Embed Size (px)

Citation preview

1

Florian Leblanc

www.centre-cired.fr

ENGREF

16 Novembre 2016

Semaine Athens

Energie, économie et climat :Les enjeux des nouveaux hydrocarbures

non-conventionnels

Points abordés

Le pétrole et le gaz dans le mix énergétique mondiale

L’exploitation du pétrole

Notion de ressource – réserve

La théorie du peak oil

Scénarios sur la stratégie du Moyen-Orient

Les nouveaux hydrocarbures non-conventionnels

Impacts environnementaux

Cas des émissions fugitives de méthane

Nouvelle abondance énergétique ? Le cas US

2

Généralités : le pétrole et le gaz dans le mix énergétique mondiale

3

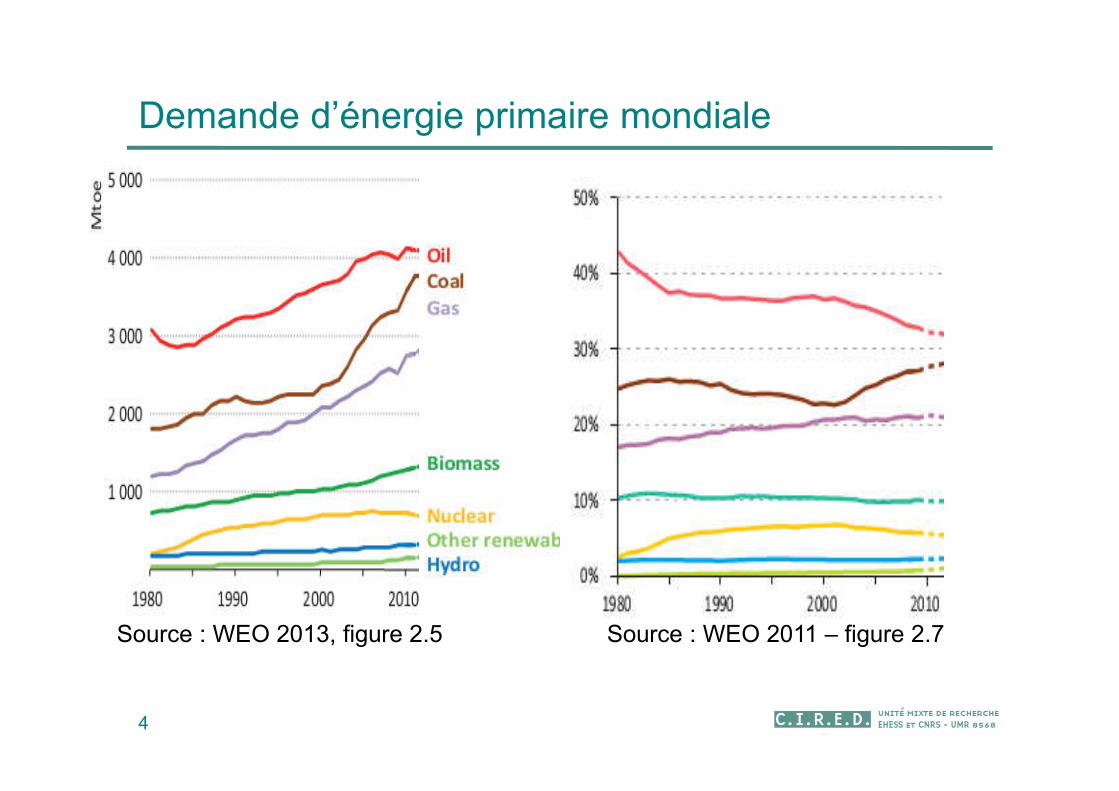

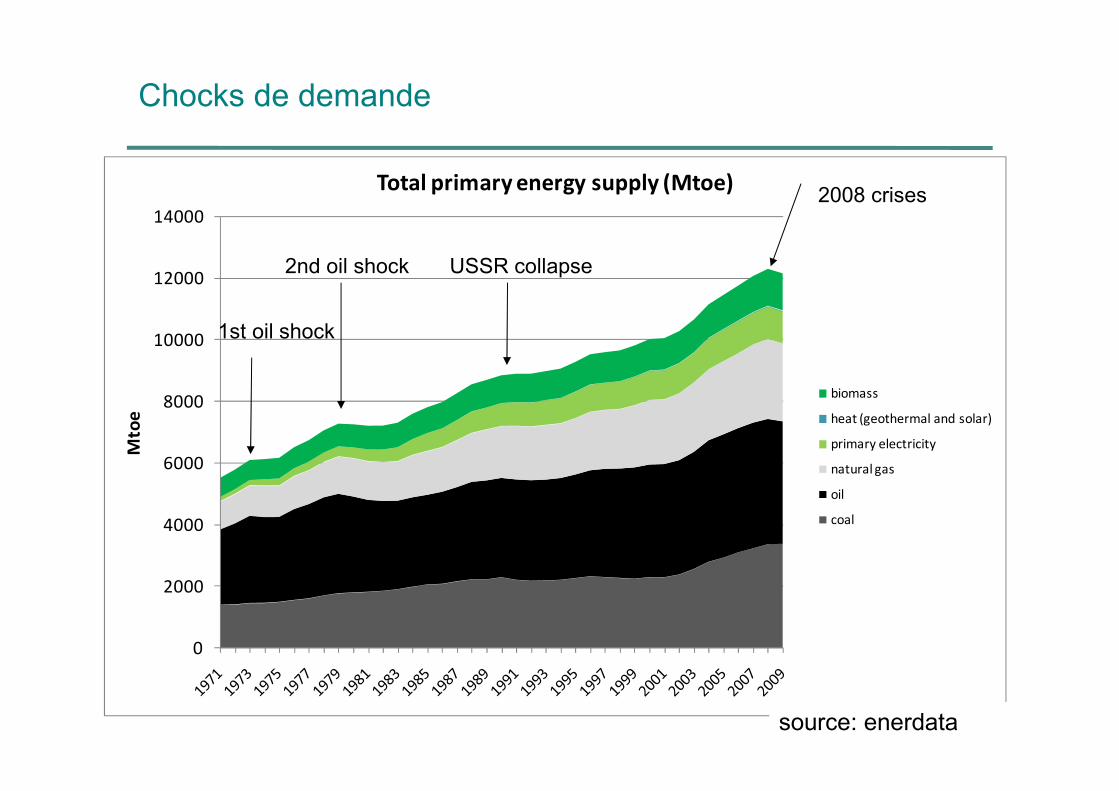

Demande d’énergie primaire mondiale

4

Source : WEO 2013, figure 2.5 Source : WEO 2011 – figure 2.7

0

2000

4000

6000

8000

10000

12000

14000

Mto

e

Total primary energy supply (Mtoe)

biomass

heat (geothermal and solar)

primary electricity

natural gas

oil

coal

1st oil shock

2nd oil shock USSR collapse

source: enerdata

Chocks de demande

2008 crises

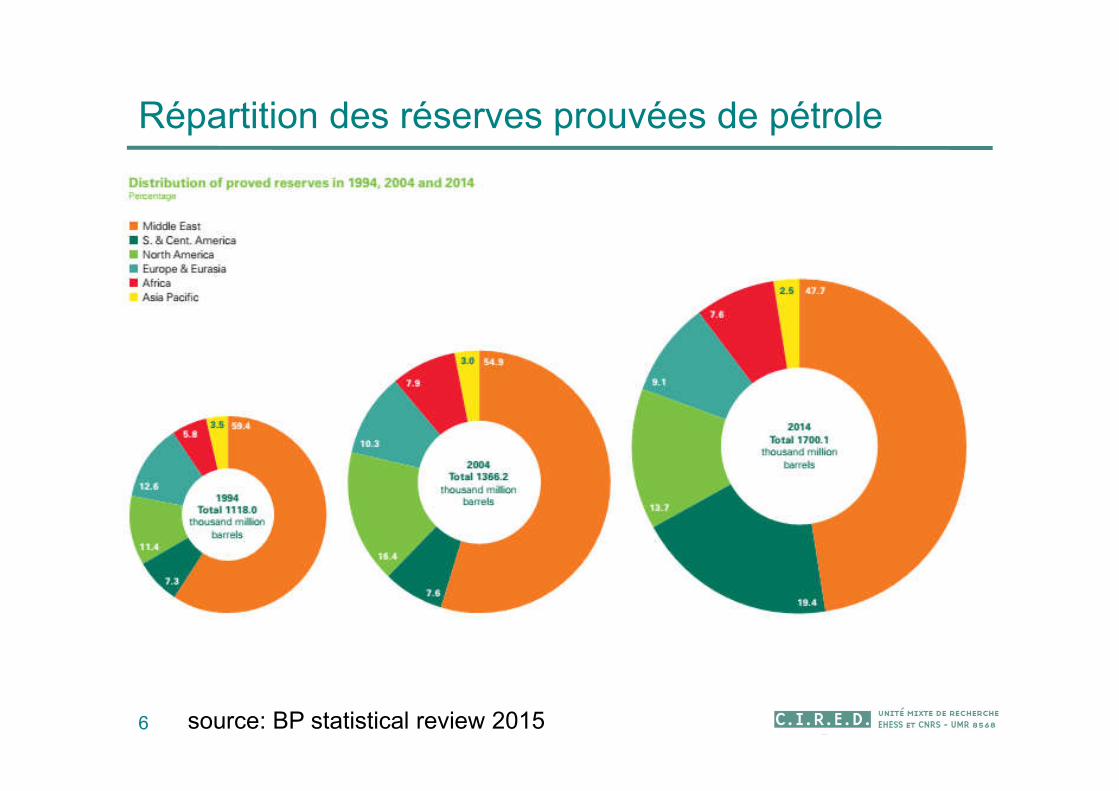

Répartition des réserves prouvées de pétrole

6 source: BP statistical review 2015

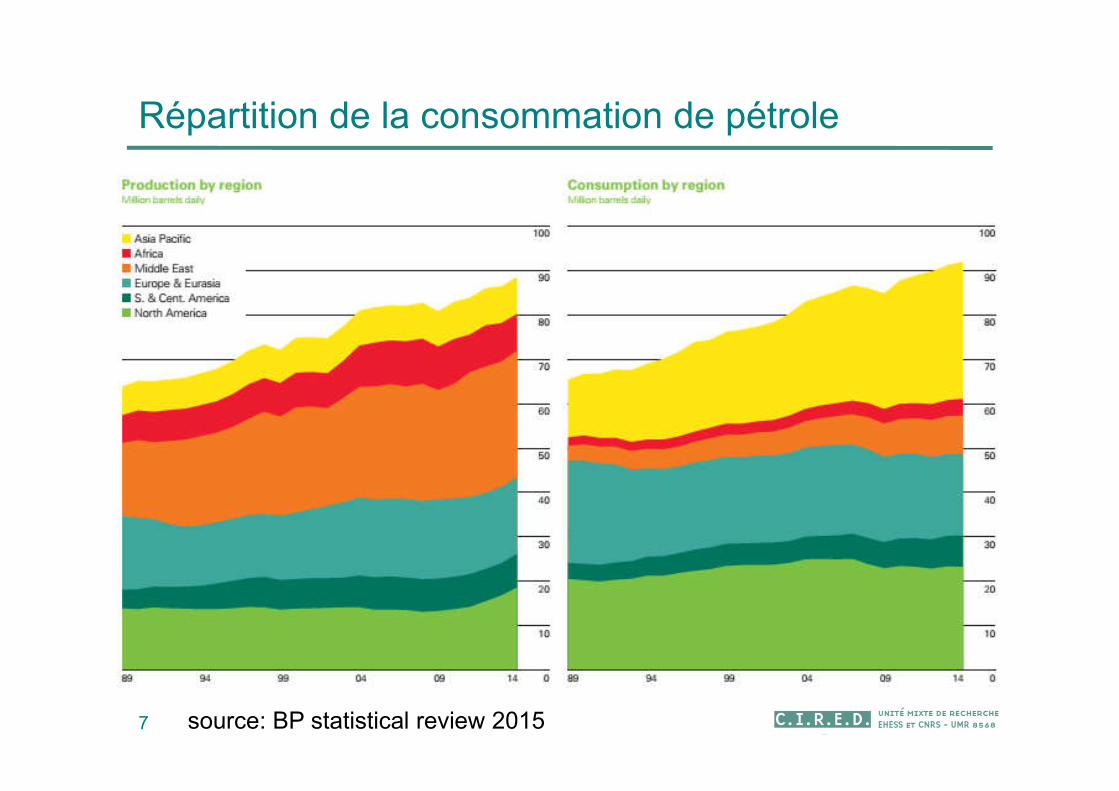

Répartition de la consommation de pétrole

7 source: BP statistical review 2015

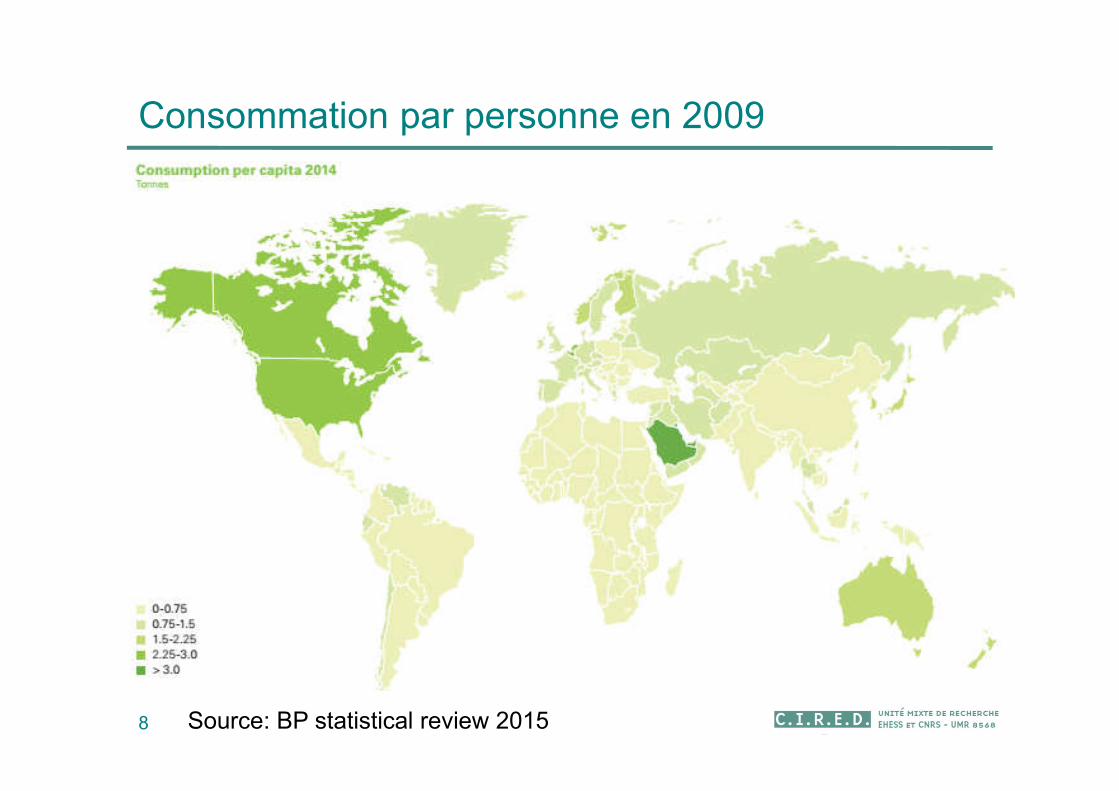

Consommation par personne en 2009

8 Source: BP statistical review 2015

9source: BP statistical review 2015

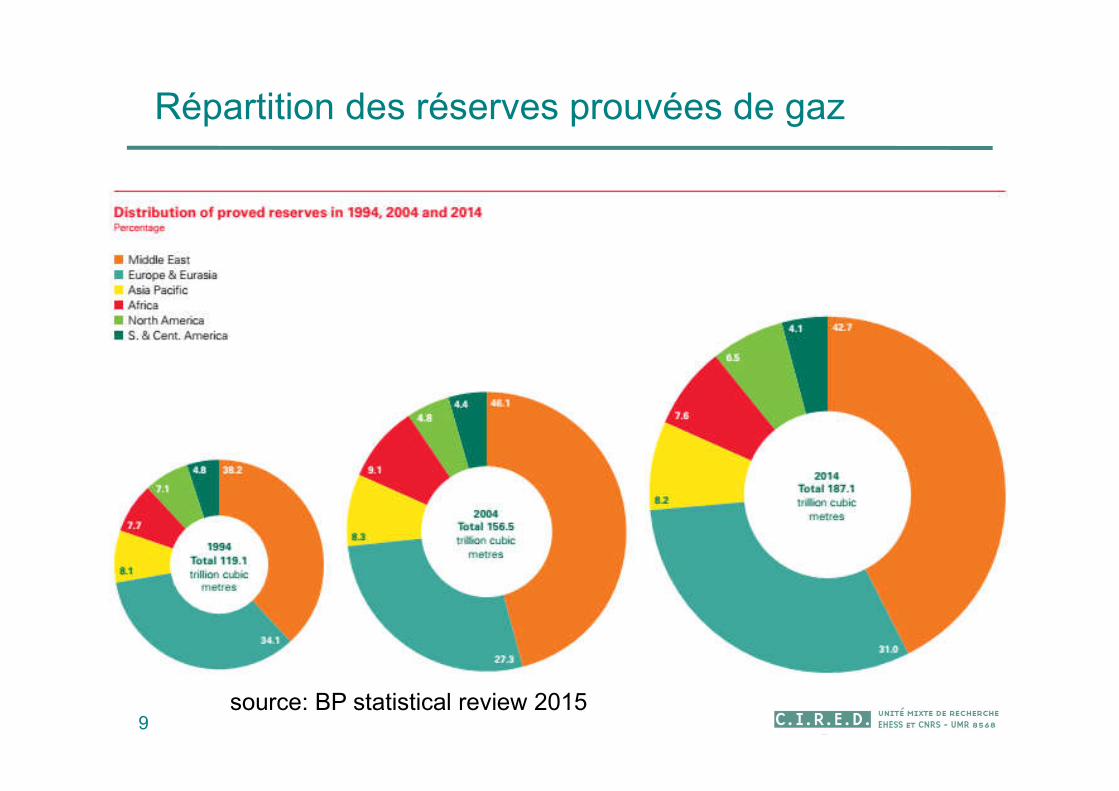

Répartition des réserves prouvées de gaz

10source: BP statistical review 2015

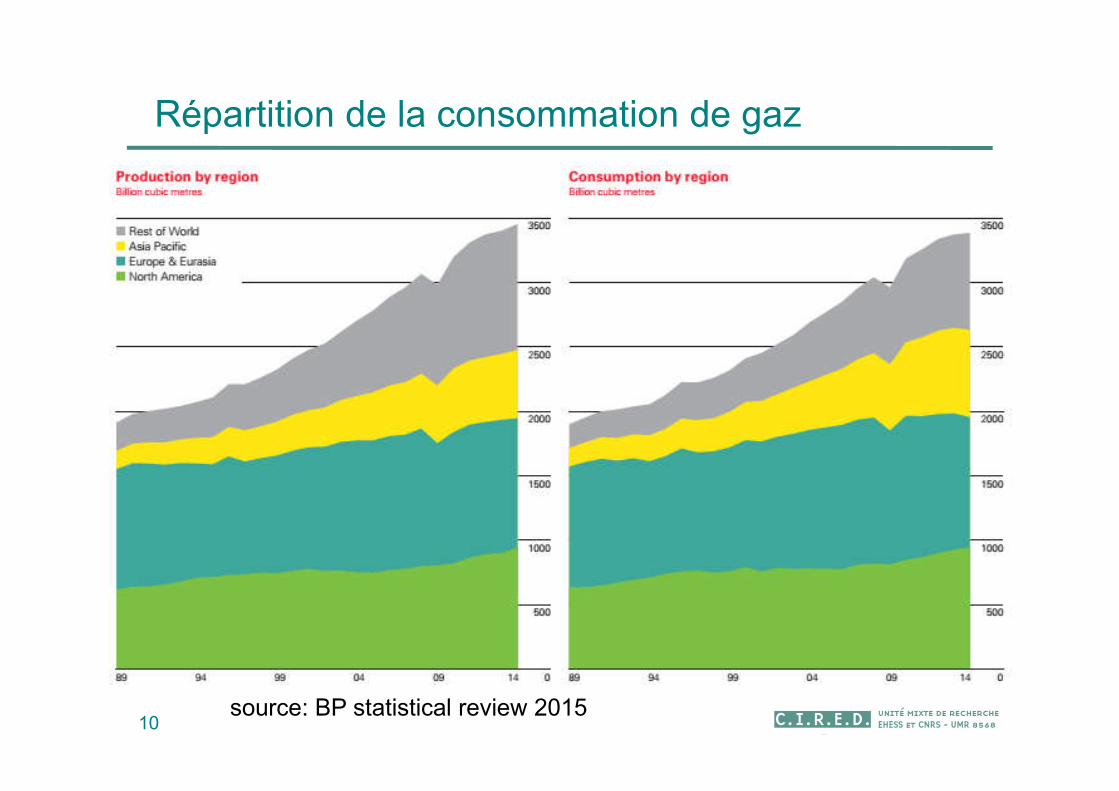

Répartition de la consommation de gaz

11

Liens entre pétrole et gaz

12

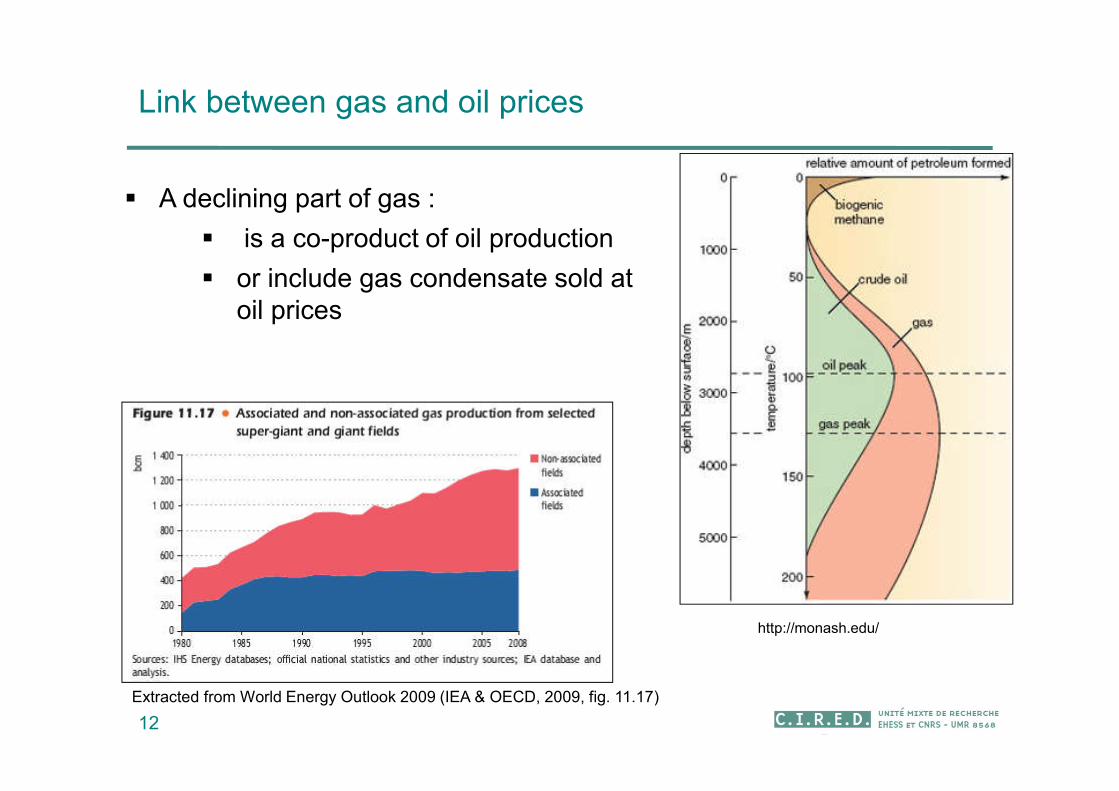

Link between gas and oil prices

A declining part of gas :

is a co-product of oil production

or include gas condensate sold at oil prices

Extracted from World Energy Outlook 2009 (IEA & OECD, 2009, fig. 11.17)

http://monash.edu/

13

Link between gas and oil prices

Strong substitutions but with uncertainties :

long-term gas prices elasticity to oil prices : between 0.14 (Brown and Yücel, 2008) and 0.924 (Asche et al., 2012).

14

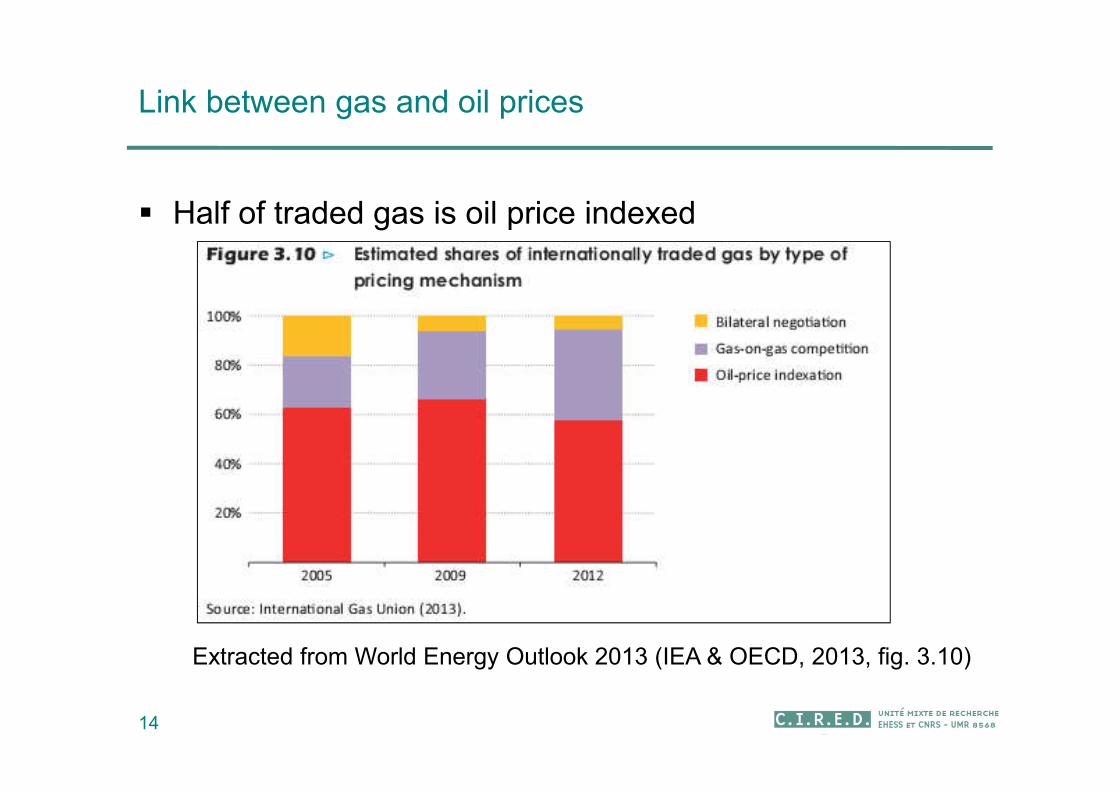

Link between gas and oil prices

Half of traded gas is oil price indexed

Extracted from World Energy Outlook 2013 (IEA & OECD, 2013, fig. 3.10)

Dynamique d’exploitation du pétrole

15

Citations

« aucune chance pour que l’humanité s’autolimite, à mon avis … Tout ce qui pourra être extrait, transformé, brulé, le sera .. après, on verra »

(commentaire, blog the Oil Man)

16

Citations

« Les hydrocarbures sont bien trop précieux pour qu’ils ne soient pas exploités jusqu’à la dernière goutte de pétrole, au dernier mètre cube de gaz naturel et même à la dernière tonne de charbon économiquement accessibles. »

(Christian Gérondeau, ParisTechReview, 15 octobre 2010)

17

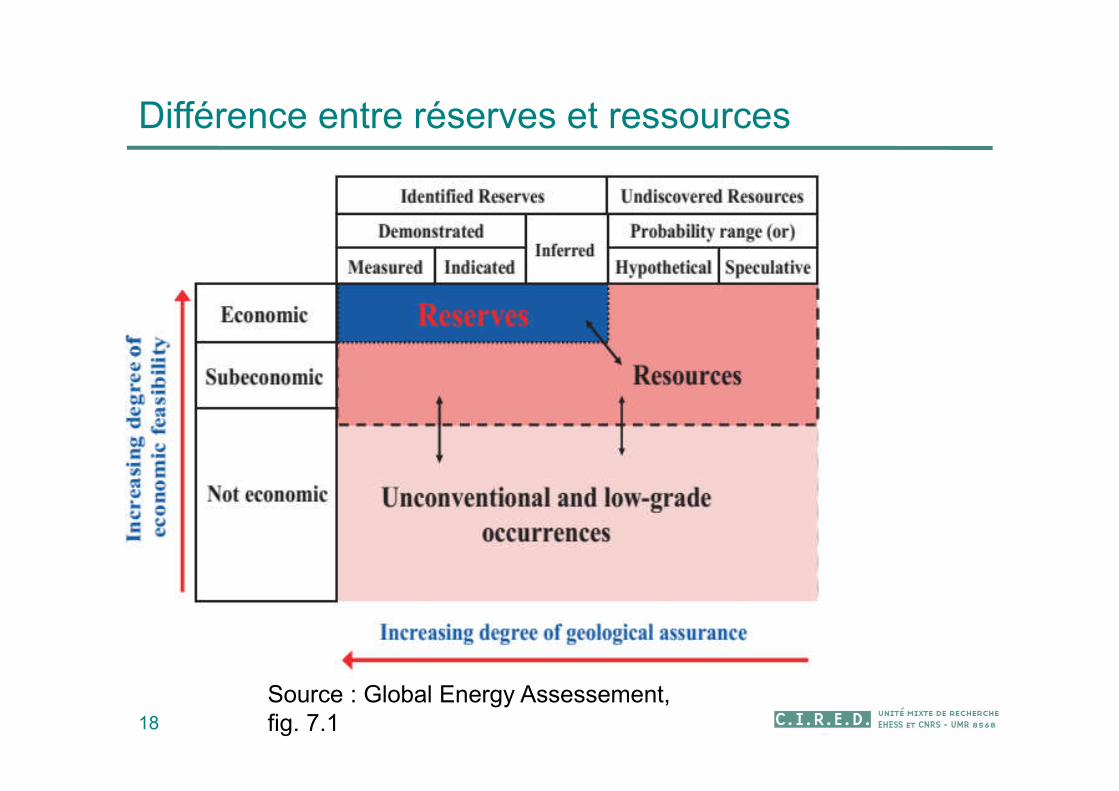

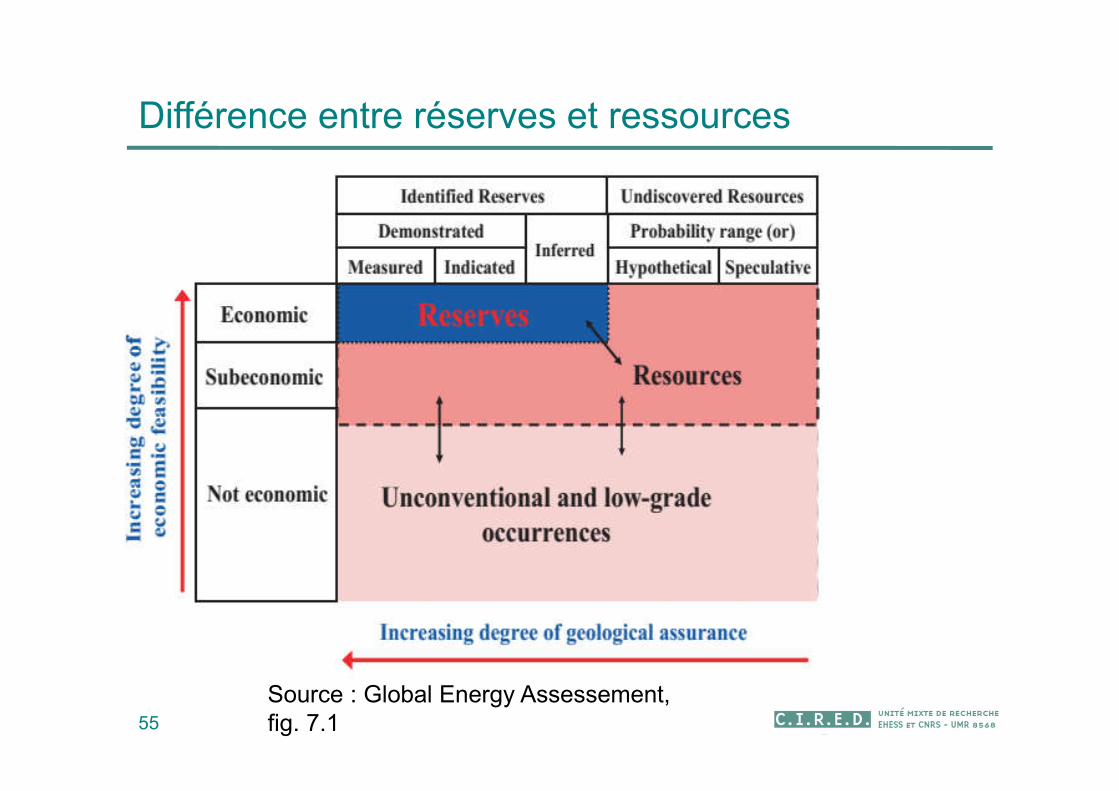

Différence entre réserves et ressources

18

Limite économique

PossiblesProbablesProuvées

Réserves

Source : Global Energy Assessement, fig. 7.1

Ressource

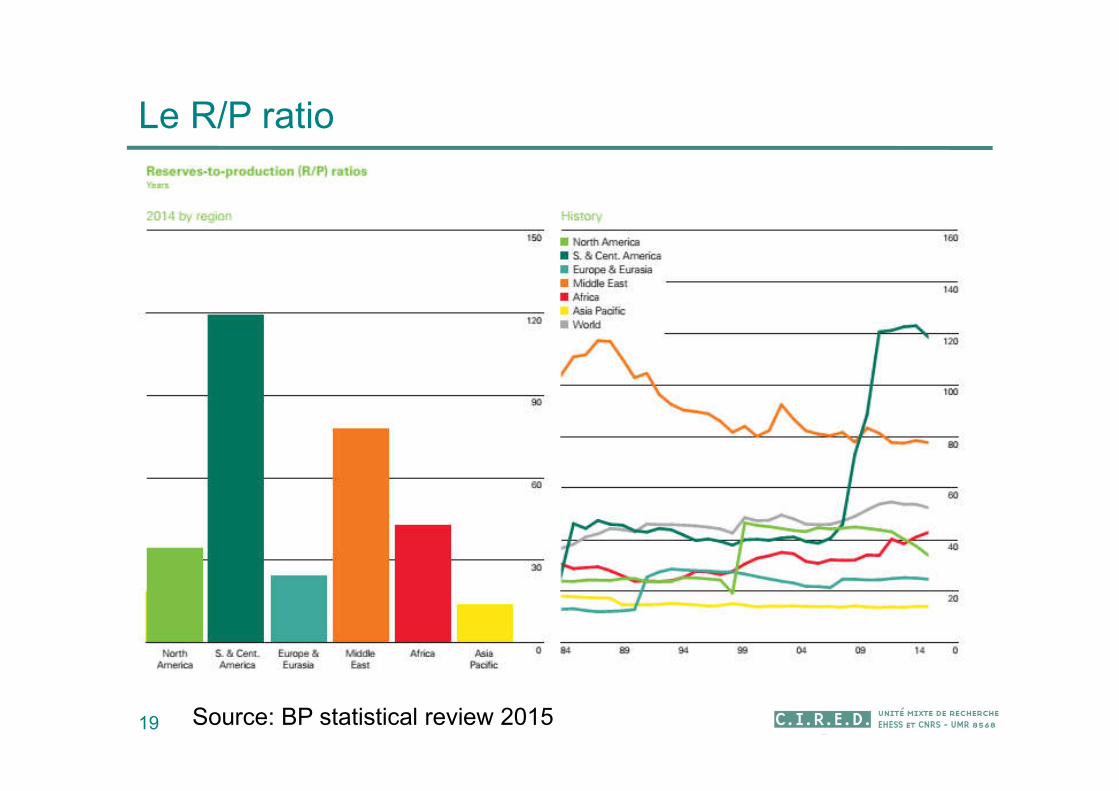

Le R/P ratio

19 Source: BP statistical review 2015

La dynamique d’exploitation du pétrole

20

Exploration

Acquisition d’information avec les découvertes

Informations conduisent à plus de découvertes

Epuisement

Les découvertes sont fonctions du montant de pétrole restant à découvrir

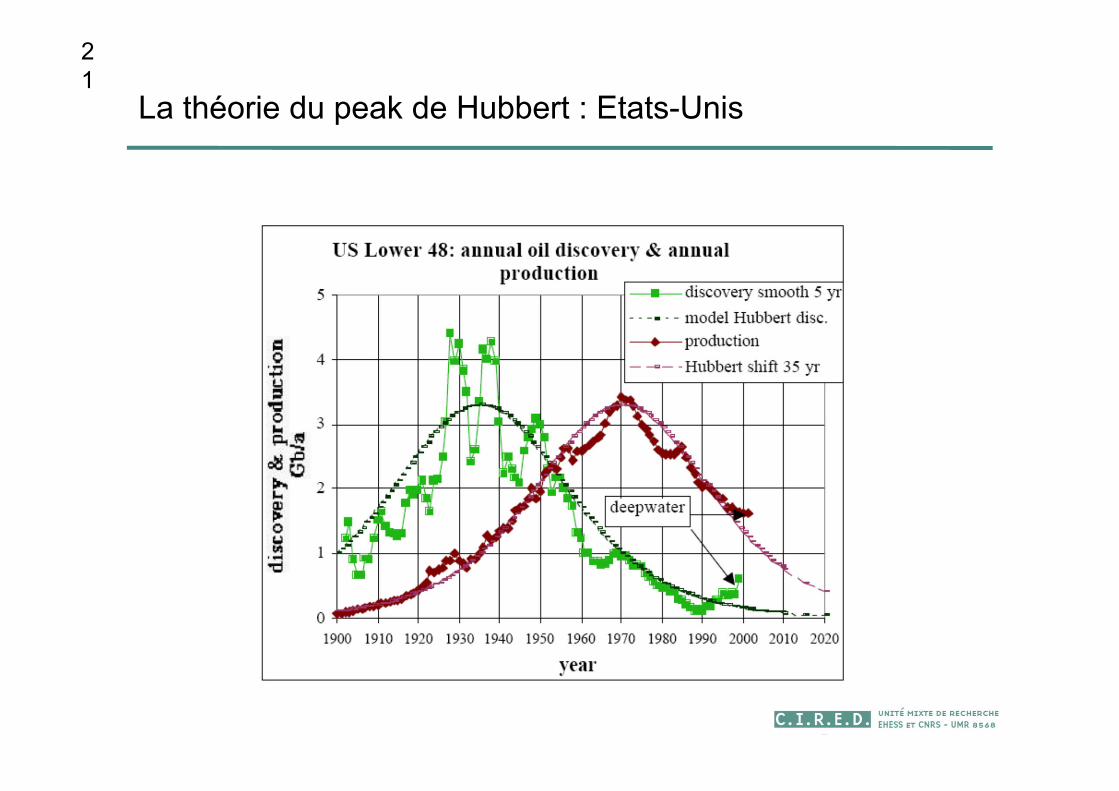

La théorie du peak de Hubbert : Etats-Unis

21

Source: Laherrere, 2003

Oil discoveries shifted 35 years and United States production (without Alaska)

Les courbes de Hubbert

Avantages :

Prise en compte des contraintes géologiques

Inconvénients

Plus difficilement extrapolable à une échelle globale

22

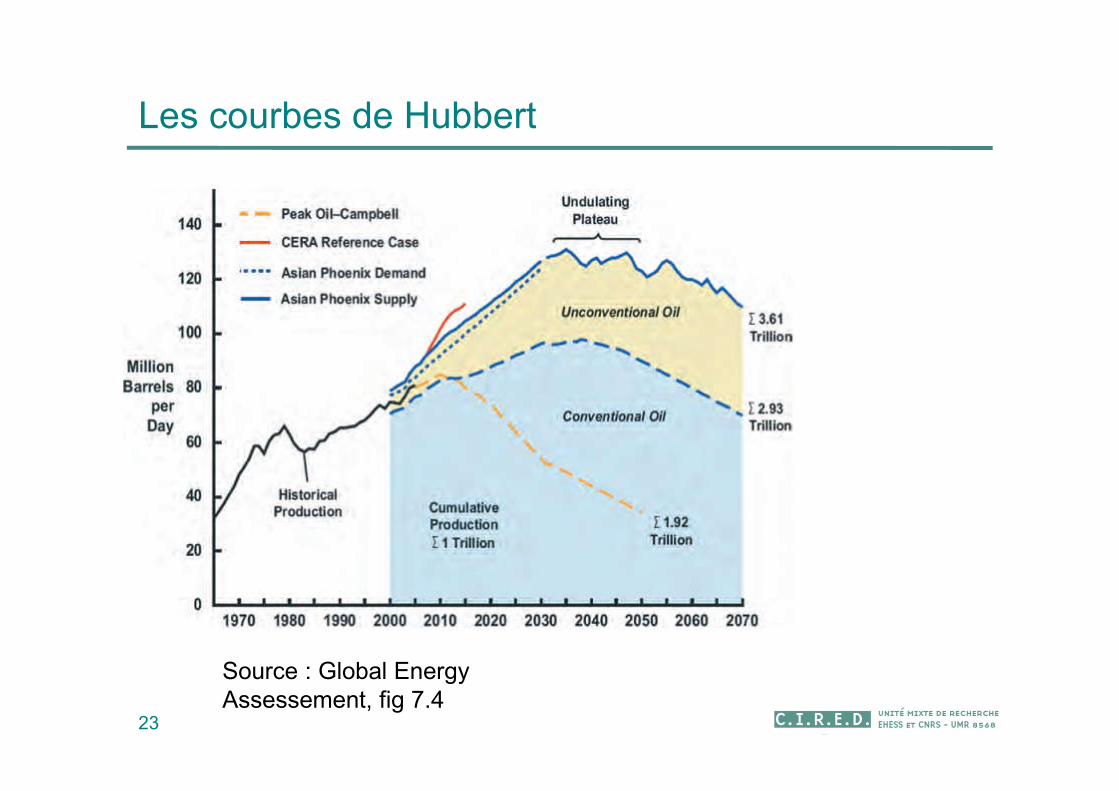

Les courbes de Hubbert

23

Source : Global Energy Assessement, fig 7.4

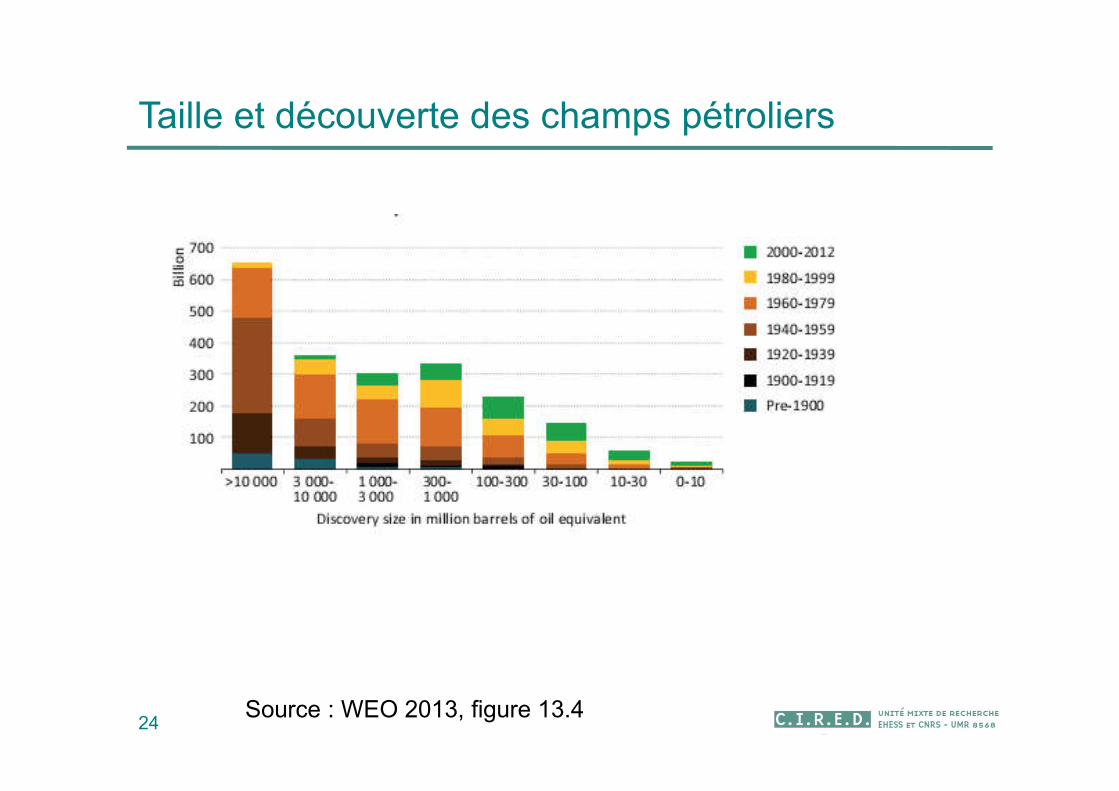

Taille et découverte des champs pétroliers

24Source : WEO 2013, figure 13.4

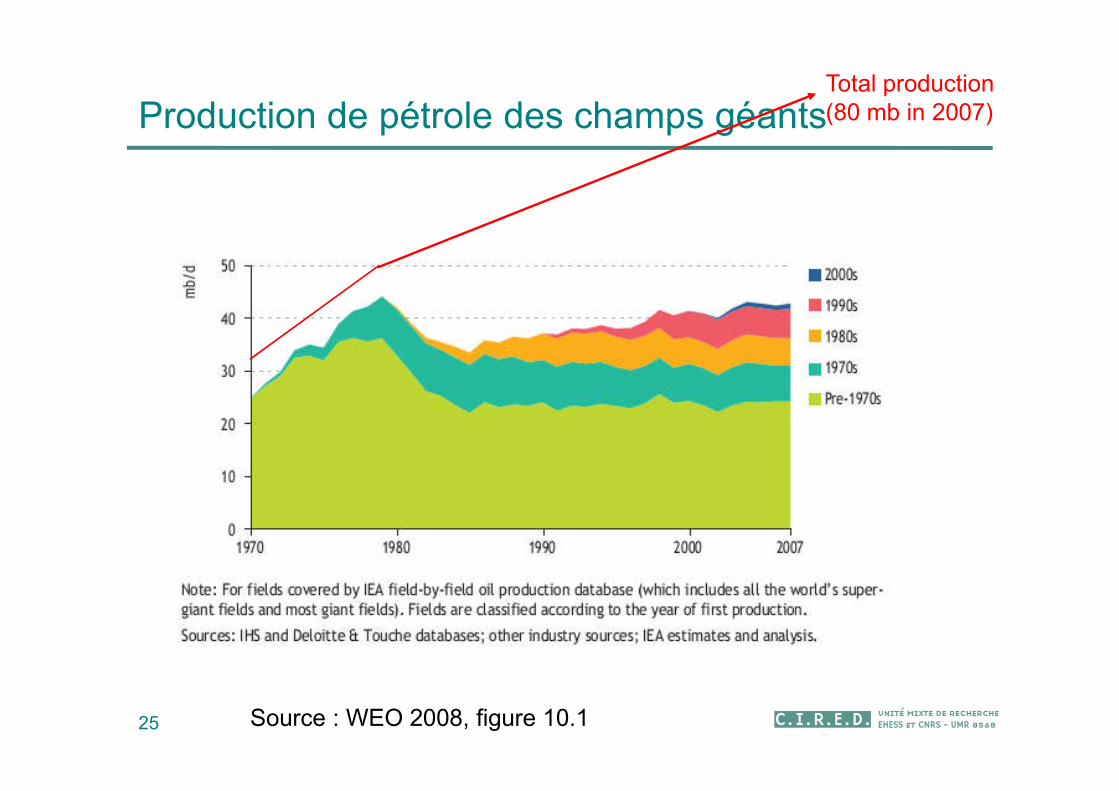

Production de pétrole des champs géants

25 Source : WEO 2008, figure 10.1

Total production(80 mb in 2007)

Dynamique d’exploitation du pétrole

et politiques climatiques

26

Modèle et scénarios

Le modèle Imaclim-R

Scénarios prospectifs

Rôles des scenarios

Let’s test the consequences of the three hypothesis

Assessment of the macroeconomic cost of oil scarcity

Impact of climate policies

All the following results are obtained with the IMACLIM-R model.

http://www.imaclim.centre-cired.fr/

28

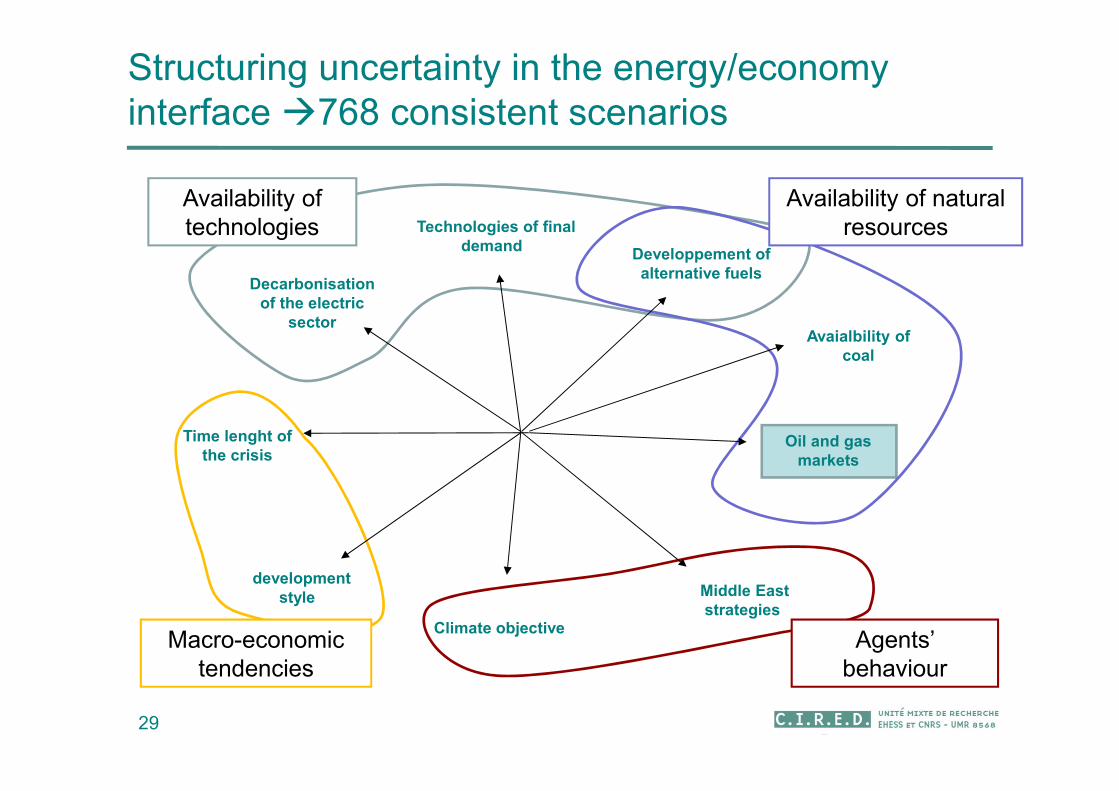

29

Availability of technologies

Availability of natural resources

Agents’ behaviour

Macro-economictendencies

Avaialbility of coal

Climate objective

Technologies of final demand

Developpement of alternative fuels

Oil and gas markets

developmentstyle Middle East

strategies

Time lenght of the crisis

Decarbonisation of the electric

sector

Structuring uncertainty in the energy/economy interface 768 consistent scenarios

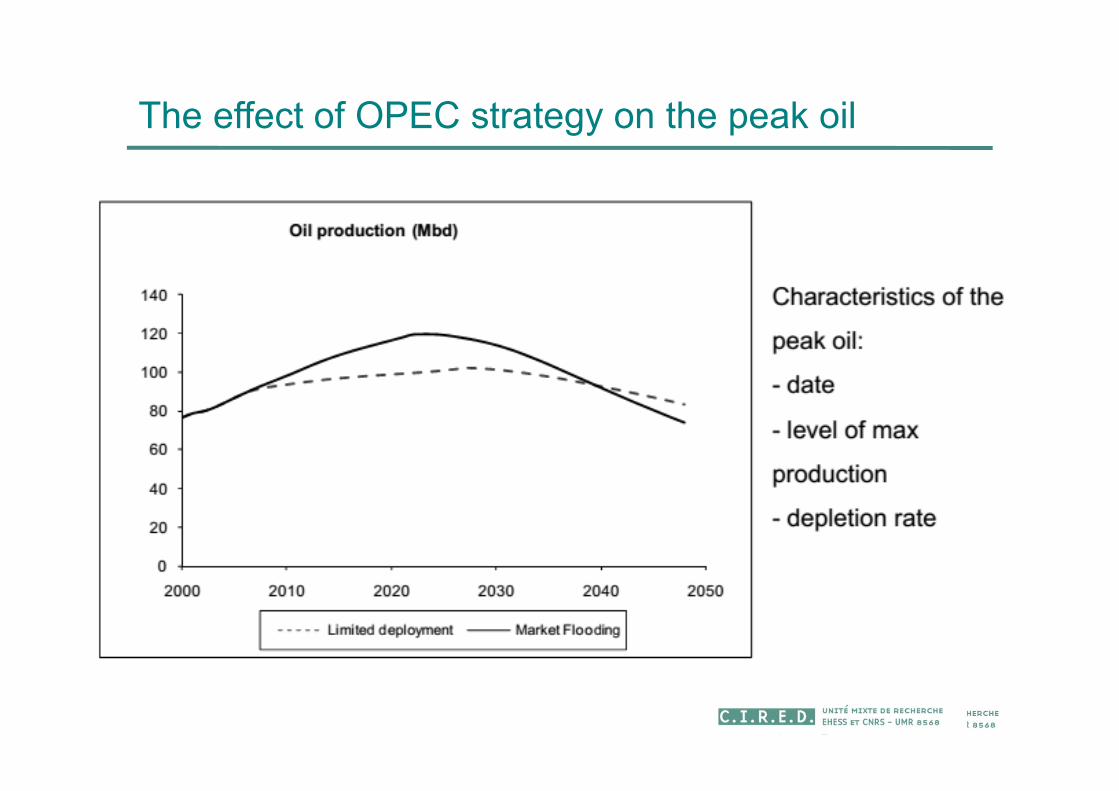

The effect of OPEC strategy on the peak oil

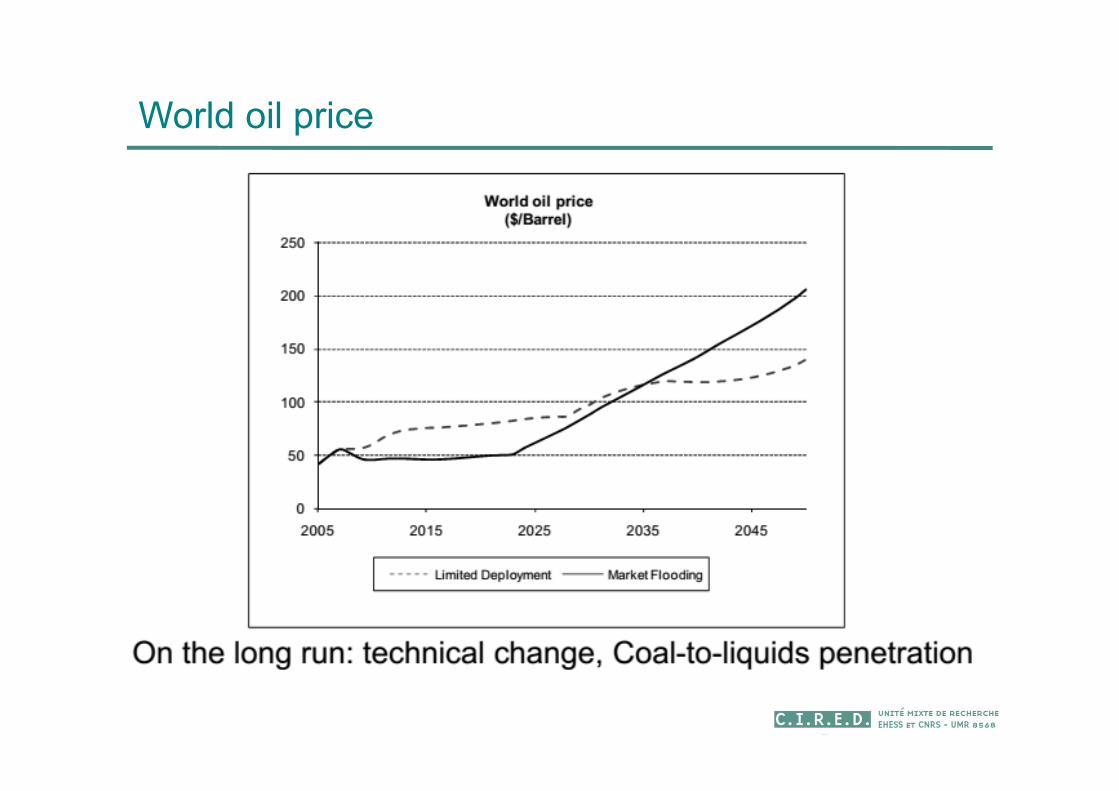

World oil price

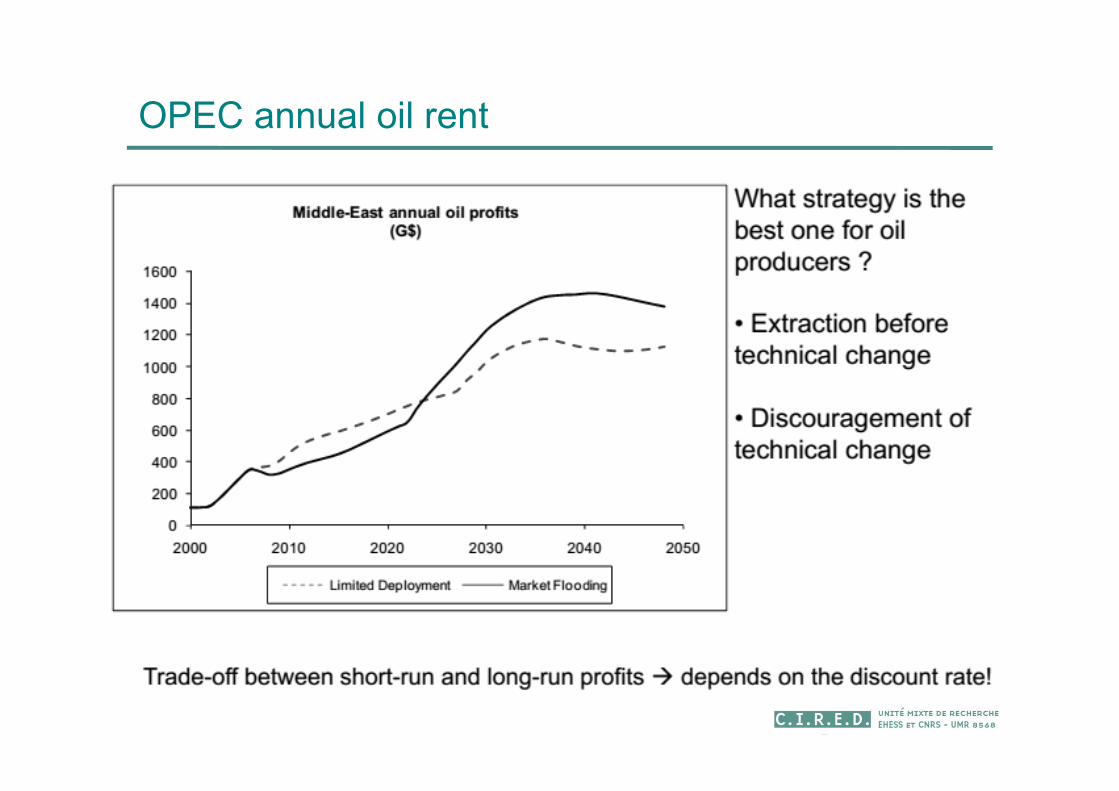

OPEC annual oil rent

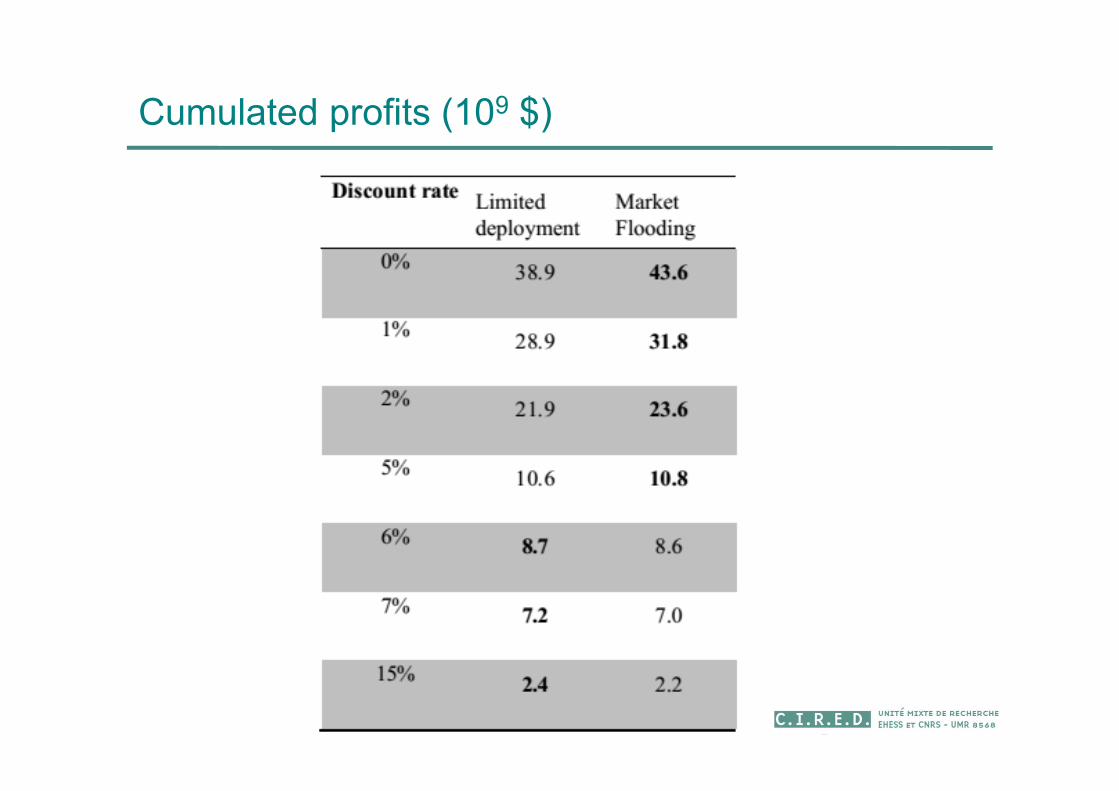

Cumulated profits (109 $)

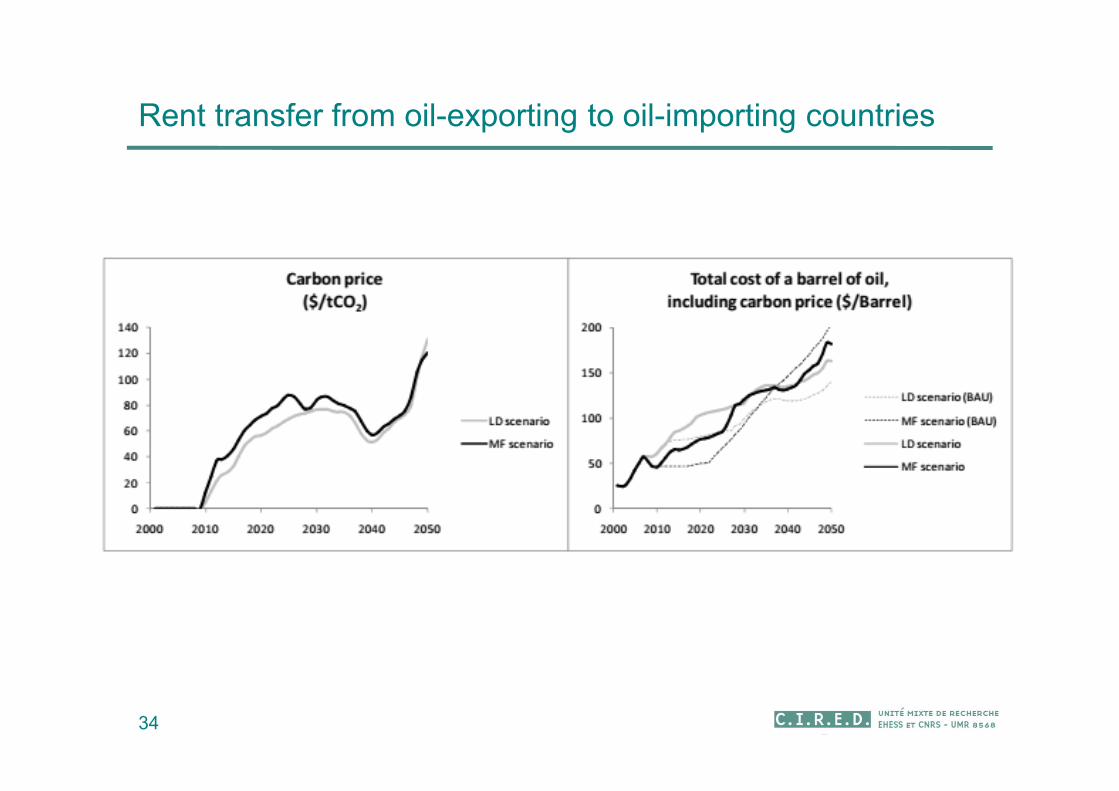

Rent transfer from oil-exporting to oil-importing countries

34

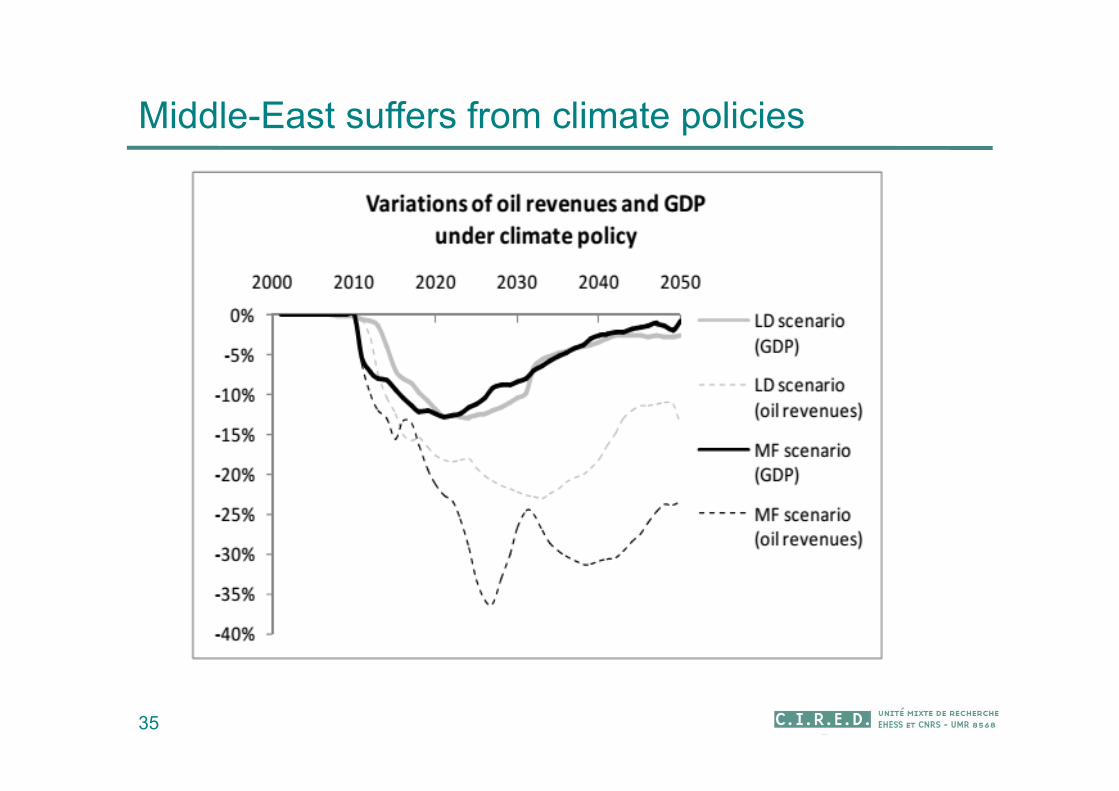

Middle-East suffers from climate policies

35

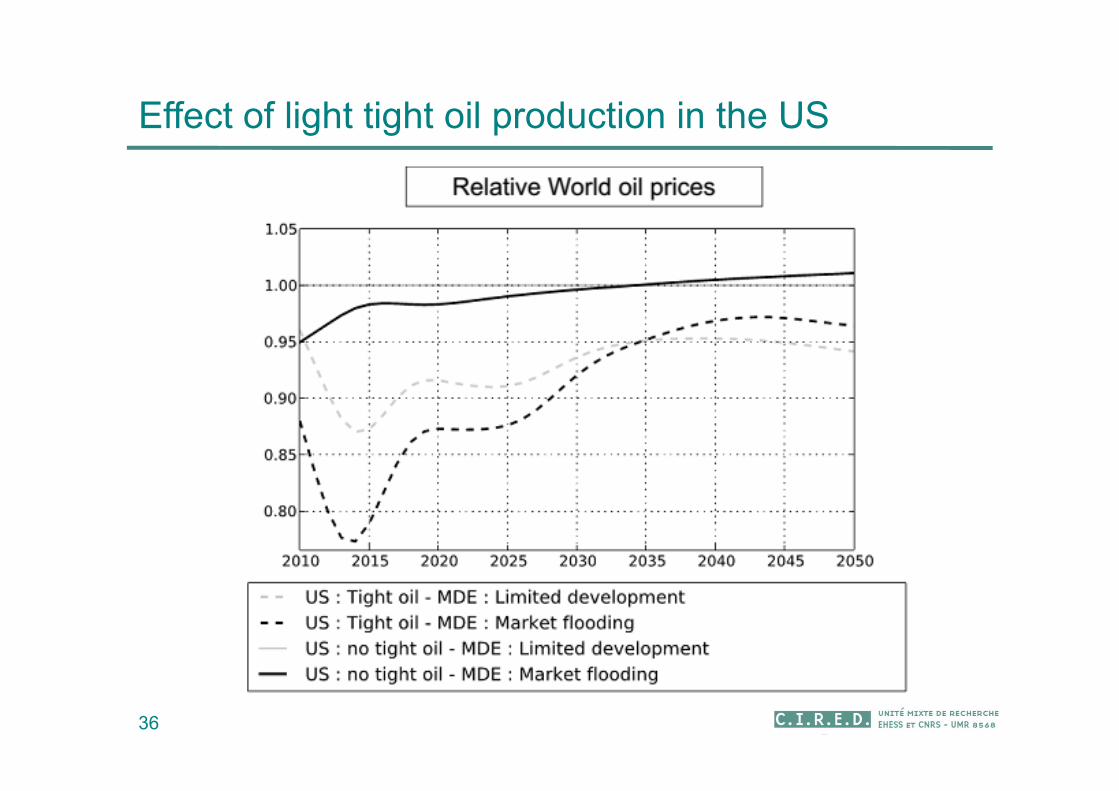

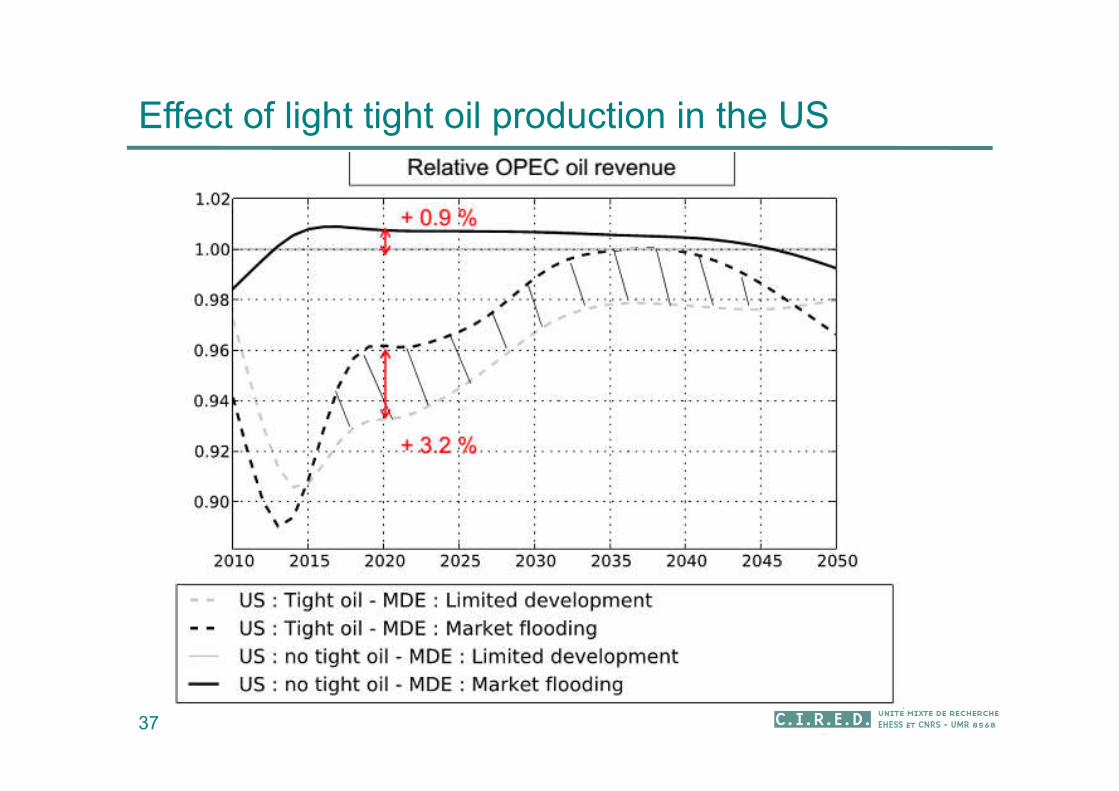

Effect of light tight oil production in the US

36

37

Effect of light tight oil production in the US

Les nouveaux hydrocarbures non-conventionnels

38

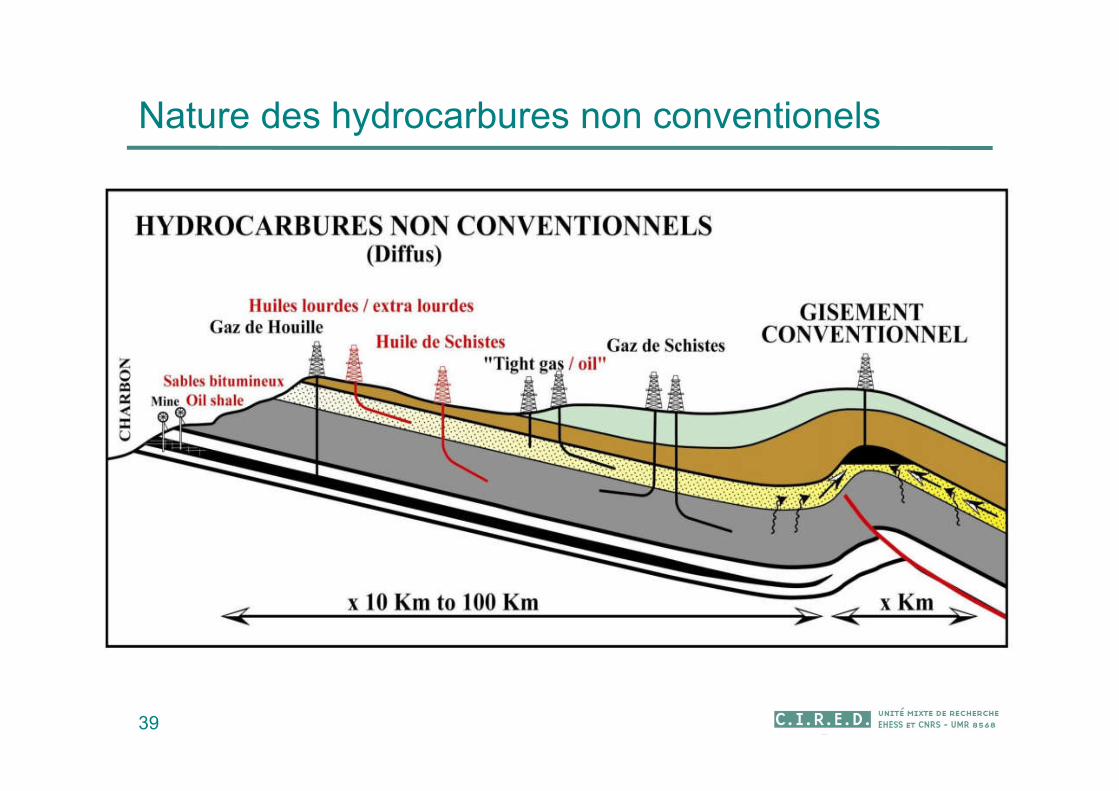

Nature des hydrocarbures non conventionels

39

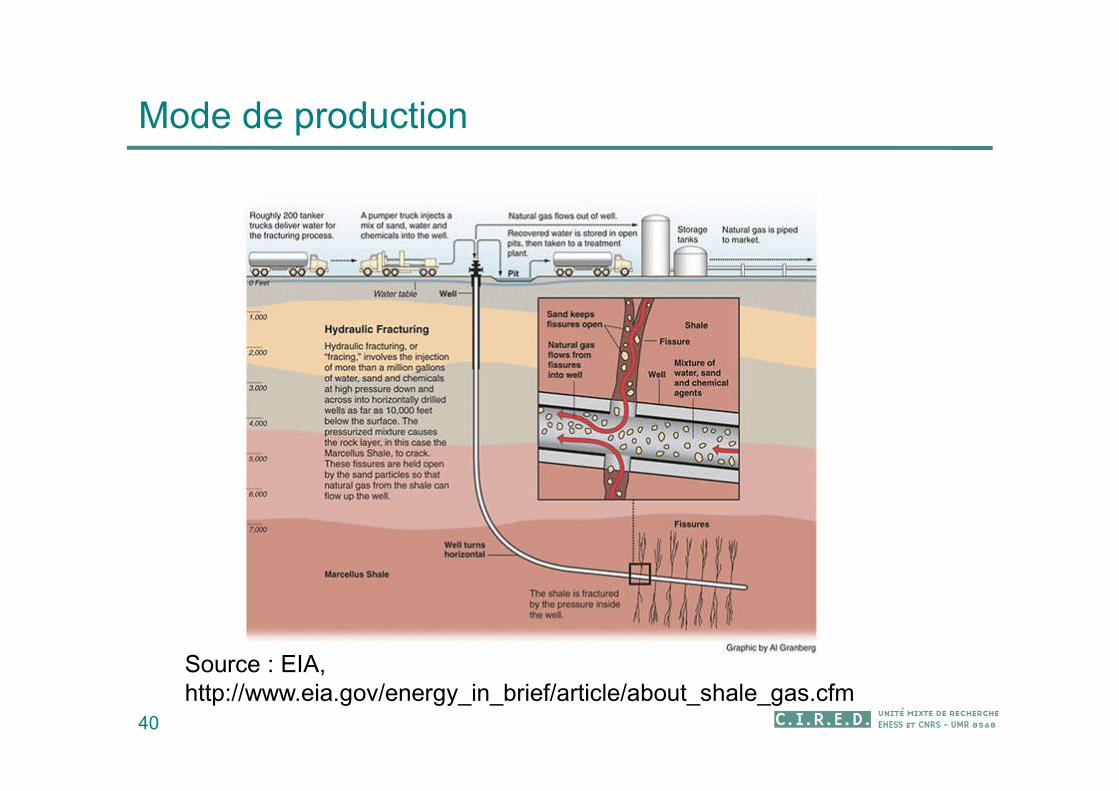

Mode de production

40

Source : EIA, http://www.eia.gov/energy_in_brief/article/about_shale_gas.cfm

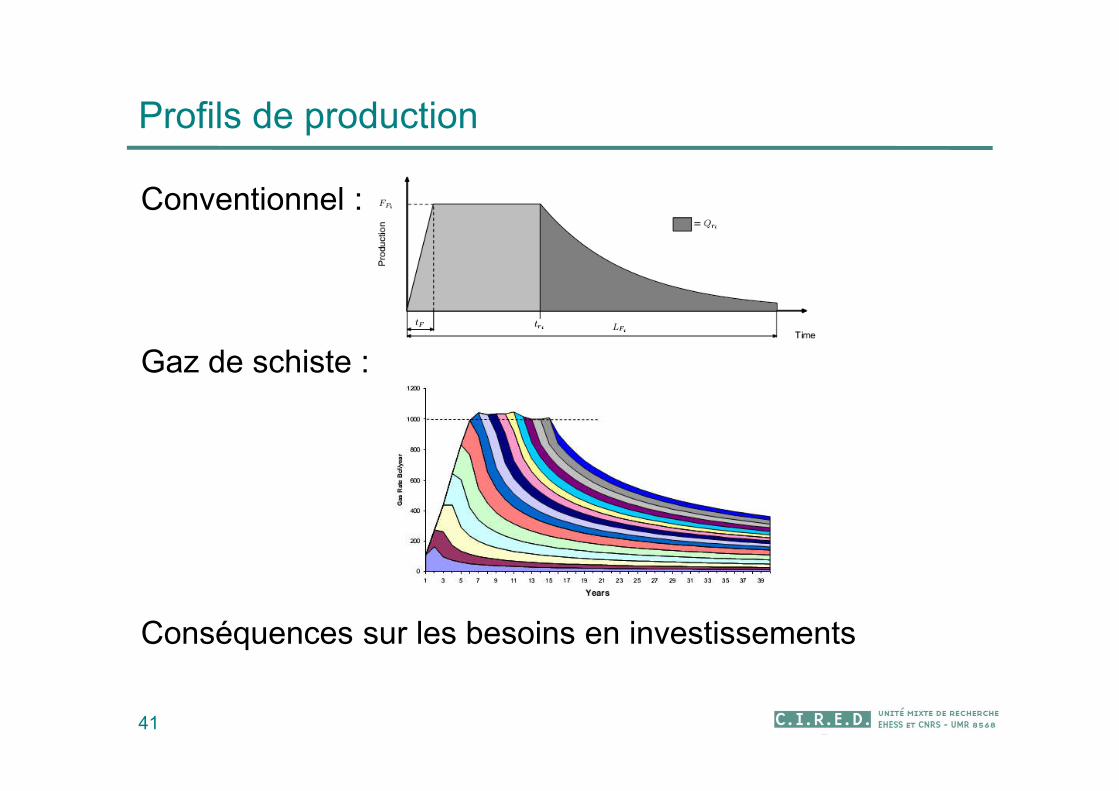

Profils de production

41

Conventionnel :

Gaz de schiste :

Conséquences sur les besoins en investissements

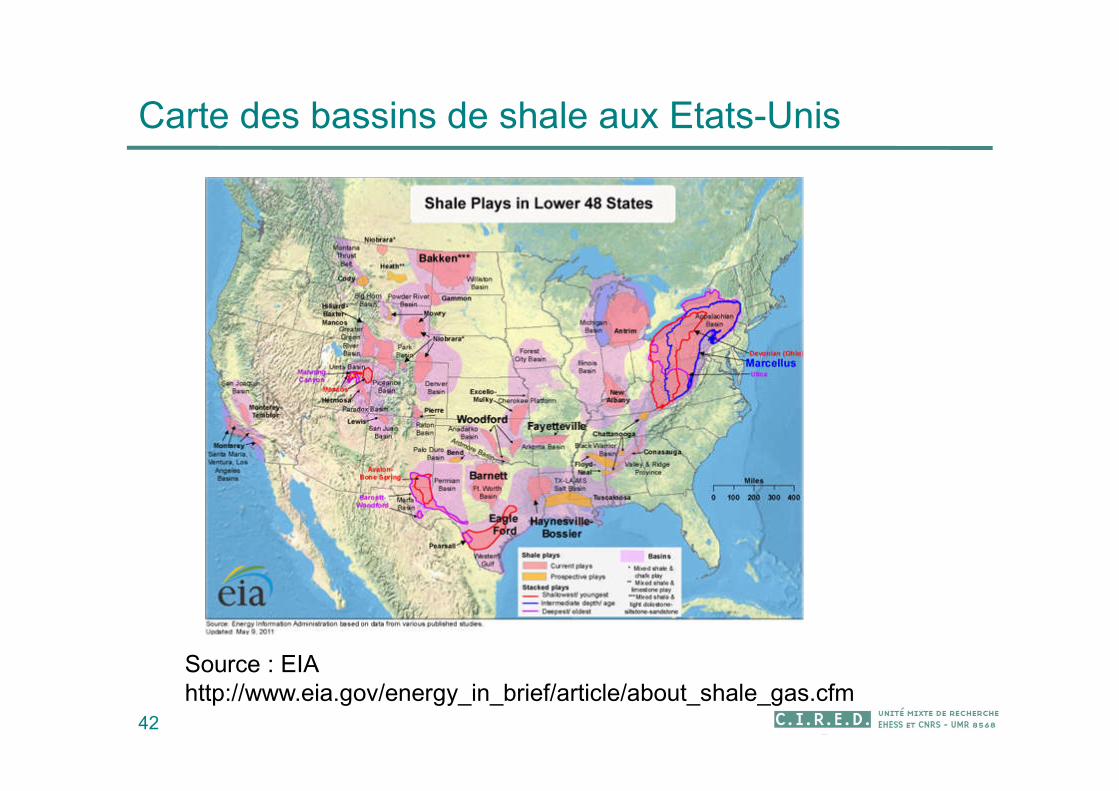

Carte des bassins de shale aux Etats-Unis

42

Source : EIA http://www.eia.gov/energy_in_brief/article/about_shale_gas.cfm

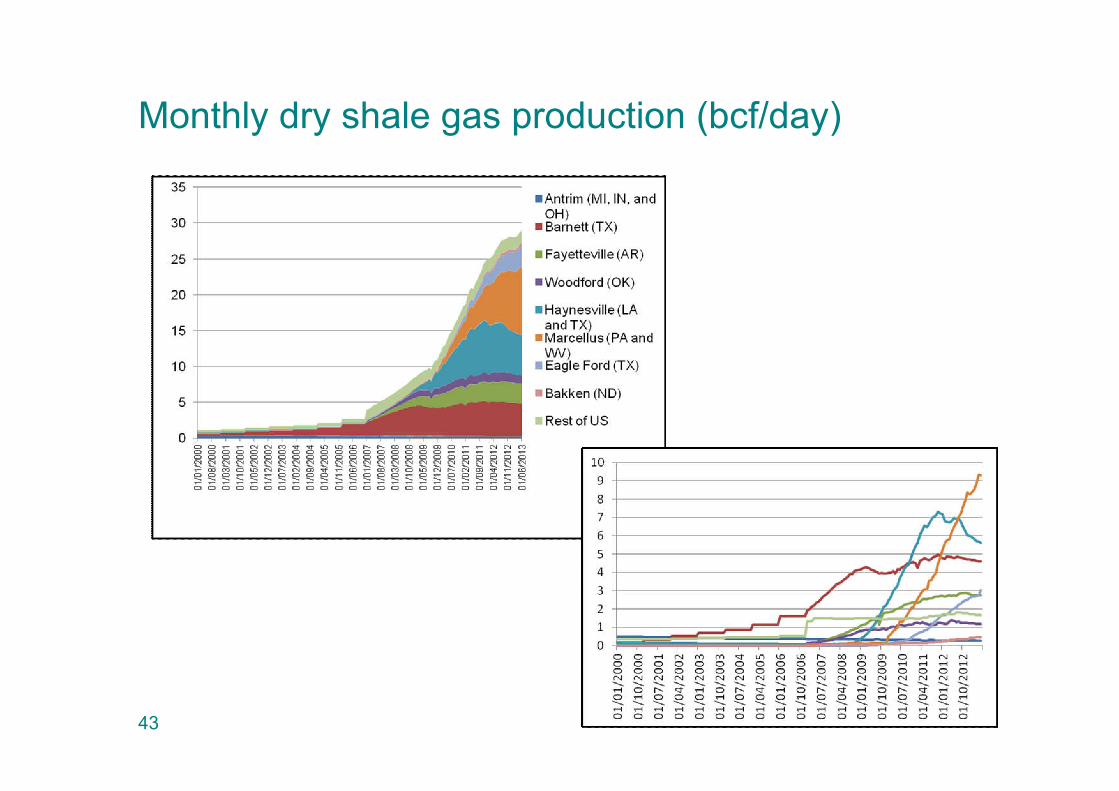

Monthly dry shale gas production (bcf/day)

43

44

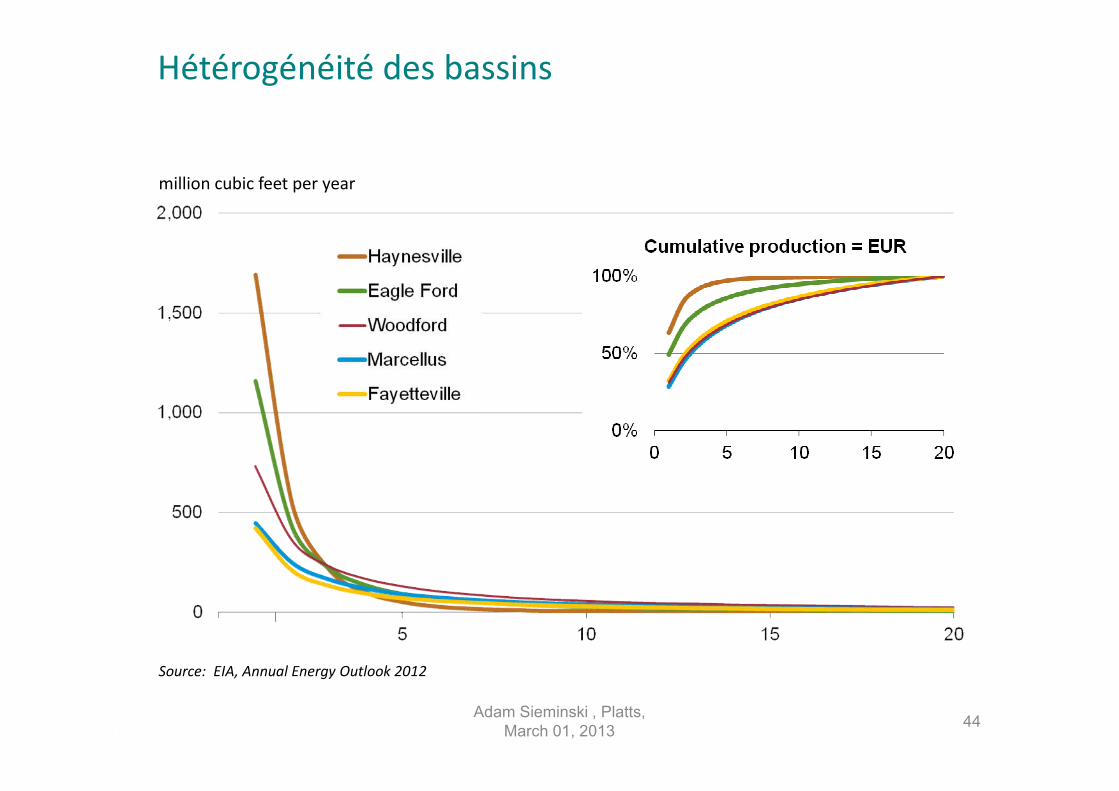

million cubic feet per year

Source: EIA, Annual Energy Outlook 2012

1

Adam Sieminski , Platts, March 01, 2013

Hétérogénéité des bassins

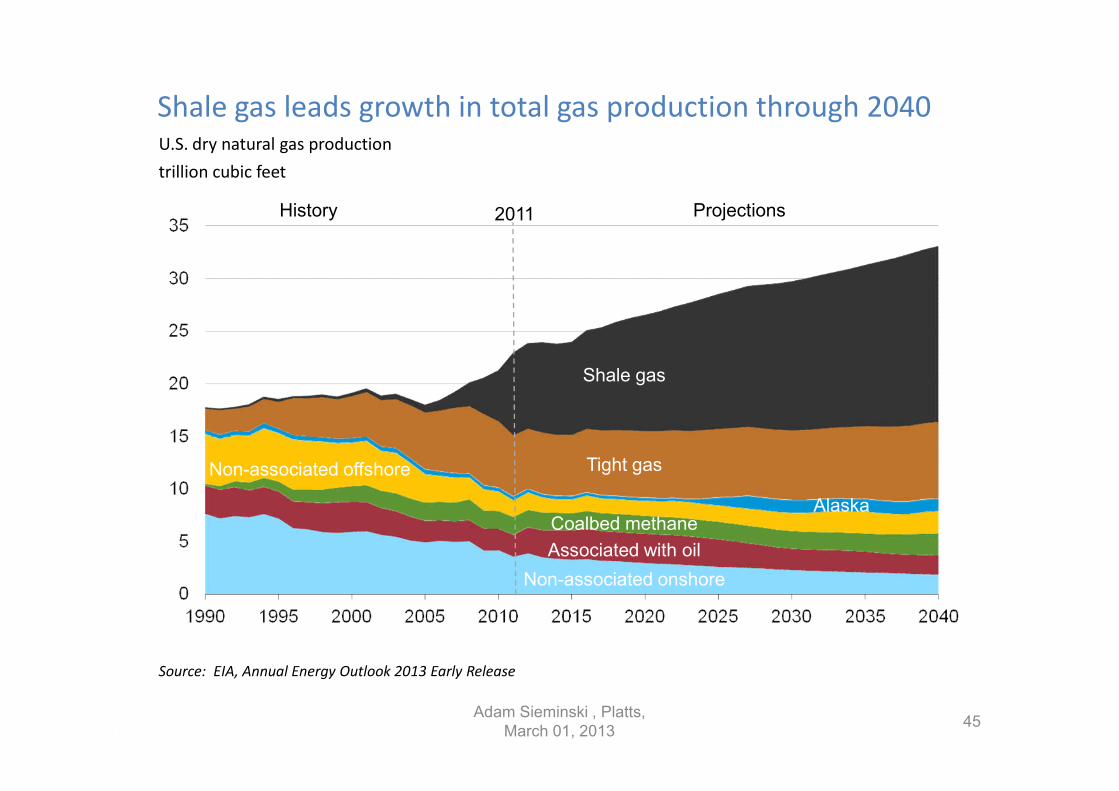

Shale gas leads growth in total gas production through 2040

45

U.S. dry natural gas production

trillion cubic feet

Source: EIA, Annual Energy Outlook 2013 Early Release

Associated with oil

Coalbed methane

Tight gas

Shale gas

Alaska

Non-associated onshore

Non-associated offshore

ProjectionsHistory 2011

Adam Sieminski , Platts, March 01, 2013

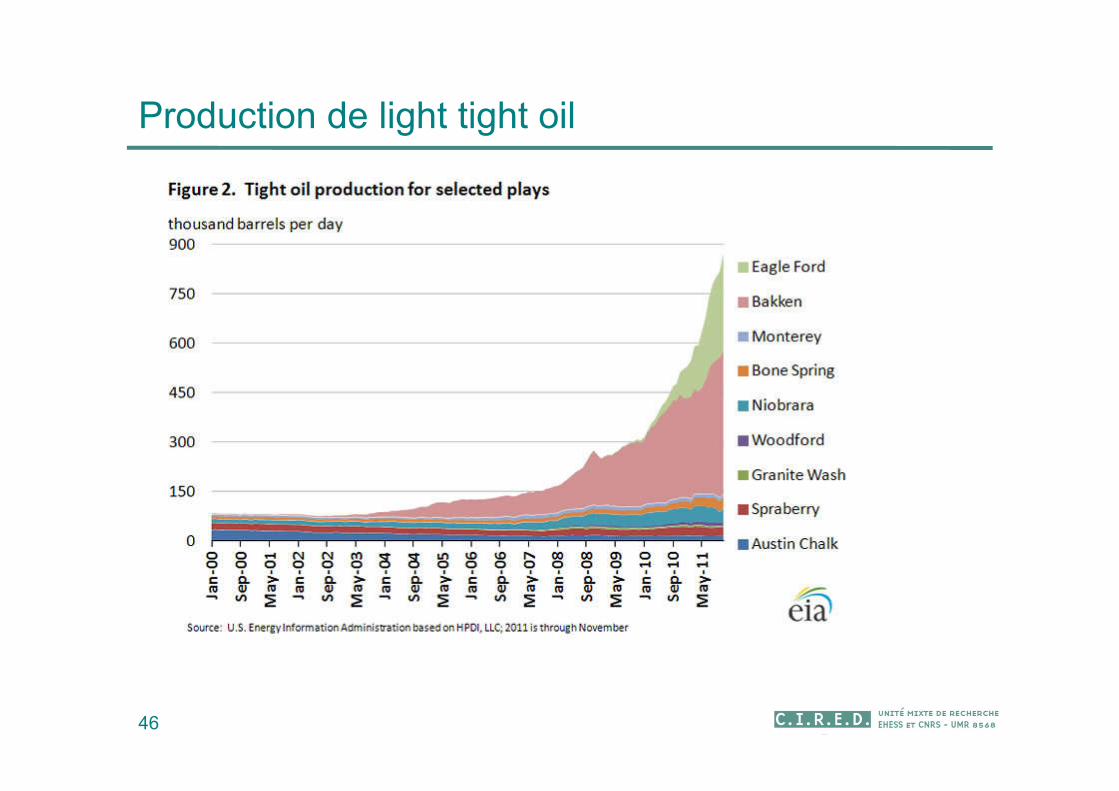

Production de light tight oil

46

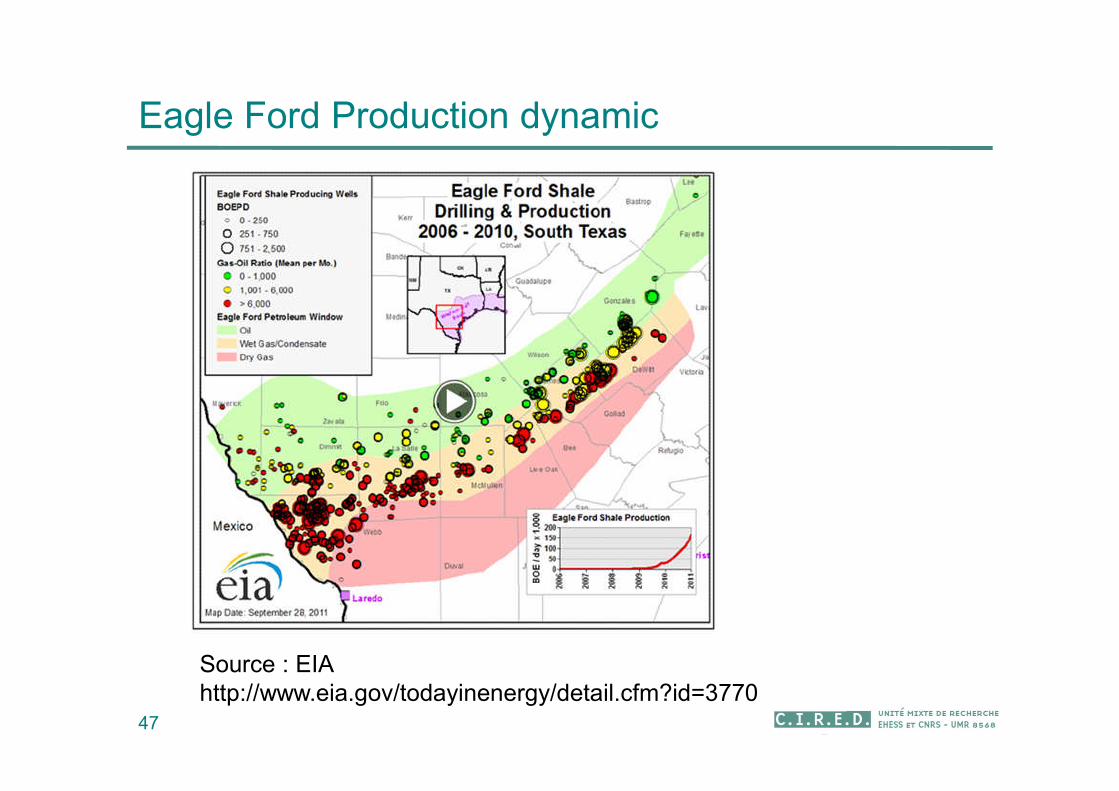

Eagle Ford Production dynamic

47

Source : EIA http://www.eia.gov/todayinenergy/detail.cfm?id=3770

48

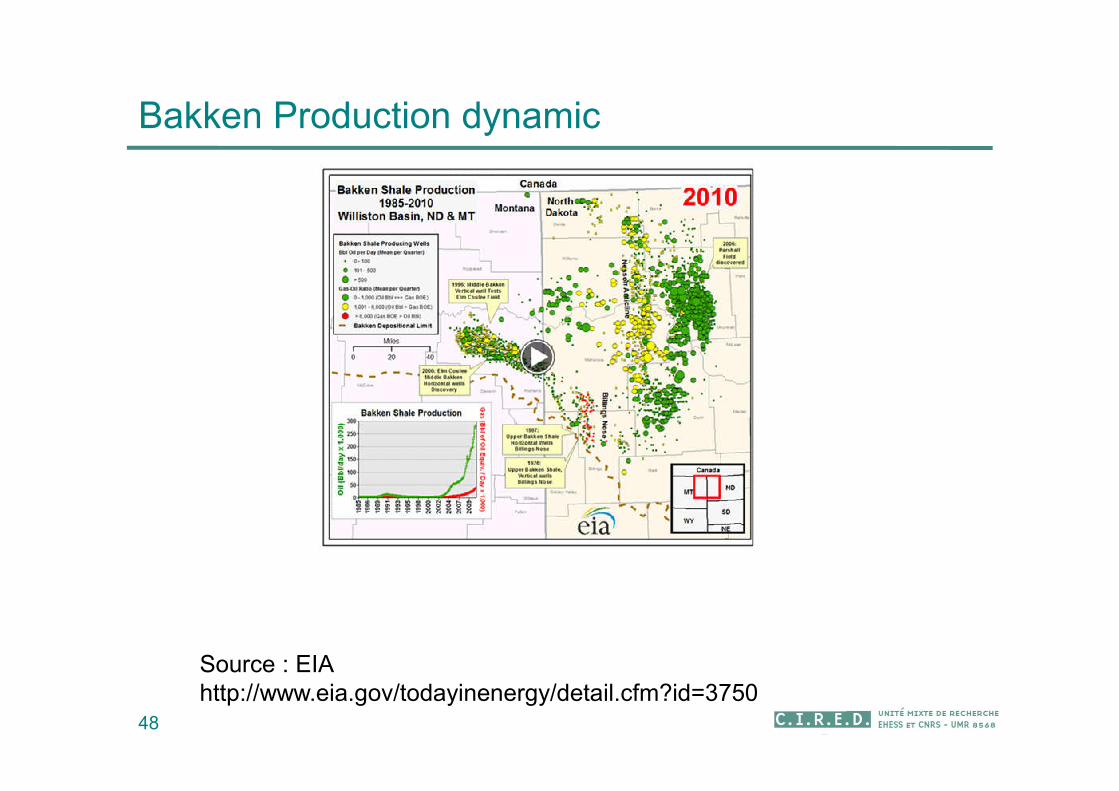

Source : EIA http://www.eia.gov/todayinenergy/detail.cfm?id=3750

Bakken Production dynamic

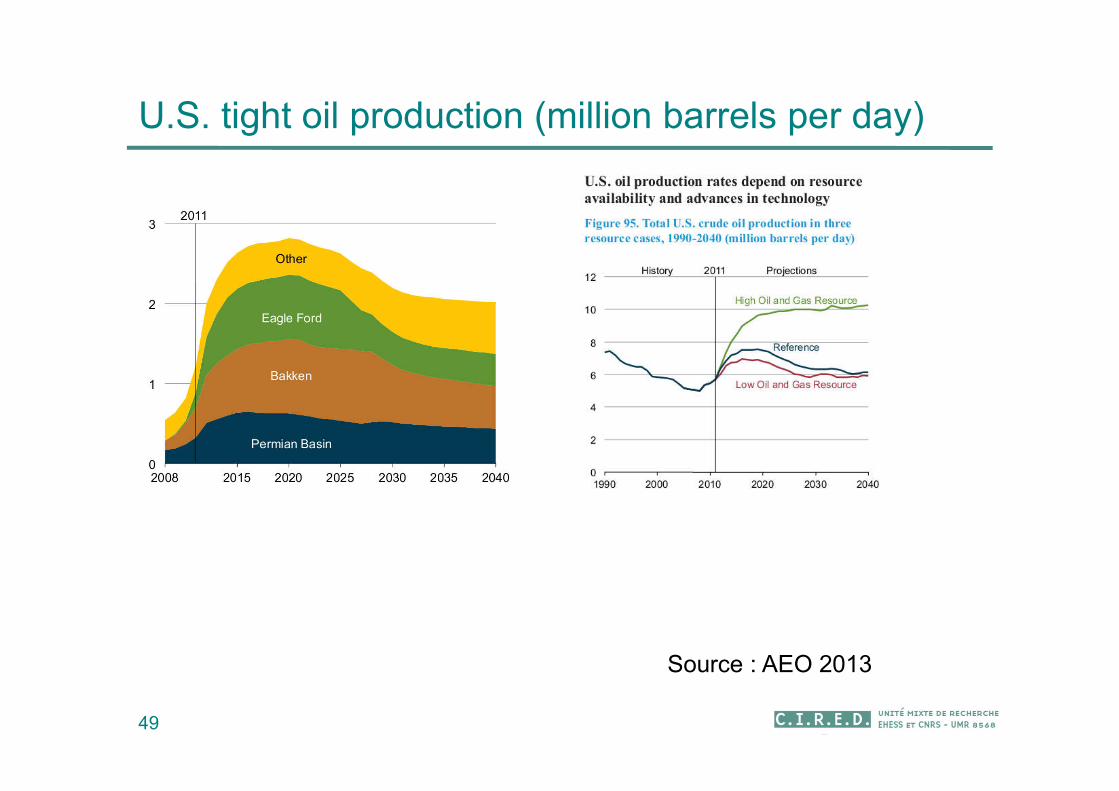

U.S. tight oil production (million barrels per day)

49

Source : AEO 2013

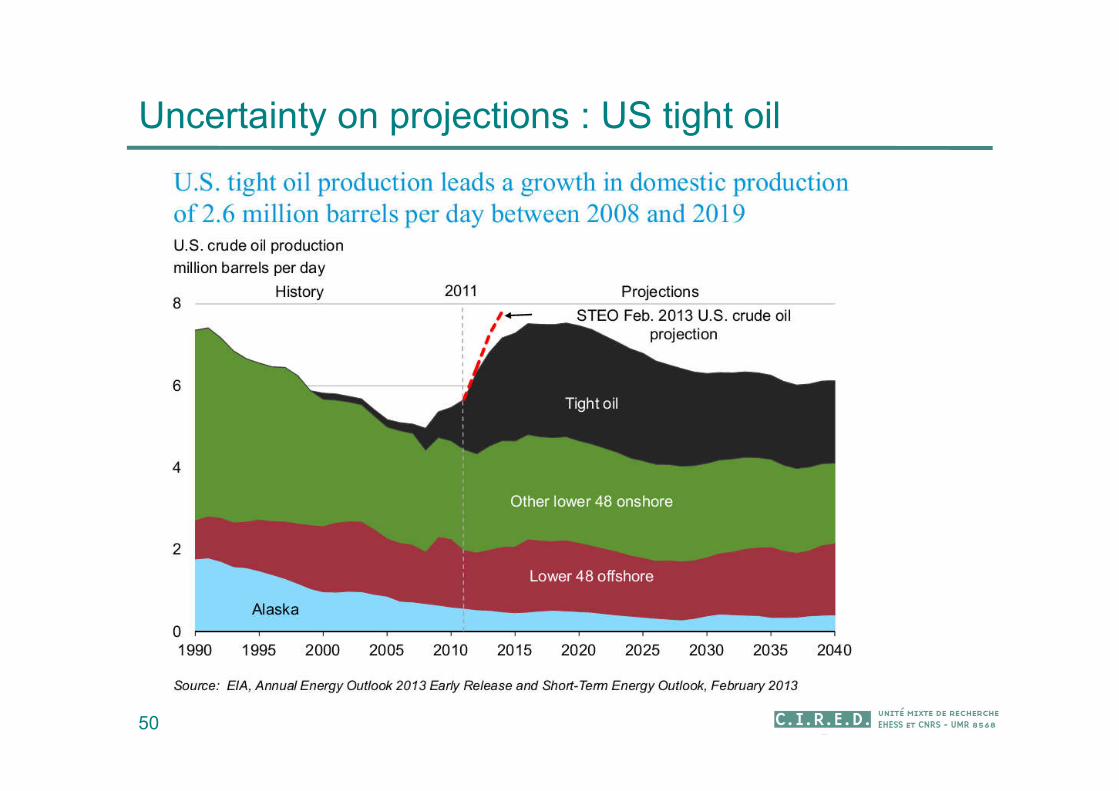

Uncertainty on projections : US tight oil

50

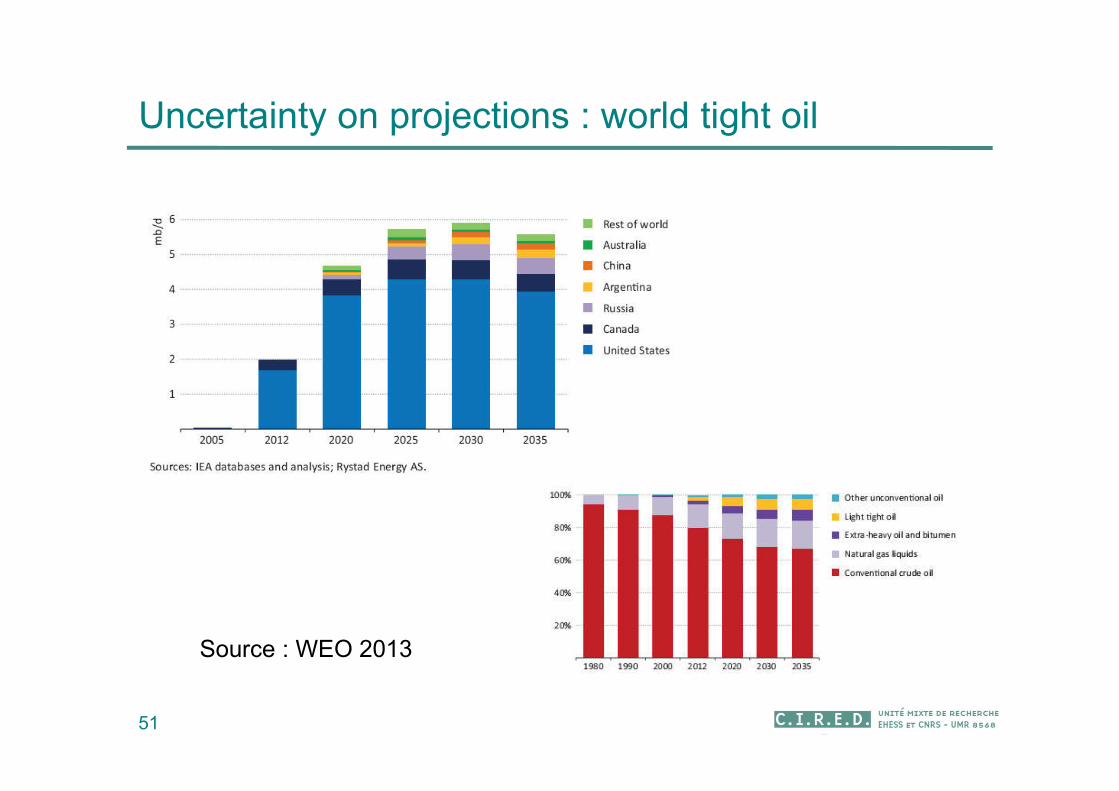

Uncertainty on projections : world tight oil

51

Source : WEO 2013

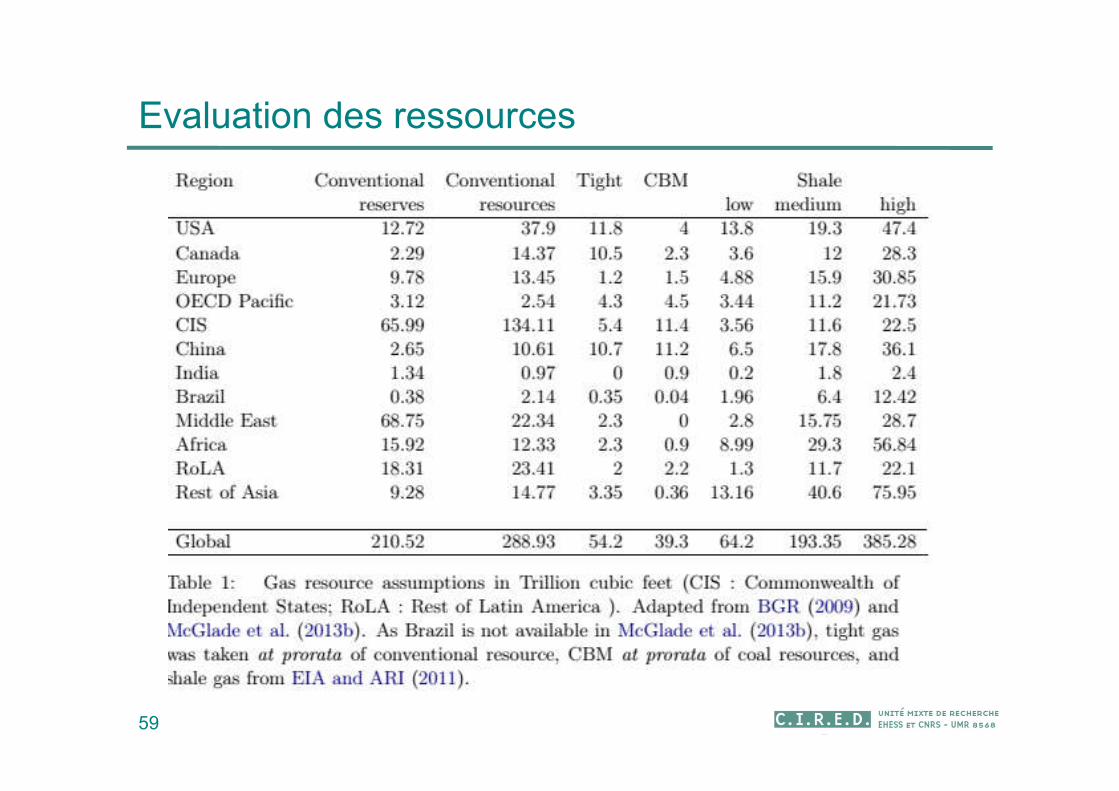

Evaluation des ressources

52

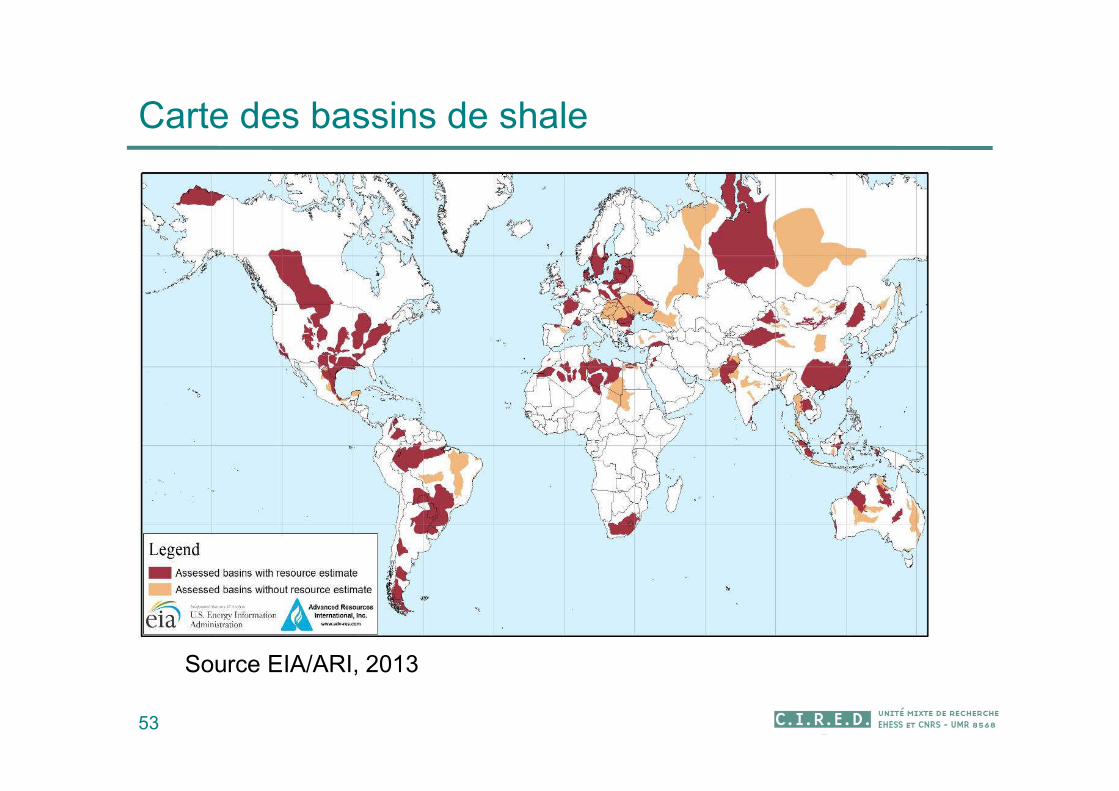

Carte des bassins de shale

53

Source EIA/ARI, 2013

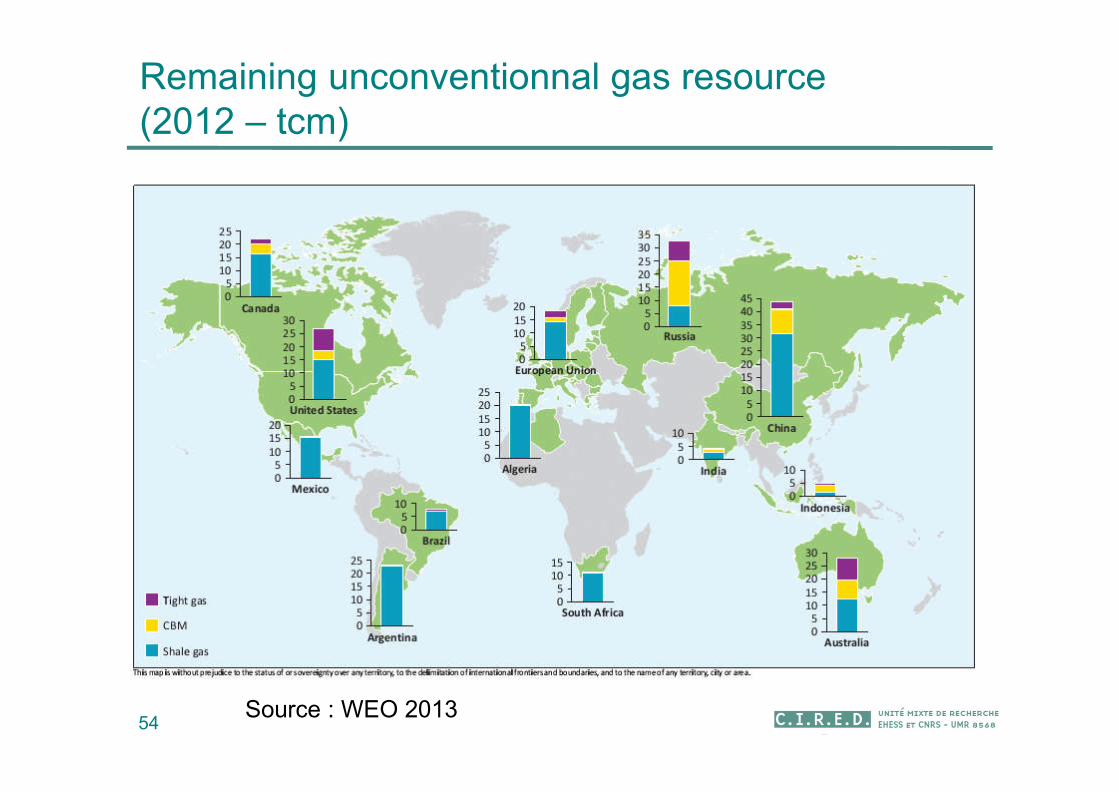

Remaining unconventionnal gas resource (2012 – tcm)

54Source : WEO 2013

Différence entre réserves et ressources

55

Limite économique

PossiblesProbablesProuvées

Réserves

Source : Global Energy Assessement, fig. 7.1

Ressource

Shale gas resources estimation methods (McGlade 2013)

56

Literature review ( subjective choice of study, no uncertainty)

Bottom-up analysis of geological parameters

Extrapolation of production experience

Problem : sweet spots versus non

Shale gas resources estimation methods (McGlade 2013)

57

Bottom-up analysis of geological parameters

Originally Gas in Place + Recovery Factor

Area or volume

Total organic content

Minerals type (clay, quartz)

Gas pressure

Recovery factor is 20-30% (80% for conventional gas)

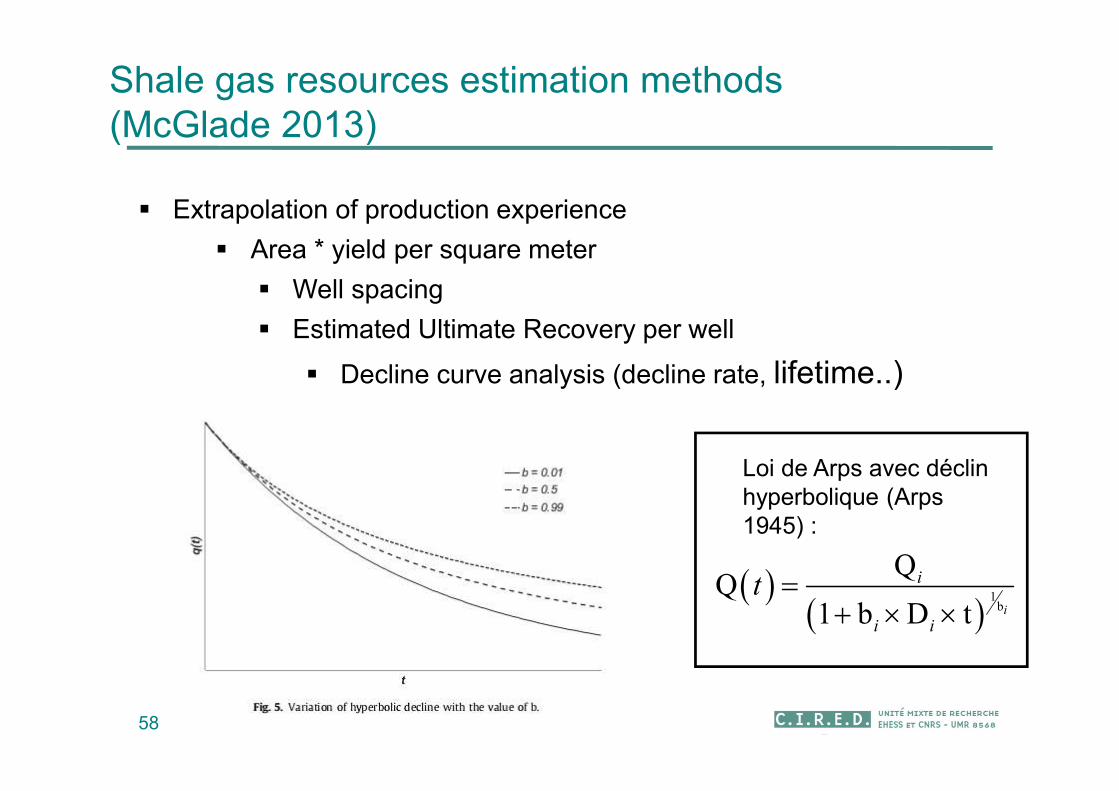

Shale gas resources estimation methods (McGlade 2013)

58

Extrapolation of production experience

Area * yield per square meter

Well spacing

Estimated Ultimate Recovery per well

Decline curve analysis (decline rate, lifetime..)

1b

1 b D t i

i

i i

t

Loi de Arps avec déclin hyperbolique (Arps 1945) :

Evaluation des ressources

59

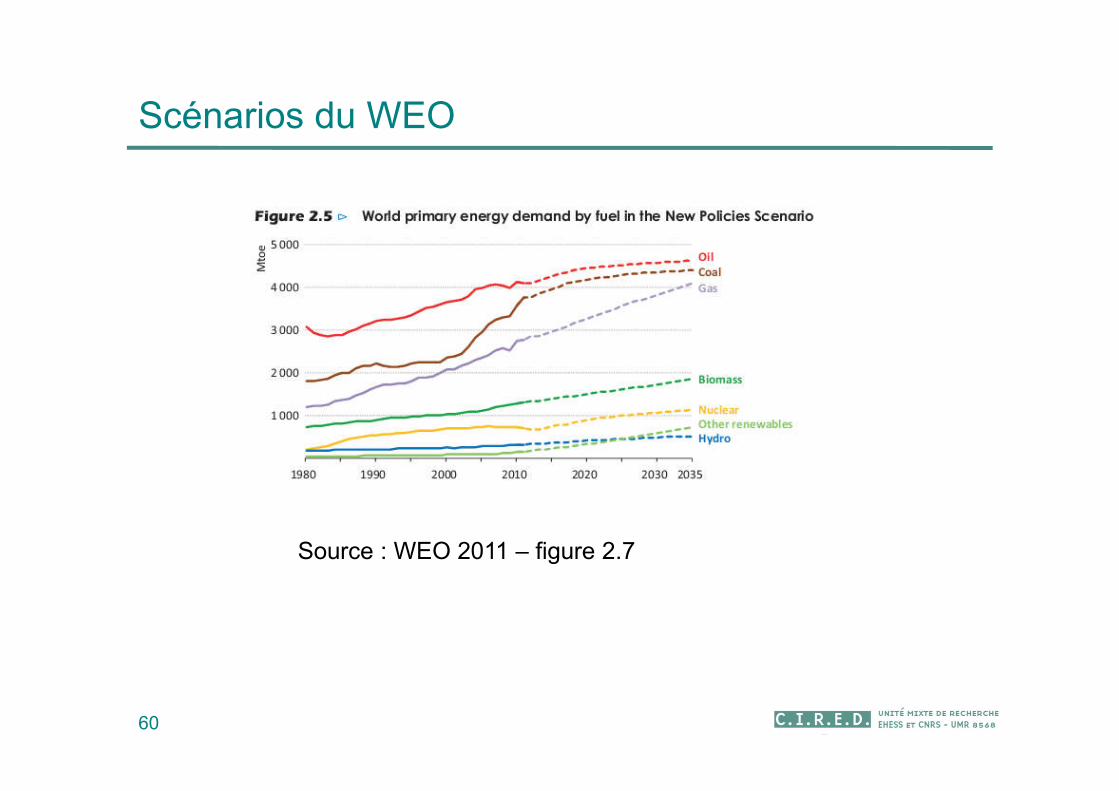

Scénarios du WEO

60

Source : WEO 2011 – figure 2.7

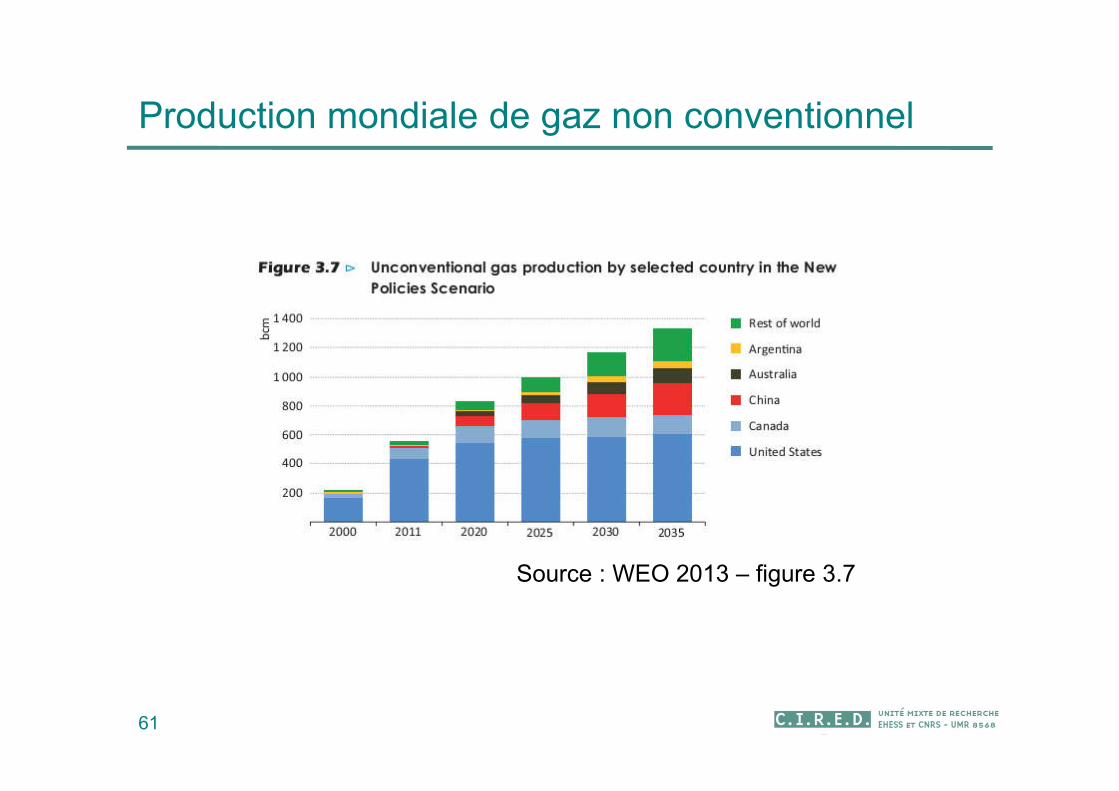

Production mondiale de gaz non conventionnel

61

Source : WEO 2013 – figure 3.7

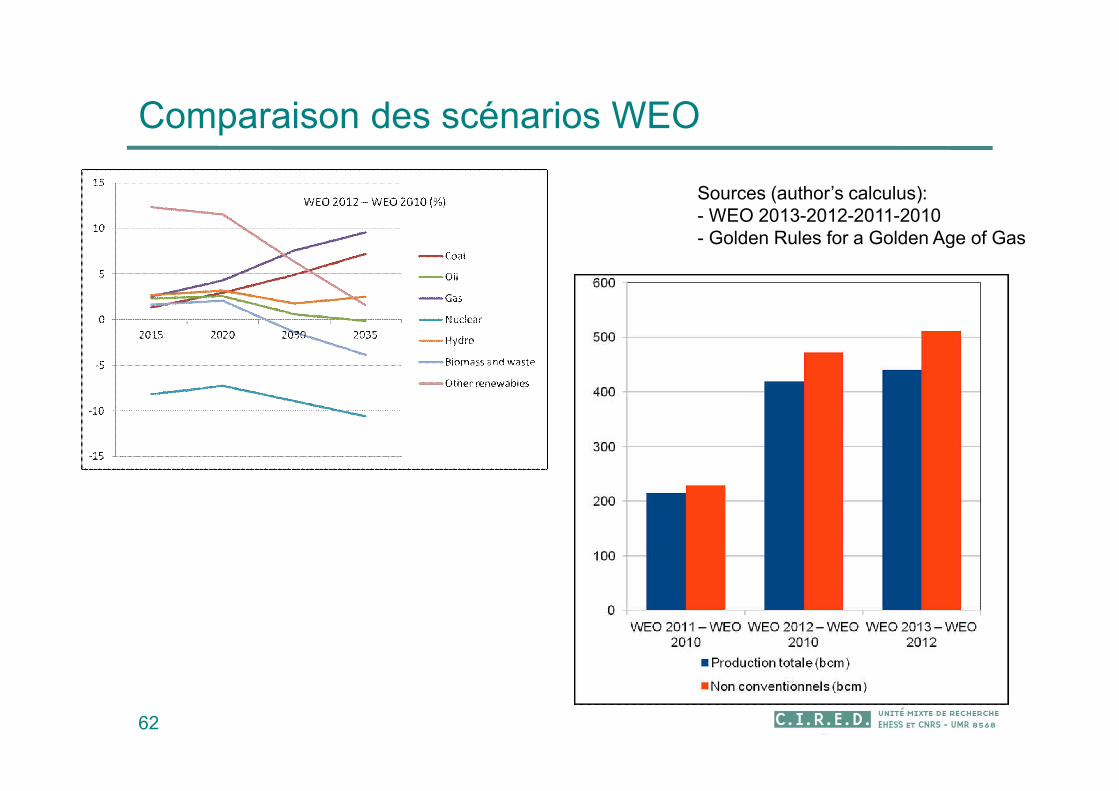

Comparaison des scénarios WEO

62

Sources (author’s calculus): - WEO 2013-2012-2011-2010- Golden Rules for a Golden Age of Gas

Impacts environnementaux

63

Impacts environnementaux

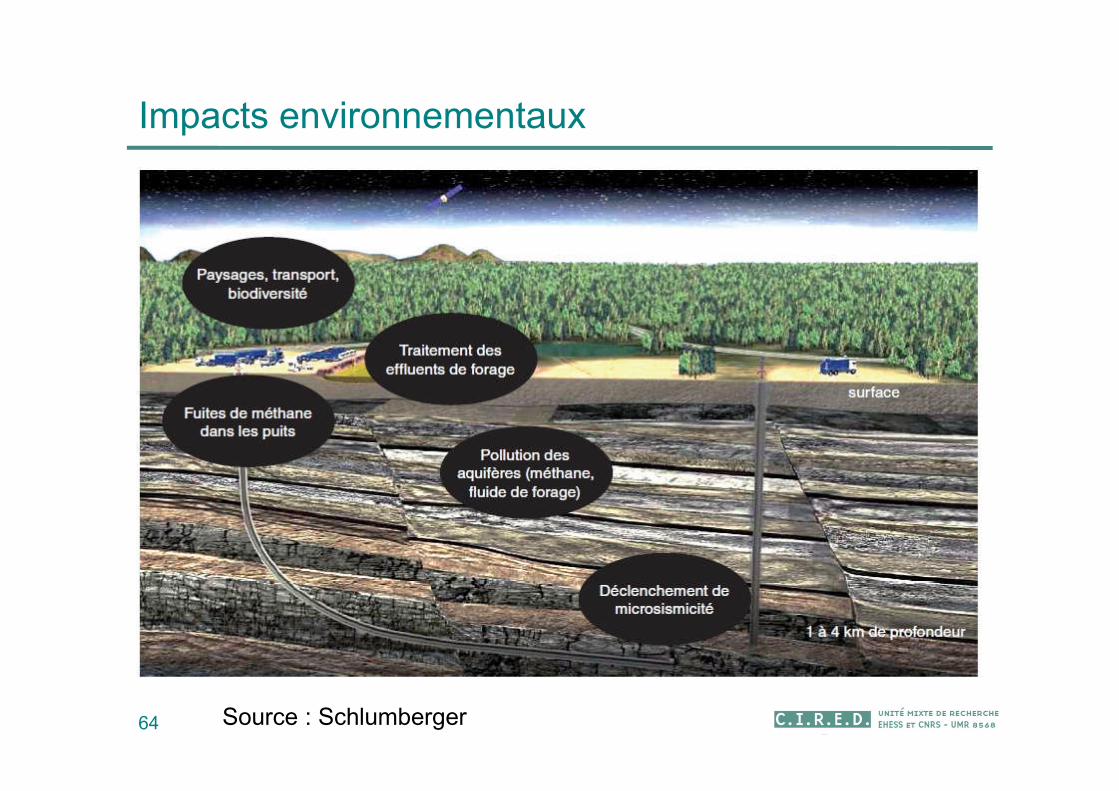

64 Source : Schlumberger

Impacts environnementaux

65

Différentes echelles

Quels problèmes peuvent être réglés par la technologie ?

Quid du surcouts de la qualité des forages, des institutions ?

Importation de gaz de schiste US : Nimby ?

GdS en Algérie : Nimby ?

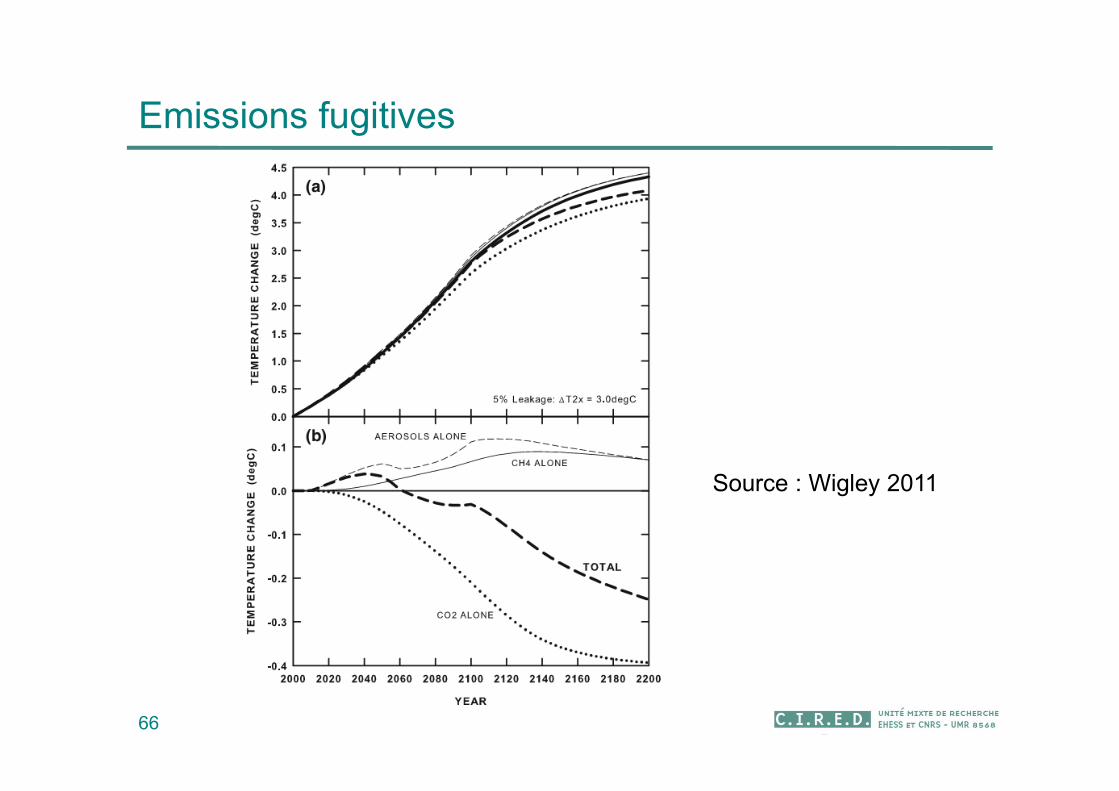

Emissions fugitives

66

Source : Wigley 2011

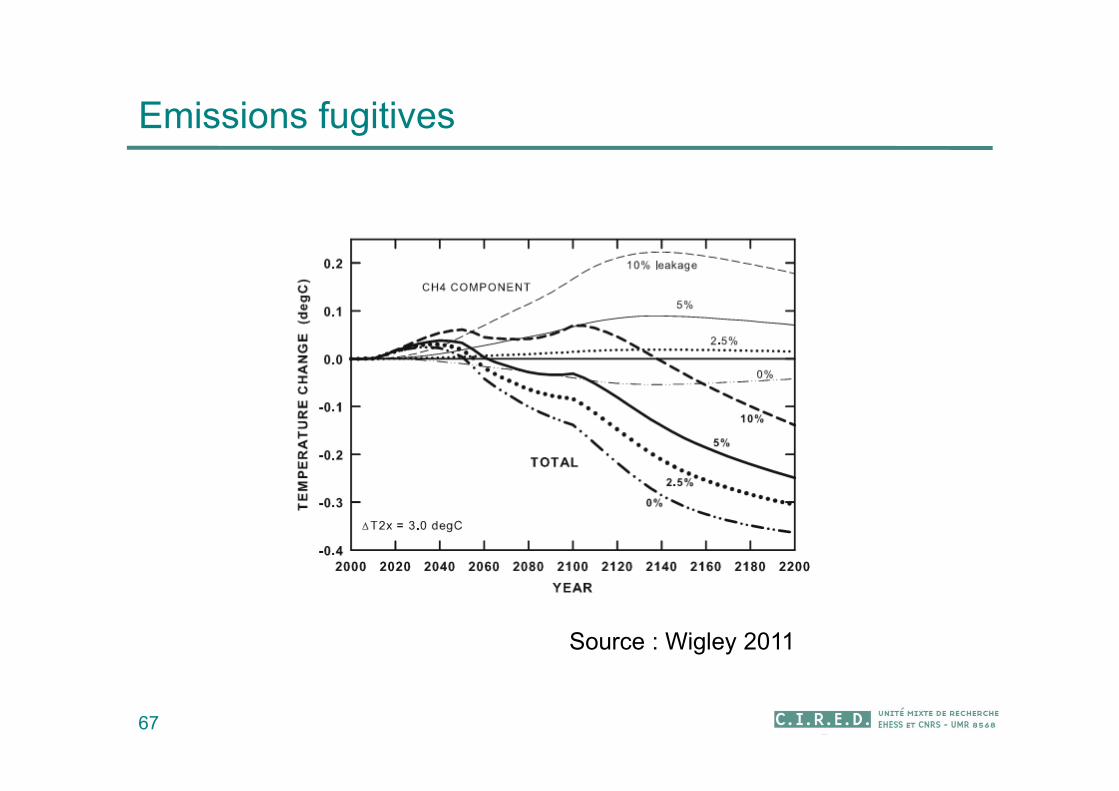

Emissions fugitives

67

Source : Wigley 2011

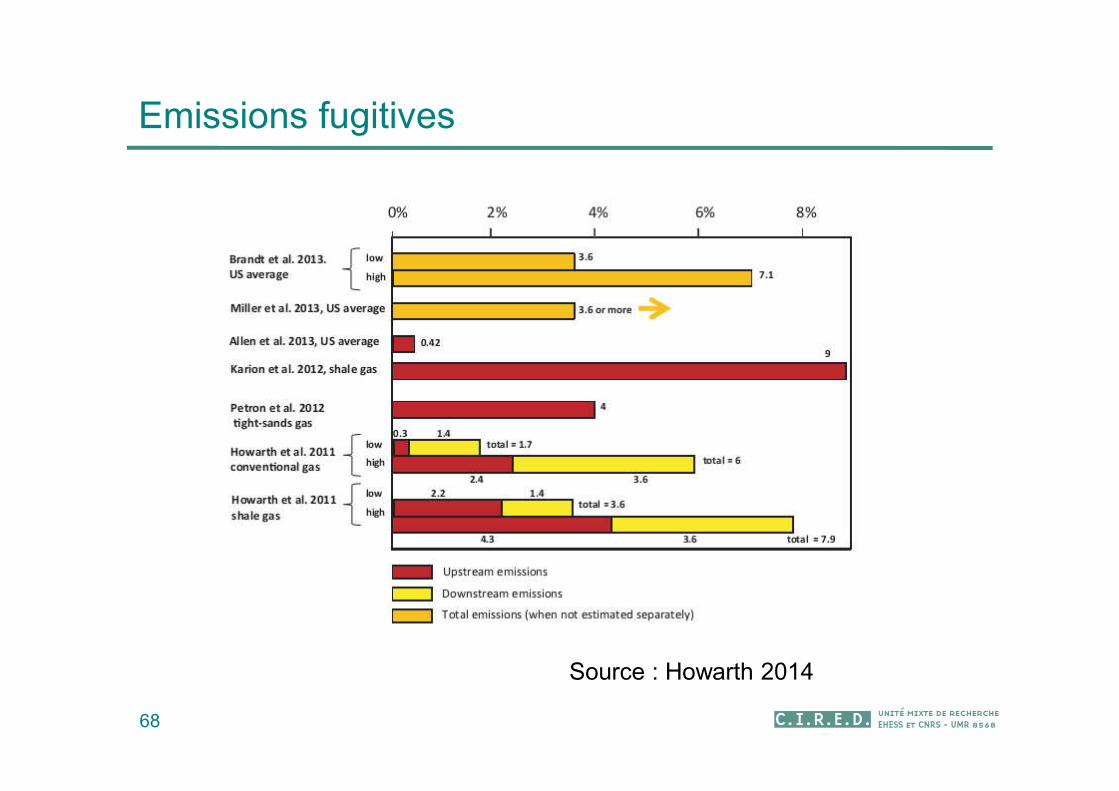

Emissions fugitives

68

Source : Howarth 2014

Emissions fugitives

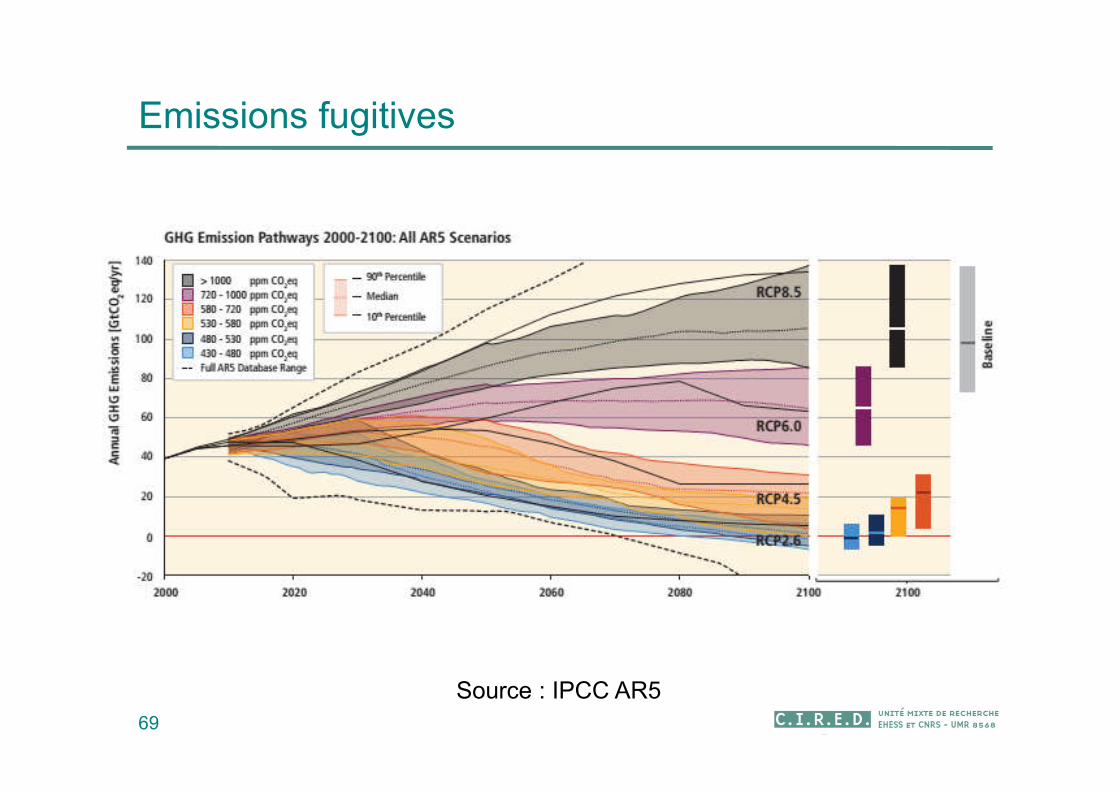

69

Source : IPCC AR5

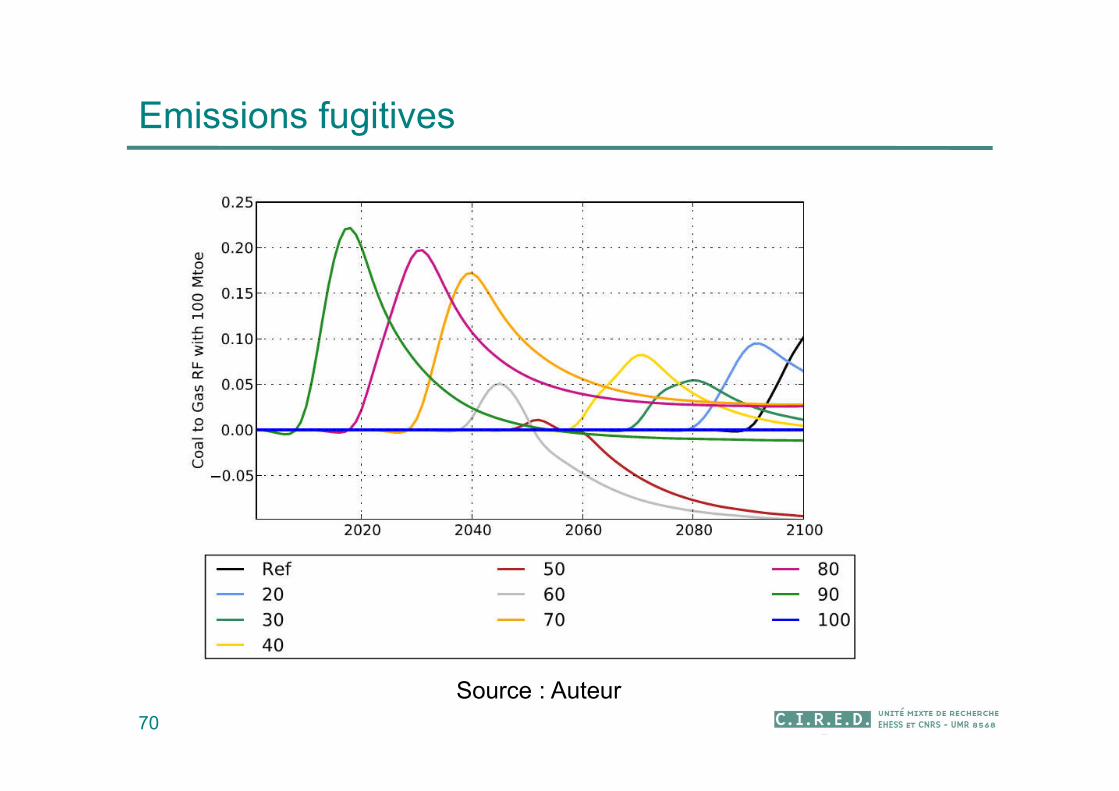

Emissions fugitives

70

Source : Auteur

Le gaz de Lacq

71

Le gaz de Lacq

72

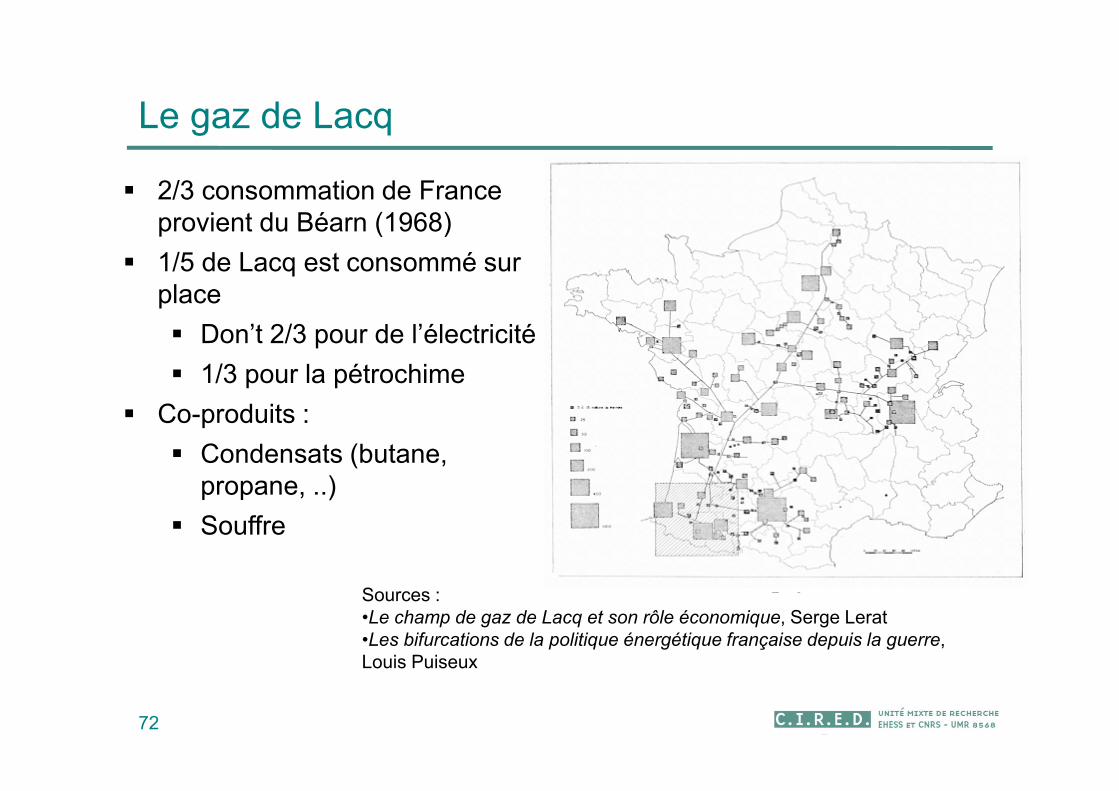

2/3 consommation de France provient du Béarn (1968)

1/5 de Lacq est consommé sur place

Don’t 2/3 pour de l’électricité

1/3 pour la pétrochime

Co-produits :

Condensats (butane, propane, ..)

Souffre

Sources :•Le champ de gaz de Lacq et son rôle économique, Serge Lerat•Les bifurcations de la politique énergétique française depuis la guerre, Louis Puiseux

Le principe de précaution

73

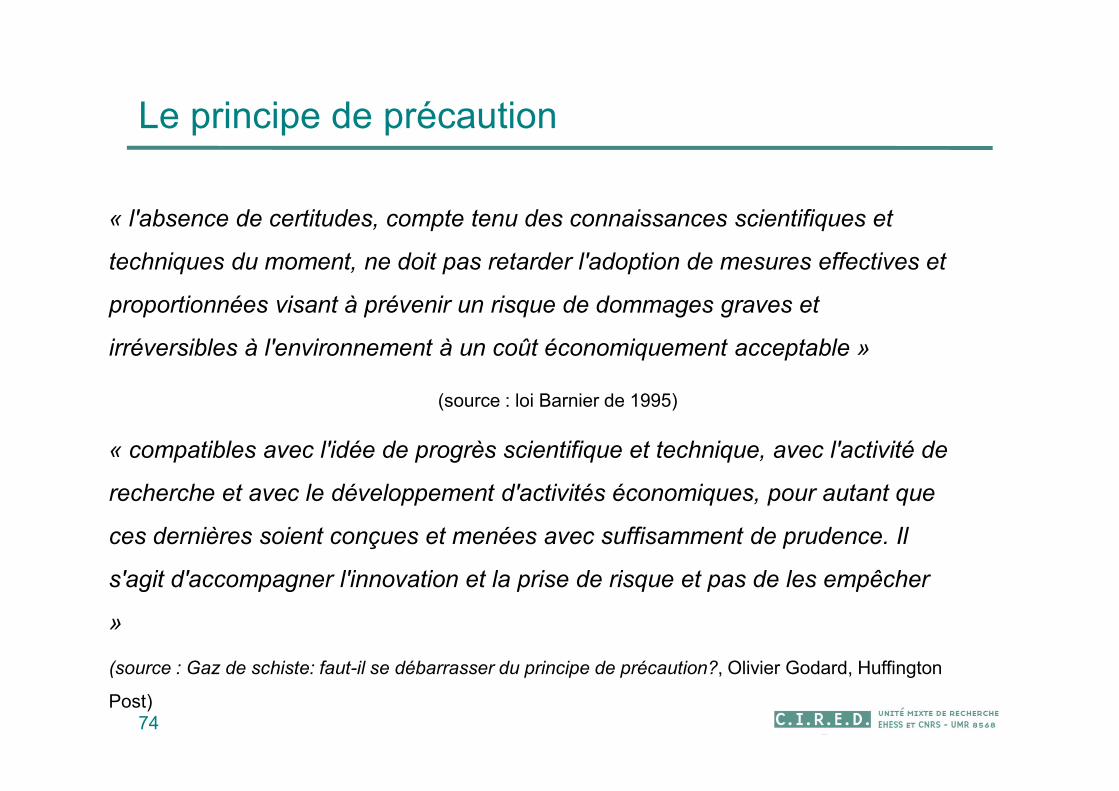

Le principe de précaution

74

« l'absence de certitudes, compte tenu des connaissances scientifiques et

techniques du moment, ne doit pas retarder l'adoption de mesures effectives et

proportionnées visant à prévenir un risque de dommages graves et

irréversibles à l'environnement à un coût économiquement acceptable »

(source : loi Barnier de 1995)

« compatibles avec l'idée de progrès scientifique et technique, avec l'activité de

recherche et avec le développement d'activités économiques, pour autant que

ces dernières soient conçues et menées avec suffisamment de prudence. Il

s'agit d'accompagner l'innovation et la prise de risque et pas de les empêcher

»

(source : Gaz de schiste: faut-il se débarrasser du principe de précaution?, Olivier Godard, Huffington

Post)

Scénarios prospectifs :GdS et LTO aux US : le

paradoxe de la compétitivité

75

Succès US : causes

76

Couplage de technologies

Géologie favorable – densité de population

Propriété du sol

Degré de libéralisation du marché gazier, étendu du réseau

Culture du pétrole, tissu denses de sociétés spécialisées

Réglementation favorable (notamment sur l’eau)

Succès US

77

Chute du prix du gaz

Prix spot /3 depuis 2008, prix industriel 3-4 fois moins cher qu’en Europe

Nombreuses retombées économiques

Revenus des ménages - emplois

Prix de l’électricité (2-3 fois moins cher /Europe)

Investissements en prétrochimie

Projets d’exporation

Plutôt vers le marché asiatique

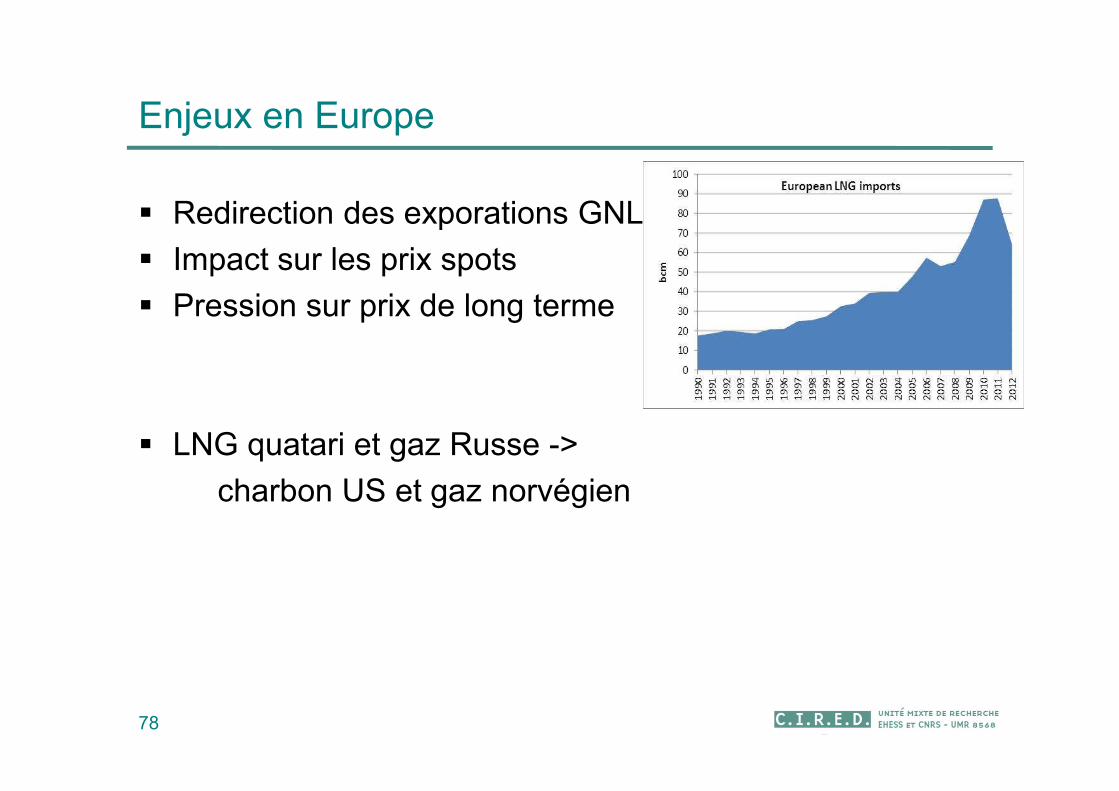

Enjeux en Europe

Redirection des exporations GNL

Impact sur les prix spots

Pression sur prix de long terme

LNG quatari et gaz Russe ->

charbon US et gaz norvégien

78

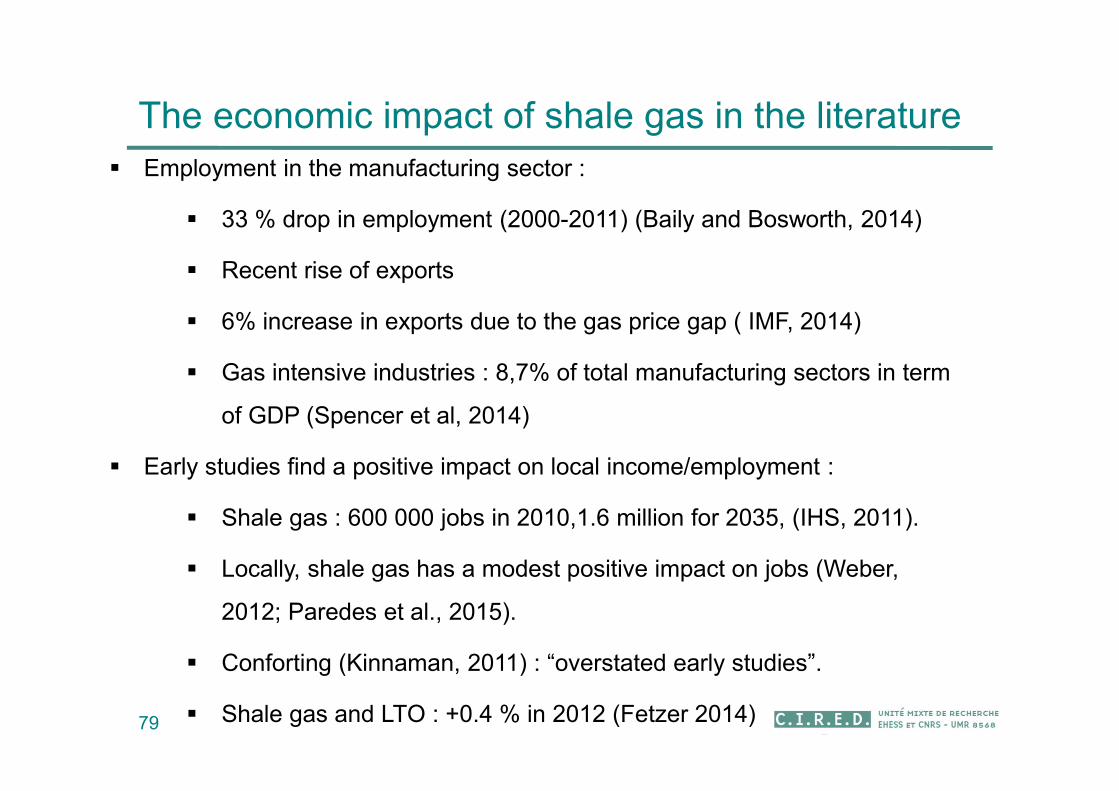

The economic impact of shale gas in the literature

Employment in the manufacturing sector :

33 % drop in employment (2000-2011) (Baily and Bosworth, 2014)

Recent rise of exports

6% increase in exports due to the gas price gap ( IMF, 2014)

Gas intensive industries : 8,7% of total manufacturing sectors in term

of GDP (Spencer et al, 2014)

Early studies find a positive impact on local income/employment :

Shale gas : 600 000 jobs in 2010,1.6 million for 2035, (IHS, 2011).

Locally, shale gas has a modest positive impact on jobs (Weber,

2012; Paredes et al., 2015).

Conforting (Kinnaman, 2011) : “overstated early studies”.

Shale gas and LTO : +0.4 % in 2012 (Fetzer 2014)79

80

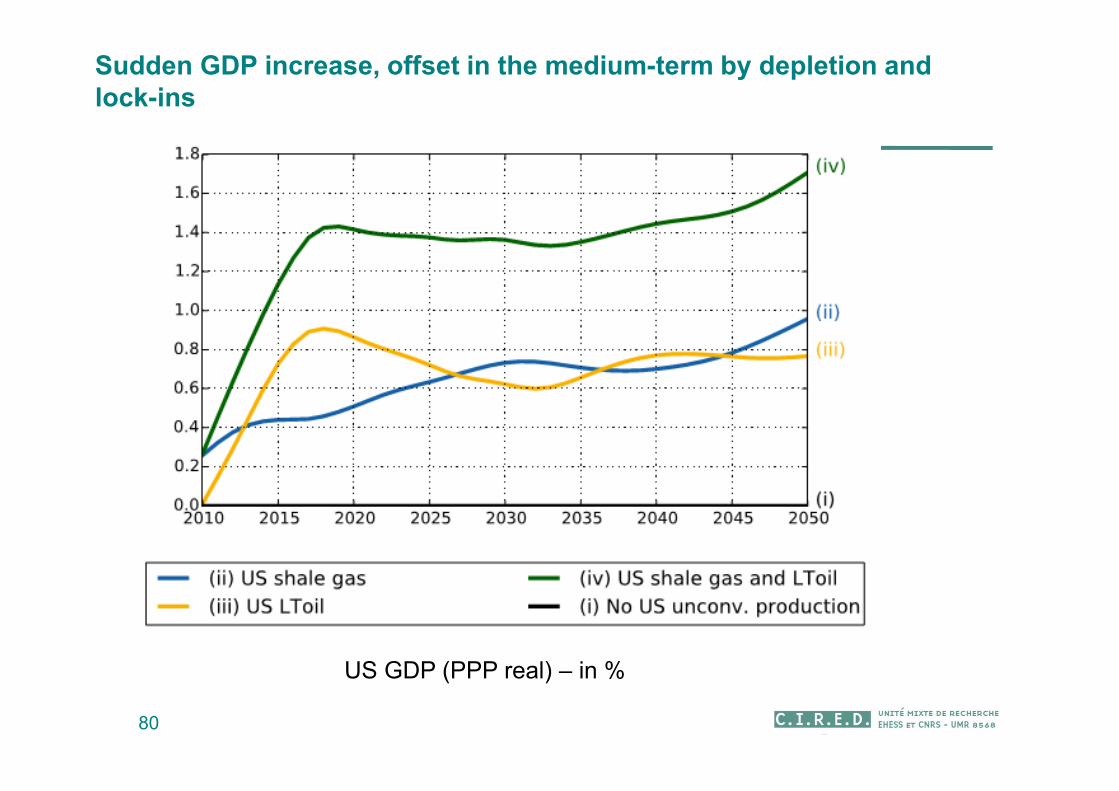

Sudden GDP increase, offset in the medium-term by depletion and lock-ins

US GDP (PPP real) – in %

81

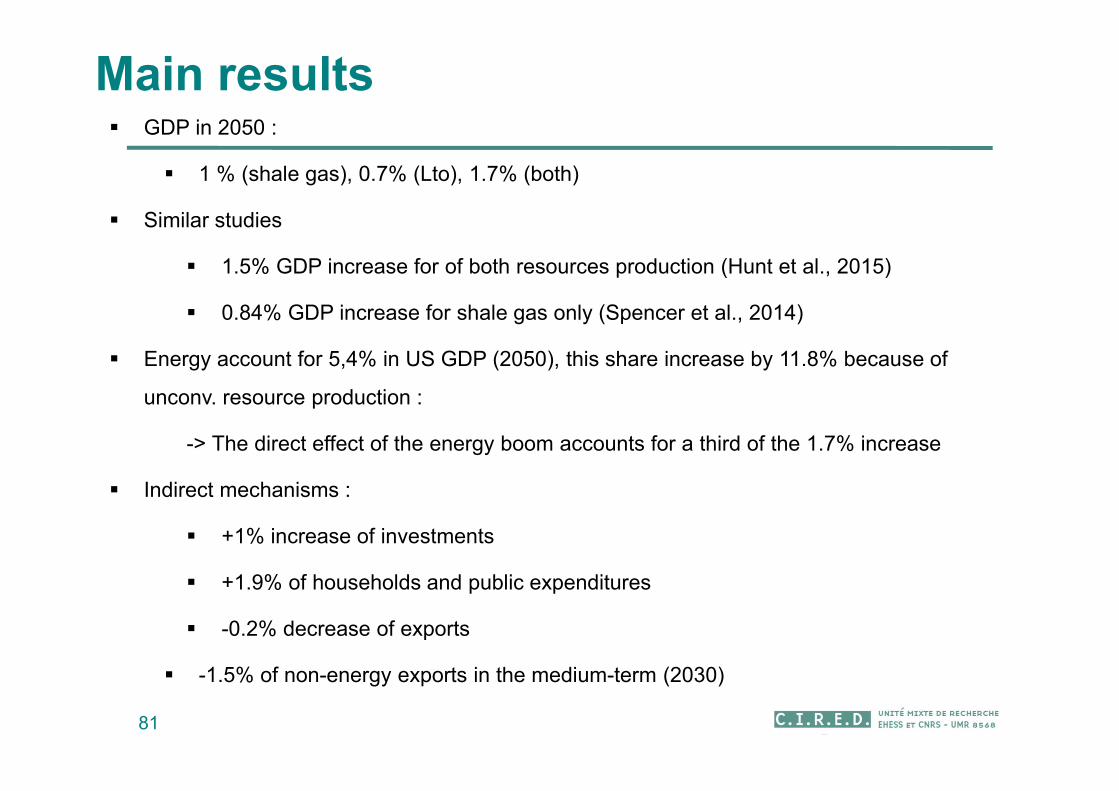

Main results GDP in 2050 :

1 % (shale gas), 0.7% (Lto), 1.7% (both)

Similar studies

1.5% GDP increase for of both resources production (Hunt et al., 2015)

0.84% GDP increase for shale gas only (Spencer et al., 2014)

Energy account for 5,4% in US GDP (2050), this share increase by 11.8% because of

unconv. resource production :

-> The direct effect of the energy boom accounts for a third of the 1.7% increase

Indirect mechanisms :

+1% increase of investments

+1.9% of households and public expenditures

-0.2% decrease of exports

-1.5% of non-energy exports in the medium-term (2030)

82

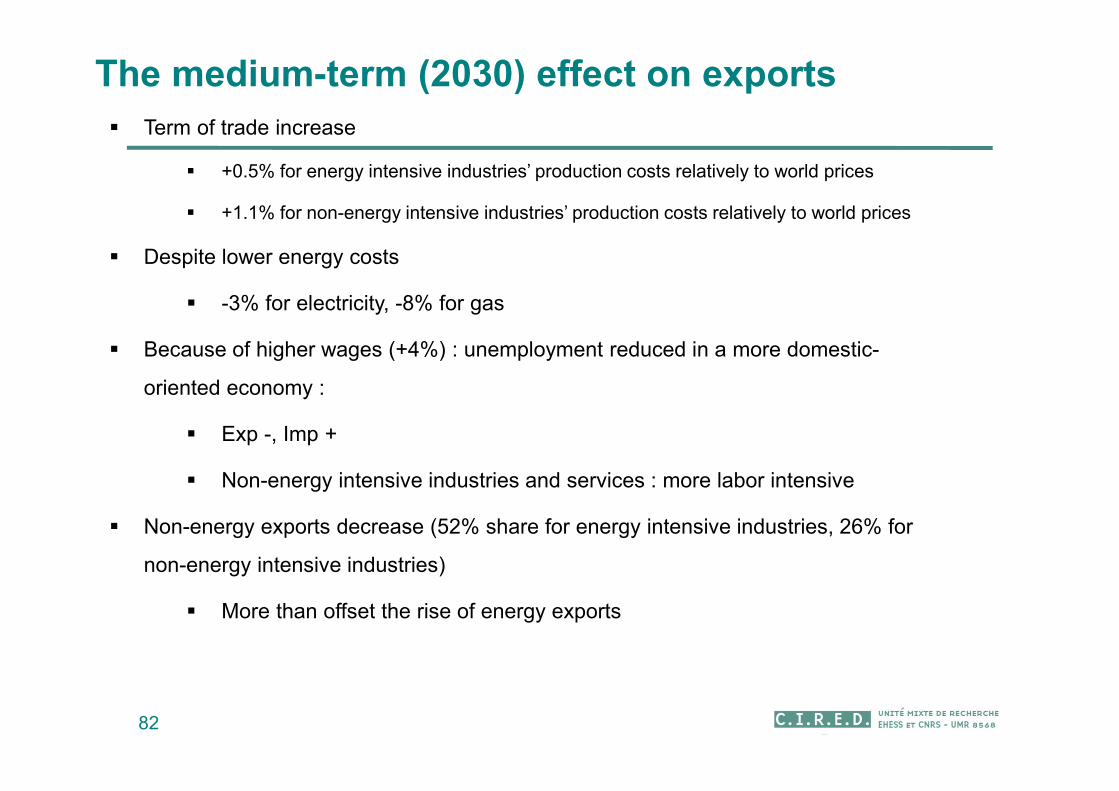

The medium-term (2030) effect on exports

Term of trade increase

+0.5% for energy intensive industries’ production costs relatively to world prices

+1.1% for non-energy intensive industries’ production costs relatively to world prices

Despite lower energy costs

-3% for electricity, -8% for gas

Because of higher wages (+4%) : unemployment reduced in a more domestic-

oriented economy :

Exp -, Imp +

Non-energy intensive industries and services : more labor intensive

Non-energy exports decrease (52% share for energy intensive industries, 26% for

non-energy intensive industries)

More than offset the rise of energy exports

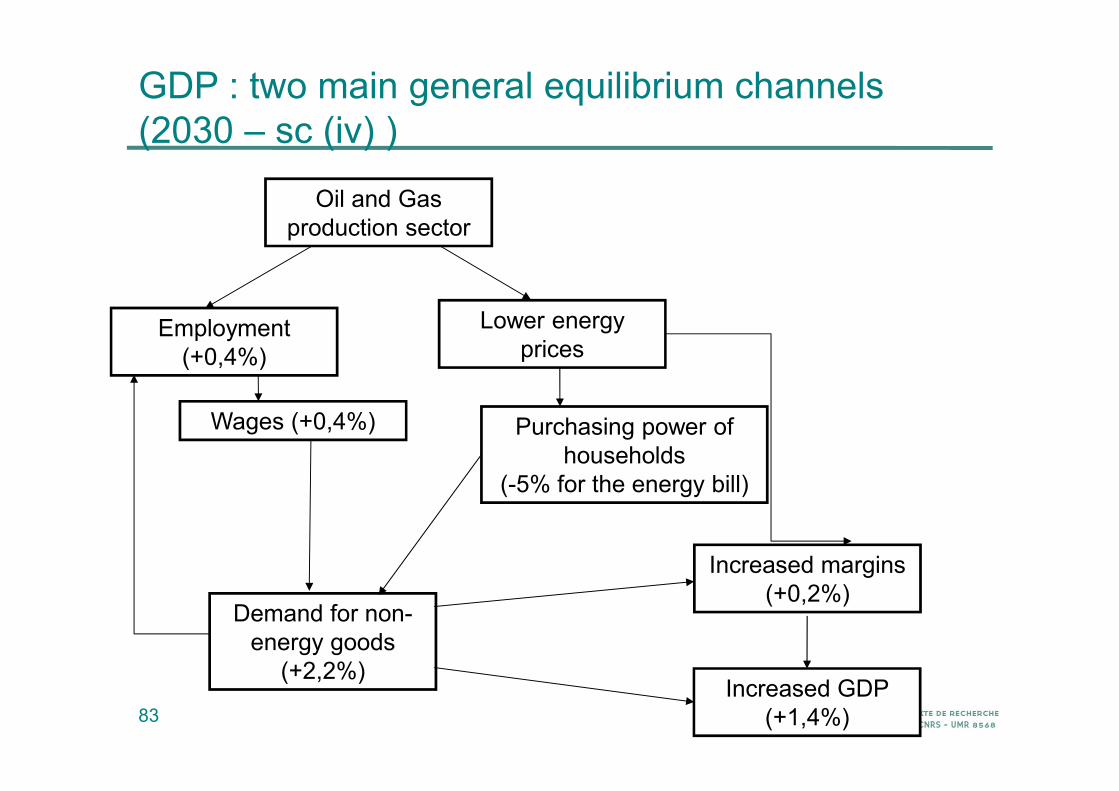

GDP : two main general equilibrium channels (2030 – sc (iv) )

83

Purchasing power of households

(-5% for the energy bill)

Lower energy prices

Demand for non-energy goods

(+2,2%)

Employment (+0,4%)

Oil and Gas production sector

Wages (+0,4%)

Increased margins (+0,2%)

Increased GDP (+1,4%)

84

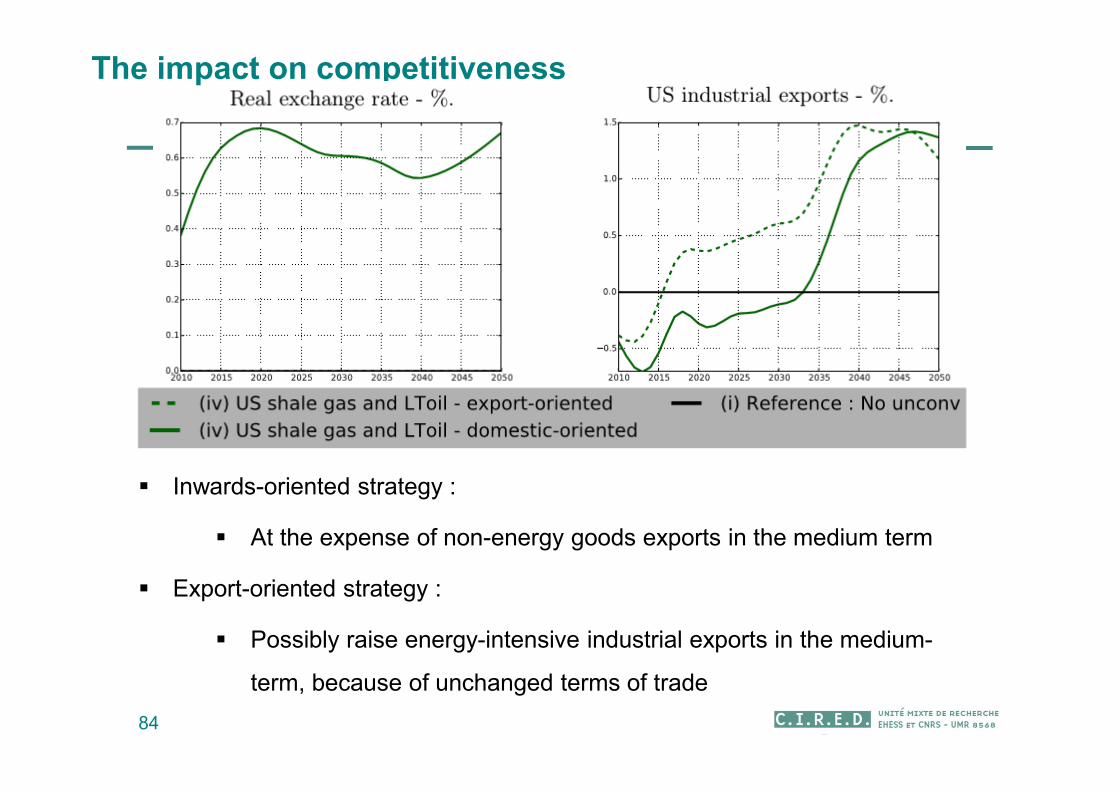

The impact on competitiveness

Inwards-oriented strategy :

At the expense of non-energy goods exports in the medium term

Export-oriented strategy :

Possibly raise energy-intensive industrial exports in the medium-

term, because of unchanged terms of trade

85

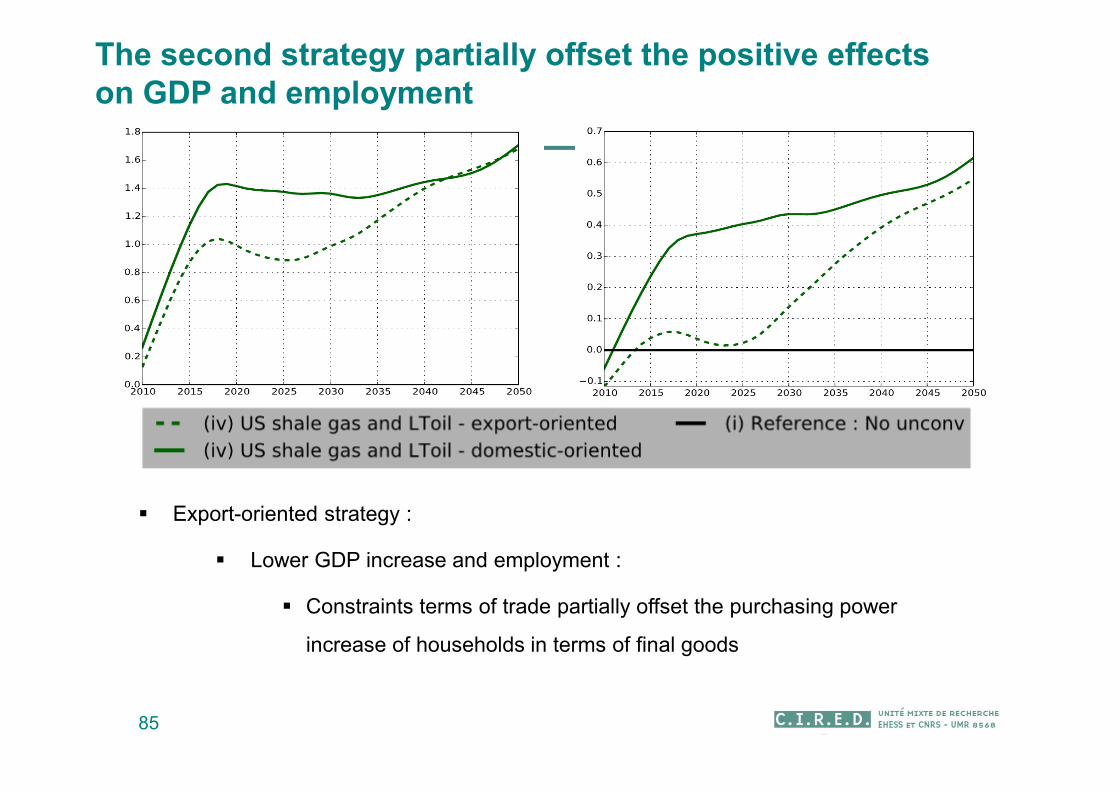

The second strategy partially offset the positive effects on GDP and employment

Export-oriented strategy :

Lower GDP increase and employment :

Constraints terms of trade partially offset the purchasing power

increase of households in terms of final goods

Bibliography

86

Bibliography

87

Bibliography

88

Merci pour votre attention !

89

Contact :

Présentation :

http://www.imaclim.centre-cired.fr/-> Equipe-> Christophe Cassen

Annexe 1Dynamique d’exploitation du

pétrole et politiques climatiques

90

91

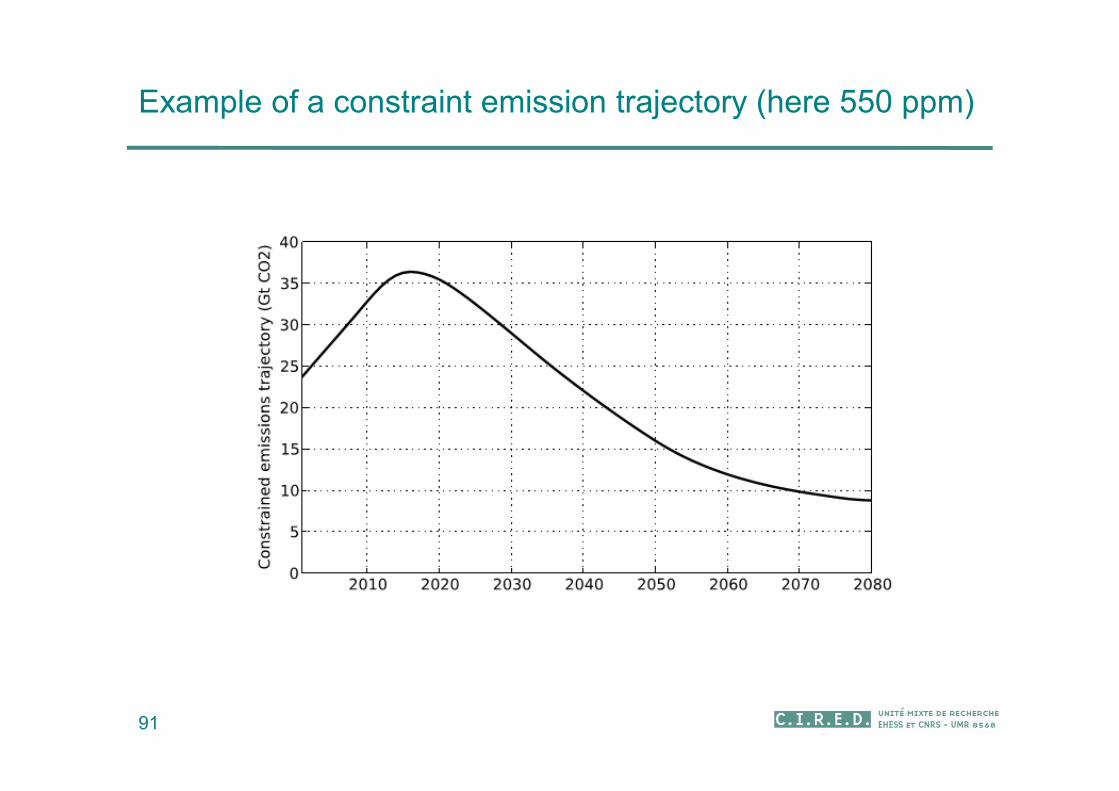

Example of a constraint emission trajectory (here 550 ppm)

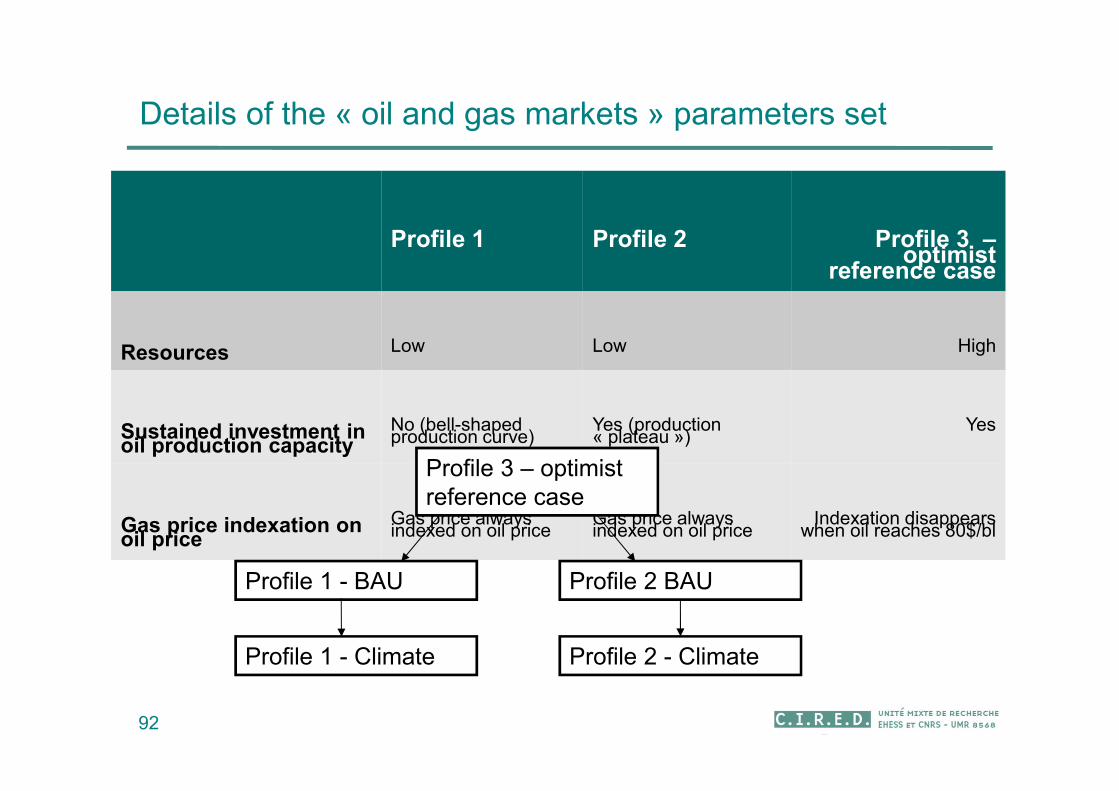

Details of the « oil and gas markets » parameters set

92

Profile 1 Profile 2 Profile 3 –optimist

reference case

Resources Low Low High

Sustained investment in oil production capacity

No (bell-shaped production curve)

Yes (production « plateau »)

Yes

Gas price indexation on oil price

Gas price always indexed on oil price

Gas price always indexed on oil price

Indexation disappears when oil reaches 80$/bl

Profile 3 – optimist reference case

Profile 1 - BAU Profile 2 BAU

Profile 1 - Climate Profile 2 - Climate

Influence of the other parameters

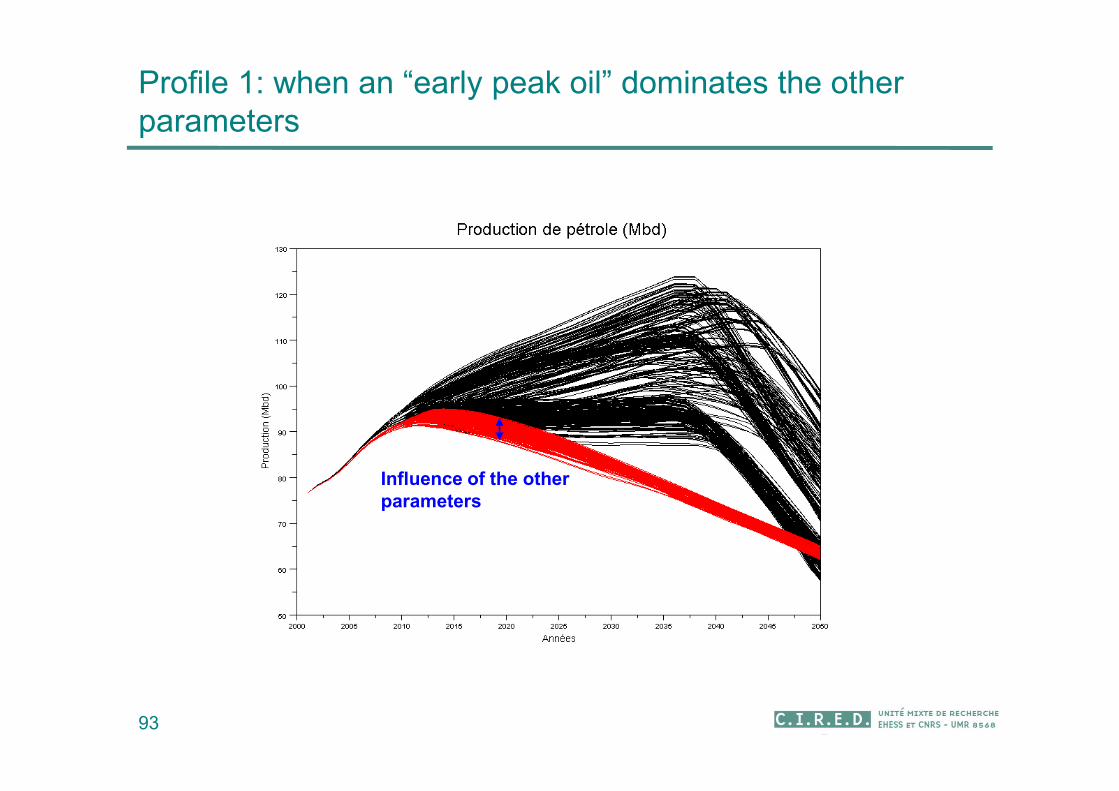

93

Profile 1: when an “early peak oil” dominates the other parameters

94

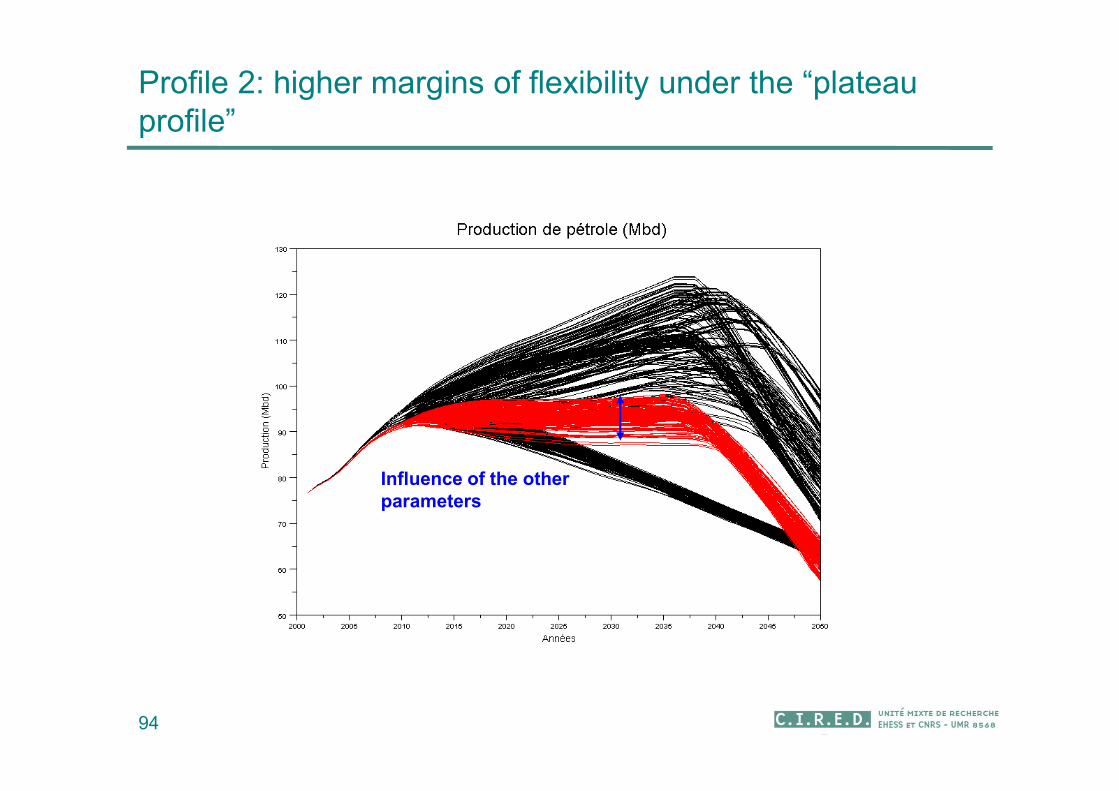

Influence of the other parameters

Profile 2: higher margins of flexibility under the “plateau profile”

95

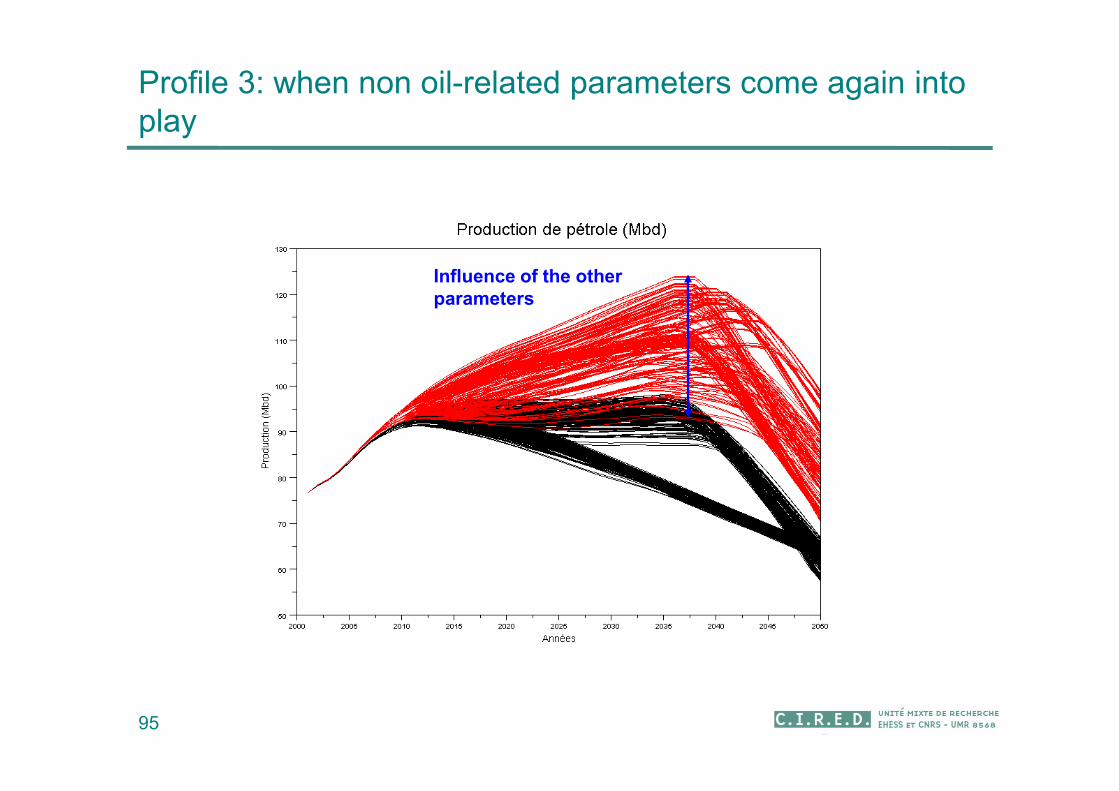

Influence of the other parameters

Profile 3: when non oil-related parameters come again into play

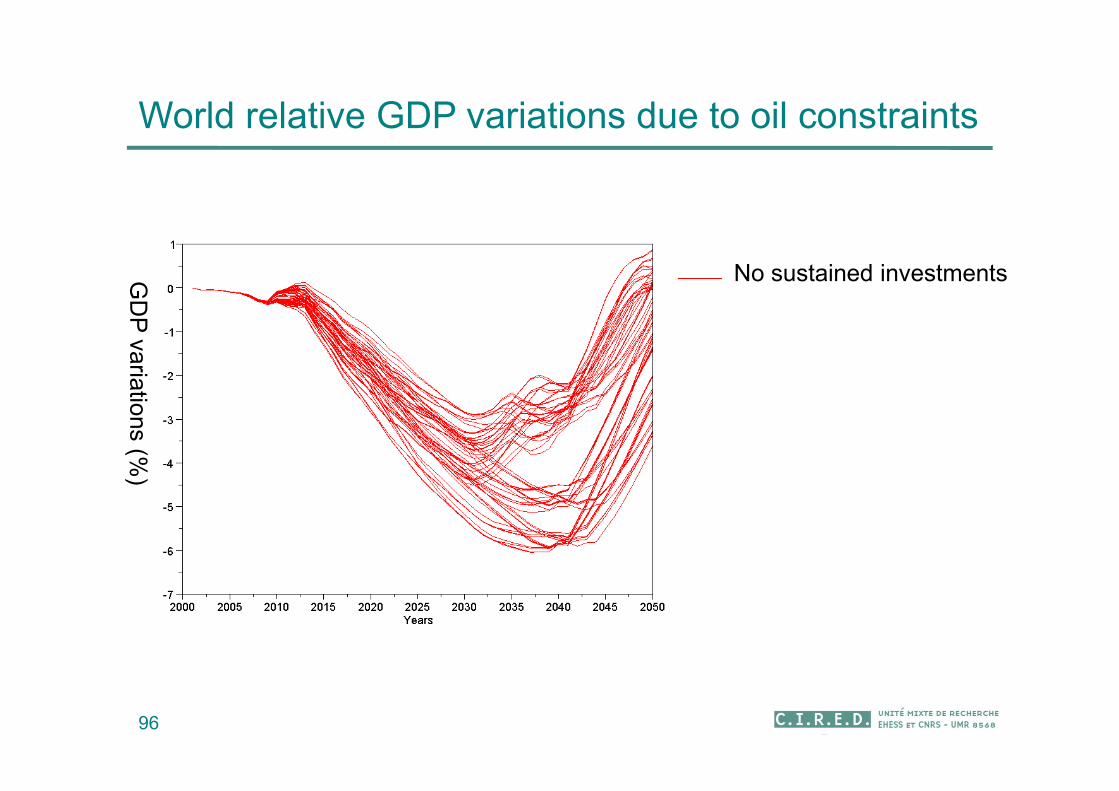

World relative GDP variations due to oil constraints

96

No sustained investmentsGD

P va

riatio

ns (%

)

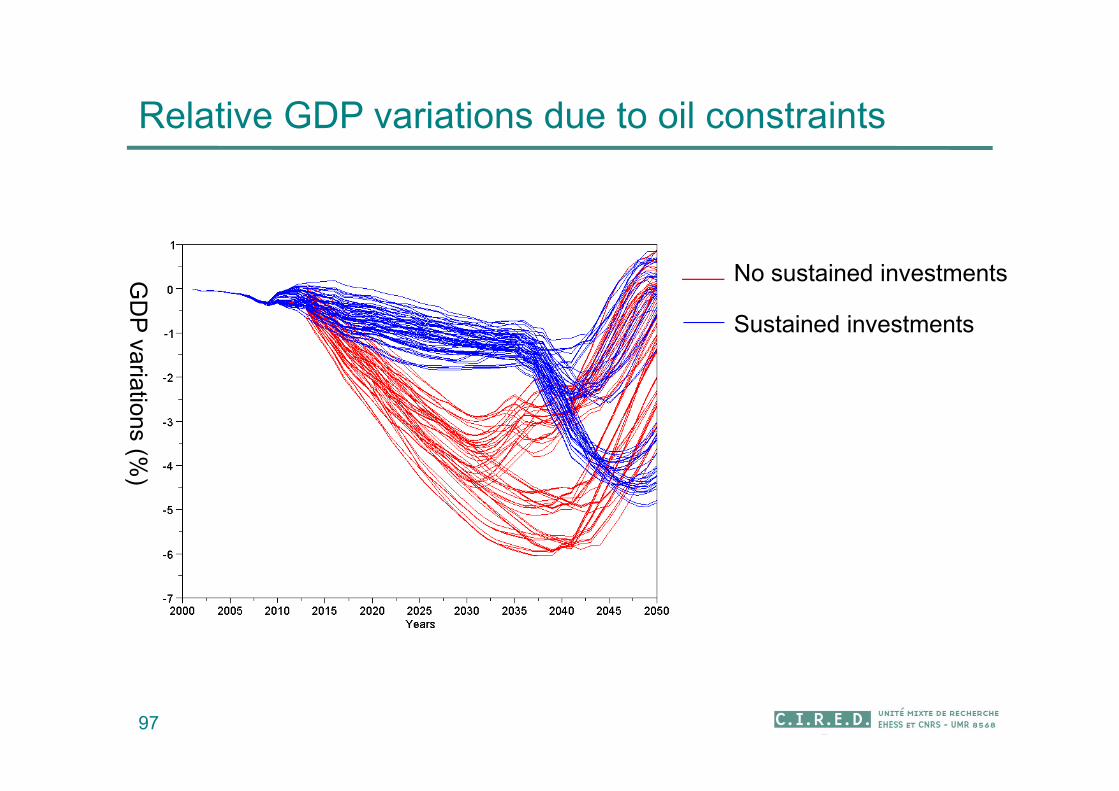

Relative GDP variations due to oil constraints

97

No sustained investmentsGD

P va

riatio

ns (%

)

Sustained investments

Relative GDP variations due to oil constraints

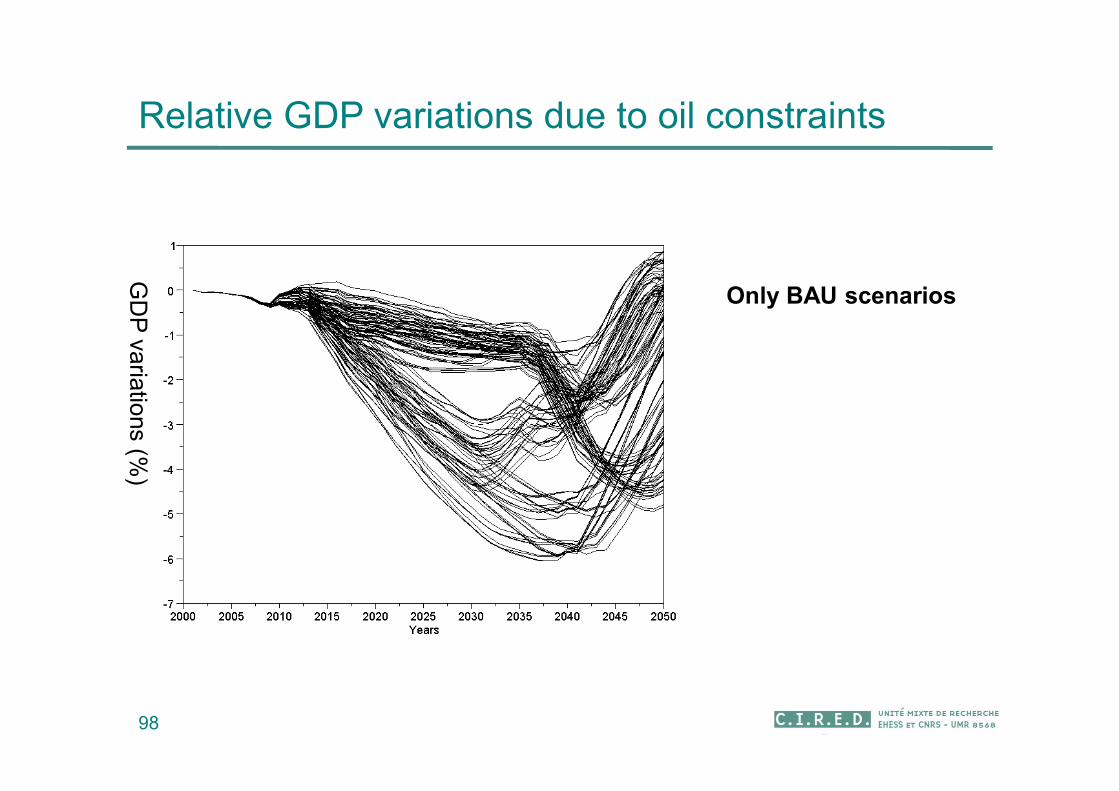

98

GD

P va

riatio

ns (%

)

Only BAU scenarios

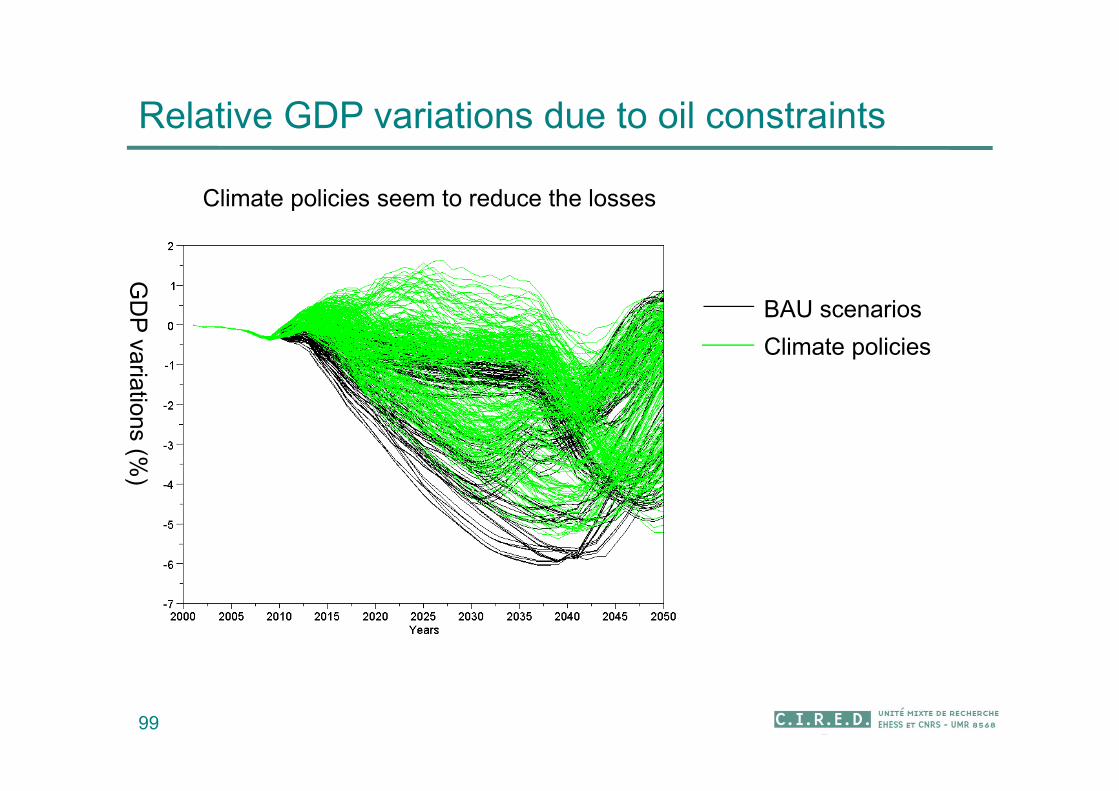

Relative GDP variations due to oil constraints

99

BAU scenarios

GD

P va

riatio

ns (%

)

Climate policies

Climate policies seem to reduce the losses

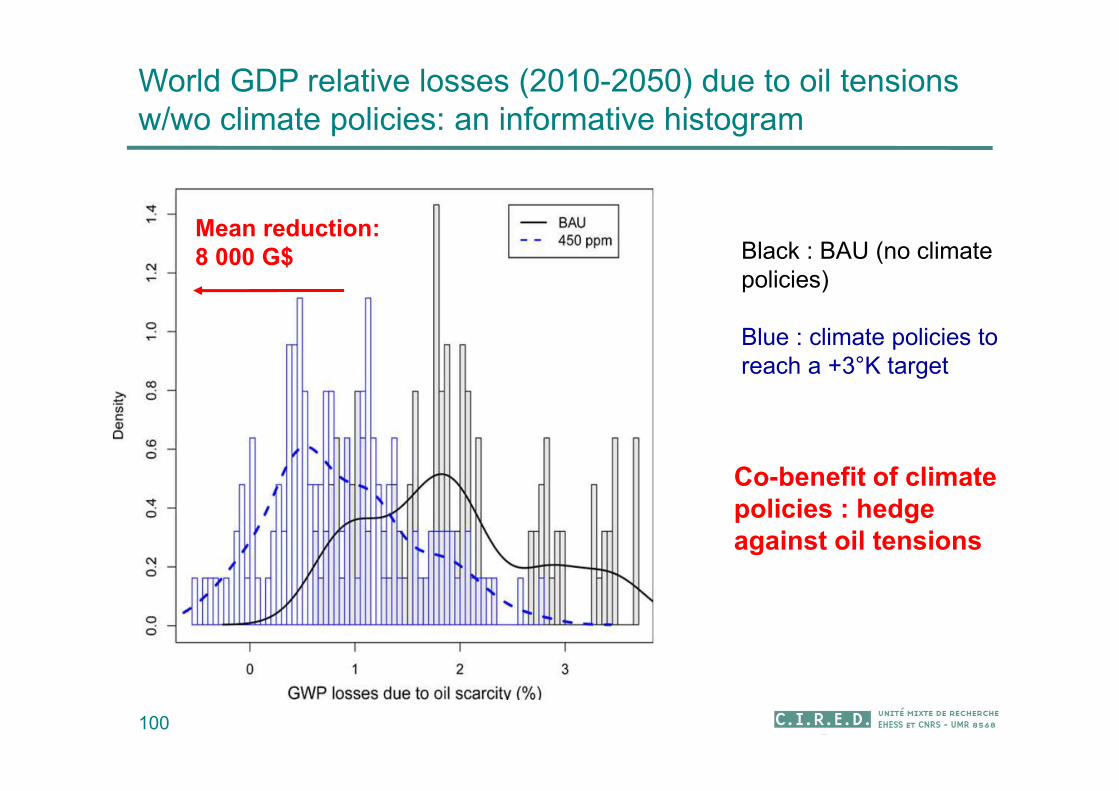

World GDP relative losses (2010-2050) due to oil tensions w/wo climate policies: an informative histogram

100

Black : BAU (no climate policies)

Blue : climate policies to reach a +3°K target

Mean reduction: 8 000 G$

Co-benefit of climate policies : hedge against oil tensions

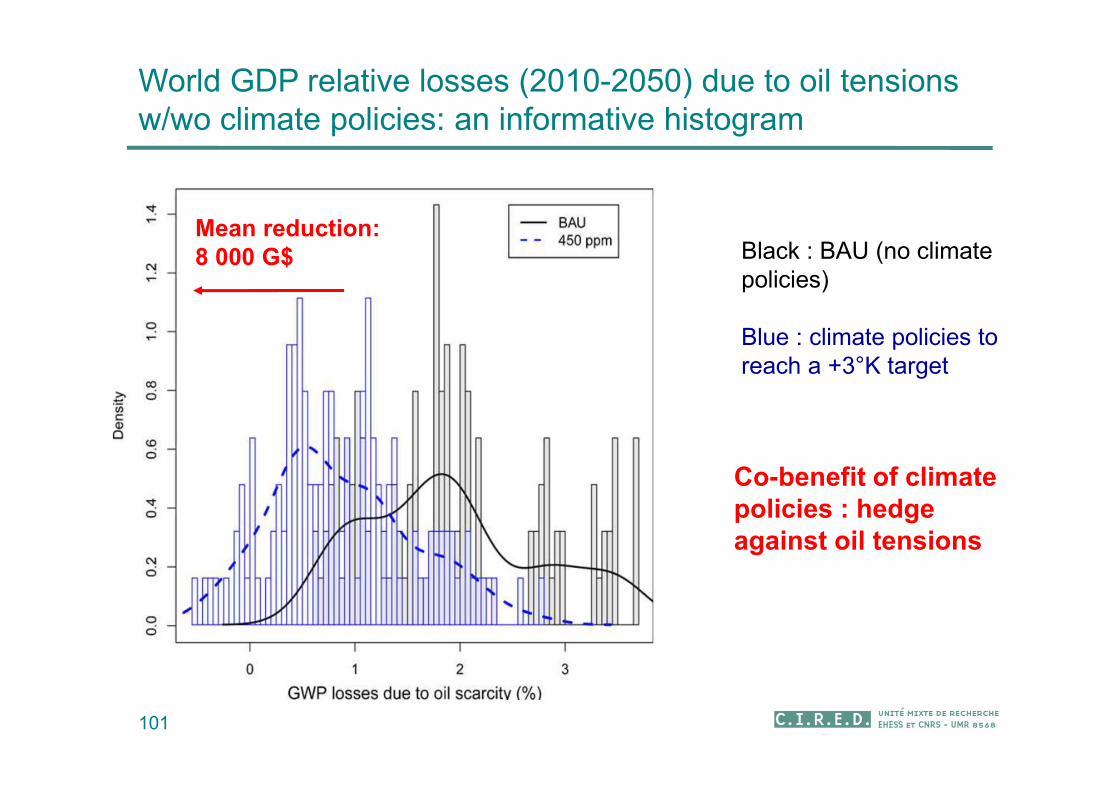

World GDP relative losses (2010-2050) due to oil tensions w/wo climate policies: an informative histogram

101

Black : BAU (no climate policies)

Blue : climate policies to reach a +3°K target

Mean reduction: 8 000 G$

Co-benefit of climate policies : hedge against oil tensions