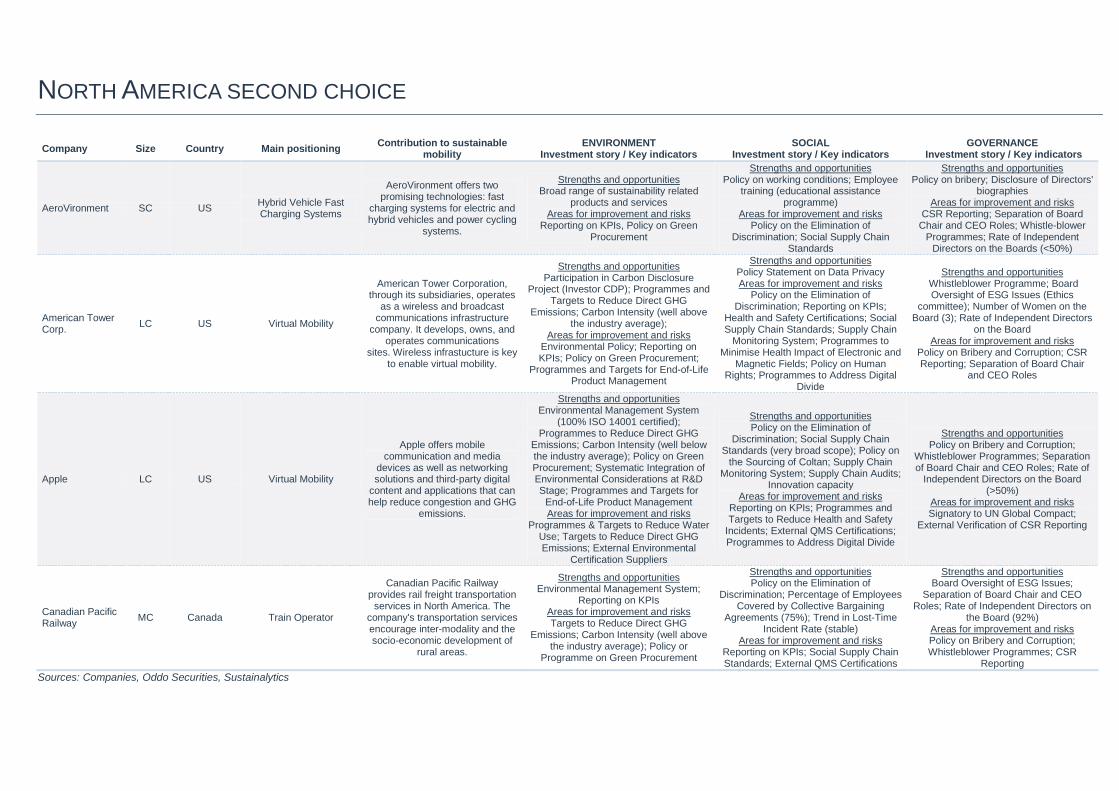

North America first choice 91

North America second choice 94

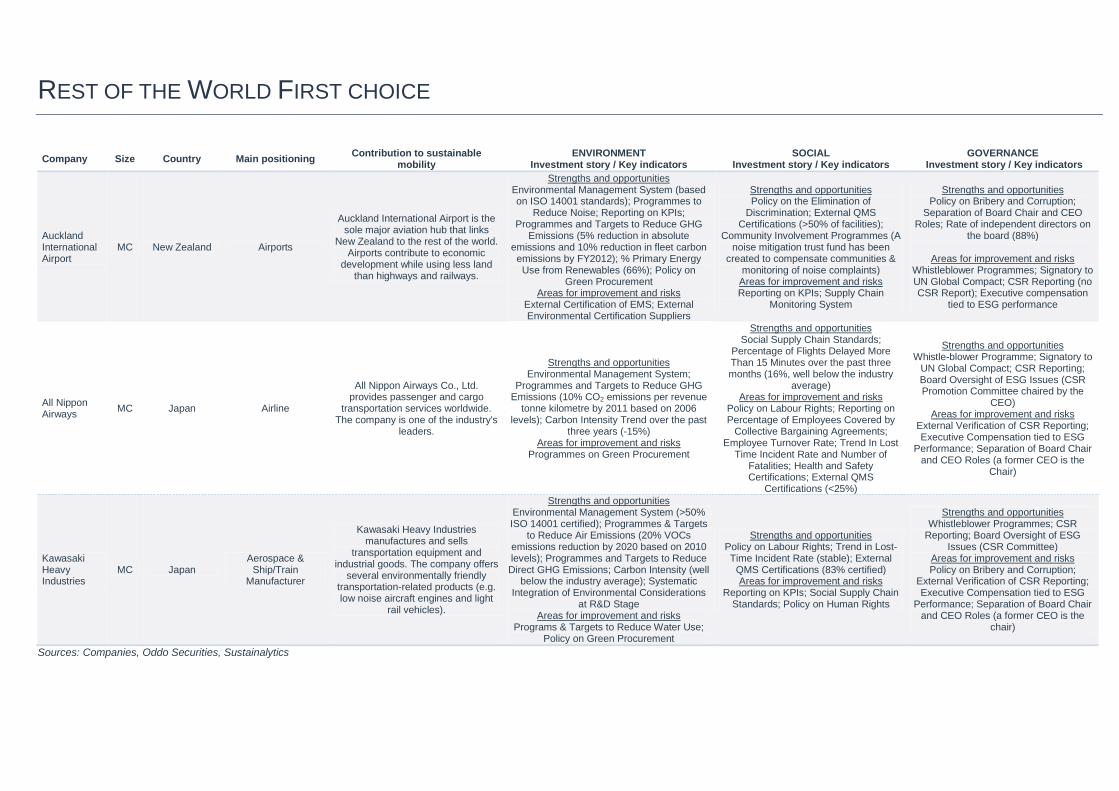

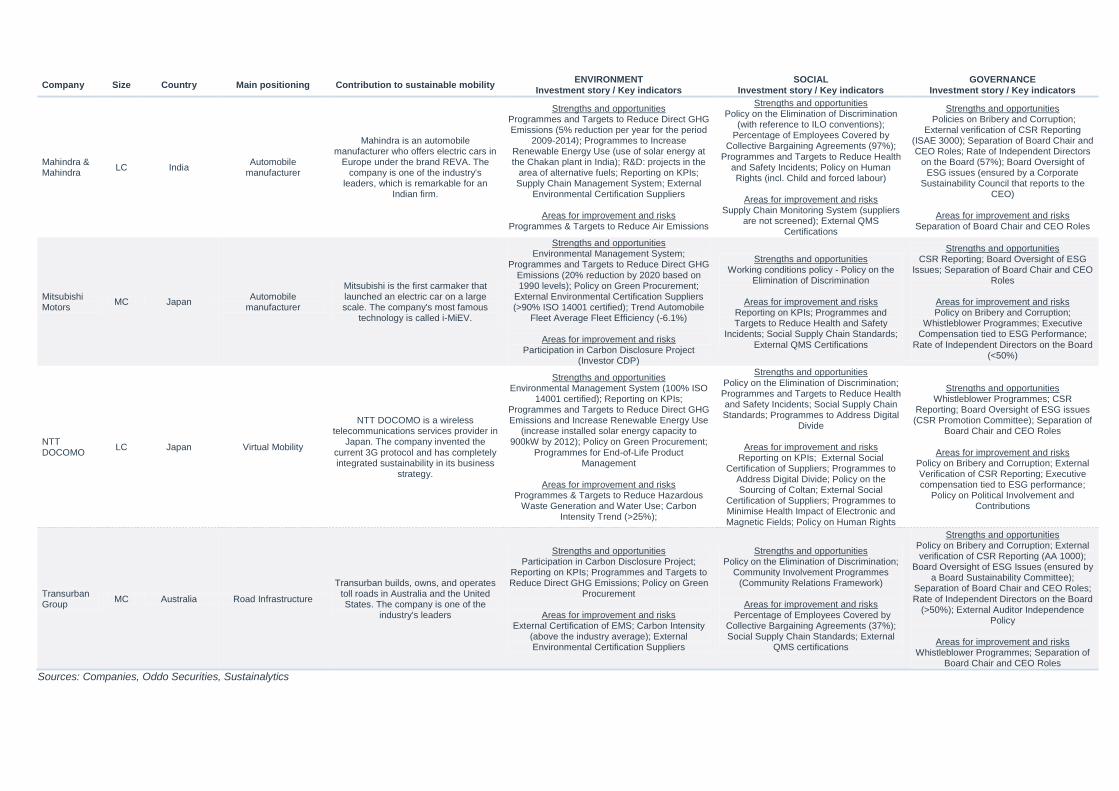

Rest of the World First choice 98

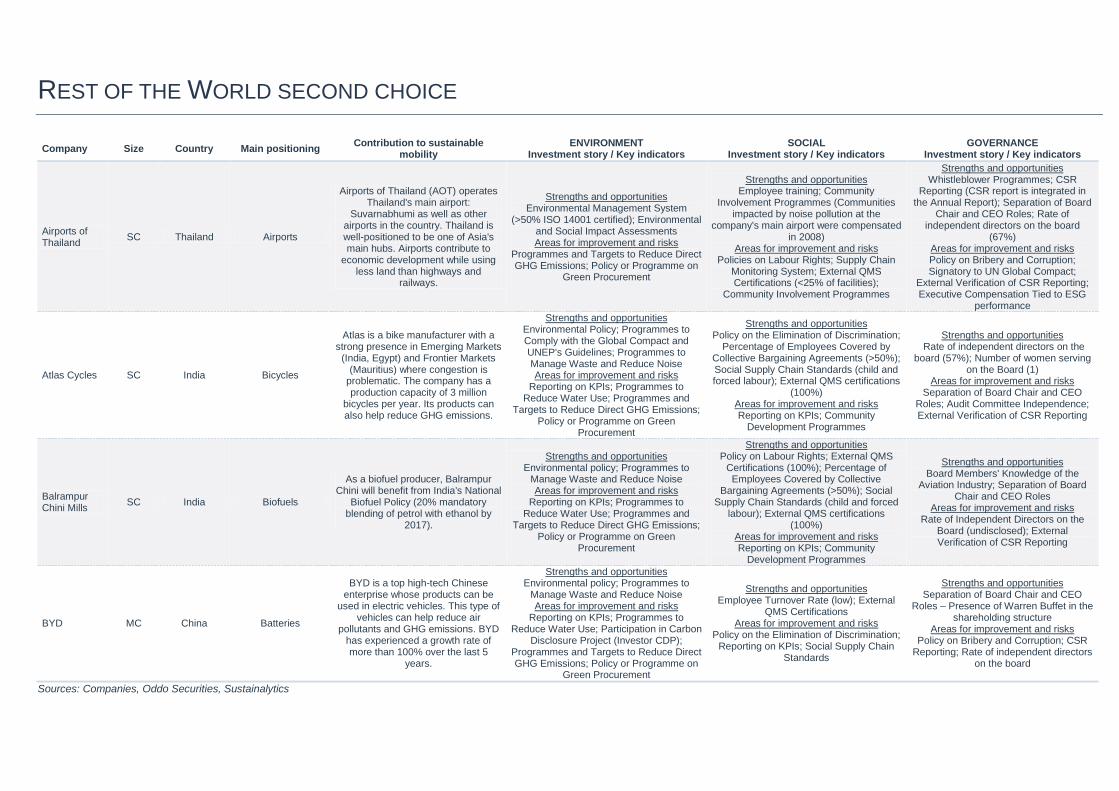

Rest of the World second choice 100

6

SUSTAINABLE MOBILITY - DEFINITIONS, CHALLENGES AND

PROSPECTS

“Today, after more than a century of electric technology, we have extended our

central nervous system itself in a global embrace, abolishing both space and

time as far as our planet is concerned”

Marshall McLuhan, 1964, Understanding Media

"If the automobile, the subway and the aircraft were the emblems of transport in

the twentieth century, especially the shoes and the Smartphone, are those of

Homo Mobilis fluid and connected to the twenty-first century”

Georges Amar, Homo Mobilis the new age of mobility, 2010

Transport vs. mobility, sustainability and

sustainable mobility - What do we mean?

What is mobility and sustainable mobility?

Mobility can be defined as ―the behavioural movement of humans in space,

whether for frequent travel of everyday life, displacement of disruption in daily

life such as tourism, or changes in residential areas involving a change in

territory lived.‖1

Adapting the definition of sustainability given by the World Business Council for

Sustainable Development, sustainable mobility is the ability to meet the needs

of a society to move freely, gain access, communicate, trade and establish

relationship without sacrificing other essential human or ecological value today

or in the future.

One can understand that for mobility to be sustainable, it must follow and adapt

itself to the new environment and new needs of society while avoiding

disruptions in the societal, environmental and economic well-being that could

offset the socio-economic benefits of accessibility improvement…

From "transport" to "mobility"…

Over the past few years, the notion of mobility has replaced that of transport,

and this trend reflects a change in our way of considering our displacements

and travels.

1 Jean-Pierre Orfeuil, Marie-Hélène Massot, THOUGHT THE MOBILITY OF TOMORROW - TEST FOR PROSPECTIVE

CLAIRVOYANCE, Research Centre for Environment and Transport Area Local Institutions, University Paris XIII Val de Marne,

First half 2005

7

The notion of transport with its grammatically in inherent duality between the

carrier and the passenger, expresses a certain passivity of the individual

being transported. It also implies that the movement is not an end in itself but

merely a means to get from one point to another, from a point of origin to a

destination.

In contrast, mobility is less passive, it is an activity. The notion of mobility

recognises and values the active nature of the mobile person. This

enhancement explains the revival of soft modes (cycling, walking ...) but also

involves the cognitive action of the traveller who guides him/herself in the

transportation networks

Another difference between transport and mobility is the universal nature of

mobility. Transportation equipment is a tool, whereas mobility is an attribute of

people, objects, companies and local areas. Mobility becomes almost a human

right as evidenced in developed countries by the progress made around the

"disabled", the establishment of "minimum service" in transport and in

developing countries by the unavoidable extension of major roads and public

transport.

Mobility is a key and strategic activity of modern life. Both in developed and

developing countries, one can hardly understand any professional life, leisure,

study, friendship, community or cultural activities or even family life, without a

relatively large capacity for movement. An increasing proportion of the activities

of daily life takes place "in mobility", rather than in fixed locations only. The

improvement of technologies has made mobility easier: quicker transport, more

services to help people to organise their trips (from the GPS to the travel

agency) and obviously more choices (between types of transport and tools used

to organise journeys). This rise in the number of tools and types of transport,

makes mobility choices very strategic and subsequently prompts people to

consider mobility not only as a need but also as an opportunity.

A wide scope of analysis

We aim to analyse the present and the future of sustainable mobility both in

developed countries and emerging countries. To this end, we will have to

examine the contrasts between the features of mobility in these two groups of

countries. These differences are referred as “the mobility divide” (or ―the

mobility opportunity divide‖), which corresponds to the wide disparity in mobility

opportunities that currently exist between the mobility options available to the

average citizen in the poorest developing regions and those experienced today

by the average citizen in the developed world.

Furthermore, we aim to encompass in our analysis both physical mobility (the

actual transportation of goods and people) and virtual mobility (the use of the

internet and telecommunications technology, or ICT) to connect people to

people and people to goods.

In 1998, Andreas Schafer, in his book The future mobility of the world

population, pointed out that in the early 1960s two-thirds of the distance made

were by the OECD countries. 30 years later, this figure stood at just over 50%.

This evolution of the demand and the transport dynamic towards developing

countries will be a focal point of our study.

Taking into account the specificities of mobility issues between developed and

developing countries, and analysing the development and limits of virtual and

physical mobility, we will explain what sustainable mobility is made for, how and

what benefits players can draw from it.

Mobility is almost a

human right

Mobility is active,

universal and strategic

From the poorest to the

richest

Both physical and

virtual mobility

8

Mobility and its dynamics over the long term:

towards Hypermobility

The emergence of the "Global Village" (M. McLuhan)

In 1964, Marshall McLuhan popularised the notion of ―global village‖ in his book,

Understanding Media: ―Today, after more than a century of electric technology,

we have extended our central nervous system itself in a global embrace,

abolishing both space and time as far as our planet is concerned‖.

The ―global village‖ defined by Marshall McLuhan was enabled by:

the surge in car use and the development of major roads which have

fostered people‘s autonomy and mobility

the triumph of container transport by sea and by air which has made the

long-distance goods transportation of goods easier and cheaper than before

the opening up of trade barriers and frontiers thanks to new global

regulations (WTO, Schengen Area, etc.)

Whilst in 1950, five hundred and fifty million tons of goods were traded between

the US, Europe and Asia, by 2010 trade between this regions amounted to 7

trillion tons!

Nonetheless, one has to mention that this global village was defined before it

actually existed. Indeed, although in the 60s physical mobility was clearly

improving, it was in the 90s that the internet was making the global village real.

Note that today, the term "Global Village" is mostly used as a metaphor to

describe the World Wide Web. By enabling people to interact and share

information easily from all over the world, this technology fosters the idea of a

global village in which everyone can be informed and react quickly on what is

happening in other regions, other countries.

Is virtual mobility a substitute for physical mobility? In the early 1990s,

people were becoming aware of the need for reducing greenhouse gases and

other issues due to the development of transport (congestion, road casualties

etc.). Therefore, the development of the internet and the mobile phone could

have been a way to substitute for travel. However, total travel volumes have

continued to grow and the impact of virtual mobility has not been able to reverse

this trend. There are reasons to believe that IT has fostered people‘s desire to

travel, as it facilitates more contacts in a given time over larger distances, and

that these contacts generate the need or willingness to meet face-to-face. That

is why we can describe this trend as a kind of ―virtual mobility‖ which is fully a

part of our life‘s mobility.

Everyday strategic hypermobility!

The academic article “Green Mobility: the evolution of transport” published in

2000 by the Rockefeller University of New York pointed out some human

instincts related to mobility defined by Yacov Zahavi in 1980.

Yacov Zahavi measured travel time in the 1970s: the result was about one

hour per day over the year and the entire adult population. What is surprising is

that recent measures give the same result; the travel time budget was also

about one hour 5,000 years ago. This can be explained by the fact that some

activities are being rationalised (bulk purchases in supermarkets, working all

day long), others were being replaced by remote contacts (relationship banking,

making appointments), while others grow (accompanying children, visits and

leisure especially among inactive).

Another human instinct mentioned by Yacov Zahavi is that of returning to the

lair in the evening. This ―homing instinct‖ lies at the heart of airlines‘ success.

“Shoes and the

smartphone are the

emblems of Homo

Mobilis”

The internet increases

willingness to meet face-

to-face

Transport: about one

hour a day

9

Airbus Industries found that about 60% of air passengers in Europe do their

business and return on the same day, notwithstanding the higher fare.

Finally, Yacov Zahavi highlighted the fact that humans are territorial animals.

The objective of territorial animals is to have as large a territory as possible

within the natural limits of the possibilities to acquire and manage it. Most of

human history is a bloody testimony to the instinct to maximise range. For

humans, a large accessible territory means greater liberty in choosing the three

points of gravity of lives: the home, the workplace, and the school. Four-fifths of

all travel ends in this ambit.

These elements allow drawing a kind of rational model in the Weber

perspective, on the production of mobility and its transformations in the long

term. Jean-Pierre Orfeuil in the academic report “Imagine tomorrow’s mobility”

published in 2005, points out that individual players are not "minimisers" of cost,

but "maximisers‖ of opportunities: they leverage the best of city resources and

conditions of mobility (in terms of price, speed and modes network structure) in

an envelope of money and time budget data.

Ultimately, individuals develop important organisational skills. The activities

which require transport and movements are less routine, times and places

frequented are now more varied than yesterday.

Overview of passenger and freight transport

worldwide

Obviously, more and more people are travelling: from one street to another,

from one city to another, from one country to another. But, what is more difficult

is to describe the global modal split in passenger transport i.e. evaluate the

number of km travelled by road/train/bus/metro/sea/air. The main difficulty

stems from the lack of information about transport particularly from developing

countries which do not have set up yet efficient tools to collect transport data.

The OECD database can provide us with transport statistics since the 1970s but

not every year for every country; figures for China every year, for example, are

not published. The most accurate and exhaustive available statistics are those

from the UE as all members have to collect transport data which is regularly

compiled by Eurostat.

Overview of passenger transport

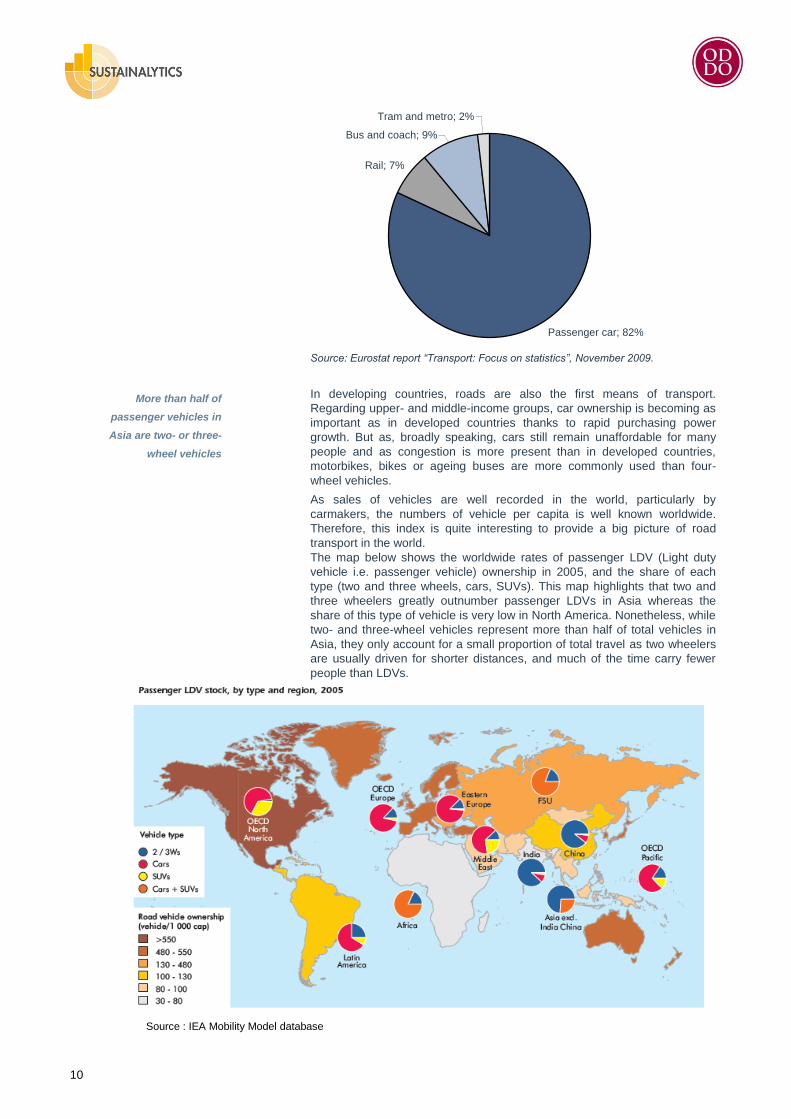

Passenger transport: roads dominate overall

One of the mean features about passenger transport in the world is that both

in developing and developed countries, roads remain the means of

transport of choice for much of the population.

In developed countries, urbanisation has always been vehicle-oriented: most

residents have a strong preference for travelling in the comfortable, air-

conditioned motors cars that are often among their proudest possession.

The Car is one of the symbols of The Glorious Thirty (1950s-1970s), owning

a car was often considered the symbol of success and in a way complies

with the consumer society‘s desire for autonomy and individuality. As shown

in the graph below, transport by passenger cars dominates by far in the EU-

27 (82%) and by including ―bus and coaches‖, roads correspond to 91% of

the km travelled by passengers in the EU.

Most of European

business men are day-

trippers

Four-fifths of travel is

between the home, the

workplace and the school

A vehicle-oriented

urbanisation in developed

countries

10

Source: Eurostat report “Transport: Focus on statistics”, November 2009.

In developing countries, roads are also the first means of transport.

Regarding upper- and middle-income groups, car ownership is becoming as

important as in developed countries thanks to rapid purchasing power

growth. But as, broadly speaking, cars still remain unaffordable for many

people and as congestion is more present than in developed countries,

motorbikes, bikes or ageing buses are more commonly used than four-

wheel vehicles.

As sales of vehicles are well recorded in the world, particularly by

carmakers, the numbers of vehicle per capita is well known worldwide.

Therefore, this index is quite interesting to provide a big picture of road

transport in the world.

The map below shows the worldwide rates of passenger LDV (Light duty

vehicle i.e. passenger vehicle) ownership in 2005, and the share of each

type (two and three wheels, cars, SUVs). This map highlights that two and

three wheelers greatly outnumber passenger LDVs in Asia whereas the

share of this type of vehicle is very low in North America. Nonetheless, while

two- and three-wheel vehicles represent more than half of total vehicles in

Asia, they only account for a small proportion of total travel as two wheelers

are usually driven for shorter distances, and much of the time carry fewer

people than LDVs.

Passenger transport in the EU-27 by type of transport, 2006 -% in km

Passenger car; 82%

Rail; 7%

Bus and coach; 9%

Tram and metro; 2%

More than half of

passenger vehicles in

Asia are two- or three-

wheel vehicles

Source : IEA Mobility Model database

11

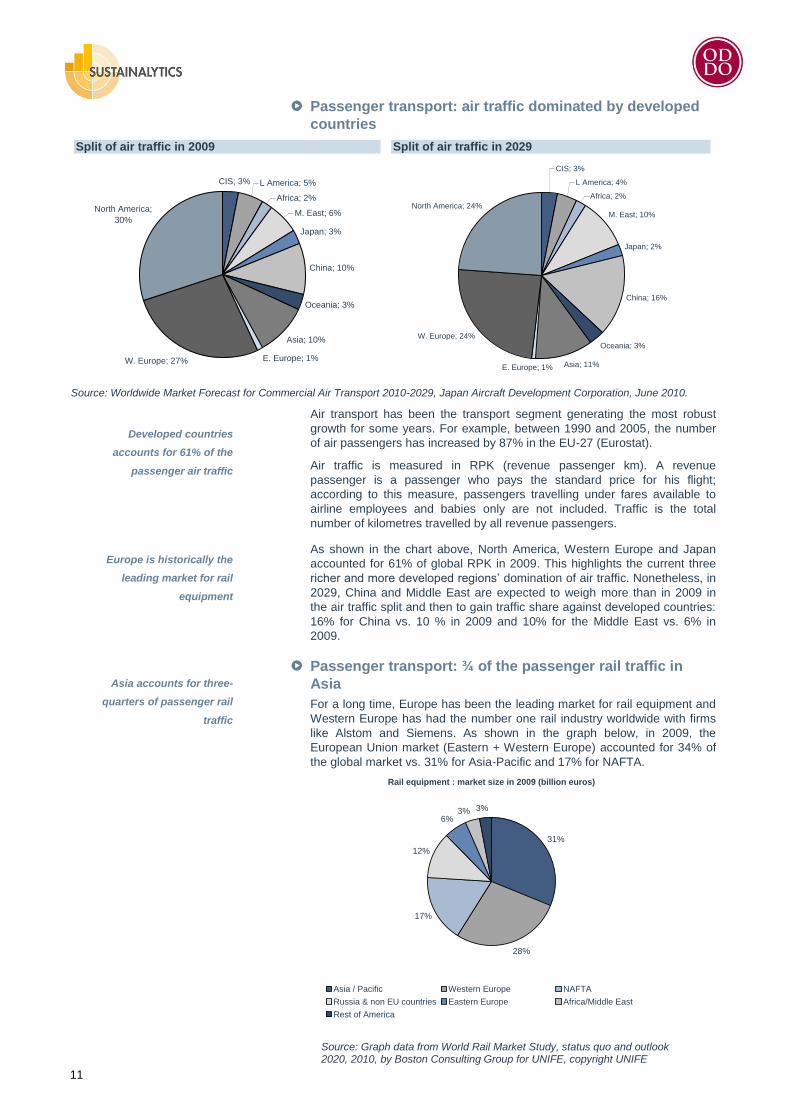

Passenger transport: air traffic dominated by developed

countries

Split of air traffic in 2009 Split of air traffic in 2029

Source: Worldwide Market Forecast for Commercial Air Transport 2010-2029, Japan Aircraft Development Corporation, June 2010.

Air transport has been the transport segment generating the most robust

growth for some years. For example, between 1990 and 2005, the number

of air passengers has increased by 87% in the EU-27 (Eurostat).

Air traffic is measured in RPK (revenue passenger km). A revenue

passenger is a passenger who pays the standard price for his flight;

according to this measure, passengers travelling under fares available to

airline employees and babies only are not included. Traffic is the total

number of kilometres travelled by all revenue passengers.

As shown in the chart above, North America, Western Europe and Japan

accounted for 61% of global RPK in 2009. This highlights the current three

richer and more developed regions‘ domination of air traffic. Nonetheless, in

2029, China and Middle East are expected to weigh more than in 2009 in

the air traffic split and then to gain traffic share against developed countries:

16% for China vs. 10 % in 2009 and 10% for the Middle East vs. 6% in

2009.

Passenger transport: ¾ of the passenger rail traffic in

Asia

For a long time, Europe has been the leading market for rail equipment and

Western Europe has had the number one rail industry worldwide with firms

like Alstom and Siemens. As shown in the graph below, in 2009, the

European Union market (Eastern + Western Europe) accounted for 34% of

the global market vs. 31% for Asia-Pacific and 17% for NAFTA.

Splt of air traffic in 2009

CIS; 3% L America; 5%

Africa; 2%

M. East; 6%

Japan; 3%

China; 10%

Oceania; 3%

Asia; 10%

E. Europe; 1%W. Europe; 27%

North America;

30%

Split of air traffic 2029

CIS; 3%

L America; 4%

Africa; 2%

M. East; 10%

Japan; 2%

China; 16%

Oceania; 3%

Asia; 11%E. Europe; 1%

W. Europe; 24%

North America; 24%

Rail equipment : market size in 2009 (billion euros)

31%

28%

17%

12%

6%3% 3%

Asia / Pacific Western Europe NAFTA

Russia & non EU countries Eastern Europe Africa/Middle East

Rest of America

Developed countries

accounts for 61% of the

passenger air traffic

Europe is historically the

leading market for rail

equipment

Asia accounts for three-

quarters of passenger rail

traffic

Source: Graph data from World Rail Market Study, status quo and outlook 2020, 2010, by Boston Consulting Group for UNIFE, copyright UNIFE

12

In 2009, for the first time, Asia/Pacific‘s market size overtook that of Western

Europe. This illustrates the relative saturation of the Western Europe market

compared to the vast opportunities presented by Asian countries in terms of

rail infrastructure demand. Asia, thanks to its demographic size, already

dominates passenger rail traffic: in 2010, the area accounted for three-

quarters of the world's mainline passenger rail traffic with India and

China alone representing half of the worldwide traffic.2

The market trend is obviously in favour of rail development thanks to

emerging market growth, the global awareness on environmental issues and

soaring oil prices. Thus, between 2007 and 2009, the rail market grew by

5.8% whilst global GDP expanded by just 1%.

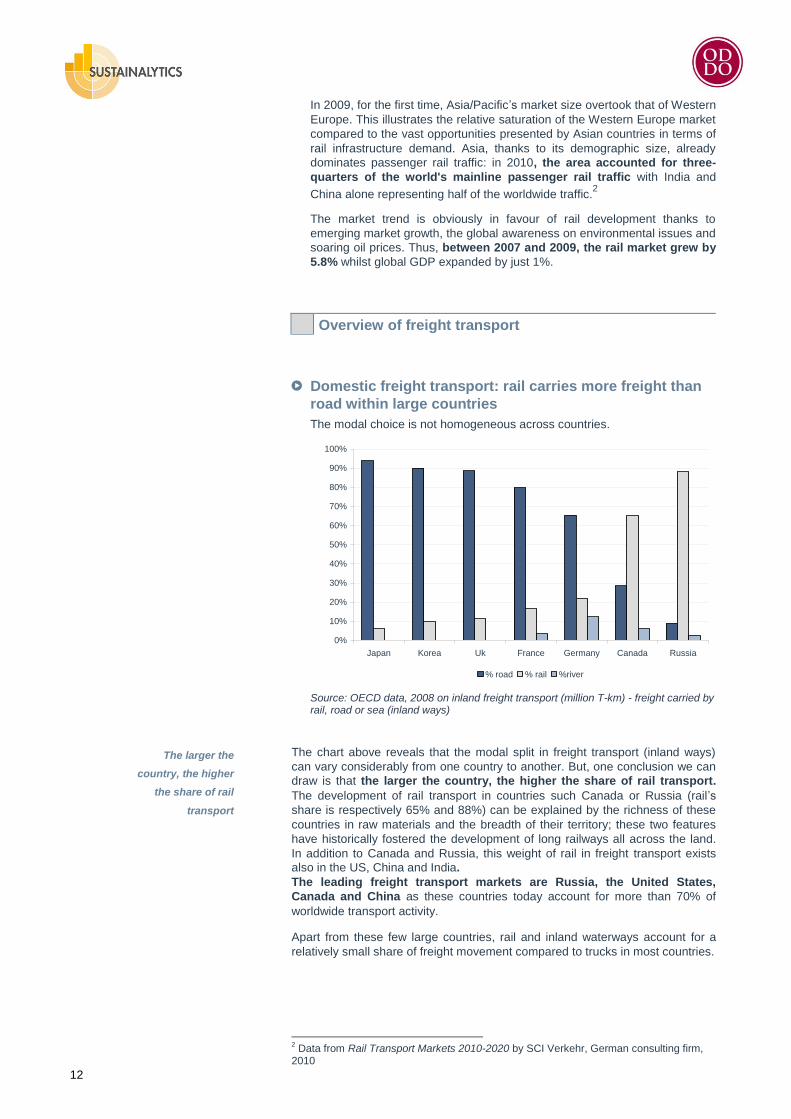

Overview of freight transport

Domestic freight transport: rail carries more freight than

road within large countries

The modal choice is not homogeneous across countries.

Source: OECD data, 2008 on inland freight transport (million T-km) - freight carried by rail, road or sea (inland ways)

The chart above reveals that the modal split in freight transport (inland ways)

can vary considerably from one country to another. But, one conclusion we can

draw is that the larger the country, the higher the share of rail transport.

The development of rail transport in countries such Canada or Russia (rail‘s

share is respectively 65% and 88%) can be explained by the richness of these

countries in raw materials and the breadth of their territory; these two features

have historically fostered the development of long railways all across the land.

In addition to Canada and Russia, this weight of rail in freight transport exists

also in the US, China and India.

The leading freight transport markets are Russia, the United States,

Canada and China as these countries today account for more than 70% of

worldwide transport activity.

Apart from these few large countries, rail and inland waterways account for a

relatively small share of freight movement compared to trucks in most countries.

2 Data from Rail Transport Markets 2010-2020 by SCI Verkehr, German consulting firm,

2010

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Japan Korea Uk France Germany Canada Russia

% road % rail %river

The larger the

country, the higher

the share of rail

transport

13

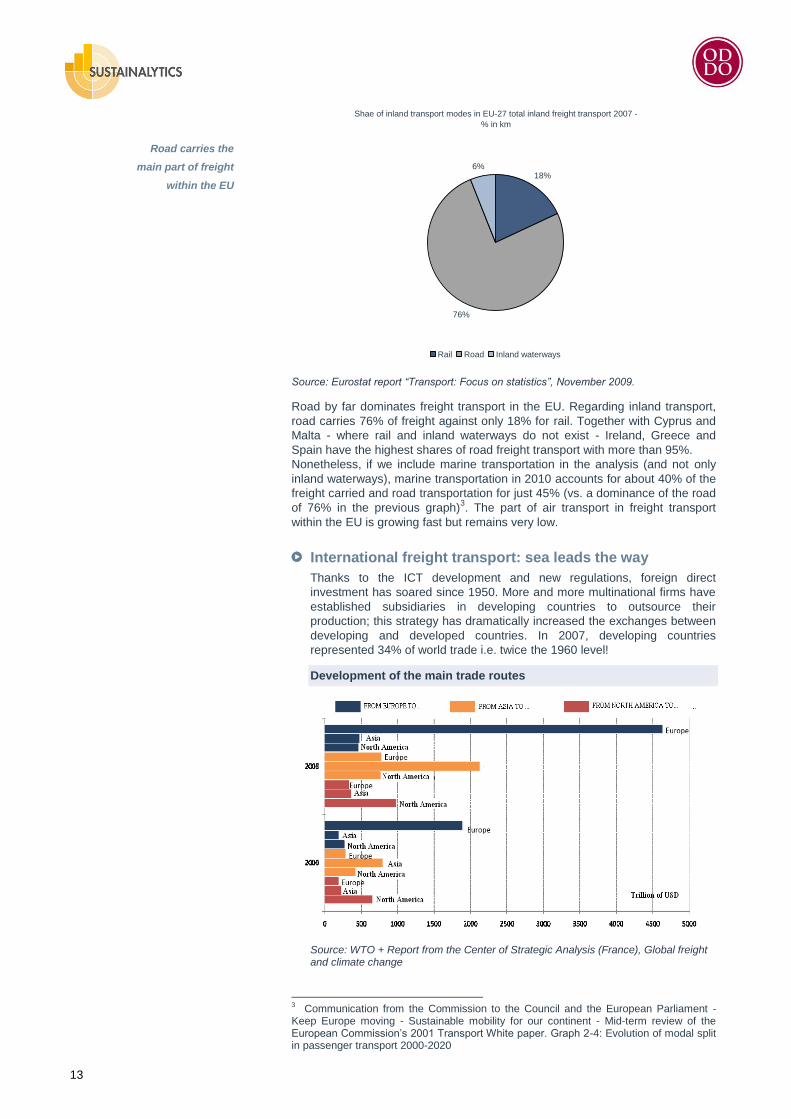

Source: Eurostat report “Transport: Focus on statistics”, November 2009.

Road by far dominates freight transport in the EU. Regarding inland transport,

road carries 76% of freight against only 18% for rail. Together with Cyprus and

Malta - where rail and inland waterways do not exist - Ireland, Greece and

Spain have the highest shares of road freight transport with more than 95%.

Nonetheless, if we include marine transportation in the analysis (and not only

inland waterways), marine transportation in 2010 accounts for about 40% of the

freight carried and road transportation for just 45% (vs. a dominance of the road

of 76% in the previous graph)3. The part of air transport in freight transport

within the EU is growing fast but remains very low.

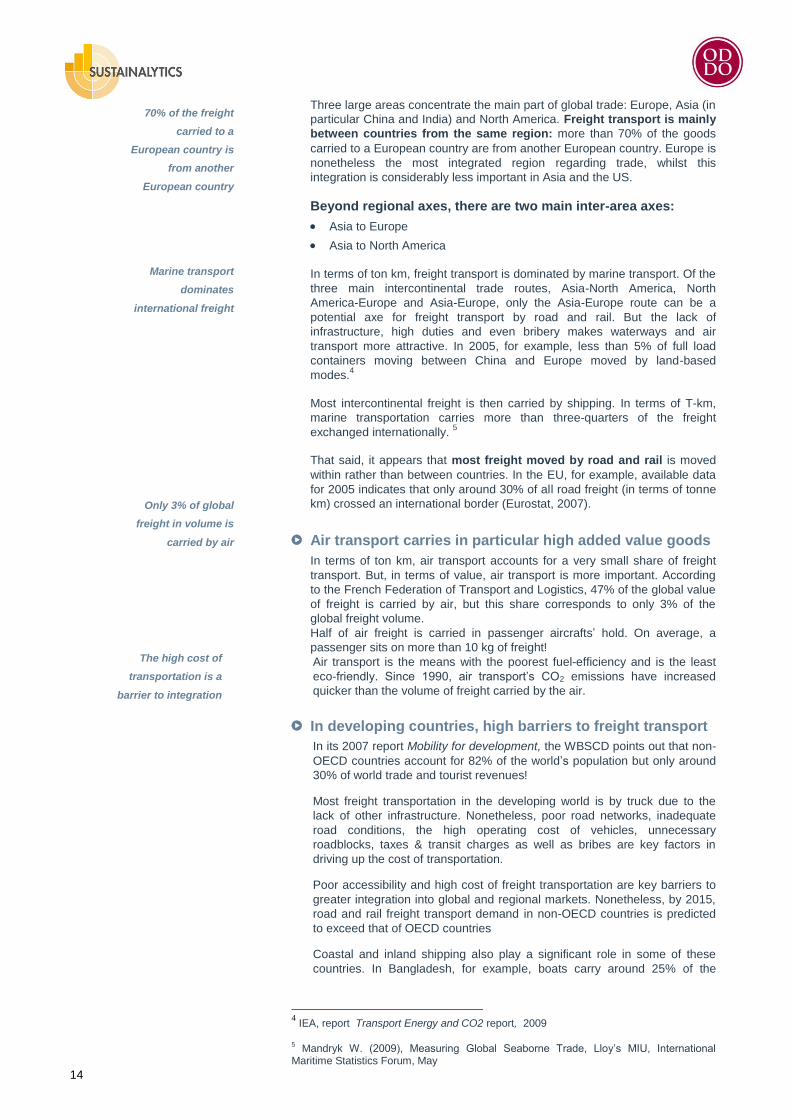

International freight transport: sea leads the way

Thanks to the ICT development and new regulations, foreign direct

investment has soared since 1950. More and more multinational firms have

established subsidiaries in developing countries to outsource their

production; this strategy has dramatically increased the exchanges between

developing and developed countries. In 2007, developing countries

represented 34% of world trade i.e. twice the 1960 level!

Development of the main trade routes

Source: WTO + Report from the Center of Strategic Analysis (France), Global freight and climate change

3 Communication from the Commission to the Council and the European Parliament -

Keep Europe moving - Sustainable mobility for our continent - Mid-term review of the European Commission‘s 2001 Transport White paper. Graph 2-4: Evolution of modal split in passenger transport 2000-2020

Shae of inland transport modes in EU-27 total inland freight transport 2007 -

% in km

18%

76%

6%

Rail Road Inland waterways

Road carries the

main part of freight

within the EU

14

Three large areas concentrate the main part of global trade: Europe, Asia (in

particular China and India) and North America. Freight transport is mainly

between countries from the same region: more than 70% of the goods

carried to a European country are from another European country. Europe is

nonetheless the most integrated region regarding trade, whilst this

integration is considerably less important in Asia and the US.

Beyond regional axes, there are two main inter-area axes:

Asia to Europe

Asia to North America

In terms of ton km, freight transport is dominated by marine transport. Of the

three main intercontinental trade routes, Asia-North America, North

America-Europe and Asia-Europe, only the Asia-Europe route can be a

potential axe for freight transport by road and rail. But the lack of

infrastructure, high duties and even bribery makes waterways and air

transport more attractive. In 2005, for example, less than 5% of full load

containers moving between China and Europe moved by land-based

modes.4

Most intercontinental freight is then carried by shipping. In terms of T-km,

marine transportation carries more than three-quarters of the freight

exchanged internationally. 5

That said, it appears that most freight moved by road and rail is moved

within rather than between countries. In the EU, for example, available data

for 2005 indicates that only around 30% of all road freight (in terms of tonne

km) crossed an international border (Eurostat, 2007).

Air transport carries in particular high added value goods

In terms of ton km, air transport accounts for a very small share of freight

transport. But, in terms of value, air transport is more important. According

to the French Federation of Transport and Logistics, 47% of the global value

of freight is carried by air, but this share corresponds to only 3% of the

global freight volume.

Half of air freight is carried in passenger aircrafts‘ hold. On average, a

passenger sits on more than 10 kg of freight!

Air transport is the means with the poorest fuel-efficiency and is the least

eco-friendly. Since 1990, air transport‘s CO2 emissions have increased

quicker than the volume of freight carried by the air.

In developing countries, high barriers to freight transport

In its 2007 report Mobility for development, the WBSCD points out that non-

OECD countries account for 82% of the world‘s population but only around

30% of world trade and tourist revenues!

Most freight transportation in the developing world is by truck due to the

lack of other infrastructure. Nonetheless, poor road networks, inadequate

road conditions, the high operating cost of vehicles, unnecessary

roadblocks, taxes & transit charges as well as bribes are key factors in

driving up the cost of transportation.

Poor accessibility and high cost of freight transportation are key barriers to

greater integration into global and regional markets. Nonetheless, by 2015,

road and rail freight transport demand in non-OECD countries is predicted

to exceed that of OECD countries

Coastal and inland shipping also play a significant role in some of these

countries. In Bangladesh, for example, boats carry around 25% of the

4 IEA, report Transport Energy and CO2 report, 2009

5 Mandryk W. (2009), Measuring Global Seaborne Trade, Lloy‘s MIU, International

Maritime Statistics Forum, May

70% of the freight

carried to a

European country is

from another

European country

Marine transport

dominates

international freight

Only 3% of global

freight in volume is

carried by air

The high cost of

transportation is a

barrier to integration

15

country‘s freight. In the Mekong delta area of Vietnam, over two-thirds of

freight is carried by inland waterways.

Global trends of mobility

Trends in passenger transport

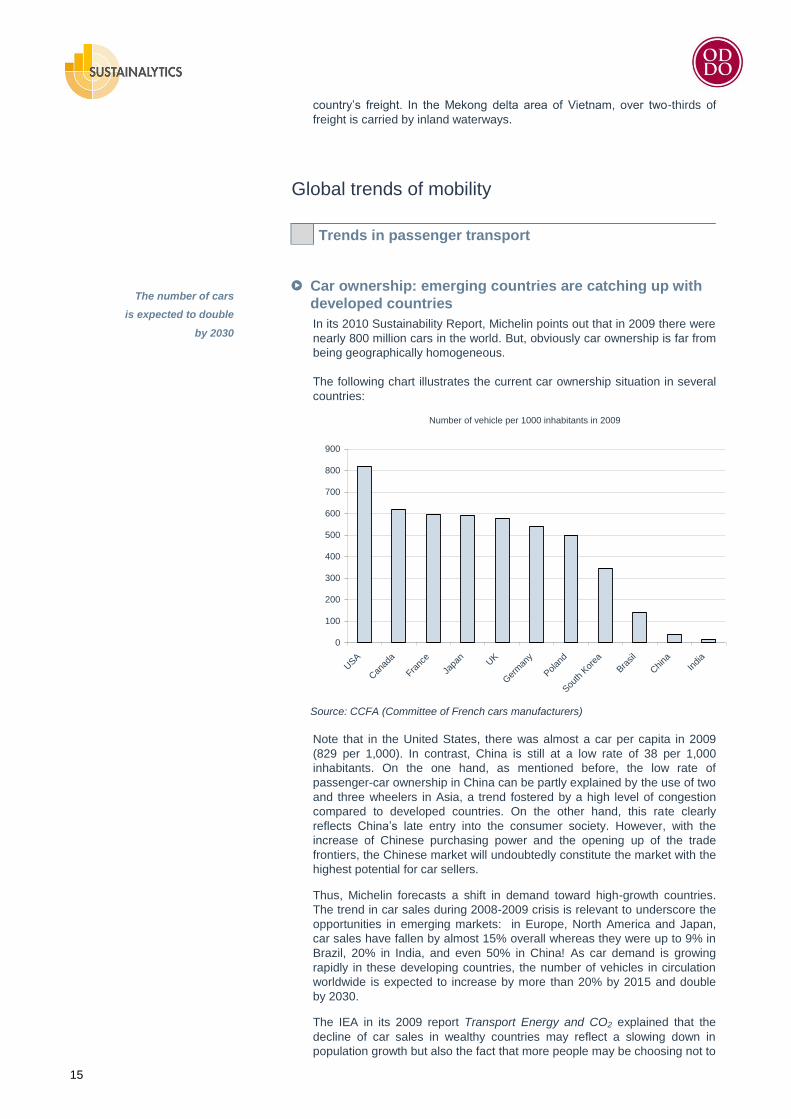

Car ownership: emerging countries are catching up with

developed countries

In its 2010 Sustainability Report, Michelin points out that in 2009 there were

nearly 800 million cars in the world. But, obviously car ownership is far from

being geographically homogeneous.

The following chart illustrates the current car ownership situation in several

countries:

Source: CCFA (Committee of French cars manufacturers)

Note that in the United States, there was almost a car per capita in 2009

(829 per 1,000). In contrast, China is still at a low rate of 38 per 1,000

inhabitants. On the one hand, as mentioned before, the low rate of

passenger-car ownership in China can be partly explained by the use of two

and three wheelers in Asia, a trend fostered by a high level of congestion

compared to developed countries. On the other hand, this rate clearly

reflects China‘s late entry into the consumer society. However, with the

increase of Chinese purchasing power and the opening up of the trade

frontiers, the Chinese market will undoubtedly constitute the market with the

highest potential for car sellers.

Thus, Michelin forecasts a shift in demand toward high-growth countries.

The trend in car sales during 2008-2009 crisis is relevant to underscore the

opportunities in emerging markets: in Europe, North America and Japan,

car sales have fallen by almost 15% overall whereas they were up to 9% in

Brazil, 20% in India, and even 50% in China! As car demand is growing

rapidly in these developing countries, the number of vehicles in circulation

worldwide is expected to increase by more than 20% by 2015 and double

by 2030.

The IEA in its 2009 report Transport Energy and CO2 explained that the

decline of car sales in wealthy countries may reflect a slowing down in

population growth but also the fact that more people may be choosing not to

Number of vehicle per 1000 inhabitants in 2009

0

100

200

300

400

500

600

700

800

900

USA

Can

ada

Franc

e

Japa

nUK

Ger

man

y

Polan

d

Sou

th K

orea

Bra

sil

China

India

The number of cars

is expected to double

by 2030

16

own an automobile or as a family choose to own only one vehicle instead of

two or more. Recent surveys in Japan show that the younger generation

has to some degree lost some interest in cars and focuses more on new

communication devices such as mobile phones or laptop computers.

But in developing countries, rates of car ownership are growing rapidly,

suggesting that mass transit options are insufficient. Many families

purchase LDVs as soon as they can afford them. The emergence of low-

cost cars, such as the Tata Nano in India, will probably further accelerate

LDV ownership rates. The number of motorised two wheelers also

continues to grow rapidly. Indeed, as congestion is more and more acute,

two wheelers may still be the easiest way to get around.

Urban and conventional rail growth driven by China and

India, potential technological breakthrough expected

Rail growth was and will be driven by megatrends such as population

growth, road congestion, urbanisation and new sustainable development

issues.

Concerning conventional rail: according to Unife (Union of European

Railway Industry), the global rail equipment market is expected to grow

by 2.4% per year until 2016.

Concerning urban rail (metro, bus, and tram): the International union of

railways (in its 2008 report) expects to see an average increase of 3%

per year of the market until 2020.

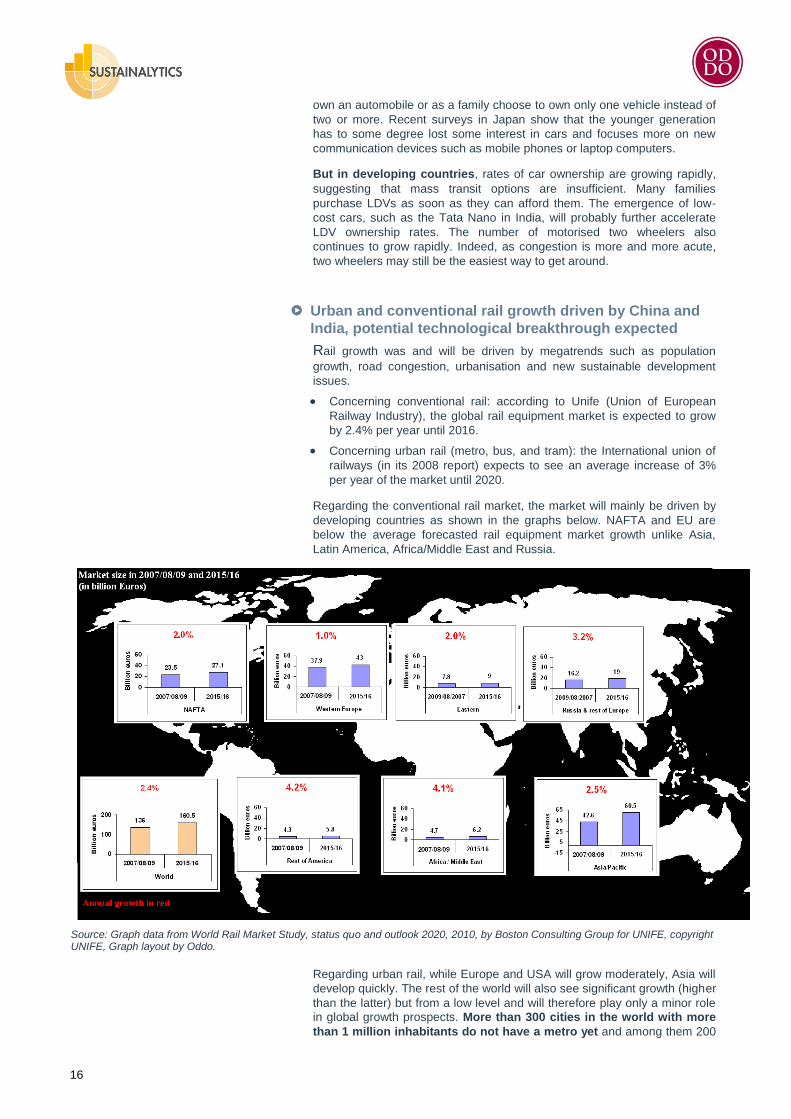

Regarding the conventional rail market, the market will mainly be driven by

developing countries as shown in the graphs below. NAFTA and EU are

below the average forecasted rail equipment market growth unlike Asia,

Latin America, Africa/Middle East and Russia.

Source: Graph data from World Rail Market Study, status quo and outlook 2020, 2010, by Boston Consulting Group for UNIFE, copyright UNIFE, Graph layout by Oddo.

Regarding urban rail, while Europe and USA will grow moderately, Asia will

develop quickly. The rest of the world will also see significant growth (higher

than the latter) but from a low level and will therefore play only a minor role

in global growth prospects. More than 300 cities in the world with more

than 1 million inhabitants do not have a metro yet and among them 200

17

are located in Asia; these figures highlight the high potential of the urban rail

market in Asia.

High population growth, ever-increasing per capita GDP and extensive

investment in rail infrastructure will see China and India continue to drive

growth.

China is likely to bring around 2000 km of new metro lines into service in

the next ten years. Similarly, India is also investing heavily in new

metros, with rapid expansion underway in Delhi and new projects in

several cities.

Long-distance passenger rail will enjoy strong growth due to high-speed

rail projects. In China, 13,000 km of new high-speed lines will be

completed by 2012. Furthermore, Western Europe will benefit from new

lines in Spain, Italy and France as the European Commission aims to

hold 50% of the freight and passenger transport market by train and

waterways by 2050.

Air transport: one-third of the 2009-2029 deliveries of

aircrafts will be for Asia Pacific airlines!

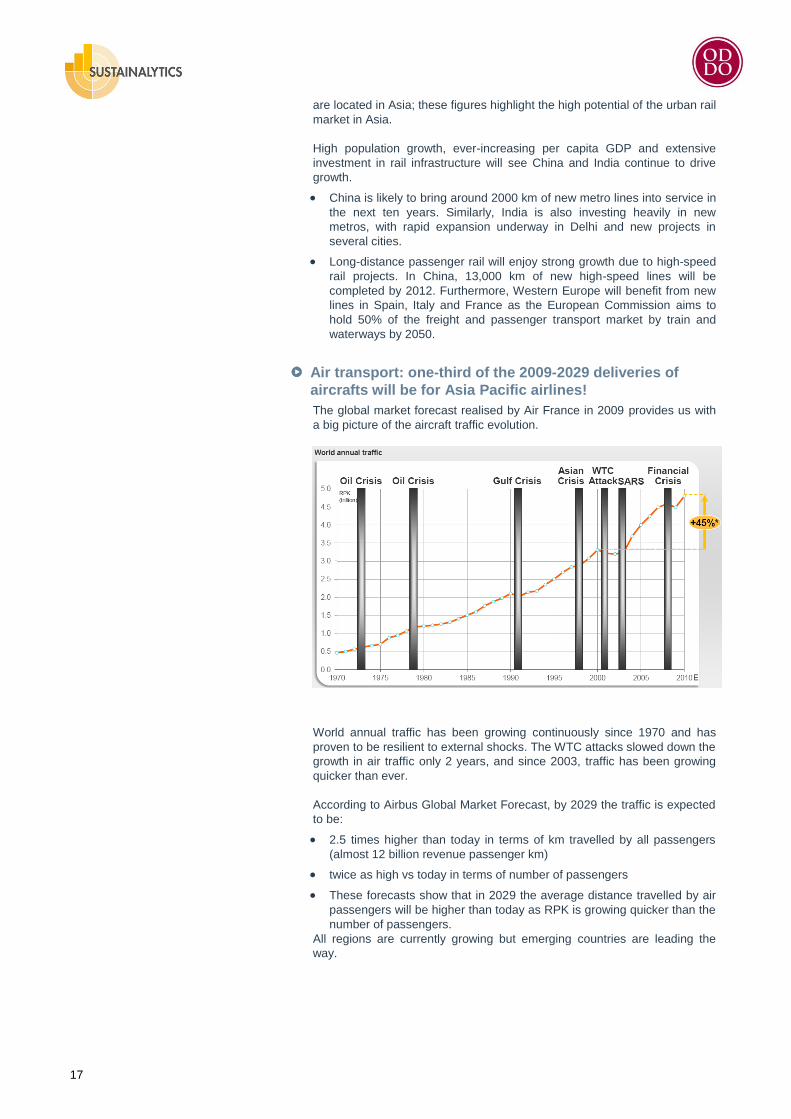

The global market forecast realised by Air France in 2009 provides us with

a big picture of the aircraft traffic evolution.

World annual traffic has been growing continuously since 1970 and has

proven to be resilient to external shocks. The WTC attacks slowed down the

growth in air traffic only 2 years, and since 2003, traffic has been growing

quicker than ever.

According to Airbus Global Market Forecast, by 2029 the traffic is expected

to be:

2.5 times higher than today in terms of km travelled by all passengers

(almost 12 billion revenue passenger km)

twice as high vs today in terms of number of passengers

These forecasts show that in 2029 the average distance travelled by air

passengers will be higher than today as RPK is growing quicker than the

number of passengers.

All regions are currently growing but emerging countries are leading the

way.

18

Table below: passenger traffic

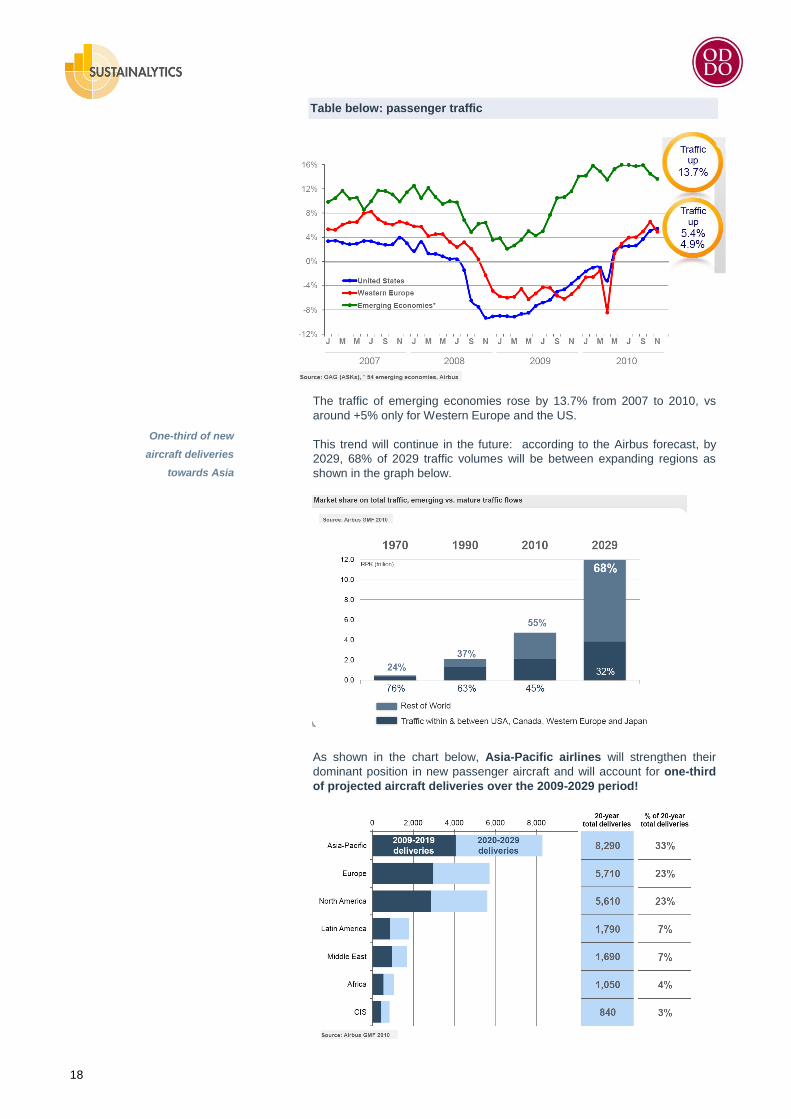

The traffic of emerging economies rose by 13.7% from 2007 to 2010, vs

around +5% only for Western Europe and the US.

This trend will continue in the future: according to the Airbus forecast, by

2029, 68% of 2029 traffic volumes will be between expanding regions as

shown in the graph below.

As shown in the chart below, Asia-Pacific airlines will strengthen their

dominant position in new passenger aircraft and will account for one-third

of projected aircraft deliveries over the 2009-2029 period!

One-third of new

aircraft deliveries

towards Asia

19

Trends in freight transport

Three factors will drive growth and the trend in freight

traffic worldwide:

1. Emerging countries’ spectacular growth: China and India will drive

growth in freight traffic. These two countries which currently represent

7% and 3% respectively of the world economy may represent 30% and

14% respectively by 2050 (against 29% for the EU and 27% for the US)

according to the CEPII (French Center of Forecast research and

financial information). Moreover, contrary to the EU and North America,

which mainly consume goods imported from neighbouring countries, the

new Asian emerging countries are more prone to export to developed

countries which may increasingly raise the average distance travelled by

goods. However, another scenario is that the increase of purchasing

power in the region (particularly in China, India and South Korea) makes

the demand enough to significantly increase trade within the Asian area.

In any case, the transport overview will clearly be modified.

2. Scarcity of resources: fuel prices will continue to rise which will

increase the appeal of fuel-efficient transport.

3. Climate change: the political implementation of environmental targets

will also favour fuel-efficient transport‘s appeal.

Positive momentum on worldwide rail freight: rail revival!

The three drivers mentioned above could logically lead to more public

funding concerning investment in railways. Indeed, rail is one of the most

fuel-efficient modes of transport and is compatible with the vast expanse of

a number of emerging countries (Brazil, China, and India). Thus, upgrades

and renewals along rail freight corridors are already being pushed ahead,

especially in India, China, the Middle East and Eastern Europe.

As rail is generally not as flexible as road transport and requires high

investment, many countries will be more inclined to promote an

intermodal system i.e. a partial transfer of freight from road to rail

through financial incentives or regulatory policies.

For already some years, the European Commission has considered

intermodal rail/road system an ideal solution to curb CO2 emissions. But its

words have not really been followed by actions. Indeed, in Europe, since

the 1970s, the share of freight transport carried by train has been

decreasing: the volume of goods carried by train was 16% in 2007 against

29% in 1970.6 The decline in rail can be explained by several reasons: less

industrial activity, greater volatility of the goods carried which makes road

flexibility more attractive, the relatively low price of fuel and, in many

countries, the huge investment made by governments in the development of

highways (6,000 km were built in France between 1970 and 2000) at the

expense of rail investment.

Air transport: Asia will triple its aircraft fleet

In spite of soaring fuel costs, air transport remains interesting for freight with

high added value. Indeed, for these products, the cost of transport is

generally less than 4% of the final price of sales. Then, even if fuel prices

are rising, air transport remains pertinent for this market range.

During the 2008-2009 crisis, which impacted air freight traffic, airline

companies reduced the number of air cargo and optimised the use of

storage room in the passenger aircraft. This leads us to believe that the

crisis and surging fuel price may have a positive effect on air transport GHG

6 French rail freight: the new battle of rail, Hubert HAENEL, François GERBAUD (French

Minister of Transport), February 2003

20

emissions as it has led some companies to make freight transport

optimisation a priority.

Like all the other means of transport, air transport growth will be driven by

development in Asia. Meanwhile, in European and US air markets, demand

is tending more towards the replacement of ageing aircrafts, Boeing

forecast that the number of aircraft in the Asia-Pacific fleet will nearly triple,

from 4,110 in 2009 to 12,200 in 2029. Half of the world‘s new traffic added

during the next 20 years will be to, from, or within the Asia-Pacific region as

the latter depends heavily on air cargo to transport goods over difficult

terrain and vast stretches of ocean.

Some of the world‘s largest and most efficient cargo operators compete to

transport high-value and time-sensitive exports to markets outside the

region. To modernise their fleets and meet the growing demand for air

travel, Asia-Pacific-based airlines will need more than 10,300 new aircraft,

valued at more than US$1.3 trillion, over the next 20 years.

China will remain the largest market for aircraft outside the United States.

Indeed, although high-speed rail is competitive in many short-haul markets,

(less than 800 km), efficient integration of rail and air transport can stimulate

demand for longer-haul air travel. China is forecast to take delivery of 4,330

new aircraft—including those from its own developing aircraft

programmes—valued at US$ 480 billion over the next 20 years.

Marine transportation adopts new strategy

Marine transportation is the least flexible transport since fixed costs are very

high. Then, the 2008-2009 crisis has considerably impacted freight carried

by vessels and consequently many vessels were totally inactive over the

period.

But, in a way, this inactivity had a positive effect: indeed, it led some owners

to scrap their older or less cost-effective vessels. But, in parallel, the crisis

implied the end of new vessel sales: Det Norkske Veritas assesses that

more than 300 orders for new cargo vessels were cancelled in May 2009.

Facing the surge in fuel price and the decrease in demand, some sea

carriers have adopted a new strategy: they negotiate with their clients an

increase of the time needed to transport the goods (i.e. lower vessel speed)

in exchange for transporting more goods (as they had many boats

available). As fuel consumption is correlated to speed cubed, decreasing

the vessel‘s speed can lead to significant cost savings!

Marine transport is one of the most fuel-efficient forms of transport and,

therefore, a key player in sustainable mobility in the future. But its relative

lack of flexibility and high cost implies the need for global regulation and

subsidies to:

foster its development vs growth in road and air transport

enable it to renew its ageing fleet to adopt new efficient vessels and

avoid further oil spills.

Virtual mobility or e-substitution

E-substitution consists in substituting displacements by distance services and

relations. At present, millions of people, particularly in developed countries,

instead of going directly to the bank or to the supermarket, order their new

credit card, buy a new dress, organise their next holidays, comfortably seated at

their computer. Thus, this virtual mobility or e-substitution is a relevant topic in

any discussion of mobility trends.

But virtual mobility doest not mean less physical mobility. Indeed, contrary to

what was expected in the 1990s, ICT has not resulted in a reduction of people‘s

mobility. ICT has fostered the desire of people to meet other people with whom

they interact on the World Wide Web. Some 800 million people are today

600 million people

belong to the

community!

21

members of the Facebook community and this figure is expected to double in

a few years.

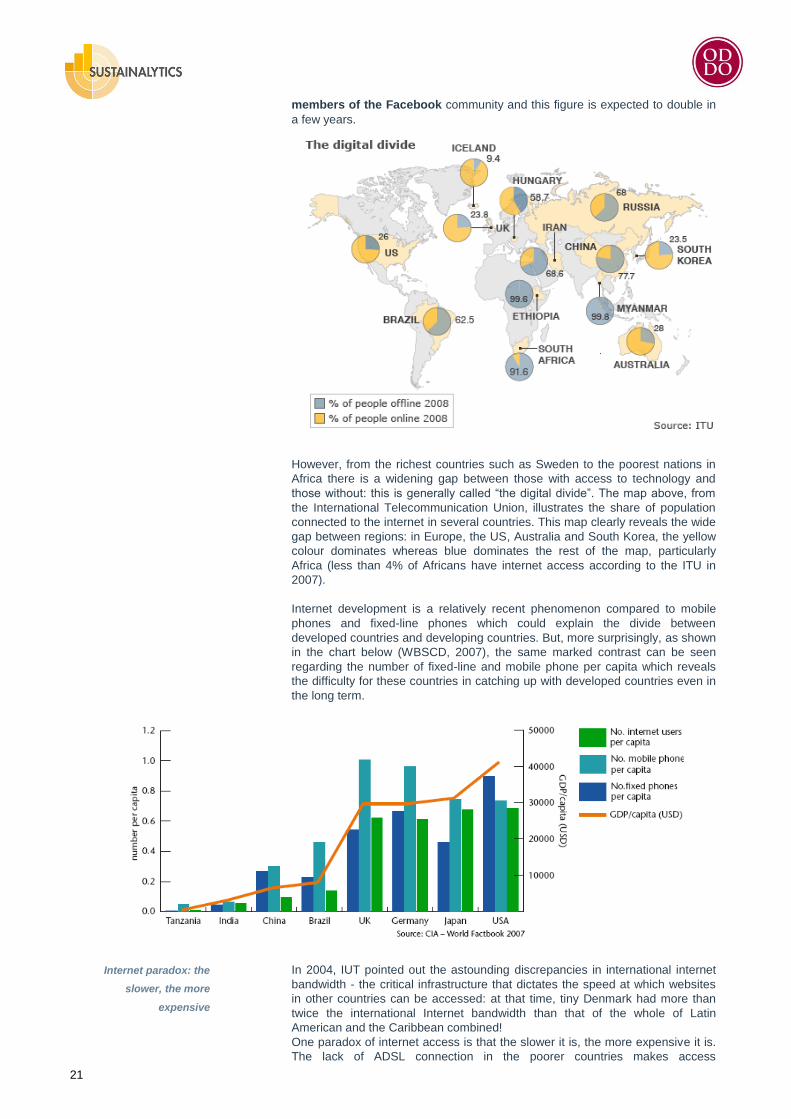

However, from the richest countries such as Sweden to the poorest nations in

Africa there is a widening gap between those with access to technology and

those without: this is generally called ―the digital divide‖. The map above, from

the International Telecommunication Union, illustrates the share of population

connected to the internet in several countries. This map clearly reveals the wide

gap between regions: in Europe, the US, Australia and South Korea, the yellow

colour dominates whereas blue dominates the rest of the map, particularly

Africa (less than 4% of Africans have internet access according to the ITU in

2007).

Internet development is a relatively recent phenomenon compared to mobile

phones and fixed-line phones which could explain the divide between

developed countries and developing countries. But, more surprisingly, as shown

in the chart below (WBSCD, 2007), the same marked contrast can be seen

regarding the number of fixed-line and mobile phone per capita which reveals

the difficulty for these countries in catching up with developed countries even in

the long term.

In 2004, IUT pointed out the astounding discrepancies in international internet

bandwidth - the critical infrastructure that dictates the speed at which websites

in other countries can be accessed: at that time, tiny Denmark had more than

twice the international Internet bandwidth than that of the whole of Latin

American and the Caribbean combined!

One paradox of internet access is that the slower it is, the more expensive it is.

The lack of ADSL connection in the poorer countries makes access

Internet paradox: the

slower, the more

expensive

22

unaffordable for the lion‘s share of the inhabitants. According to the World Bank,

connection fees in Africa are the highest: between US$ 250 and US$ 300 per

month!

Beyond this global view, one can add that the digital divide can also be

observed within countries on the same continent, regions in the same countries,

cities in the same region. In 2006, 37% of Europeans stated that they do not

have any knowledge of computing (Demunter, 2006) and 10% of European

senior citizens are internet users.

The revolution in motion: the new paradigms of

mobility

Unavoidably slow innovation

Over the last decade, the main players in mobility have intended to improve the

ESG impacts of mobility via innovation capacity and improved technologies.

Today‘s trend is to rely on people as well. The framework of this report not only

highlights technological aspects of sustainable mobility, it also takes into

account a change in the behaviour of travellers. Indeed, in order to be more

efficient, sustainable mobility should combine both technological improvement

and behavioural change. This is what we call the new paradigms of mobility.

Financial inertia 7 Demand channelling of the scale necessary to produce major reductions

in GHG emissions would not, however, produce ―quick‖ results. While each

individual makes decisions relating to transport use every day, most of

these decisions are constrained by decisions that have been taken decades

or even centuries ago. Some of these decisions can be altered relatively

quickly – in a matter of days or months. But many require a much longer

period to take effect if unacceptable disruption is to be avoided.

Over short periods of one or two years, most of the technological and

physical characteristics of transport systems, most of the demand-related

location and transport use characteristics and many of the behavioural

response patterns of transport users are largely fixed. As a result, many

demand channelling measures at best can have only a very limited impact

on personal travel choices and goods transport arrangements over such

periods.

Most studies of the impact of changes in the price of transport fuel, the

imposition of road tolls or altering the relative price of shipping freight by

road versus rail, for example, have found that the impact of these measures

on total transport activity or on the modal mix of transport activity over

periods of one or two years is likely to be relatively small. Studies of the

responsiveness of personal transportation demand generally find that a 1%

increase in the cost of transport reduces transport demand by about one-

tenth of one percent (VTPI 2003). This is a significant response.

But it is not large enough to produce a major change in the trajectory of

transport activity, especially when other factors (like income growth) are

working to keep transport activity growing.

It was only in the 1960s that Europe and Japan began to achieve mass

motorisation. The US interstate highway system was begun in the 1950s.

With the exception of Germany, Europe‘s motorways developed in the

1970s. The first enclosed shopping mall appeared in the US in the mid

1950s. The Japanese ―bullet train‖ began operating in 1964 and the French

high speed train in 1981. Air transport did not become a significant mode of

mass long-distance travel until the 1970s. International container shipping

has been a significant freight transport mode only during the past 30 years.

Overnight package delivery service over distances of several thousand

7 Mobility 2030 - meeting the challenges to sustainability - WBCSD

Sustainable mobility

combines both

technological and

behavioural

improvements

Innovation takes

time to spread

23

miles is no more than a couple of decades old. Each of these transport

innovations was responsible for major changes in the volume and/or pattern

of transport activity. Each took several decades for its full impact to be felt.

There are many demand-led measures that, in theory, can impact the total

volume of transport activity, the modal mix of transport activity or both. But

the impact of these measures over the short to medium term when

aggregated at a national and/or regional level appears relatively small –

meaning that their potential as a tool for directly reducing transport-related

GHG emissions is likely to be quite limited.

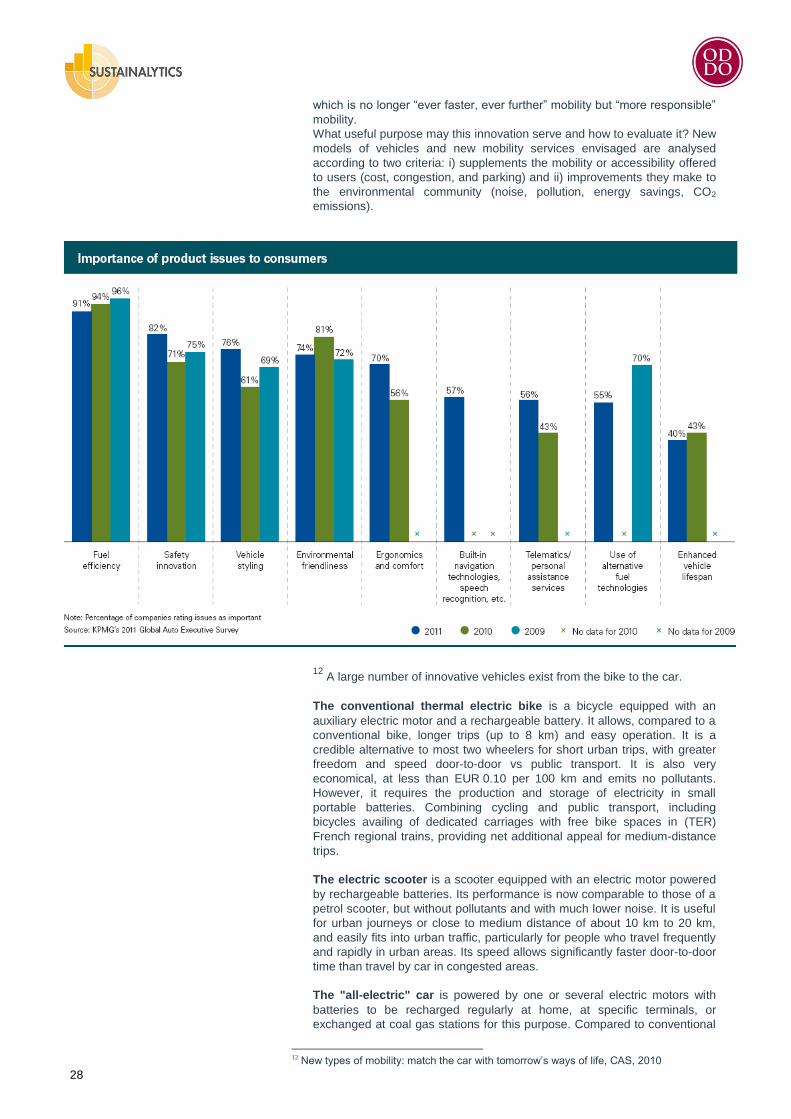

Cultural inertia 8 In KPMG‘s Global Automotive Survey 2011, Bernd Pichler, Managing

Director at Volkswagen (China) states that most customers want to be

environmentally friendly but don‘t want to compromise on performance‖.

Total sales of hybrid/EV are still expected to lag well behind traditional

internal combustion-powered cars due to some significant challenges that

have not yet been resolved, including safety, reliability, comfort, image and

undoubtedly cost.

As indicated by Georges Amar in his book Homo Mobilis – the new age of

mobility, since the existence of statistics on the subject, the first decline in

the number of miles travelled by automobiles in the USA was seen in mid-

2008!

Political inertia is a structural weight

Governments are an important player in terms of shaping the transport or

mobility landscape. Crucial investments in infrastructure have traditionally

been driven by public policies. Note, in particular, that the development and

expansion of the road and railway systems in different countries in the past

decade could not have been achieved without public financing. However, in

the past years a political inertia is becoming evident stemming from

financial and cultural constraints (public investment, heavy inconvenience of

public transport works), strategic industries (oil, automotive, aviation, etc.)

and lobbying activities.

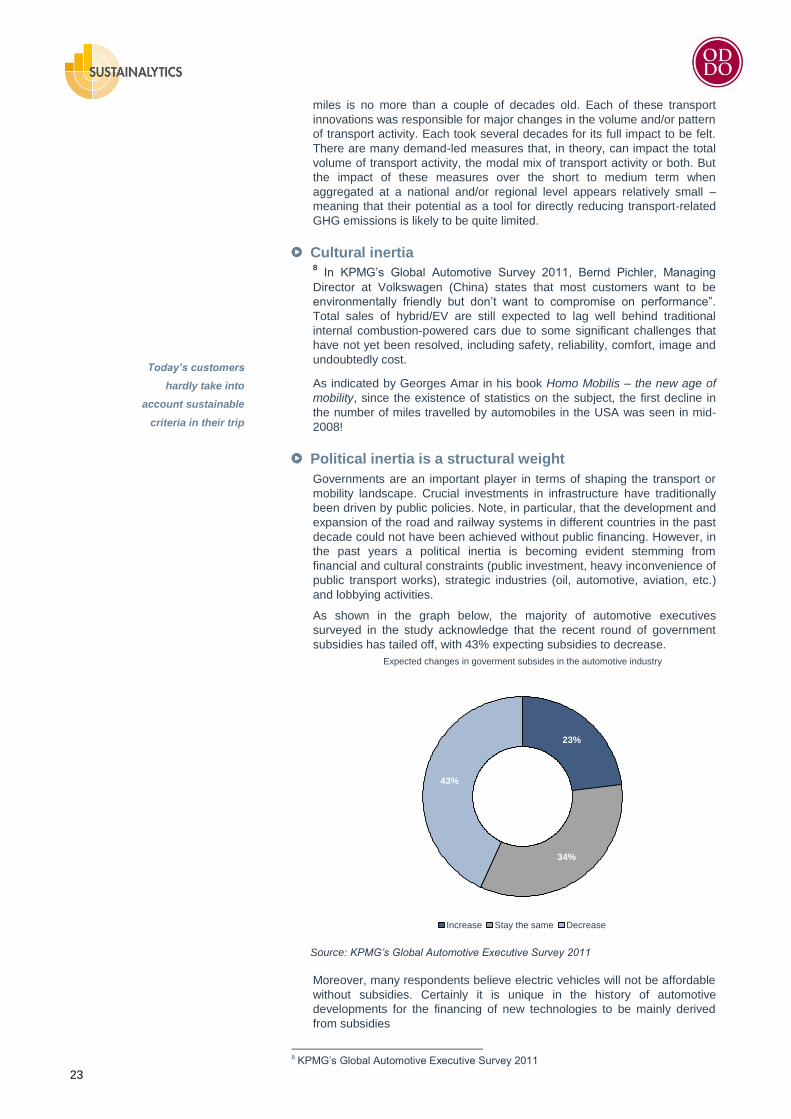

As shown in the graph below, the majority of automotive executives

surveyed in the study acknowledge that the recent round of government

subsidies has tailed off, with 43% expecting subsidies to decrease.

Source: KPMG’s Global Automotive Executive Survey 2011

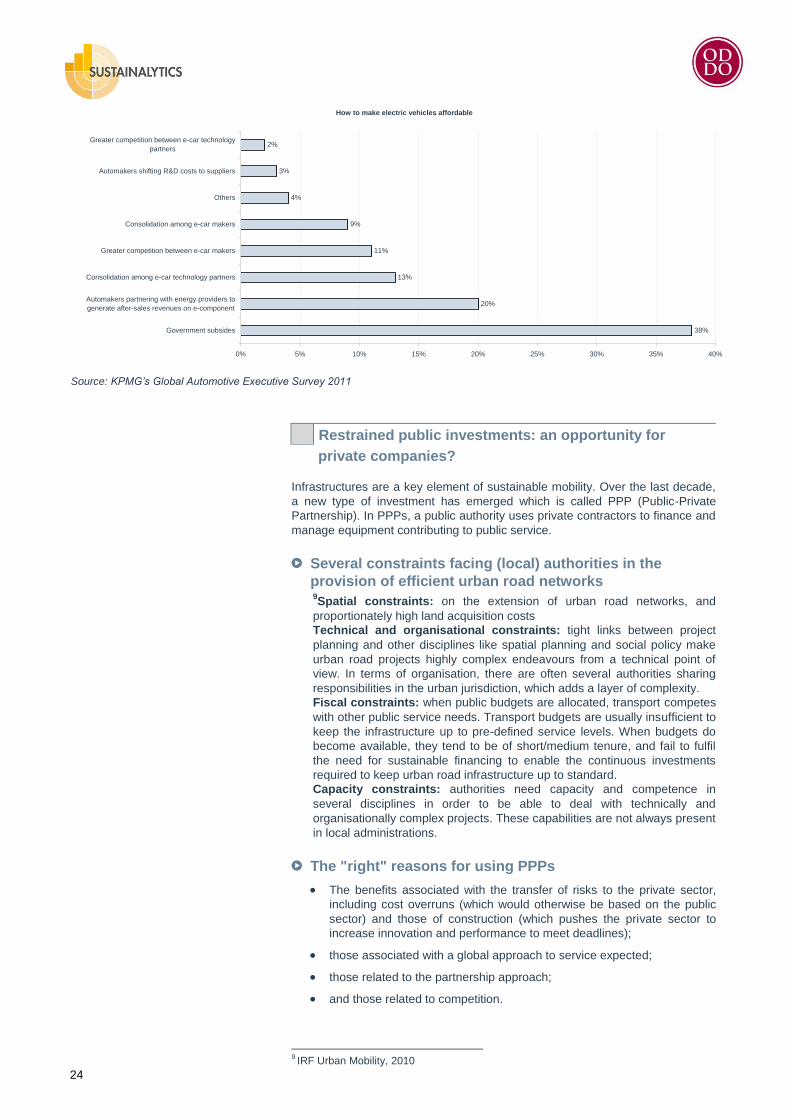

Moreover, many respondents believe electric vehicles will not be affordable

without subsidies. Certainly it is unique in the history of automotive

developments for the financing of new technologies to be mainly derived

from subsidies

8 KPMG‘s Global Automotive Executive Survey 2011

Expected changes in goverment subsides in the automotive industry

23%

34%

43%

Increase Stay the same Decrease

Today’s customers

hardly take into

account sustainable

criteria in their trip

24

Source: KPMG’s Global Automotive Executive Survey 2011

Restrained public investments: an opportunity for

private companies?

Infrastructures are a key element of sustainable mobility. Over the last decade,

a new type of investment has emerged which is called PPP (Public-Private

Partnership). In PPPs, a public authority uses private contractors to finance and

manage equipment contributing to public service.

Several constraints facing (local) authorities in the

provision of efficient urban road networks 9Spatial constraints: on the extension of urban road networks, and

proportionately high land acquisition costs

Technical and organisational constraints: tight links between project

planning and other disciplines like spatial planning and social policy make

urban road projects highly complex endeavours from a technical point of

view. In terms of organisation, there are often several authorities sharing

responsibilities in the urban jurisdiction, which adds a layer of complexity.

Fiscal constraints: when public budgets are allocated, transport competes

with other public service needs. Transport budgets are usually insufficient to

keep the infrastructure up to pre-defined service levels. When budgets do

become available, they tend to be of short/medium tenure, and fail to fulfil

the need for sustainable financing to enable the continuous investments

required to keep urban road infrastructure up to standard.

Capacity constraints: authorities need capacity and competence in

several disciplines in order to be able to deal with technically and

organisationally complex projects. These capabilities are not always present

in local administrations.

The "right" reasons for using PPPs

The benefits associated with the transfer of risks to the private sector,

including cost overruns (which would otherwise be based on the public

sector) and those of construction (which pushes the private sector to

increase innovation and performance to meet deadlines);

those associated with a global approach to service expected;

those related to the partnership approach;

and those related to competition.

9 IRF Urban Mobility, 2010

How to make electric vehicles affordable

38%

20%

13%

11%

9%

4%

3%

2%

0% 5% 10% 15% 20% 25% 30% 35% 40%

Government subsides

Automakers partnering with energy providers to

generate after-sales revenues on e-component

Consolidation among e-car technology partners

Greater competition between e-car makers

Consolidation among e-car makers

Others

Automakers shifting R&D costs to suppliers

Greater competition between e-car technology

partners

25

Urban PPPs cover a wide diversity of possible schemes

Urban congestion charging: schemes which impose a fee on vehicles

entering a certain cordoned area within an urban zone, implemented

through partnership contracts pursuant to which both the public authority

and private contractor concerned bear financial risks.

Urban toll roads: toll motorways in urban areas that are the object of

concessions granted to private operators. The private operator generally

designs, constructs, maintains and operates the road in exchange for the

right to levy tolls from the users. High Occupancy Toll (HOT) lanes would

also come under this working definition.

Combined road and real estate development: PPP schemes in which

functions/aspects like road development, housing development and/or

business accommodation are combined to attain optimum quality and

enable cross-subsidising of project-elements so as to promote a viable

business case.

Urban road operation partnerships: schemes under PPP that aim to

make better use of existing urban road infrastructure capacity by using

Intelligent Transport Systems (ITS). Projects concerning parking

partnerships and interfacing with other modalities, like mass transit systems

and rail, could also be included in this category.

Long-term maintenance contracts for urban road networks: schemes

under PPP addressing long-term maintenance (sometimes including

upgrading) of the urban network, in which revenues are performance-

based.

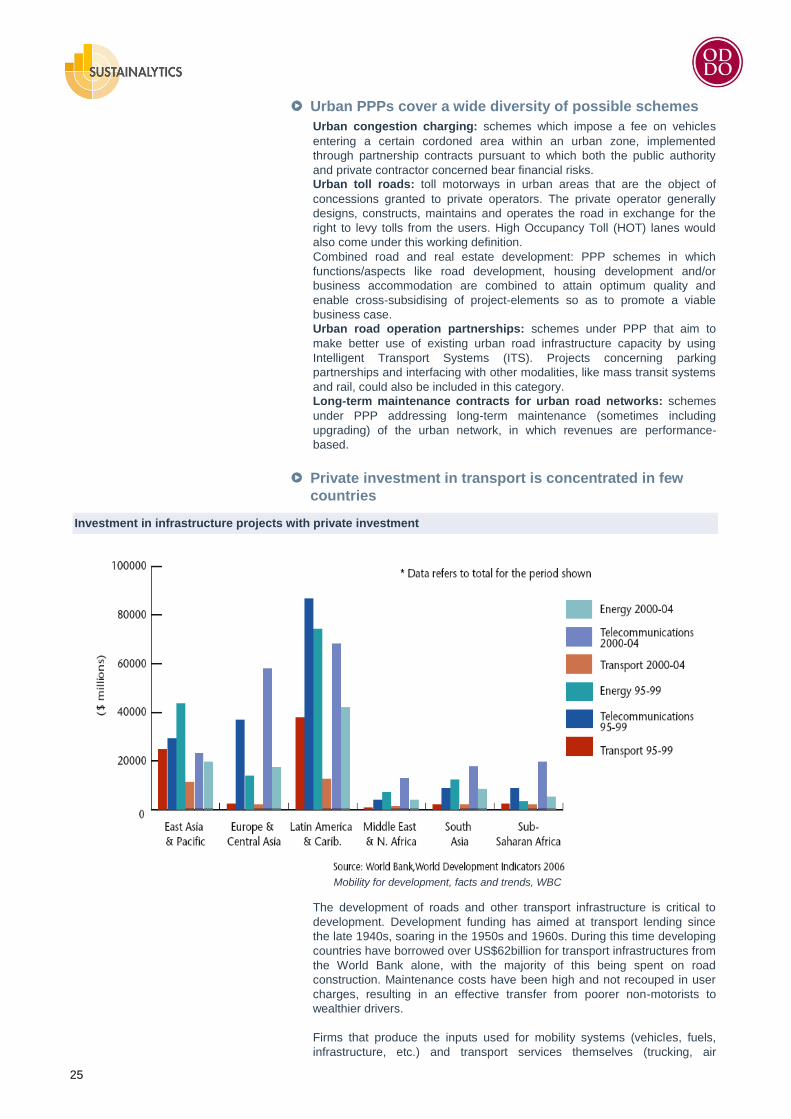

Private investment in transport is concentrated in few

countries

Investment in infrastructure projects with private investment

Mobility for development, facts and trends, WBC

The development of roads and other transport infrastructure is critical to

development. Development funding has aimed at transport lending since

the late 1940s, soaring in the 1950s and 1960s. During this time developing

countries have borrowed over US$62billion for transport infrastructures from

the World Bank alone, with the majority of this being spent on road

construction. Maintenance costs have been high and not recouped in user

charges, resulting in an effective transfer from poorer non-motorists to

wealthier drivers.

Firms that produce the inputs used for mobility systems (vehicles, fuels,

infrastructure, etc.) and transport services themselves (trucking, air

26

transport, shipping, rail transport and ICT) have an essential stake in the

financial sustainability of mobility. For the mobility opportunity divide, these

companies need to be attracted to invest and provide services to the

poorest countries and communities currently underserved by transportation.

The World Bank‘s Private Participation in Infrastructure (PPI) Project

database tracks infrastructure projects in developing countries that involve

private participation in funding and risk-taking. During the fifteen-year period

spanning 1990 to 2004, it showed early growth but a subsequent decline of

private investments in transport. This investment is highly concentrated in a

few countries, with only six accounting for nearly 80% percent of the total

investment shown: China (18%), Brazil (16%), Malaysia (11%), Mexico

(11%), Argentina (11%) and Chile (10%). In most of the other one hundred-

fifty or so developing and transition countries, new private finance for

transport infrastructure has varied from little to none. In all cases both

energy and telecommunications attract higher levels of private investment

than transport infrastructure, but the disparities are greater in those

developing regions such as sub-Saharan Africa and South Asia which are

attracting the least investment overall.

Towards a mutation of uses

For a long time, travelling was considered a tiring activity. People used to take a

means of transport at a scheduled time, from a defined point, to reach a place.

The journey was either long or not; travellers were quite passive (almost like

goods!). Nowadays, even given that the modernisation of transport allows faster

and more comfortable journeys, we are in a new age of mobility. Indeed, we are

witnessing a shift in use whereby the traveller has become more active. The

use of internet, applications on smartphones, more environmentally-friendly

innovations and the constant growth of motorisation in emerging countries have

led the way to the end of the ―ever faster, ever further‖ era. Along with

technology improvement, sustainable mobility implies a change in the behaviour

of travellers.

The empowerment of the traveller: the digital revolution 10

What if mobility did not concern vehicles but smartphones? The new

information technologies and communications that have invaded our daily

lives illustrate how we can integrate and simplify mobility. New phones that

have the ability to interact with their immediate environment provide

travellers with a continuity of information in time and space. Through their

flexibility, they improve the conditions for purchasing transport tickets,

service access and integration modes. By their values of modernity and

innovation, they improve the image of public transport and provide a unique

opportunity to attract new customers. So there is a close integration

between true mobility and digital mobility. The management of this new

intelligence involves partnerships and collaborations with unprecedented

telecom operators, software publishers, manufacturers, packagers, and

requires the commitment of all to the benefit of greater interaction of supply

and demand.

Some players already hold a key role for interactive sustainable mobility.

From an environmental point of view, companies such as Google and Tom-

Tom indicate to car drivers the shortest route from one point to another. As

a result they generate less greenhouse gas emissions.

From a social point of view, these companies are able to provide car drivers

with useful information such as alternative ways to avoid traffic congestions,

the quickest way (not always the shortest) to reach their final destination.

From a governance point of view, some public companies such as RATP,

SNCF (France) intend to provide pedestrians with a live update on

connections, or the forthcoming departures of trains/buses. While

Switzerland has a national coordinator for all means of transport and all

companies, this is not the case in France, where separate coordinators

provide updated information for their own traffic.

10

(European interviews newsletter, n°10 – 2nd semester)

Transport has not

benefited from private

investments over the

last decade

Smartphones represent a

revolutionary tool for 21st

century mobility

27

This new management of mobility makes the traveller more responsible and

active. In the near future, smartphone applications will give carbon

footprints to travellers from a point to another according to the means of

transport they use. In contrast, like raising awareness with shocking images

on cigarette packs, the carbon footprint aims to give a sense of

responsibility to travellers.

To adapt the “mobile life”: new services for people on the

move

With the modernisation of the mobile life, a number of services have been

created to fit with this new lifestyle

11

There are extensive opportunities for innovation in mobility services

Innovation in mobility stem from four sources which can be combined.

Innovative projects for vehicles and mobility services occupy media space,

advertising for car shows, video games. They shape the collective

imagination of developed countries: hybrid vehicles, small city cars, folding

electric bicycles, etc. However, these innovations remain largely at the

prototype stage, or even virtual, but the most advanced occupy only a few

niches which are not yet visible in statistics. They are derived mainly from

four sectors.

The massive use of bicycles. This is a trend observed not only in China

(where a large number of bikes are electrically assisted) or in other

countries in South-East Asia, but also in Europe. Despite urban

development organised around public transport, a number of European

cities have implemented systematic cycling policies, including Denmark and

the Netherlands. Cycling in urban areas is still underdeveloped in France,

although innovative actions have been initiated, such as self service

bicycles (Velib‘ in Paris launched by JCDecaux).

Small motorised vehicles. Many of these models, apparently new,

reinvented mobility systems, which are already widespread in some

emerging countries such as China or India (bicycle taxi, rickshaw) that are

in advance in this domain. Moreover, Japan has developed new concepts of

individual vehicles adapted to the mobility of older adults in dense crowds.

Smartphones. In all large cities, the latest generations of mobile phones,

with their localisation functions, have become a sign of modernity and the

main instrument for urban mobility: the "multi-purpose cell phone‖, a new

way of localisation and thinking within the city.

The development of a service economy. Whether for cycling or automotive

transport, users are increasingly seeking a reliable service, rather than

ownership of their means of transport. This now makes the development of

more elaborate forms of sales possible: from renting an article to supplying

a number of services, involving different transport (train + car, mobility cards

for public transports and car rentals, etc.)

Transport innovation: the heralded end of “ever further,

ever faster”?

Over the last century, mobility of both people and goods has always been

set to improve in terms of speed and making destinations ―closer‖.

However, have we reached a peak? Is our thinking still devoted to ―ever

further, ever faster‖, or are we moving towards more responsible mobility

(uptrend in the oil price, global warming, noise, multimodality issues, etc.)

It is obvious in everyday life: nowadays, advertisements on cars for

example do not highlight the speed characteristics as in the 1980s and

1990s but instead focus on CO2 emission/km, security characteristics, the

stop and go function, etc. It seems that we have entered into a new era

11

New types of mobility: match the car with tomorrow‘s ways of life, CAS, 2010

Development of a service

economy: towards the

purchase of services rather

than goods

28

which is no longer ―ever faster, ever further‖ mobility but ―more responsible‖

mobility.

What useful purpose may this innovation serve and how to evaluate it? New

models of vehicles and new mobility services envisaged are analysed

according to two criteria: i) supplements the mobility or accessibility offered

to users (cost, congestion, and parking) and ii) improvements they make to

the environmental community (noise, pollution, energy savings, CO2

emissions).

12

A large number of innovative vehicles exist from the bike to the car.

The conventional thermal electric bike is a bicycle equipped with an

auxiliary electric motor and a rechargeable battery. It allows, compared to a

conventional bike, longer trips (up to 8 km) and easy operation. It is a

credible alternative to most two wheelers for short urban trips, with greater

freedom and speed door-to-door vs public transport. It is also very

economical, at less than EUR 0.10 per 100 km and emits no pollutants.

However, it requires the production and storage of electricity in small

portable batteries. Combining cycling and public transport, including

bicycles availing of dedicated carriages with free bike spaces in (TER)

French regional trains, providing net additional appeal for medium-distance

trips.

The electric scooter is a scooter equipped with an electric motor powered

by rechargeable batteries. Its performance is now comparable to those of a

petrol scooter, but without pollutants and with much lower noise. It is useful

for urban journeys or close to medium distance of about 10 km to 20 km,

and easily fits into urban traffic, particularly for people who travel frequently

and rapidly in urban areas. Its speed allows significantly faster door-to-door

time than travel by car in congested areas.

The "all-electric" car is powered by one or several electric motors with

batteries to be recharged regularly at home, at specific terminals, or

exchanged at coal gas stations for this purpose. Compared to conventional

12 New types of mobility: match the car with tomorrow‘s ways of life, CAS, 2010

29

combustion vehicles, "all-electric" vehicles designed by car manufacturers

have a number of common characteristics:

Cost of manufacturing and use is currently higher than the equivalent

internal combustion vehicle, especially because of the price of batteries,

and requires public intervention to ensure their large-scale marketing

(less tax on the purchase or environmental bonus);

Their use implies the establishment of new rental infrastructure and

recharging batteries in the areas concerned, requiring the intervention of

new energy-supply operators, and the public authorities to adapt to the

road infrastructure;

Their energy efficiency is higher than equivalent internal combustion

vehicles, and CO2 emissions are totally dependent on the production of

electric power: very low in France (nuclear and recharge in off-peak

hours) and significantly higher in Europe on average (gas stations),

though declining because of European commitments from 2008 on

reducing greenhouse gas emissions by 2020. This performance also

depends on charging hours. Batteries offer an effective autonomy of

about 100 km to 150 km, which is adequate for daily mobility in urban

and suburban areas. However, these vehicles are still not suitable for

long-distance regarding the necessity of recharging.

Hybrid cars and plug-in hybrids use several different energy sources: a

gasoline engine and an electric motor powered by a battery (rechargeable),

with different techniques. Despite higher complexity and costs than the "all-

electric" car, this vehicle can both reduce energy consumption and urban

pollution, saving the liquid fuel (for miles driven with electric power) without

the drawback of limited autonomy (due to fossil fuel).

Use of renewable energies in vehicles is expected to increase. The EU

has planned a mandatory blending target of 10% for renewable energies by

2020. As shown in the graph below, the volume of renewable energy used

in the EU27 transport sector is expected to double by 2020.

The "low cost" vehicle is an economic model to minimise its cost, offer

attractive prices and the most competitive rates to drivers. These vehicles

meet a strong demand from users with average salaries: small size, limited