Embed Size (px)

Citation preview

1CONSO GB 28/06/05 12:48 Page 66

Caisse des Dépôts group 2Consolidated balance sheet and income statement

Central Sector 66Balance sheet and income statement

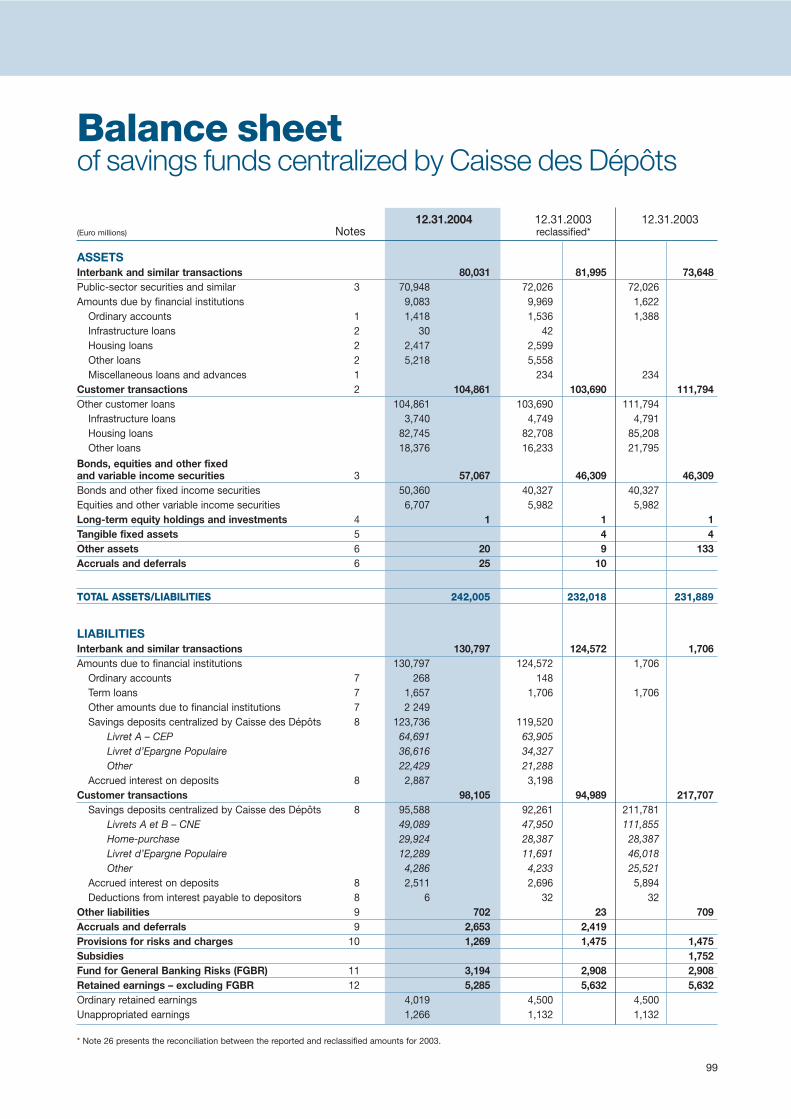

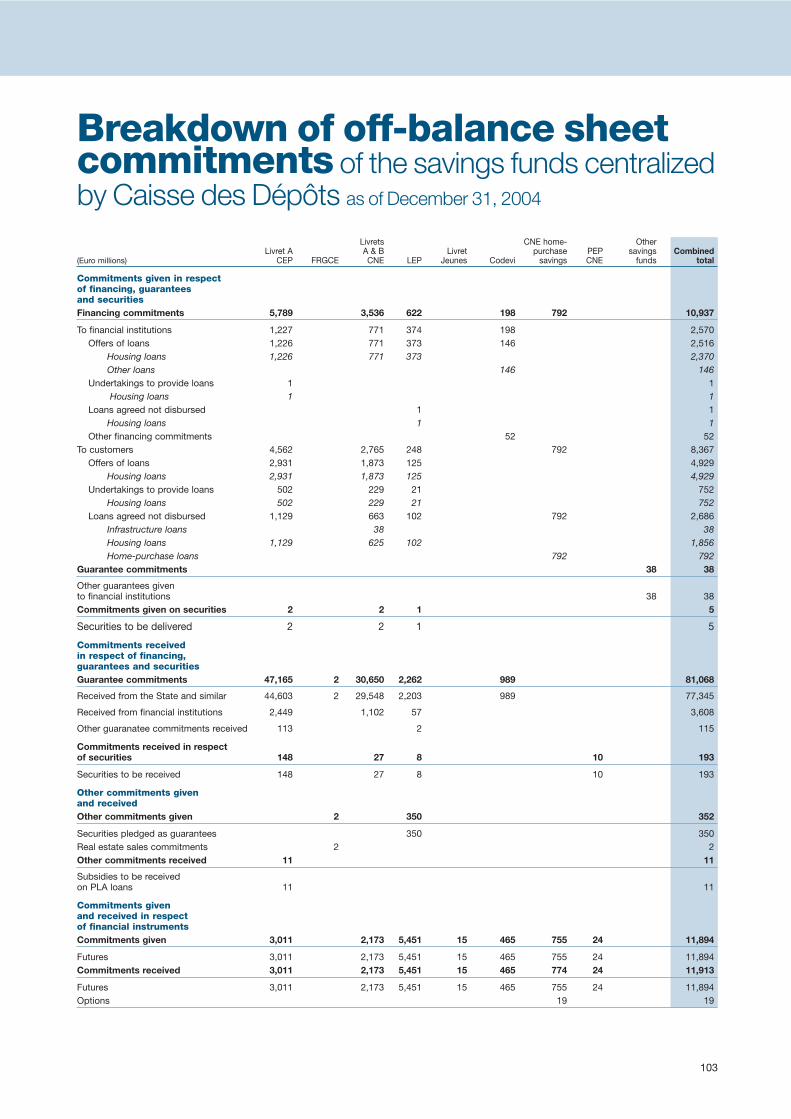

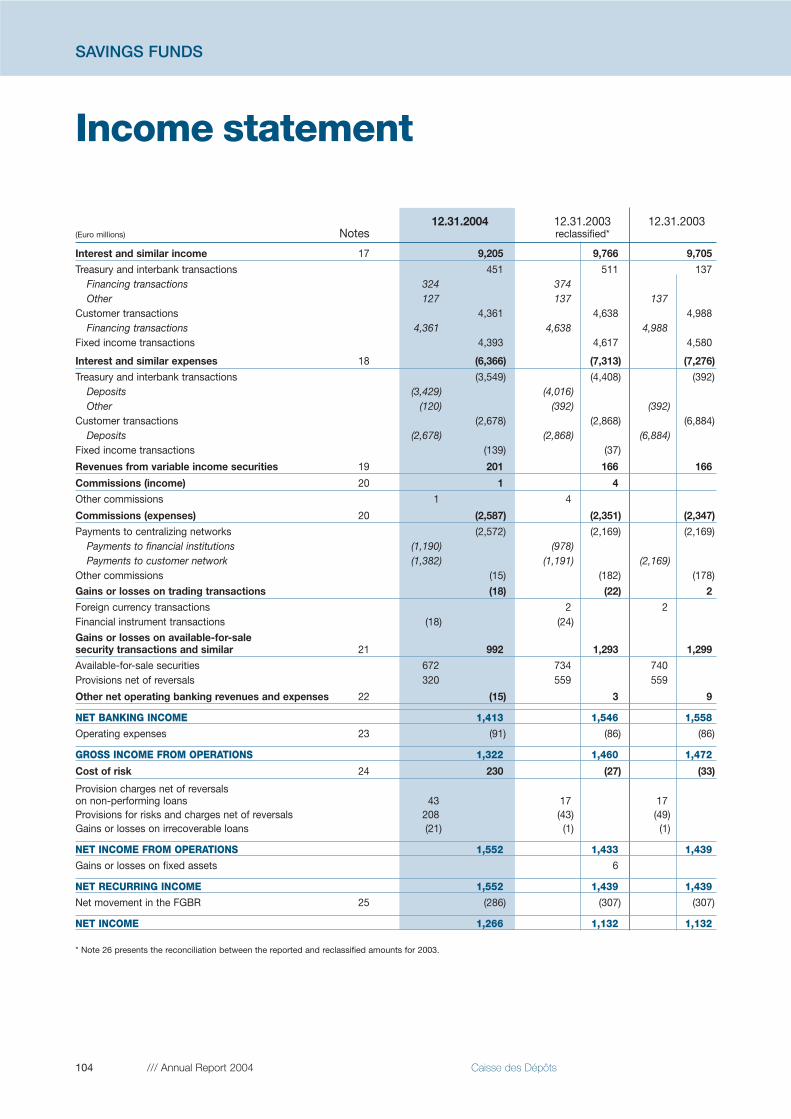

Savings funds centralized by Caisse des Dépôts 98Balance sheet and income statement

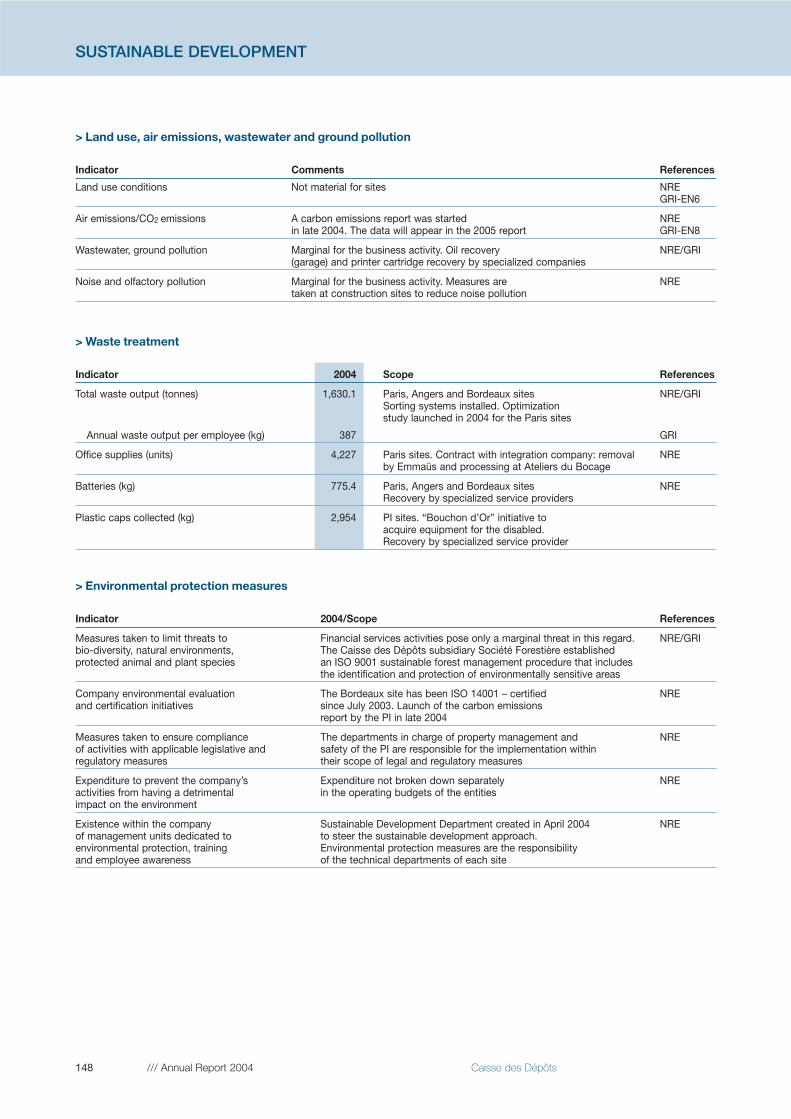

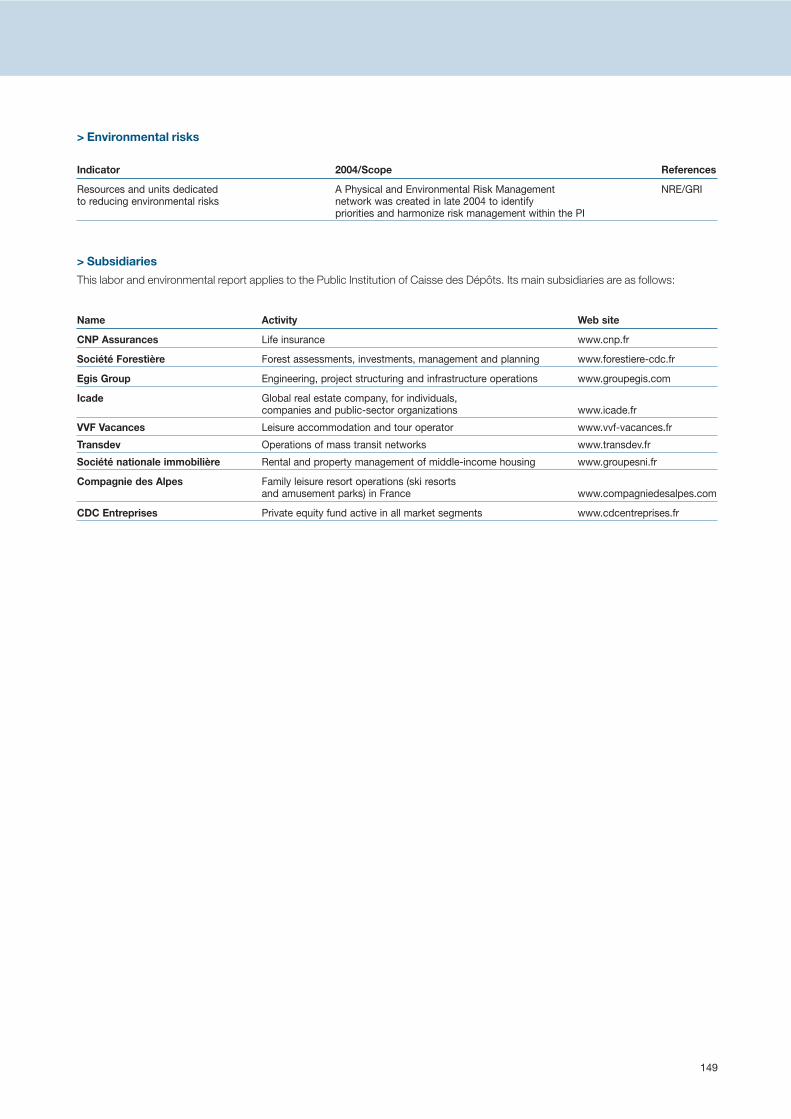

Labor, environmental and sustainabledevelopment information 143

FINANCIALSTATEMENTS 2004

Foreword

The 2004 financial statements include the audited consolidated financial statements of Caisse des Dépôts group, the audited financial statements ofCaisse des Dépôts’ Central Sector, presented in accordance with French banking regulations, and the audited financial statements of the savings fundscentralized by Caisse des Dépôts.

The financial statements of financial subsidiaries and other group units and institutions managed by Caisse des Dépôts are not appended.

2 /// Annual Report 2004 Caisse des Dépôts

CONSOLIDATED FINANCIAL STATEMENTS

Notion of group

The activities of Caisse des Dépôts derive from its original mis-sion as the legal depository for private funds that the French leg-islature wanted to safeguard by ensuring that they weremanaged in a way guaranteeing their protection.

The management of these funds, which are used to financepublic-interest investments and support local development inFrance, also led Caisse des Dépôts to become a major player infinancial markets, which it does today through specialized sub-sidiaries subject to market conditions.

This entity forms a public and decentralized group, carrying outits business in France and internationally, specialized in financialactivities and services governed by public fiduciary obligationsor exercised freely in the competitive sector:

Public-interest missions

• management of passbook savings accounts and financing forpublic housing;

• fiduciary management of major public retirement programsfrom its decentralized offices in Angers and Bordeaux;

• regulated banking and financial activities;

• support for local development, urban policy, job creation andsmall and medium-sized businesses.

Competitive businesses

• finance activities through Caisse Nationale des Caissesd’Epargne, the holding company providing strategic guidancefor the following activities:(1) investment banking activities, with the entities belonging toIxis CIB (capital markets and financing), IAM group (asset man-agement) and IIS (securities services);((2) commercial banking activities, with the entities of CFFgroup, Sanpaolo and the specialized insurance sub-sidiaries (Ecureuil vie, Ecureuil IARD);

• life insurance with CNP Assurances;

• services and engineering for local and regional developmentthrough C3D’s subsidiaries;

• real estate activities, mainly through the SNI and Icade groups;

• private equity organized around CDC Entreprises.

Highlights of the year

2004 was dominated by the Restructuring of the partnership between Caisse des Dépôts and Caisse d’Epargne Group onJune 30. Under the terms of this agreement, Caisse des Dépôtscontributed its ownership interest in its investment bank and assetmanager CDC Ixis to Caisse Nationale des Caisses d’Epargne(CNCE). Through its 35% equity interest in the capital of CNCE,Caisse des Dépôts becomes the strategic shareholder of thenewly created universal bank.

The Restructuring of the partnership with CNCE also resulted inasset transfers to Caisse des Dépôts and its direct subsidiaries.

In particular, it acquired the unlisted private equity assets of CDC Ixis through CDC Entreprises, which enabled the creationof a private equity division offering a comprehensive range ofservices.

In 2004, Caisse des Dépôts became the sole shareholder ofSociété nationale immobilière, thereby strengthening its com-petitive real estate division that also includes the Icade group.

Significant decisions were taken in the areas of the public-interest missions, ensuring their sustained development for theyears ahead. Thus two financing programs were launchedthrough the Savings Funds Division: a €4 billion loan packageaimed at financing major national infrastructure programs and a€2 billion subsidized loan program designed to finance the renovation of an additional 100,000 low-income housing unitsover five years. Urban renewal and local government infrastruc-ture projects were also targeted, with a three-fold increase incommitments made.

Finally, Caisse des Dépôts has reaffirmed its commitment toserving as a long-term strategic investor in French companiesthrough its ownership interests in leading, listed French compa-nies and its support for their development strategies. To thatend, Caisse des Dépôts created an independent AdvisoryCommittee last year. The committee is charged with establish-ing a corporate governance reference framework for the com-panies in which Caisse des Dépôts owns shares. It hasprepared a voting guide for shareholders’ meetings and aCaisse des Dépôts directors’ code.

Presentation of financial statements

For purposes of accounting and financial presentation, Caissedes Dépôts group’s activities are divided according to their two principal missions:

• the fiduciary management of the funds entrusted to Caissedes Dépôts according to the rules defining the nature of theservices provided and the related financial conditions. Thesefunds are managed individually and include, in particular, thesavings funds centralized with Caisse des Dépôts and themanagement of public retirement funds;

• the direct activity performed by the Central Sector – Caisse desDépôts’ financial and administrative entity, managed sepa-rately from the operations under mandate – and by affiliatedgroups, notably C3D, SNI, CNP Assurances and CNCE, inFrance and internationally. This activity alone is considered toconstitute a group for the purpose of preparing consolidatedfinancial statements drawn up in accordance with accountingstandards applicable to financial institutions. The consolidatingentity is the Central Sector and, depending on the level of con-trol, subsidiaries are consolidated under the full or proportionalmethod, or accounted for by the equity method.

This distinction is evidenced by the exclusion of the savingsfunds and retirement funds from the scope of consolidation.Their financial statements are presented separately.

3

Audit of the financial statements

With effect from the 2004 fiscal year, Caisse des Dépôts com-plies with the following provisions of article 30 of the March 1,1984 Law No. 84-148, as amended by article 110 of theDecember 30, 2004 Law No. 2004-1484.

“French governmental public-sector institutions, whether theyare subject to public-sector accounting regulations or not, mustappoint at least two independent auditors and two alternateauditors when they prepare consolidated financial statements in accordance with article 13 of the January 3, 1985 Law No. 85-11 relating to the consolidated financial statements ofcertain commercial and public-sector companies.”

“Each year, Caisse des dépôts et consignations presents itscompany and consolidated financial statements, audited by two independent auditors, to the Finance Committees of theNational Assembly and the Senate. Acting on the recommendationof its Chairman, the Supervisory Board of Caisse des dépôts etconsignations appoints the independent auditors and their alternates.”

4 /// Annual Report 2004 Caisse des Dépôts

CONSOLIDATED FINANCIAL STATEMENTS

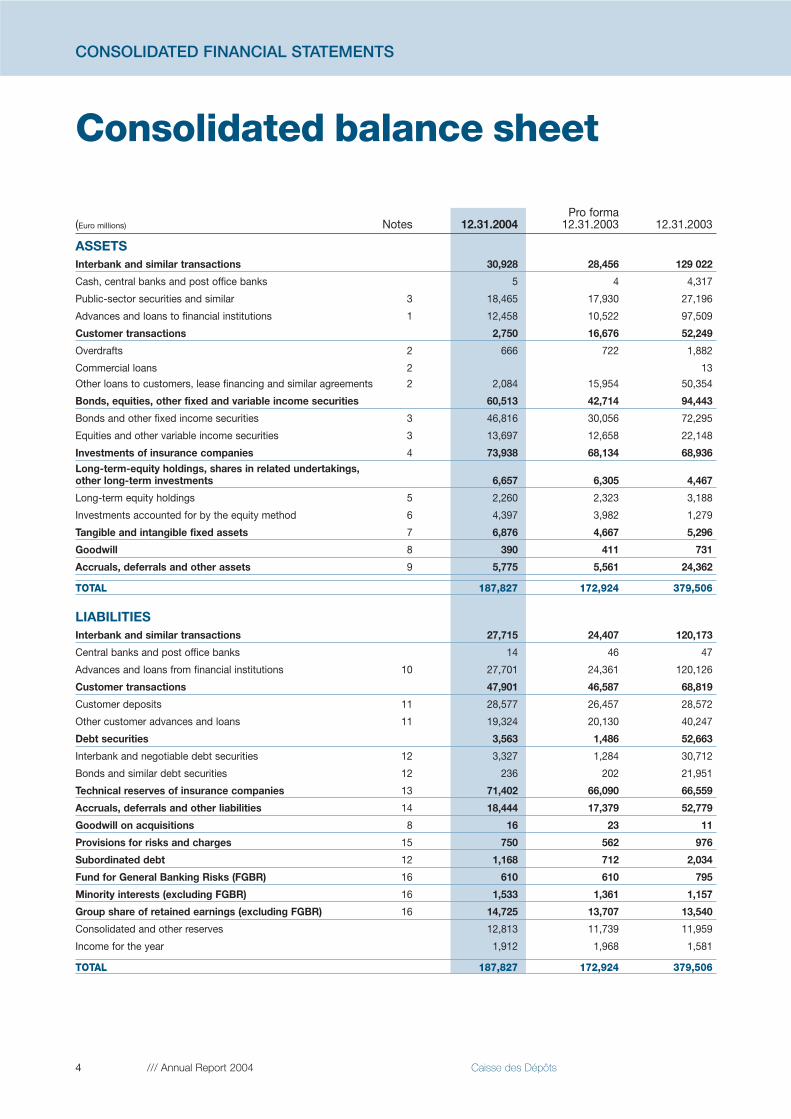

Pro forma (Euro millions) Notes 12.31.2004 12.31.2003 12.31.2003

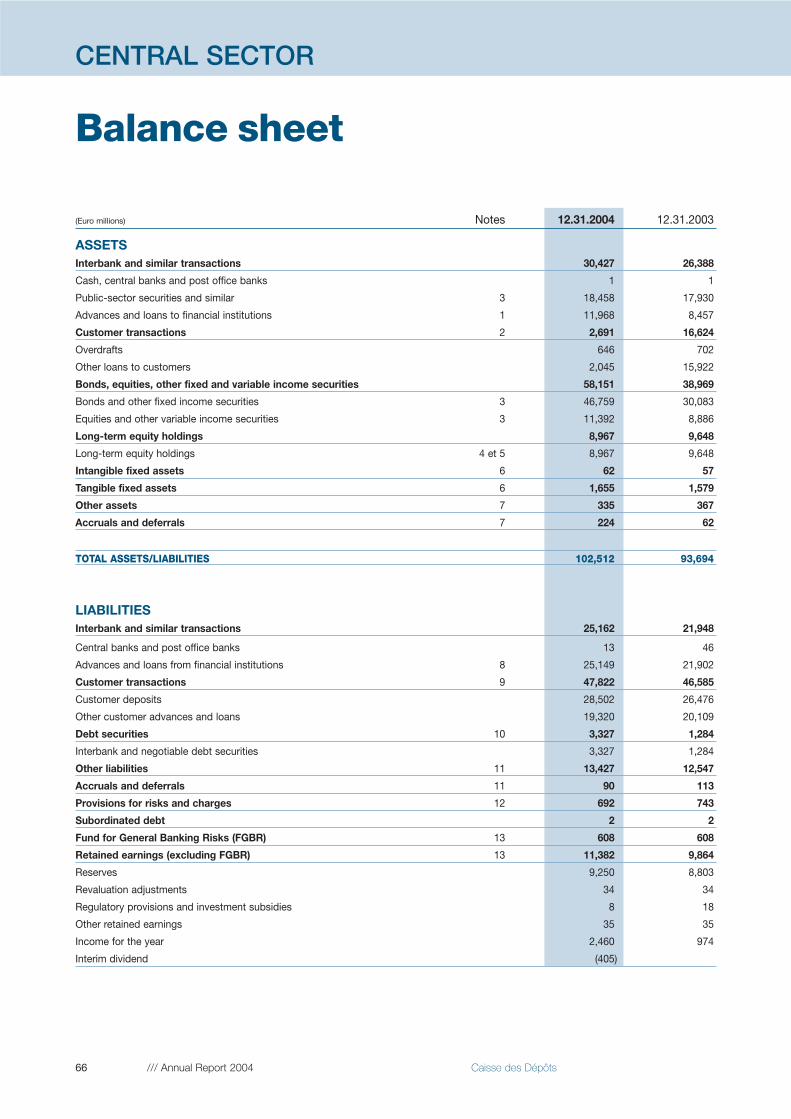

ASSETSInterbank and similar transactions 30,928 28,456 129 022

Cash, central banks and post office banks 5 4 4,317

Public-sector securities and similar 3 18,465 17,930 27,196

Advances and loans to financial institutions 1 12,458 10,522 97,509

Customer transactions 2,750 16,676 52,249

Overdrafts 2 666 722 1,882

Commercial loans 2 13

Other loans to customers, lease financing and similar agreements 2 2,084 15,954 50,354

Bonds, equities, other fixed and variable income securities 60,513 42,714 94,443

Bonds and other fixed income securities 3 46,816 30,056 72,295

Equities and other variable income securities 3 13,697 12,658 22,148

Investments of insurance companies 4 73,938 68,134 68,936Long-term-equity holdings, shares in related undertakings, other long-term investments 6,657 6,305 4,467

Long-term equity holdings 5 2,260 2,323 3,188

Investments accounted for by the equity method 6 4,397 3,982 1,279

Tangible and intangible fixed assets 7 6,876 4,667 5,296

Goodwill 8 390 411 731

Accruals, deferrals and other assets 9 5,775 5,561 24,362

TOTAL 187,827 172,924 379,506

LIABILITIESInterbank and similar transactions 27,715 24,407 120,173

Central banks and post office banks 14 46 47

Advances and loans from financial institutions 10 27,701 24,361 120,126

Customer transactions 47,901 46,587 68,819

Customer deposits 11 28,577 26,457 28,572

Other customer advances and loans 11 19,324 20,130 40,247

Debt securities 3,563 1,486 52,663

Interbank and negotiable debt securities 12 3,327 1,284 30,712

Bonds and similar debt securities 12 236 202 21,951

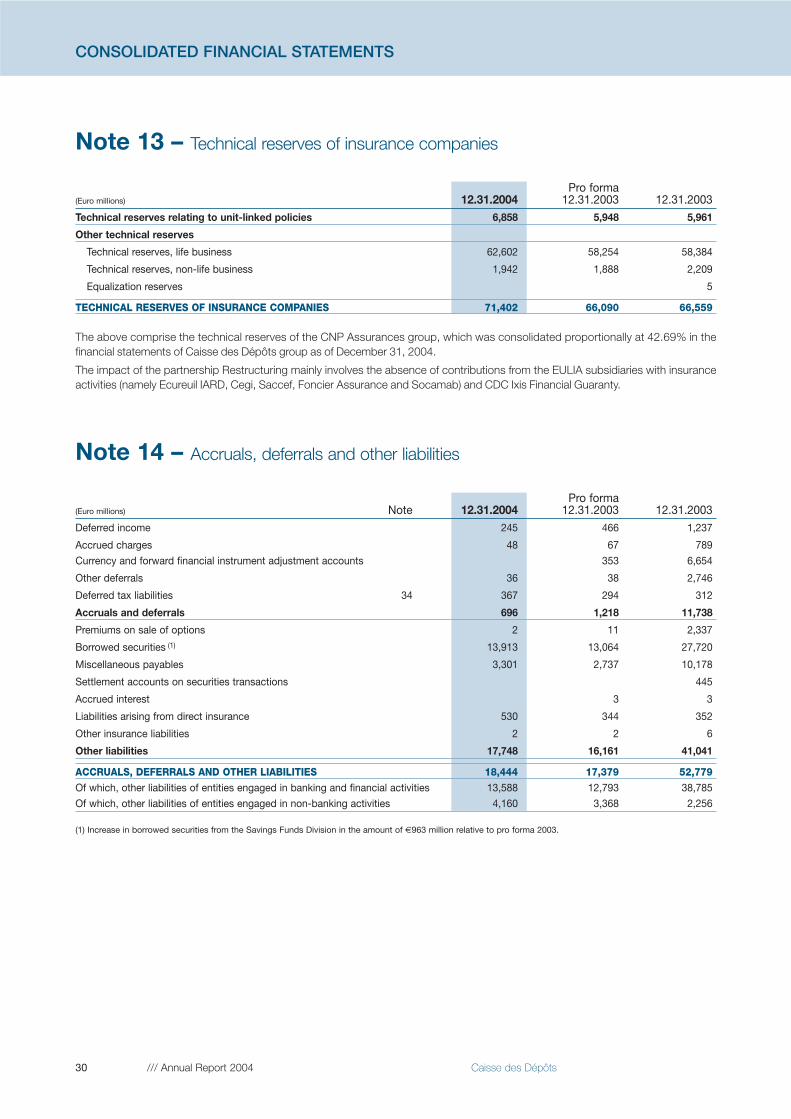

Technical reserves of insurance companies 13 71,402 66,090 66,559

Accruals, deferrals and other liabilities 14 18,444 17,379 52,779

Goodwill on acquisitions 8 16 23 11

Provisions for risks and charges 15 750 562 976

Subordinated debt 12 1,168 712 2,034

Fund for General Banking Risks (FGBR) 16 610 610 795

Minority interests (excluding FGBR) 16 1,533 1,361 1,157

Group share of retained earnings (excluding FGBR) 16 14,725 13,707 13,540

Consolidated and other reserves 12,813 11,739 11,959

Income for the year 1,912 1,968 1,581

TOTAL 187,827 172,924 379,506

Consolidated balance sheet

5

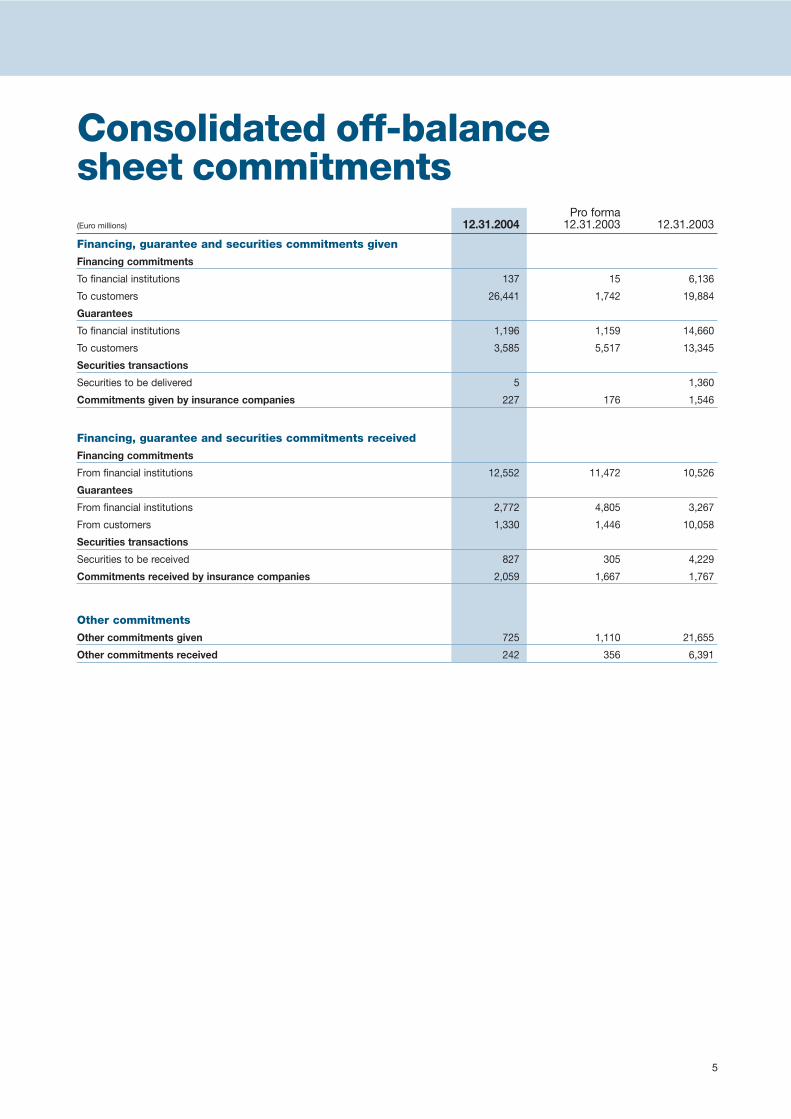

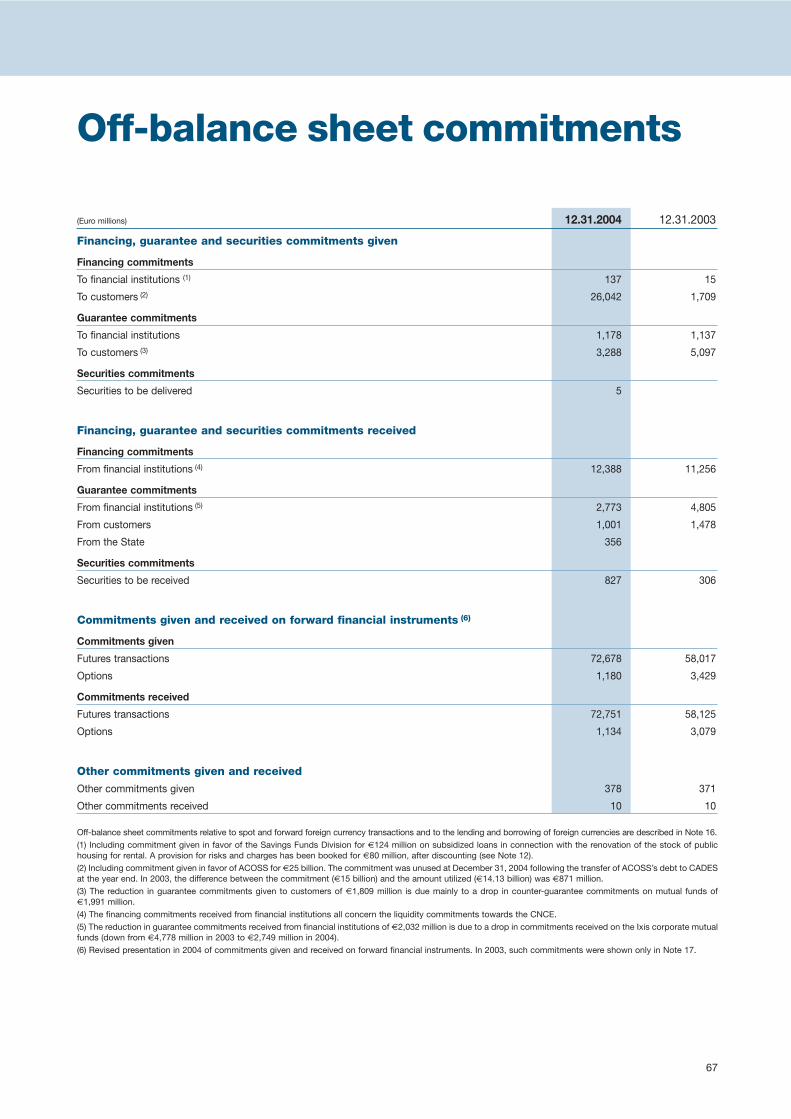

Consolidated off-balancesheet commitments

Pro forma (Euro millions) 12.31.2004 12.31.2003 12.31.2003

Financing, guarantee and securities commitments given

Financing commitments

To financial institutions 137 15 6,136

To customers 26,441 1,742 19,884

Guarantees

To financial institutions 1,196 1,159 14,660

To customers 3,585 5,517 13,345

Securities transactions

Securities to be delivered 5 1,360

Commitments given by insurance companies 227 176 1,546

Financing, guarantee and securities commitments received

Financing commitments

From financial institutions 12,552 11,472 10,526

Guarantees

From financial institutions 2,772 4,805 3,267

From customers 1,330 1,446 10,058

Securities transactions

Securities to be received 827 305 4,229

Commitments received by insurance companies 2,059 1,667 1,767

Other commitments

Other commitments given 725 1,110 21,655

Other commitments received 242 356 6,391

6 /// Annual Report 2004 Caisse des Dépôts

CONSOLIDATED FINANCIAL STATEMENTS

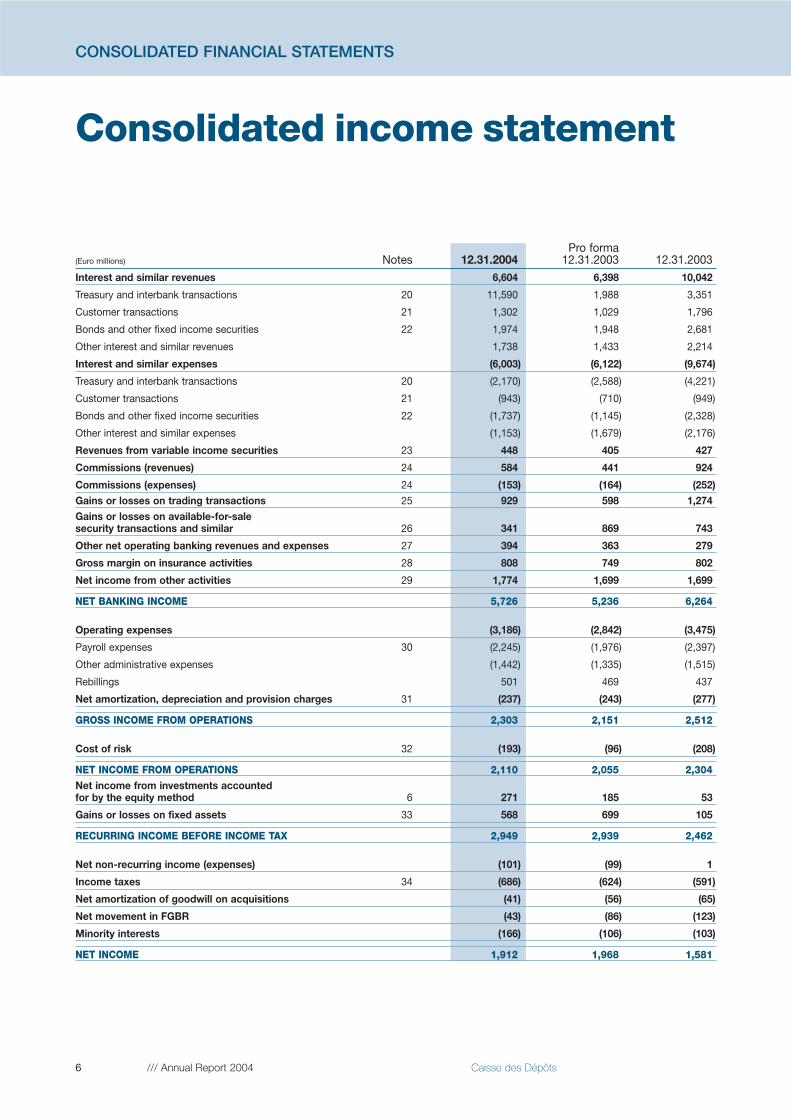

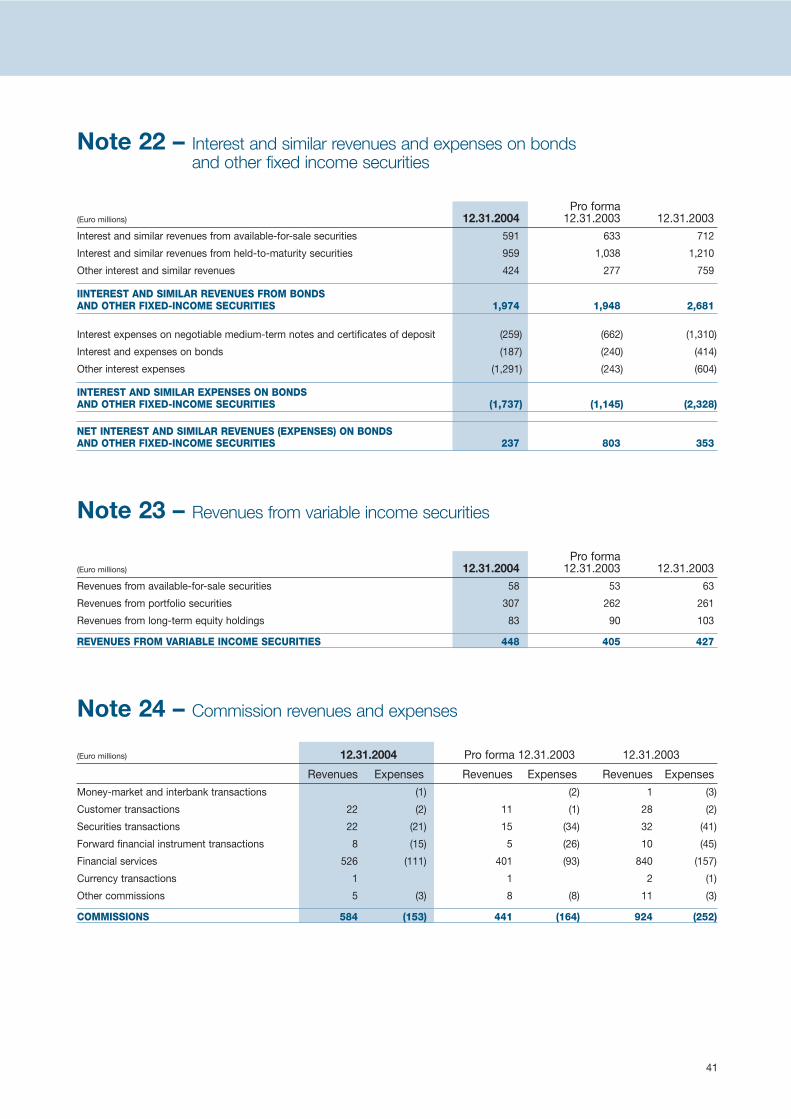

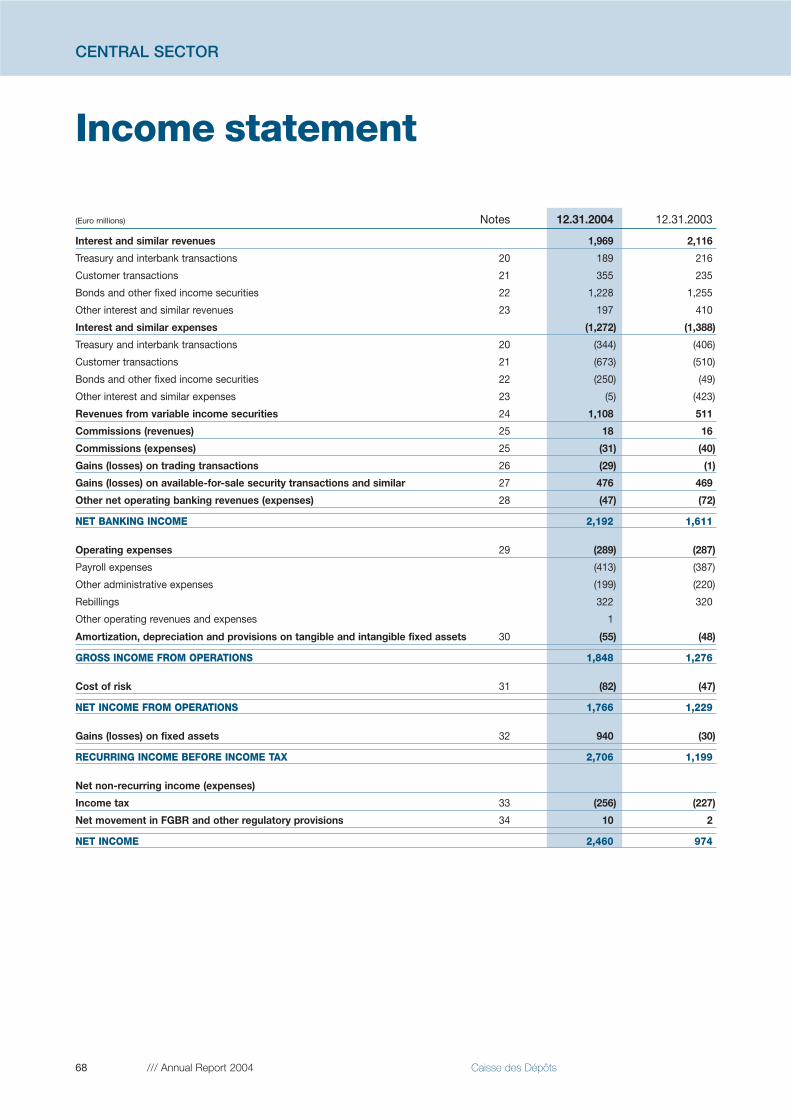

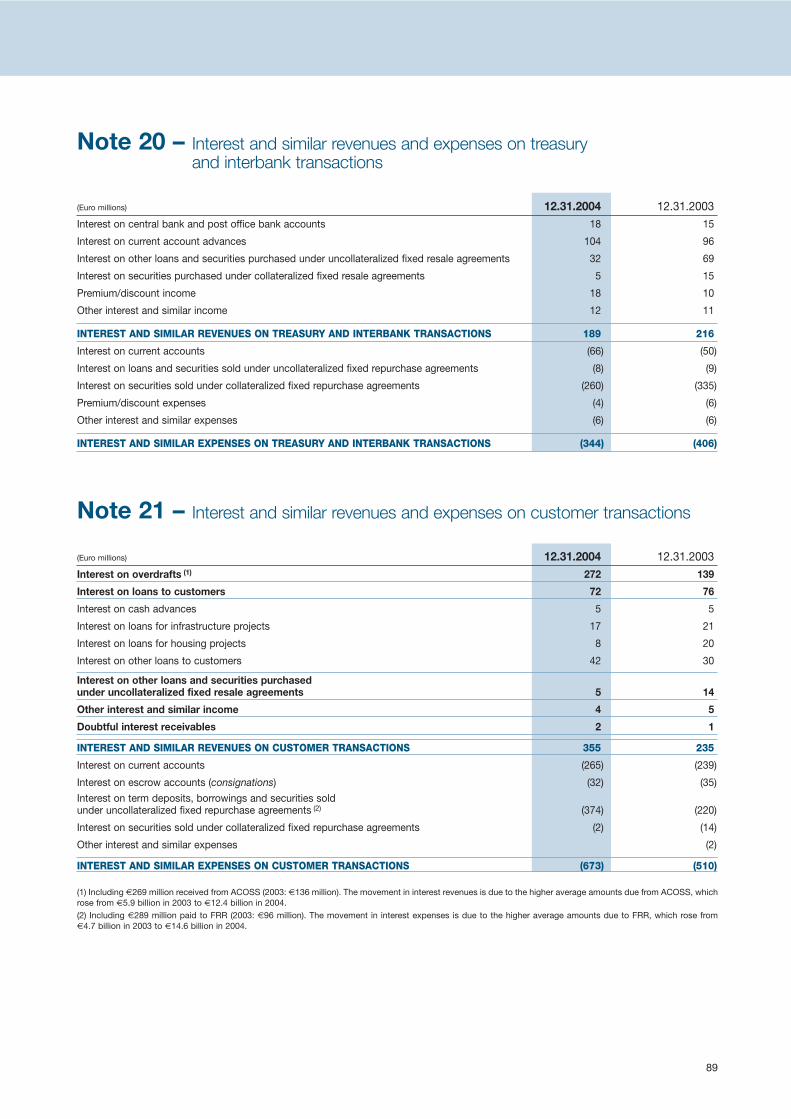

Pro forma (Euro millions) Notes 12.31.2004 12.31.2003 12.31.2003Interest and similar revenues 6,604 6,398 10,042

Treasury and interbank transactions 20 11,590 1,988 3,351

Customer transactions 21 1,302 1,029 1,796

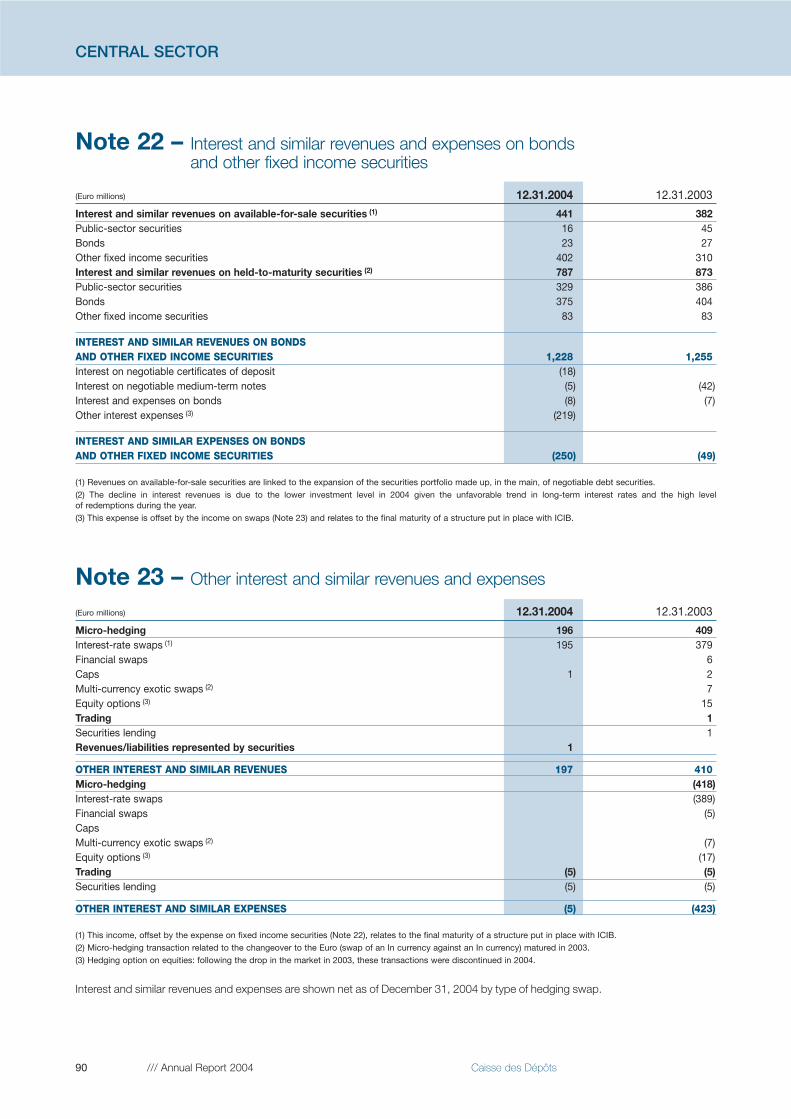

Bonds and other fixed income securities 22 1,974 1,948 2,681

Other interest and similar revenues 1,738 1,433 2,214

Interest and similar expenses (6,003) (6,122) (9,674)

Treasury and interbank transactions 20 (2,170) (2,588) (4,221)

Customer transactions 21 (943) (710) (949)

Bonds and other fixed income securities 22 (1,737) (1,145) (2,328)

Other interest and similar expenses (1,153) (1,679) (2,176)

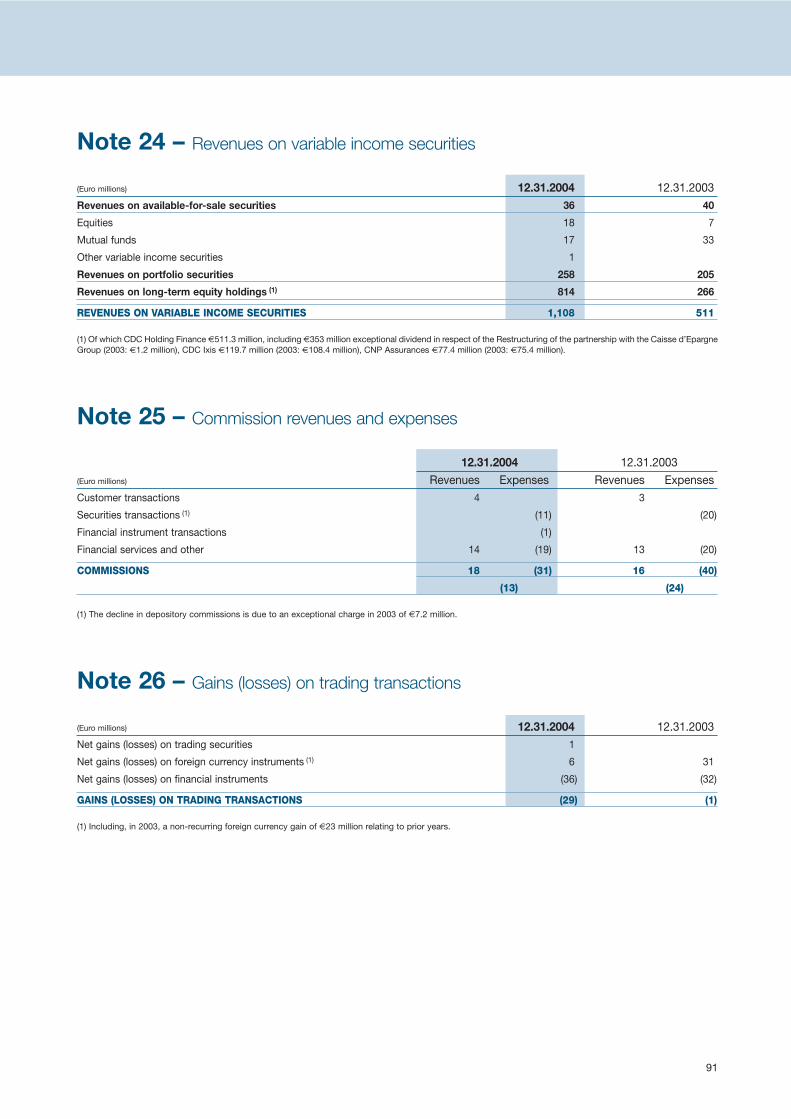

Revenues from variable income securities 23 448 405 427

Commissions (revenues) 24 584 441 924

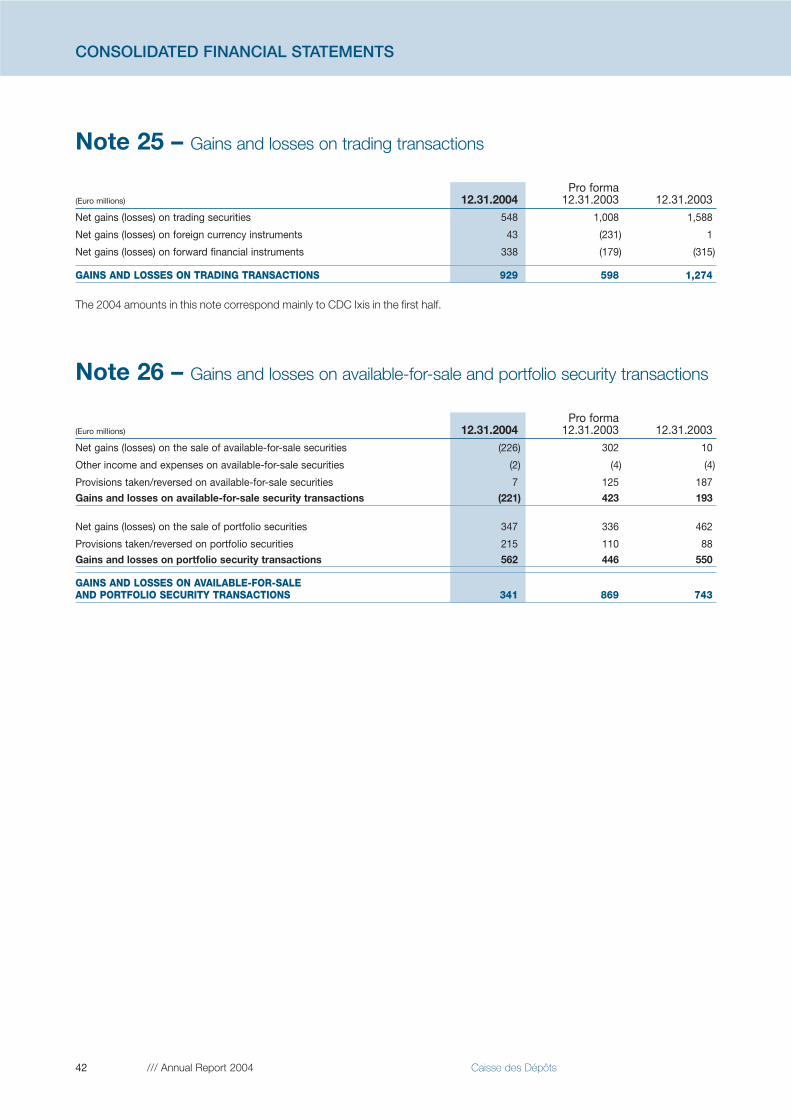

Commissions (expenses) 24 (153) (164) (252)Gains or losses on trading transactions 25 929 598 1,274Gains or losses on available-for-sale security transactions and similar 26 341 869 743

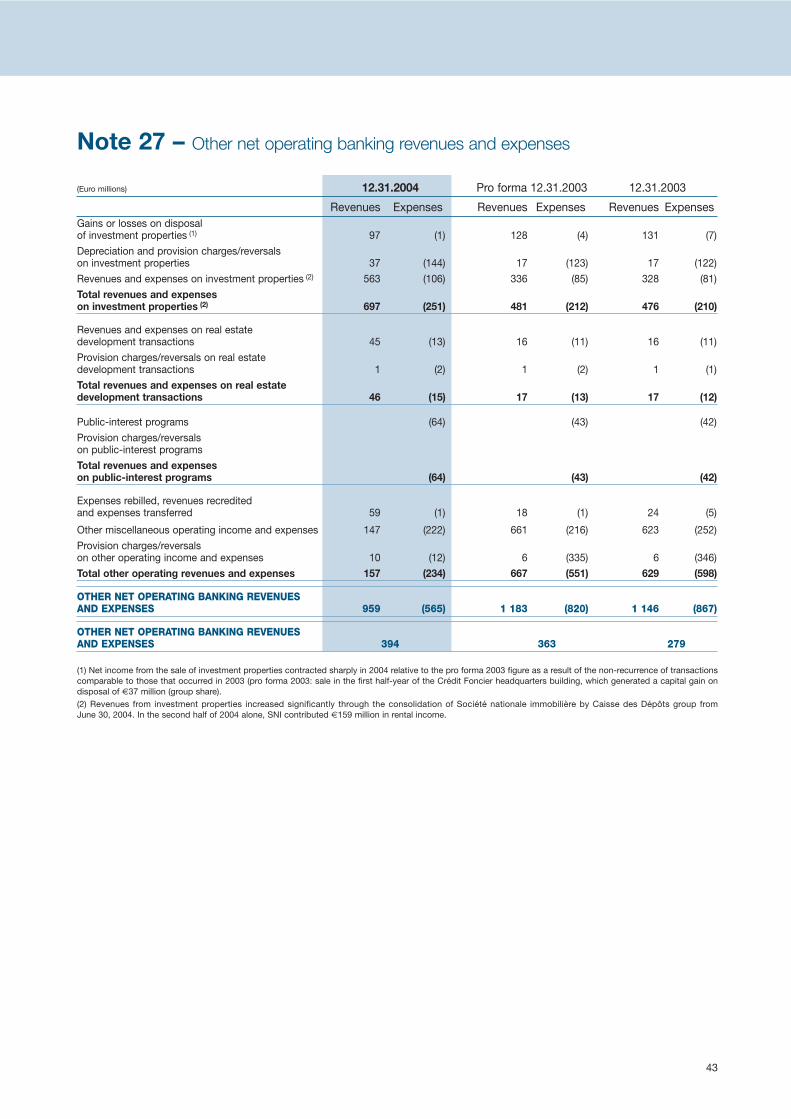

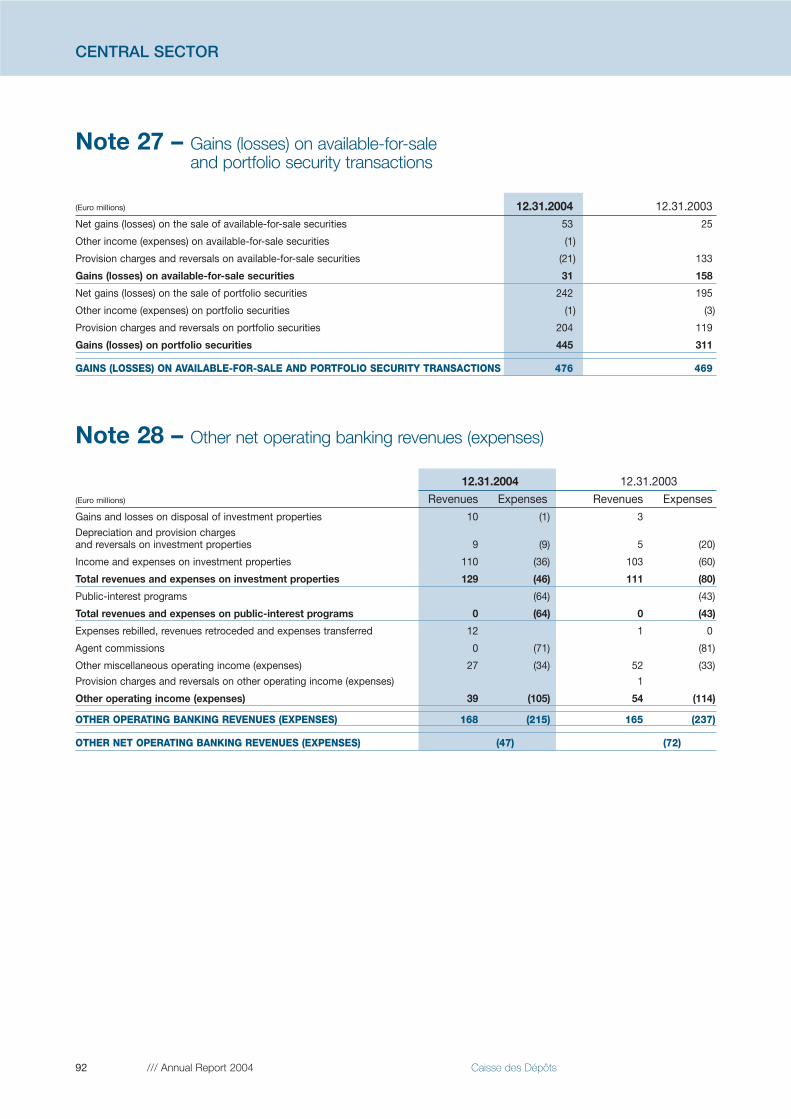

Other net operating banking revenues and expenses 27 394 363 279

Gross margin on insurance activities 28 808 749 802

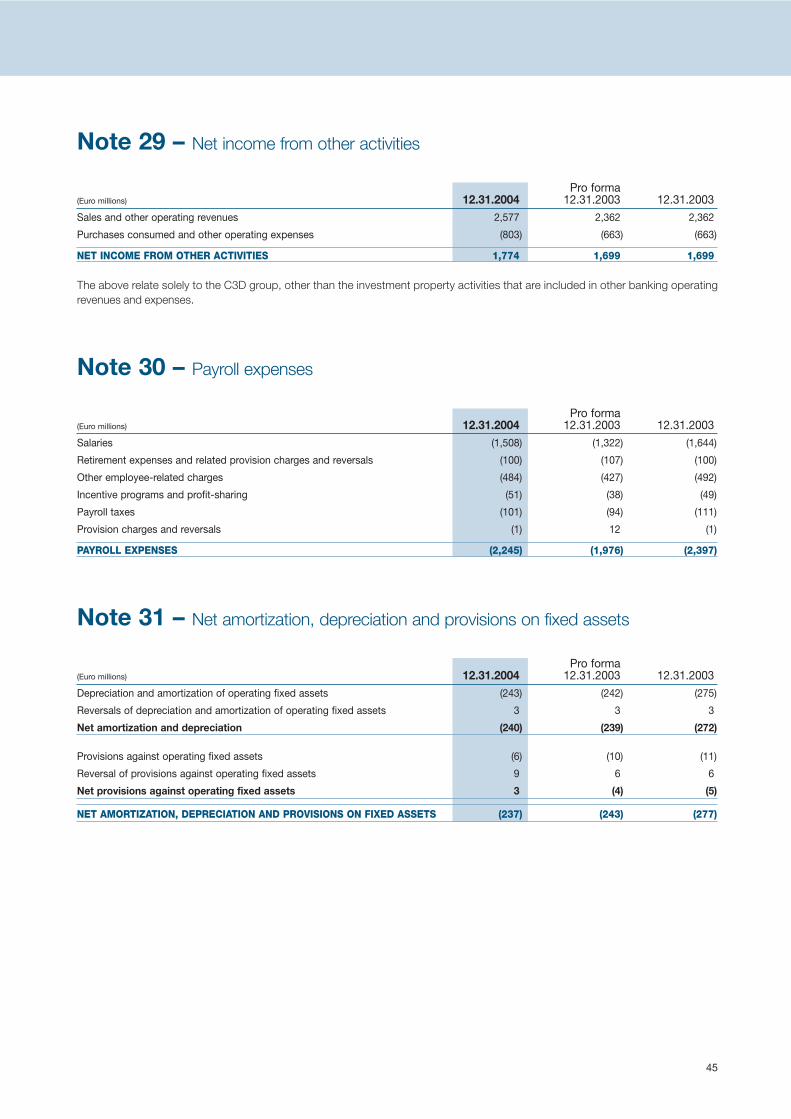

Net income from other activities 29 1,774 1,699 1,699

NET BANKING INCOME 5,726 5,236 6,264

Operating expenses (3,186) (2,842) (3,475)

Payroll expenses 30 (2,245) (1,976) (2,397)

Other administrative expenses (1,442) (1,335) (1,515)

Rebillings 501 469 437

Net amortization, depreciation and provision charges 31 (237) (243) (277)

GROSS INCOME FROM OPERATIONS 2,303 2,151 2,512

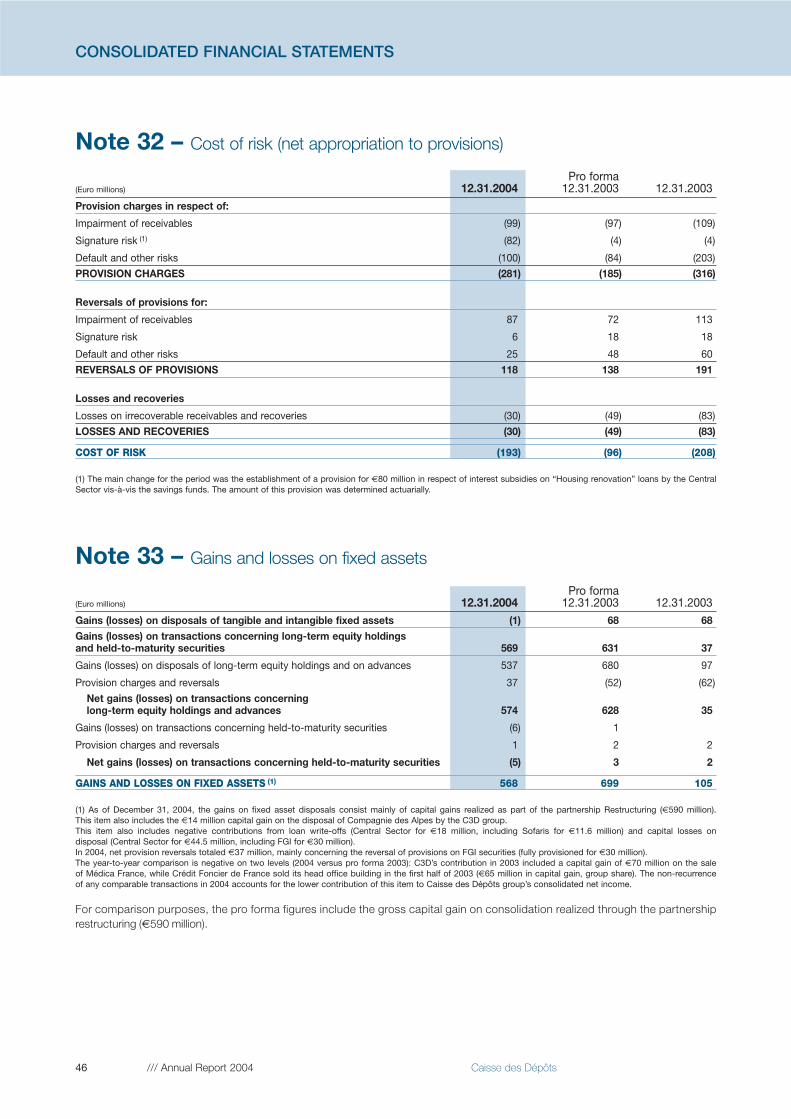

Cost of risk 32 (193) (96) (208)

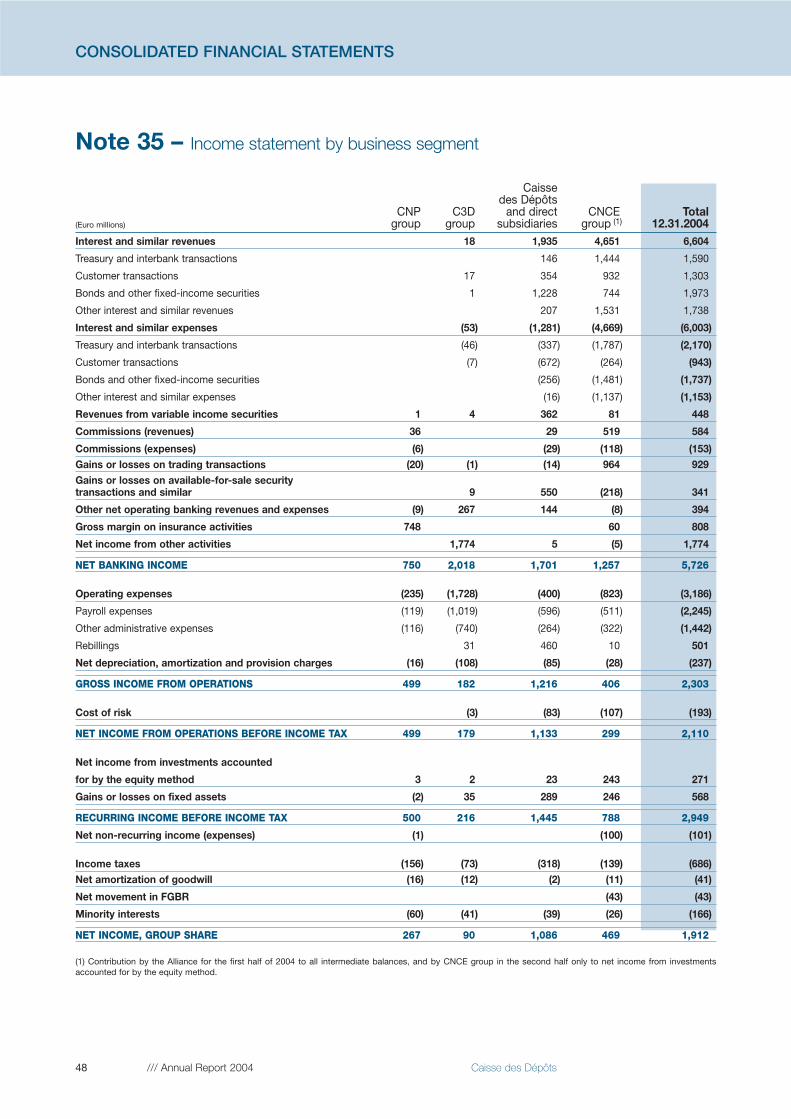

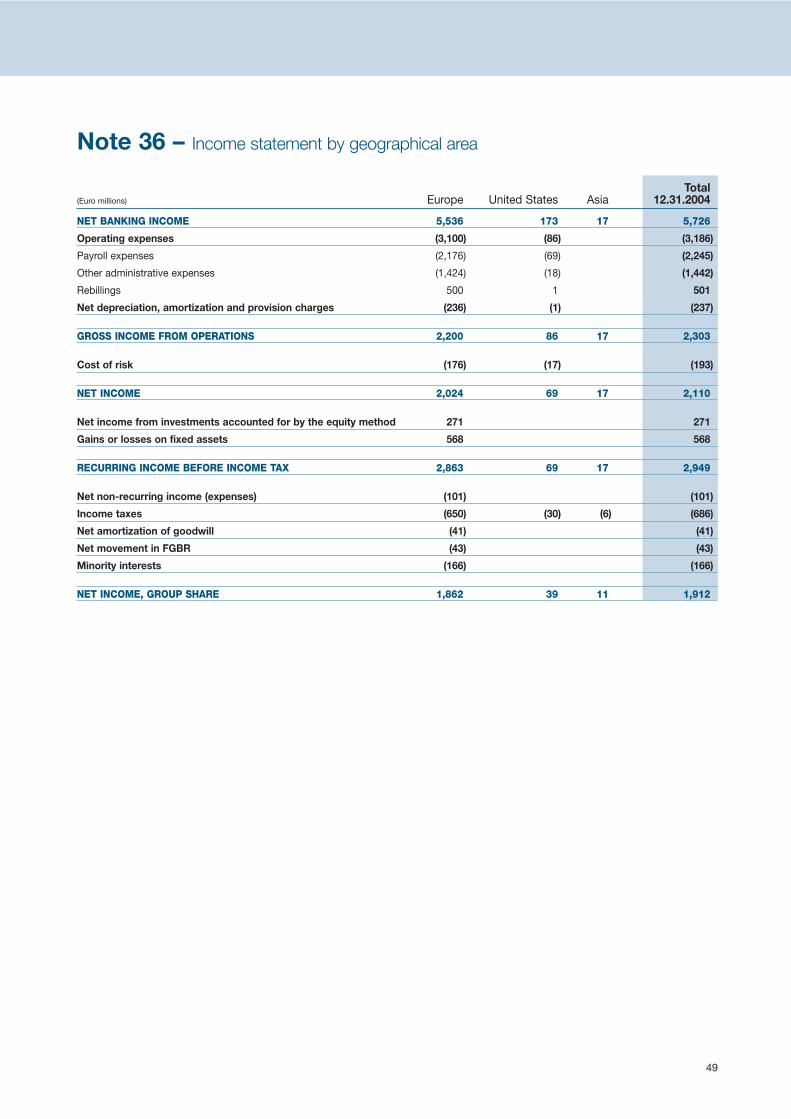

NET INCOME FROM OPERATIONS 2,110 2,055 2,304Net income from investments accountedfor by the equity method 6 271 185 53

Gains or losses on fixed assets 33 568 699 105

RECURRING INCOME BEFORE INCOME TAX 2,949 2,939 2,462

Net non-recurring income (expenses) (101) (99) 1

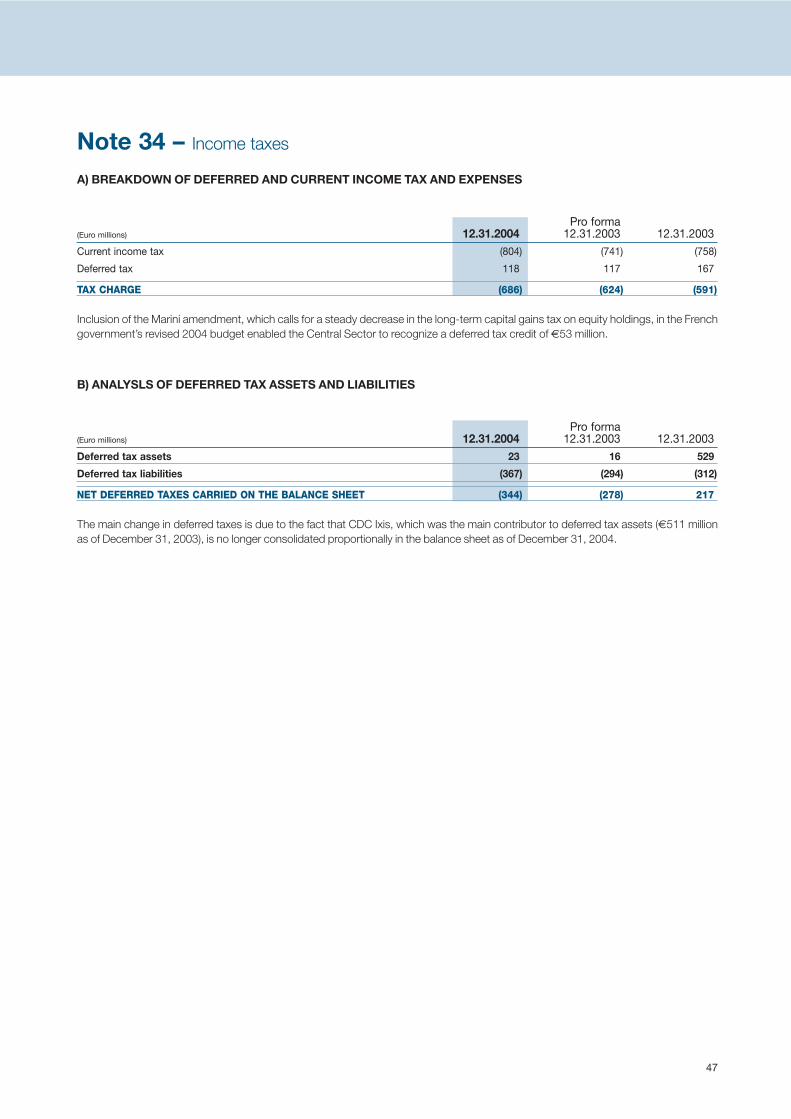

Income taxes 34 (686) (624) (591)

Net amortization of goodwill on acquisitions (41) (56) (65)

Net movement in FGBR (43) (86) (123)

Minority interests (166) (106) (103)

NET INCOME 1,912 1,968 1,581

Consolidated income statement

7

Highlights

1 – Caisse des Dépôts and Caisse d’Epargne Group signpartnership restructuring agreement

In accordance with their October 1, 2003 memorandum ofagreement, Caisse des Dépôts and Caisse d’Epargne Groupsignificantly restructured their partnership on a new and sustain-able basis. Under the agreement signed May 27, 2004, Caissedes Dépôts contributed its 50.1% equity interest in EULIA and its43.55% stake in its investment banking and asset managementsubsidiary CDC Ixis to CNCE. These contributions make Caissed’Epargne Group a universal bank, with Caisse des Dépôts as itsstrategic partner through a 35% equity interest (corresponding toa 40.214% effective financial interest) in CNCE, alongside theCaisses d’Epargne. The arrangement includes a shareholders’agreement securing the partnership between the two groups,which pledge to maintain their relative ownership interests inCNCE constant until any potential initial public offering. Theagreement clarifies their respective roles within the new entity:

• CNCE, which is 65%-owned by the Caisses d’Epargne and35% by Caisse des Dépôts, is responsible for steering the retailbanking businesses and the investment banking interests heldmainly by CDC Ixis;

• Caisse des Dépôts has strengthened its roles as a strategicshareholder of CNCE and as a long-term investor by takingdirect control of CDC Ixis’s proprietary portfolios (listed shares,private equity, real estate assets), valued at a total of €3.4 billion.

The transaction’s financial structuring resulted in a €3.3 billionprivate placement by the 29 regional savings banks (Caissesd’Epargne) in mainland France of cooperative investment certifi-cates, corresponding to non-voting preferred shares, withCNCE. Following the issue of these certificates, CNCE held a20% stake in the regional savings banks. Thus CNCE, directly,and Caisse des Dépôts, through its ownership interest in CNCE,have an interest in the business of the regional savings banks,which currently account for more than 65% of the earnings ofthe Caisse d’Epargne Group.

The partnership restructuring transactions resulted in a €405 million net capital gain, which was paid to the FrenchState during the second half of the year as an interim dividend.

During the first half of 2004, under the terms of the partnershiprestructuring, Caisse des Dépôts acquired from CDC Ixis itslisted equities portfolio for €2.1 billion and its 49% equity inter-est in Sogeposte.

In the second half of 2004, Caisse des Dépôts — through itssubsidiary CDC Entreprises, whose capital was increased by€800 million — finalized the acquisition of the private equityassets and a 65% controlling interest in CDC Entreprises CapitalInvestissement (formerly CDC Ixis Private Equity), with the bal-ance being held by CNCE. Caisse des Dépôts also acquiredfrom CDC Ixis its ownership interests in the real estate compa-nies Foncière des Pimonts (sold on to Icade at the year end),Logistis and AIH BV.

2 – Acquisition of Société nationale immobilière

In the first half of 2004, Caisse des Dépôts purchased from theFrench State an additional 74% interest in Société nationaleimmobilière (SNI), thereby bringing its total ownership interest to99.97%. SNI manages real estate assets held for its ownaccount and for third parties.

This €519 million investment is the subject of an earn-outclause, under which Caisse des Dépôts could pay a maximumadditional amount of €58.8 million based on indicators for theperiod from 2004 to 2007. At end-2004, the additional purchaseprice to be paid totaled €7.4 million.

The SNI group was consolidated into Caisse des Dépôts effective June 30, 2004.

3 – Taxation

Caisse des Dépôts has recognized the impact of the Mariniamendment to the revised 2004 budget, which calls for graduallyreducing the capital gains tax on long-term equity holdings.

Information on income taxes is provided in Note 34.

Accounting principles used in preparing the consolidatedfinancial statements of Caisse des Dépôts group

The consolidated financial statements have been prepared inaccordance with the provisions of CRC (the French AccountingRegulations Committee) Standard 99-07 regarding the consoli-dation rules applicable to companies subject to CRBF regula-tions (the French Banking and Financial Regulations Committee).

The presentation of the financial statements complies with theprovisions of CRC Standard 2000-04 regarding the consolidationrules applicable to companies subject to CRBF regulations.

Notes to the consolidated financial statements

8 /// Annual Report 2004 Caisse des Dépôts

CONSOLIDATED FINANCIAL STATEMENTS

Principal policies for accounting and presentation of the consolidated financialstatements

Comparability of the financial statements

The partnership Restructuring transactions changed signifi-cantly the consolidation scope as of June 30, 2004. The mainimpact concerned EULIA: CDC Ixis is now consolidated usingthe equity method via the holding in CNCE, whereas previouslyit was consolidated proportionally.

These changes warrant the presentation of pro forma financialstatements for 2003, incorporating the changes in consolidationscope and methods necessitated by the partnership Restructuring.

The principal adjustments between the historical and pro forma2003 financial statements are shown in Note 37.

As a result of this revised presentation, the 2004 consolidatedincome statement has been analyzed by comparison to the proforma 2003 income statement. Balance sheet movements,however, are based on historical published data.

Consolidation principles and policies

1 – Consolidation methods and scope

The consolidated financial statements include the accounts of theCentral Sector of Caisse des Dépôts, the consolidated accountsof the sub-groups and the accounts of subsidiaries, whenevertheir consolidation is material to the consolidated accounts of theentities included in the scope of the consolidation.

Those companies whose contribution to the results of the sub-group to which they belong is considered material, and newlyformed or acquired companies for which strong growth isexpected, are also consolidated.

Full consolidationUndertakings over which the group exercises exclusive controlare fully consolidated.

Exclusive control is defined as the ability of an undertaking todirect the financial and operational policies of another undertak-ing with a view to gaining economic benefits from its activities.

It results from the ownership of more than one half of the votingrights of an undertaking, or from the appointment for two suc-cessive years of more than one half of the members of the Boardof Directors or equivalent, or from the power to exert a dominantinfluence by virtue of company by-laws or agreements.

Proportional consolidationCompanies over which the group exercises joint control are proportionally consolidated.

Joint control is defined as sharing of the control of an undertak-ing jointly run by a limited number of partners or shareholders,such that the financial and operating policies result from theiragreement.

Equity methodUndertakings over which significant influence is exerted areaccounted for under the equity method. Significant influenceresults from the ability to take part in determining the financialand operational policies of an undertaking without exercisingcontrol.

Special purpose entitiesWhen the group or a group company controls an undertaking insubstance, notably by virtue of contractual agreements or provi-sions in company bylaws, the undertaking is consolidated even ifthere is no ownership of shares. The existence of control in sub-stance is assessed using the following criteria, as defined by CRCStandard 99-07: decision-making and management powers inrespect of the daily operations of a special purpose entity or inrespect of its assets; and the ability to obtain the majority or all ofthe economic benefits and exposure to a majority of the risks.

Entities that carry out their activities under a fiduciary relation-ship, where management is carried out on behalf of third partiesand in the interest of the various parties involved, are not consolidated.

The following types of companies are not consolidated: semi-public companies (SEMs and SAIEMs) and public housingcorporations (HLMs), for which access to their assets andprofits is restricted. As regards insurance activities, controlledpooled investment vehicles and transparent companies withproperty rental activities representing policyholder liabilitiesare not consolidated.

The accounts of consolidated entities are generally prepared asof December 31. Companies preparing their accounts morethan three months before or after this date are consolidatedusing accounts drawn up as of December 31.

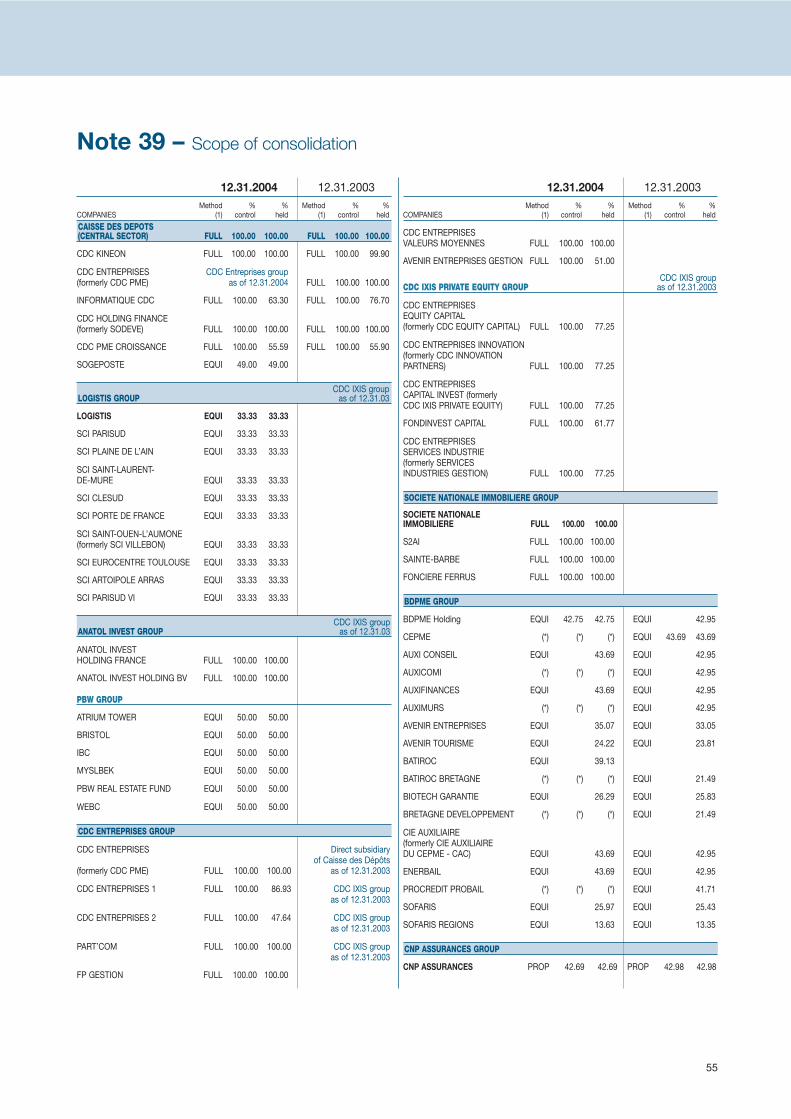

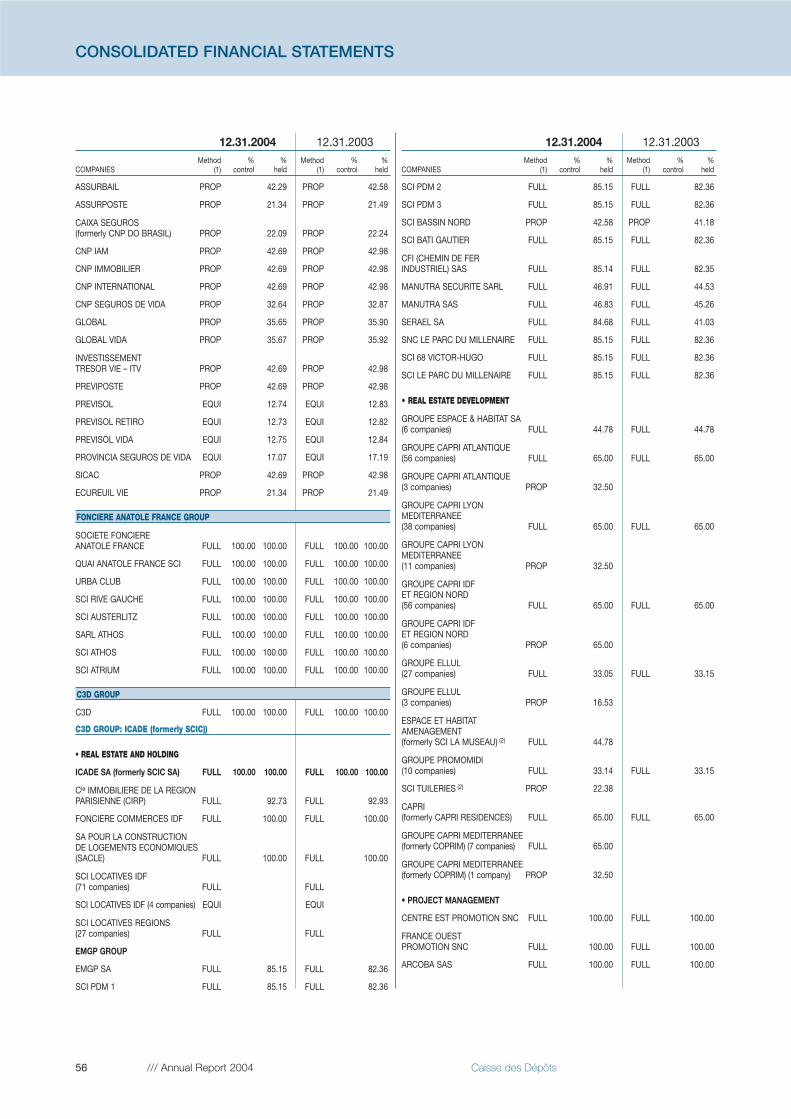

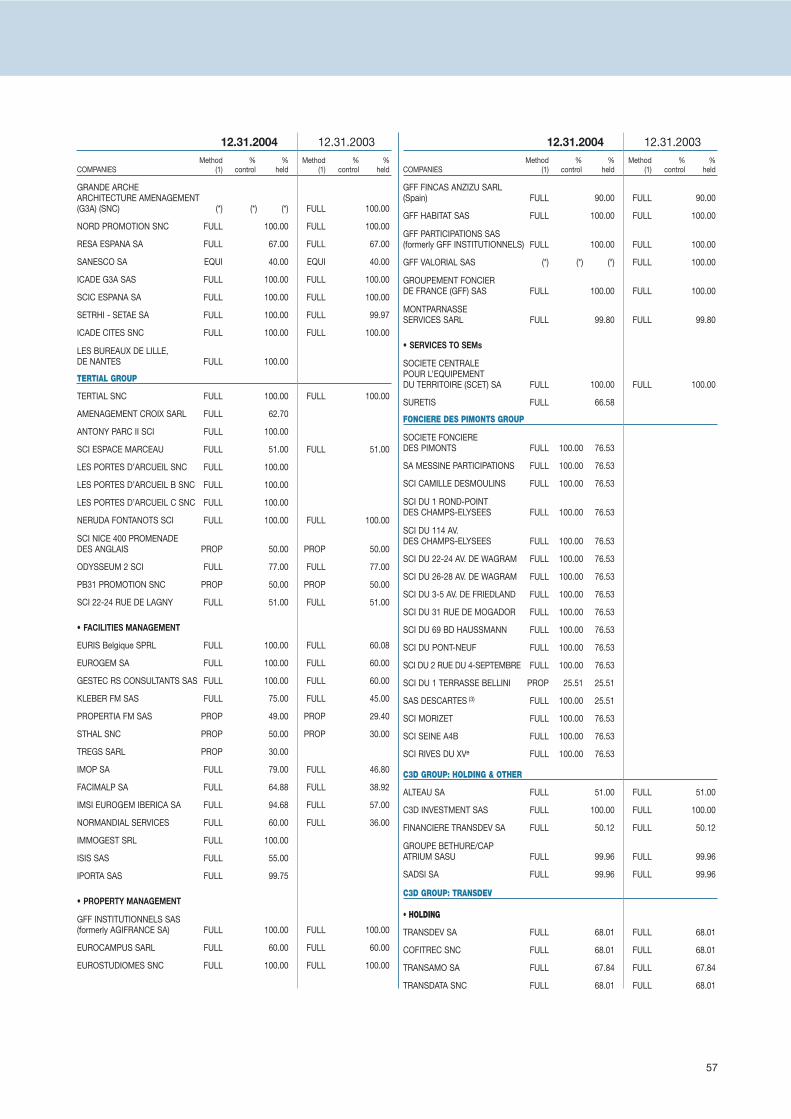

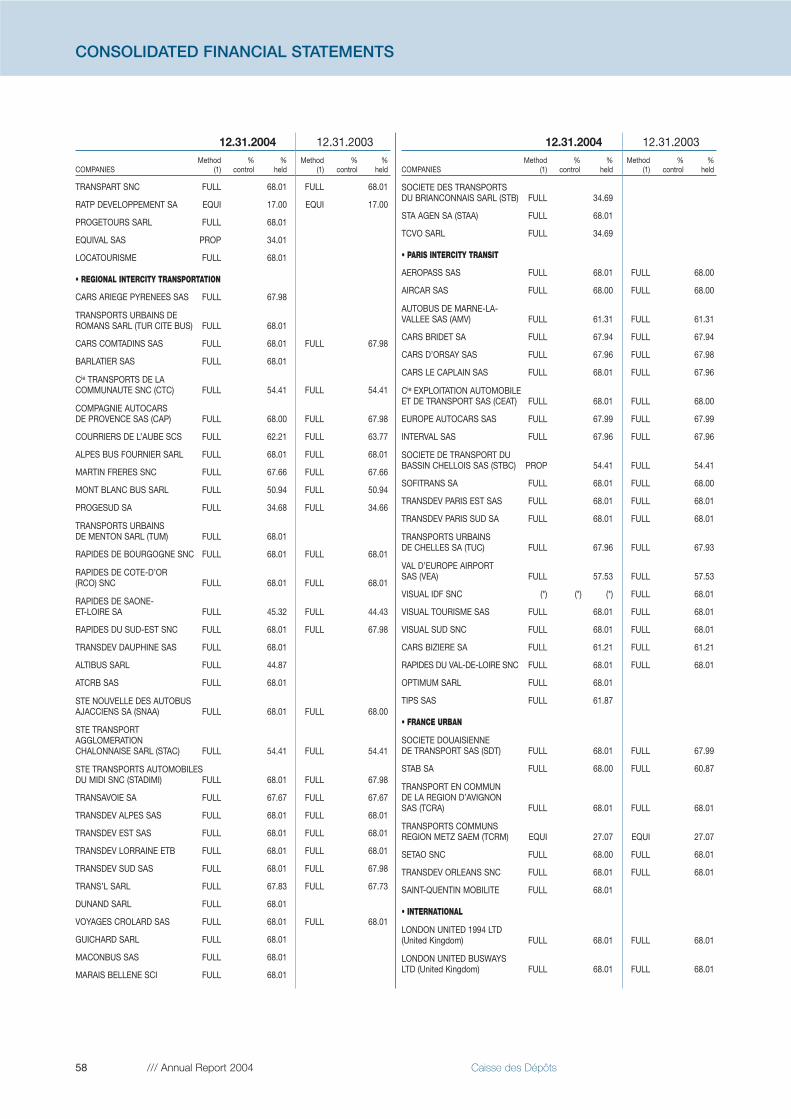

2 – Changes in the consolidation scope

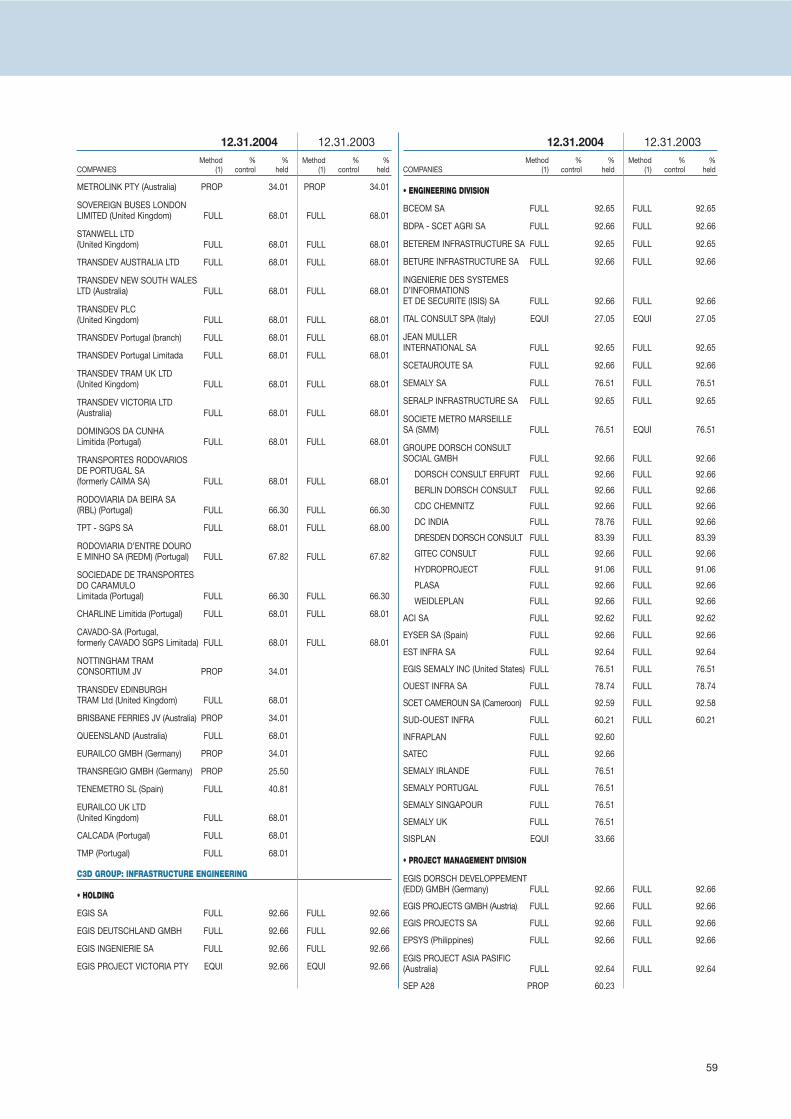

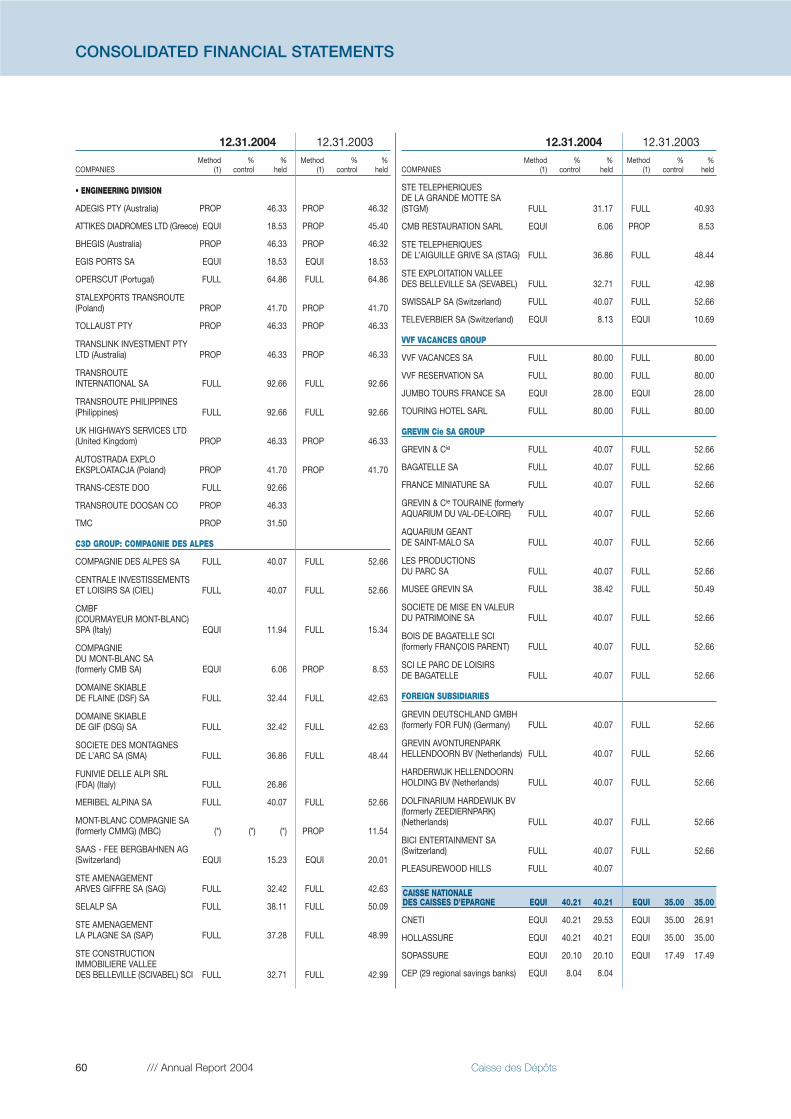

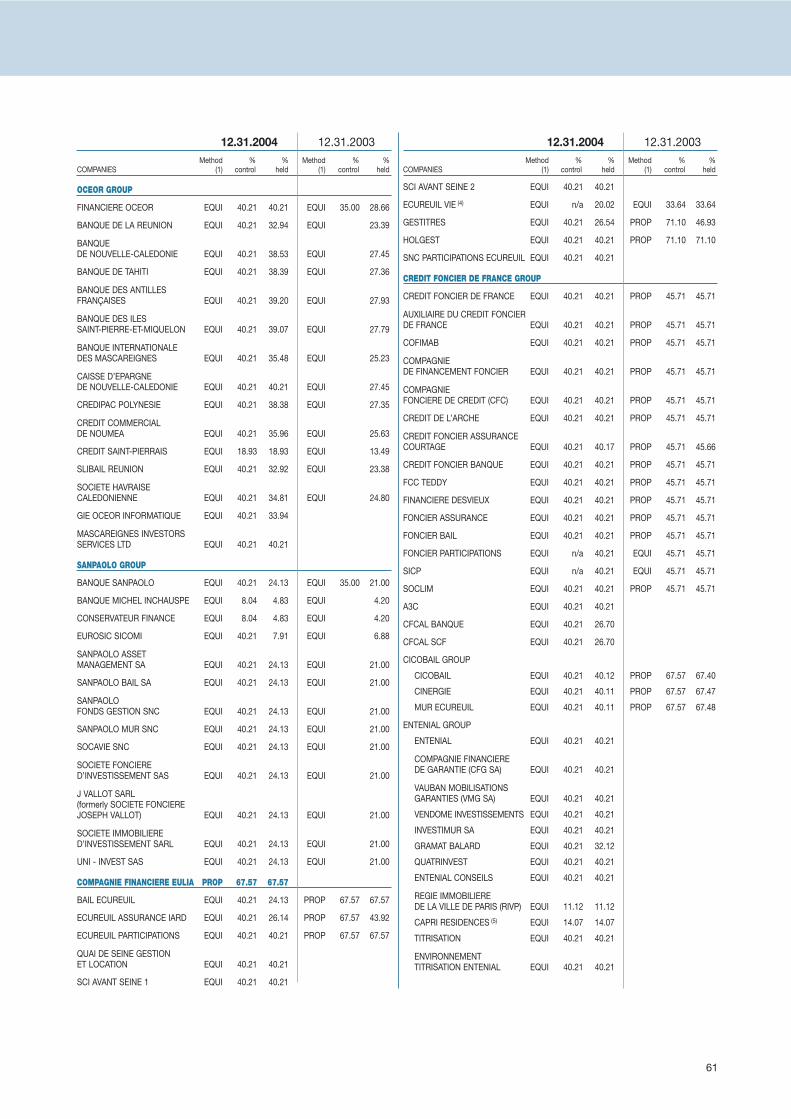

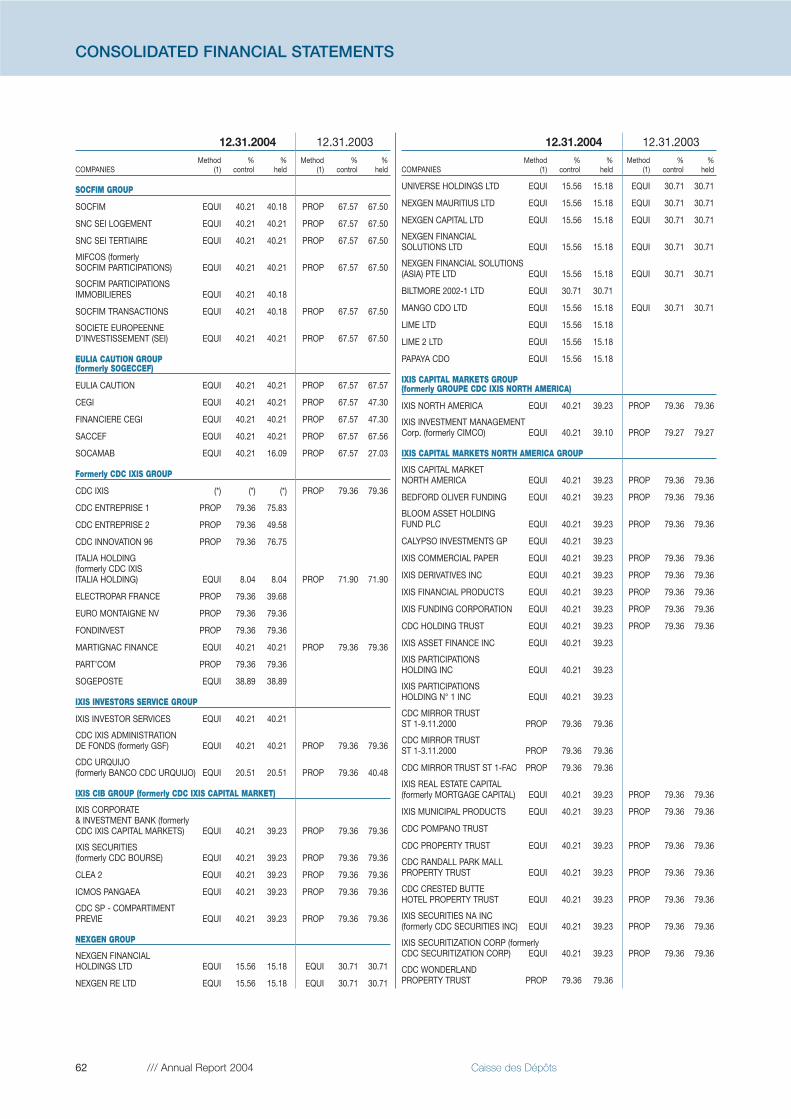

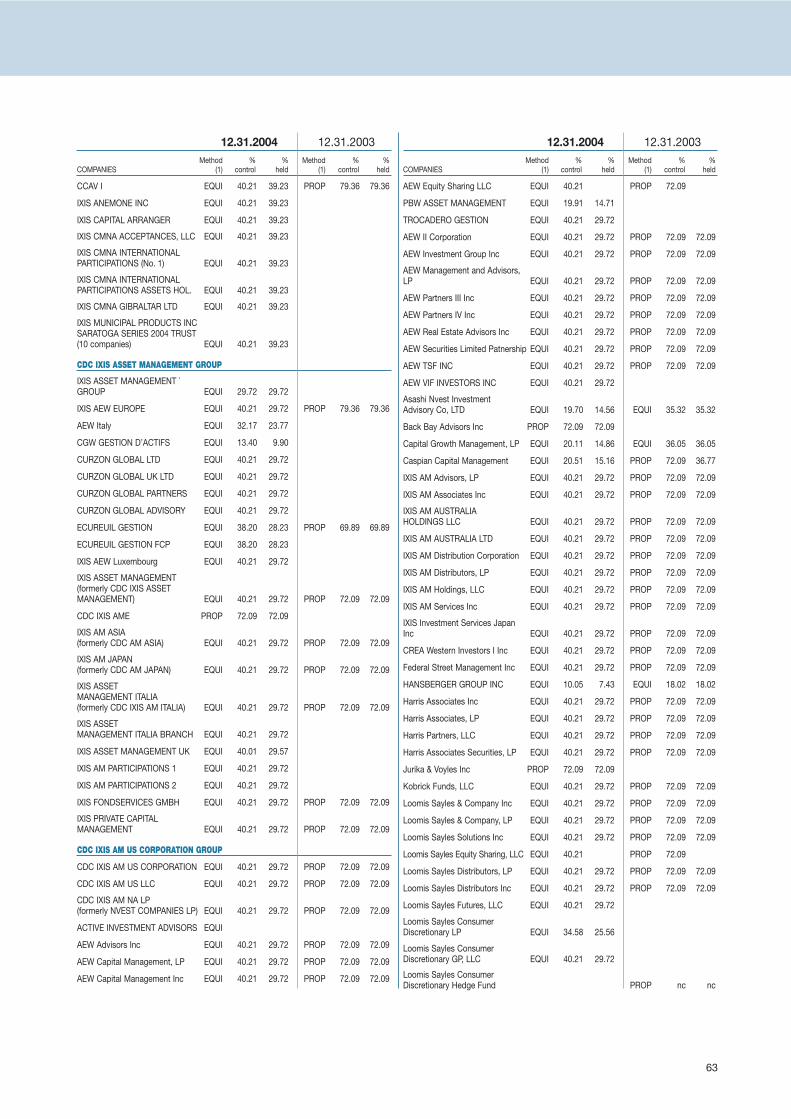

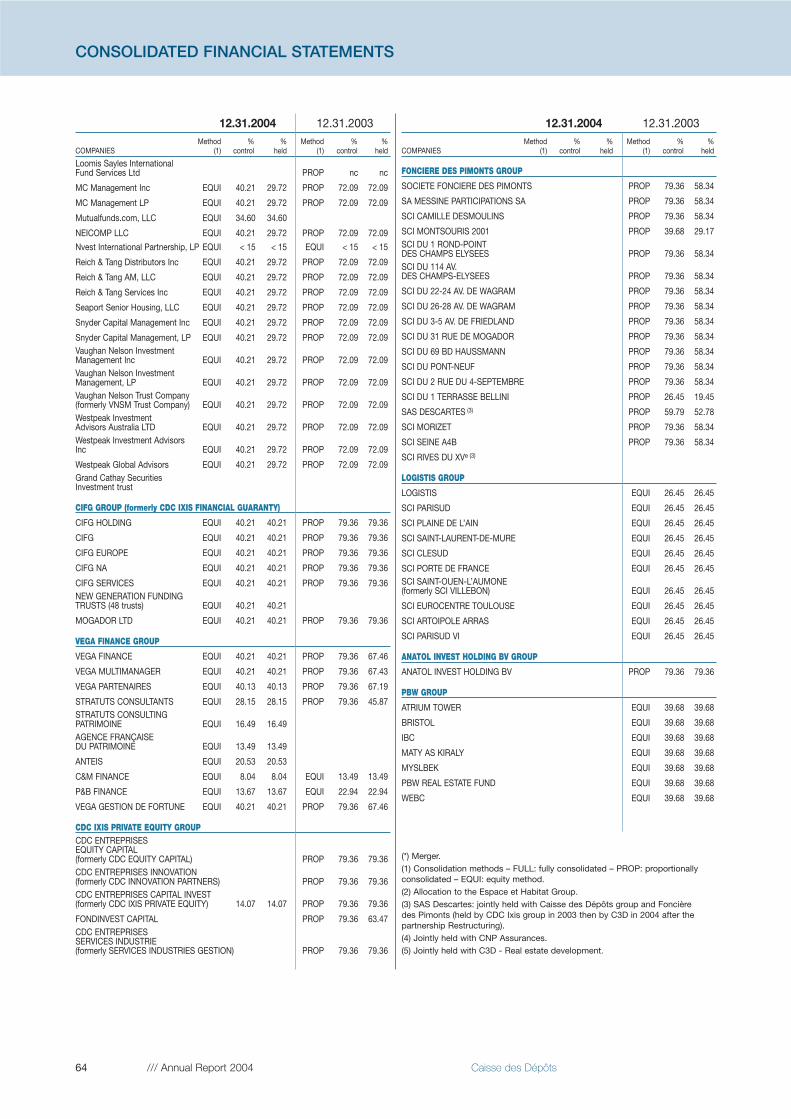

As of December 31, 2004, the consolidation scope comprised atotal of 1,012 entities, 197 more than the 815 entities consoli-dated one year earlier.

As a result of the partnership Restructuring, the consolidationmethod used for all entities within the EULIA – CDC Ixis consoli-dation scope, with the exception of real estate and private equityentities, changed from the proportional to the equity method. Anet additional 31 entities were consolidated as a result of thepartnership restructuring, including the 29 Caisses d’Epargne etde Prévoyance regional savings banks in which cooperativeinvestment certificates are held.

Excluding changes necessitated by the partnership Restructuring,an additional 166 entities have been consolidated. These aremainly in the C3D group and members of the former EULIA andCDC Ixis divisions now held through the new CNCE group.

9

3 – Goodwill and fair value adjustments

Goodwill corresponds to the difference between the cost ofshares in a consolidated undertaking and the group’s equity inthe fair value of the underlying assets, liabilities and off-balancesheet items at the acquisition date.

Fair value adjustments – corresponding to the differencebetween the value of the undertaking’s assets, liabilities and off-balance sheet items retained in consolidation and their bookvalue in the undertaking’s accounts – are amortized, writtendown or written back to income using the rules normally appli-cable to the corresponding items.

Goodwill, which may be positive or negative, is amortizedthrough the income statement over a period that reflects theassumptions made and the objectives set at the time of theacquisition, not to exceed 20 years.

If material unfavorable changes occur affecting the assumptionson which the amortization schedule is based, an exceptionalwrite-down is made and/or the rate of amortization is increased.

4 – Deferred taxes

Deferred taxes are recognized when a temporary difference isidentified between the restated carrying amount and the taxbase of assets and liabilities.

They are calculated using the liability method, whereby deferredtaxes from prior years are adjusted to account for changes in taxrates. The corresponding impact is recognized under deferredtax in the consolidated income statement.

The deferred tax rates applied to French companies were34.93% for the full rate and 15.72% for the reduced rate. In2003, the rates were 35.43% and 20.20%, respectively.

The revised 2004 French budget changed the capital gains taxrate on long-term equity holdings (15% from 2005, 8% in 2006and nil from January 1, 2007) and on portfolio securities (15% infinancial years commencing on or after January 1, 2005).

In order to finance this gradual reduction in the long-term capitalgains tax rate, the amended 2004 budget imposed a non-recurring exit tax.

Information on income taxes is provided in Note 34.

Deferred taxes are calculated separately for each tax entity. Inaccordance with the rule of prudence, deferred tax assets arerecognized only if there is a strong likelihood that they may beset against future tax liabilities.

Certain directly and indirectly held group entities make up a con-solidated tax group.

5 – Foreign currency translation

Balance sheet items and off-balance-sheet commitments of foreign companies are translated at the year-end rates, with theexception of shareholders’ equity, which is maintained at thehistorical rate. Income statements are translated on the basis ofthe average exchange rates during the year. The resulting differ-ences are entered in consolidated reserves under “Translationreserve”.

6 – Intra-group transactions

Intra-group accounts as well as income and expenses resultingfrom transactions within the group are eliminated on consolida-tion when they are material and whenever they relate to fully- or proportionally-consolidated subsidiaries.

Securities issued by group companies are also eliminated fromthe balance sheet if they are not part of the trading portfolio.

7 – Rental and leasing transactions with purchaseoption and lease-financed assets

Rental and leasing transactions are entered in the companyaccounts according to their legal nature.

Under accounting regulations, transactions that are in fact com-parable to credit transactions must be restated in the consoli-dated financial statements in such a way as to recognize theirsubstance.

Rental and leasing transactions with a purchase option aretherefore entered on the consolidated balance sheet with theoutstanding amount determined using the so-called financialmethod. The unrealized reserve, which consists of the differencebetween the reported amortization and the financial amortiza-tion of the invested capital, is recognized in consolidatedreserves net of deferred taxes.

Fixed assets acquired through a lease or similar agreement arerestated for the purpose of consolidation and entered on thebalance sheet as if their acquisition had been financed throughborrowing.

Presentation and accountingpolicies – Banking and financialactivities

1 – Income statement items

Interest and commissions classified as such are recorded on anaccruals basis. Commissions not classified as interest arerecorded on a cash basis.

2 – Foreign-currency-denominated transactions

Foreign-currency-denominated assets, liabilities and off-balance sheet commitments have been translated at theexchange rates in effect on December 31, 2004.

Currency gains and losses from ordinary currency transactionsare recorded in the income statement.

Spot foreign exchange transactions are valued at the spot rate.Forward currency transactions, other than hedging, are valuedat the forward rate of the remaining period. Forward currencytransactions for hedging purposes are valued by symmetry withthe item hedged.

Premiums and discounts related to hedged foreign currencytransactions are taken as income and expenses over the periodremaining until the maturity of these transactions.

10 /// Annual Report 2004 Caisse des Dépôts

CONSOLIDATED FINANCIAL STATEMENTS

3 – Advances and loans to financial institutions and customers

These items include loans, overdrafts and securities purchasedunder collateralized and uncollateralized fixed resale agreements.

LoansLoans are recorded as assets in the balance sheet at repaymentvalue. Accrued interest is recognized as income over the life of the loan.

Loans are classified as non-performing when a recognizedcredit risk arises, in other words once it becomes likely that partor all of the amounts due under the loan agreement will not bereceived, notwithstanding the existence of a guarantee or secu-rity deposit. In any event, non-performing loans include those forwhich payments are more than three months past due (sixmonths for real estate loans and nine months for loans to localgovernments), those where the deterioration of the counter-party’s financial situation creates the risk of non-recovery andthose that are the subject of a legal dispute.

Similarly, once a loan for a given counterparty is classified asnon-performing, all loans to that counterparty are classified asnon-performing under the contagion principle. For groups ofcompanies, the contagion principle is applied selectively.

For accounting purposes, irrecoverable non-performing loansare recognized separately. These include those loans for whichthe counterparty’s solvency is such that after the loans have beenclassified as non-performing for a reasonable amount of time, noreclassification to performing loans is foreseeable; loans forwhich an acceleration clause has been triggered; and someloans classified as non-performing for more than one year, i.e.those presenting irrecoverable characteristics and for which aprovision must be established and those for which a future trans-fer to loss is foreseeable. This assessment must be performedafter taking into account any existing loan guarantees.

Non-performing loans and irrecoverable loans may be reclassi-fied as performing loans when payments have resumed in asteady fashion for the amounts corresponding to the originalcontractual payment schedule and once the counterparty nolonger presents a default risk. They may also be classified asrestructured loans if debt has been rescheduled and followingan observation period.

For loans with recognized credit risk exposure, provisions areestablished to cover all projected losses on loans classified asnon-performing or irrecoverable. A full provision is establishedon all outstanding, accrued and unpaid interest.

Once the loan is deemed to be definitively irrecoverable, a loss is recorded.

Loans restructured at below market rates are broken out sepa-rately, where applicable, in a specific sub-category for perform-ing loans. At the time of the restructuring, the loan is recorded atnominal value less a discount, booked to cost of risk, corre-sponding to the amount of interest forfeited. This interest differ-ential is accounted for in the lending margin over the life of theloan concerned.

Securities purchased under collateralized and uncollateralized fixed resale agreementsThese securities are recorded as assets in the balance sheet onthe line representing the receivable arising from the transaction.The corresponding income is recognized on an accruals basis.Securities received as collateral and subsequently sold arerecorded as liabilities and valued at market value.

4 – Securities and securities transactions

Securities are classified under five accounting categories corre-sponding to the institution’s activities.

Trading securitiesTrading securities include in particular Treasury bills and nego-tiable debt securities. They are expected to be held for periodsnot exceeding six months. They are highly liquid and are markedto market. Changes in market value are recognized in theincome statement.

Available-for-sale securitiesAvailable-for-sale securities comprise securities that are not tobe held until maturity or for trading purposes. They also includetrading securities reclassified after being held for a period ofmore than six months. In this case, the reclassification is madeat market value on the date of the transfer.

Available-for-sale securities are treated according to the FIFOmethod and are valued as follows:

• Bonds and equities: unrealized losses calculated based ontheir year-end closing price are taken to expenses through aprovision for impairment.

• Treasury bills, negotiable debt securities, and interbankinstruments: provisions are made on the basis of the individ-ual situation of the issuer and market indicators.

Any premiums and discounts are written off over the residual lifeof the asset on a yield-to-maturity basis for negotiable debtsecurities and on a straight-line basis for other securities.

Held-to-maturity securitiesThis portfolio comprises fixed income securities that areintended to be held until maturity, and financed with dedicatedlong-term resources or covered through hedging instruments.

Unrealized capital losses resulting from differences between bookand market values are not covered by provisions. However, ifapplicable, default risks are taken into account in determining thevalue of these securities at year-end. The difference between theacquisition price and the redemption value of the securities (pre-mium or discount) is amortized using the yield-to-maturity methodfor negotiable debt securities and the straight-line method forother securities.

11

Inflation-indexed French government bonds (OATs)Given the lack of specific regulations applicable to financial insti-tutions, the effect of indexation on the face value of inflation-indexed bonds may be accounted for: when the bond is sold ormatures; or spread over the bond’s remaining life, or recognizedas income or expense for the period.

Effective December 31, 2003, the Central Sector decided torecord as income or expense any gains or losses related to theindexation of the bond’s face value to inflation, by analogy to theaccounting treatment prescribed by article R332-19 of theFrench Insurance Code, as amended by decree No. 2002-1535of December 24, 2002.

The accounting provisions of CRC Standard 2002-03 relative tocredit risk in companies subject to CRBF regulations apply,where appropriate, to credit risk for held-to-maturity securities.

Portfolio securities (TAP)Portfolio securities are investments made on a regular basis withthe aim of realizing a capital gain in the medium term but withoutthe intention of investing on a long-term basis in the develop-ment of the business or taking an active part in the operationalmanagement of the issuing undertaking.

These securities are recorded at the lower of cost or fair value.

Fair value is determined by taking into account the general eco-nomic outlook for the issuer and the remaining period for whichthe securities will be held. For listed companies, fair value is gen-erally represented by the average share price over a period suffi-ciently long to reduce the impact of sharp price fluctuations overthe expected holding period.

Non-consolidated equity securitiesNon-consolidated equity securities are recorded at acquisitioncost.

They are valued on the basis of their fair value, with reference tovarious criteria such as net assets, potential return, and capital-ization of earnings. Provisions are booked to reflect any perma-nent impairment in the fair value of these securities.

Lending and borrowing of securitiesSecurities are valued using the rules applicable to the portfolio of origin.

Borrowed securities are recorded as an asset under tradingsecurities at their market value on the day they were borrowed,and as a liability to recognize the debt towards the lender. Theyare valued on the basis of their market value on the closing date.

Loans and borrowings guaranteed by cash and notes aretreated in the same way as collateralized resale agreements.

Income from these transactions is recognized on an accrualsbasis in the income statement.

Issues indexed on fund performanceThese consist in structured issues, the most often with a zerocoupon, that are indexed on fund performance. The index ishedged by the purchase of units in the fund whose performanceaccrues entirely to the subscribers at maturity.

The overall financial engineering margin on these transactionsis estimated by reference to the market value of the units in thefund and the present value of future cash flows relating tothese issues as well as to future management expenses. Asrequired by applicable regulations, extremely prudent assump-tions are used regarding early redemption when the valuationis based on models.

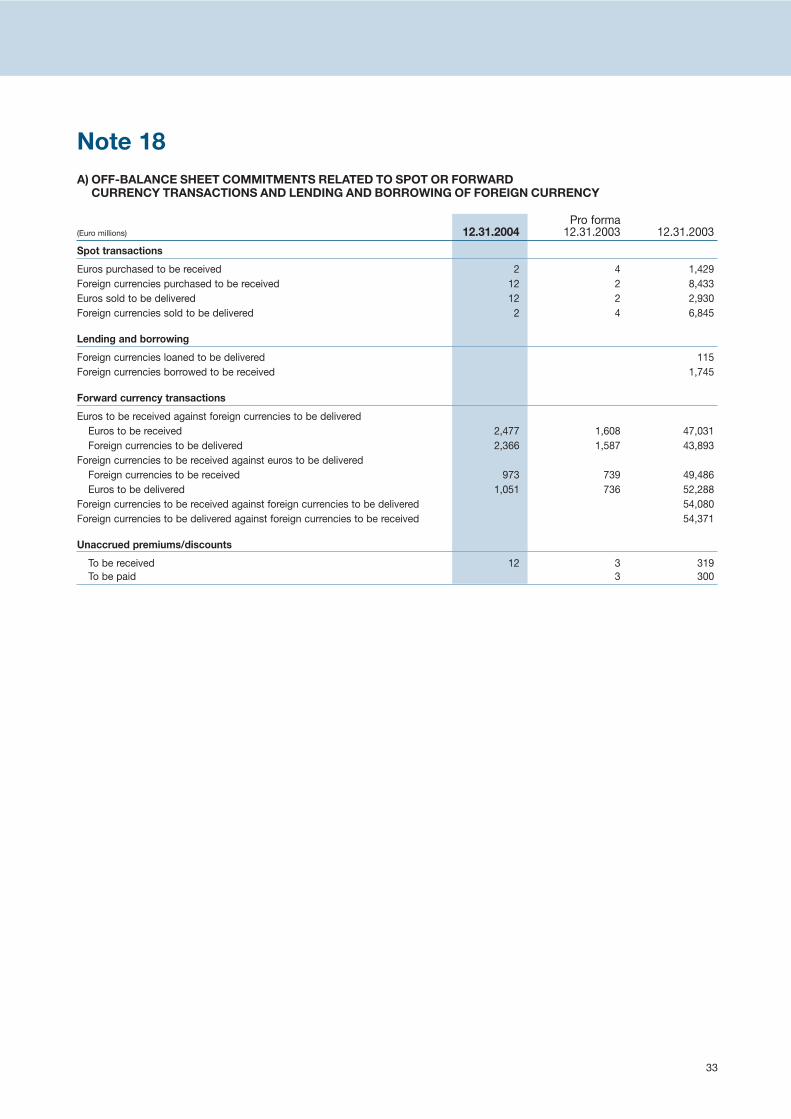

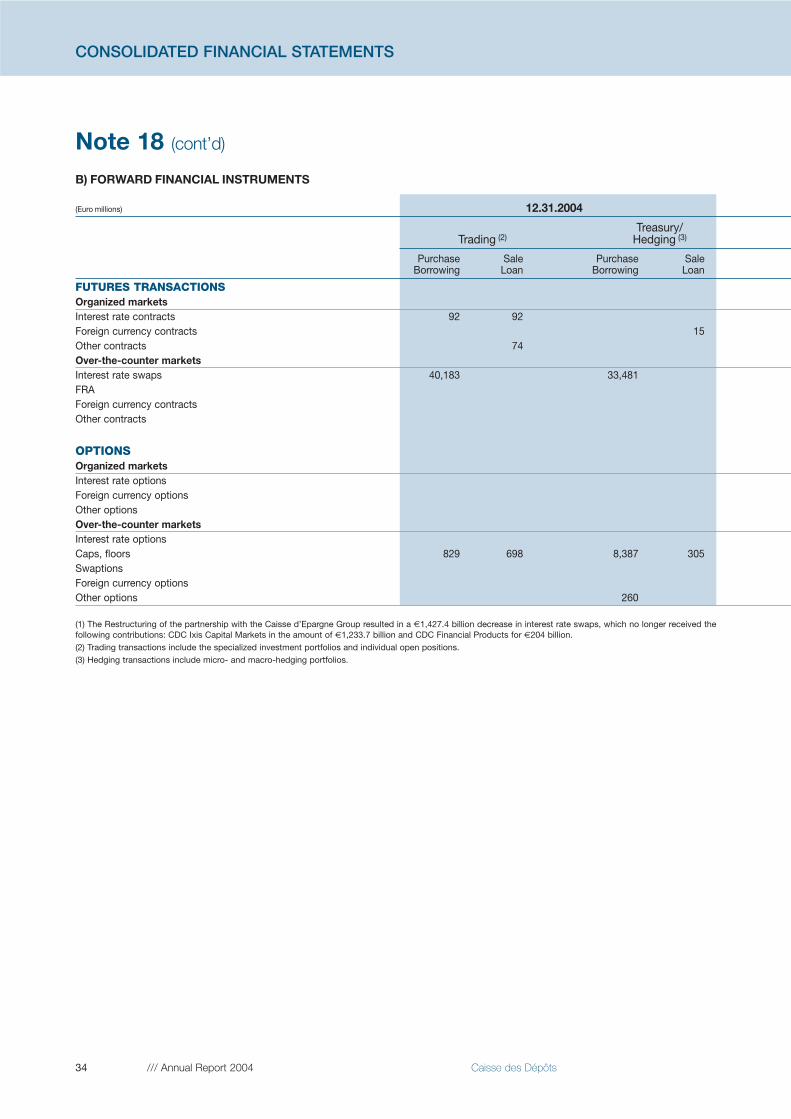

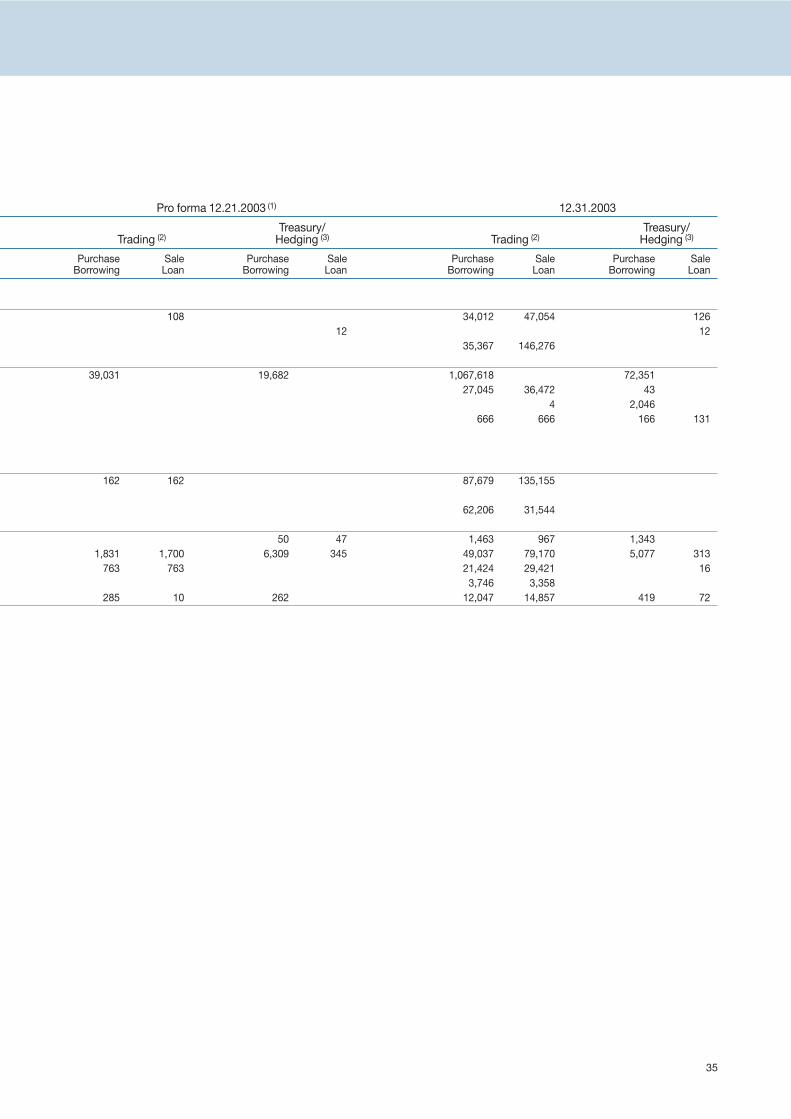

5 – Forward financial instruments

In application of the strategy defined for the development of itstrading activities and the management of market risks, theCaisse des Dépôts group operates on all organized and over-the-counter markets for interest rate, currency and equity futuresand options, in France as well as abroad. These transactions areentered into as part of specific or general hedging and the spe-cialized management of trading portfolios.

For all of these instruments, whatever the management policypursued, the face value of the futures and options contracts, thevalue of the underlying assets or the exercise price is recordedoff-balance sheet.

The method of accounting for expenses and revenues on theseinstruments depends on the management policy pursued.

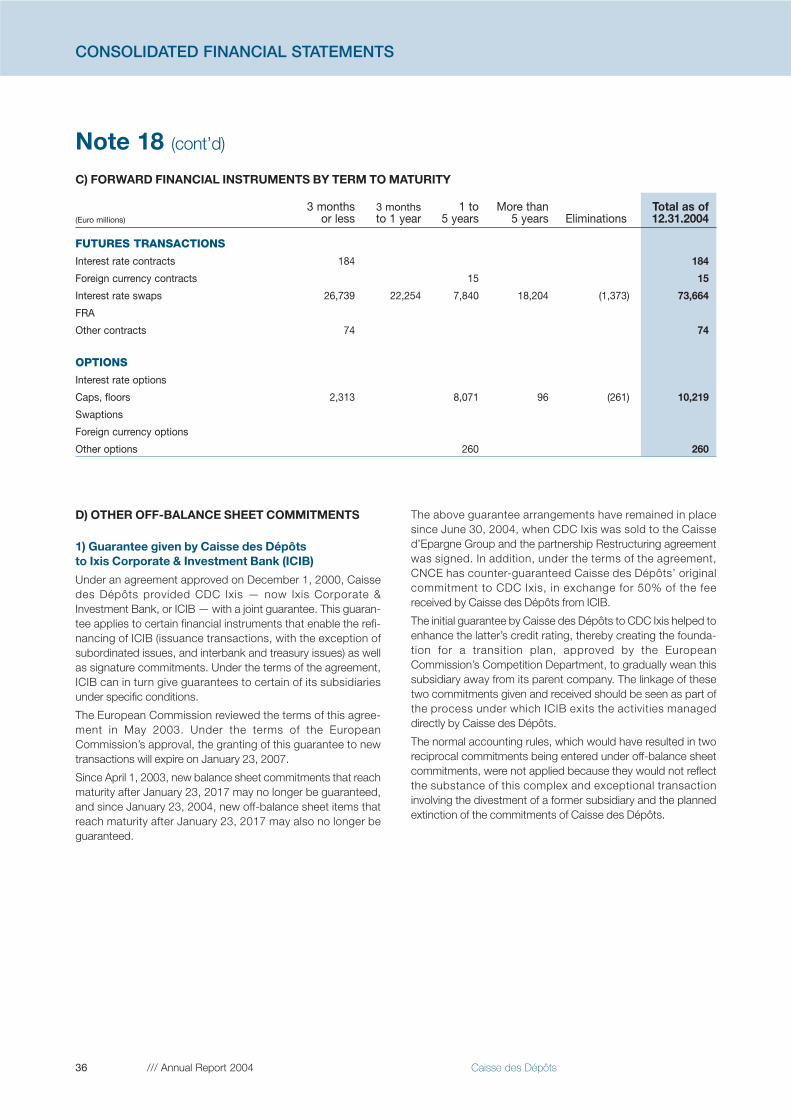

The transposition into French Law of European “fair value” and“modernization” directives resulted in the publication of CRCStandards 2004-14, 2004-15, 2004-16, 2004-17, 2004-18 and2004-19. These require disclosure of the fair value (if it can bedetermined through reference to a market value or the applicationof generally accepted models and methods) and information onthe volume and type of instrument for each category of derivativefinancial instrument. This information is provided in Note 18.

Interest rate and currency swaps

Hedging transactions: expenses and revenues resulting fromhedging instruments (taken singly or as a homogeneous group)are recognized symmetrically with the revenues and expensesresulting from the hedged transaction.

• Transactions undertaken within the context of spe-cialized portfolio management: contracts are valued atyear-end at their market value. In accordance with regulations,the market value takes into account an adjustment for defaultrisks and the discounted value of future management costs.The total net mark-to-market gain or loss is recognized in theincome statement.

12 /// Annual Report 2004 Caisse des Dépôts

CONSOLIDATED FINANCIAL STATEMENTS

Other interest rate and currency transactions These transactions relate primarily to futures and options.

• Hedging transactions: expenses or revenues are recognizedin the income statement on a symmetrical basis with the revenues or expenses on the hedged transaction;

• Other transactions: these transactions are marked to mar-ket. Unrealized gains or losses at the closing date are recog-nized in the income statement.

In order to provide a fair value of these instruments, those thatare not highly liquid are also valued by reference to their theo-retical market value.

Complex transactionsComplex transactions include derivatives, which combinerepackaged instruments of various types, characteristics andpricing methods.

Each component of the transaction is recorded on- or off-balance sheet according to the nature of the underlying.

The result is considered globally and recorded through one entryreflecting the substance of the transactions, as if they were a singleinstrument. In the case of totally new products, when not governedby explicit regulation, the accounting approach to recognition ofany gains and losses is based on similar existing products.

The method of accounting for gains and losses depends on themanagement policy pursued:

• Hedging transactions: for reasons of prudence, notably whenmarket liquidity is low, results are recorded on an accruals basis.A provision is made when market value is negative;

• Trading portfolio or transactions for which the result canbe considered as an arrangement fee: the result is recog-nized when the transaction is initiated. A discount is applied totake into account future management expenses and possibledefault risks.

Credit derivativesCredit derivatives are instruments whose purpose is to transferthe credit risk in respect of an asset from one counterparty toanother, generally in exchange for a premium paid at the outset orby installments. In the case of events predefined in the relatedcontract, known as credit events, the seller of the cover is calledupon to bear the cost under the terms defined in the contract.

There are three categories of credit derivatives: credit defaultswaps, total rate of return swaps and credit linked notes. Interms of their characteristics and risks, they may be likened tooptions, interest rate swaps and securities swaps, respectively.

In the absence of a specific accounting text, the accountingapproach for credit derivatives is based on their analogy to exist-ing products with which they can be likened and taking intoaccount the management policy being pursued:

• Hedging transactions: expenses and revenues are recog-nized symmetrically with the revenues and expenses on thehedged transaction;

• Isolated open-position transactions undertaken as partof a long-term holding: the result is booked on an accrualsbasis. A provision is made against unrealized losses;

• Specialized portfolio management transactions: whenmarket liquidity for the derivative is assured, contracts are val-ued at market price with a discount applied to take intoaccount possible default risks and the present value of futuremanagement expenses. Otherwise, contracts are valuedusing the applicable regulations for the underlying transac-tions, which involves valuing them at cost and, where neces-sary, establishing a provision for impairment.

Market valuesWhen the market price of the instruments or the valuationparameters are not officially quoted, alternative valuation meth-ods are used, making reference to one or more of the followingcriteria: price confirmation by brokers or outside counterparties,comparison with actual transactions and research by issuer orinstrument category.

When instruments are valued using models, these integrate theparameters that affect the valuation of the instruments, inparticular the liquidity level of the related markets. Applying aprudent approach, the calculations are adjusted to take accountof the weaknesses of some of these parameters, in particulartheir relevance over a long period.

6 – Tangible and intangible fixed assets

CRC Standard 2002-10 of December 12, 2002 regarding thedepreciation and amortization of assets applies to fiscal yearsbeginning on or after January 1, 2005.

Within the Caisse des Dépôts group, only the C3D group (exclud-ing Compagnie des Alpes) applied the standard in advance, in2004. The impact of this change in accounting method on theretained earnings of the Caisse des Dépôts group is not material.

Other entities within the Caisse des Dépôts group have appliedthe transition measures outlined in article 15 of the standard andcomplemented by the provisions of ruling 2003-F by the CNC(the French National Accounting Board) Urgent Issues TaskForce.

Fixed assets are valued at cost. In the case of buildings, initialfixtures, fittings and installation expenditure may be added tothe cost of acquisition.

Depreciation is calculated using the straight-line method andaccording to the type and quality of the building, over its estimated useful life. Thus, buildings are depreciated over 20 to50 years. Partial renovation work on old buildings is depreciatedover periods of between 15 and 25 years.

Installations, improvements and fittings are generally depreci-ated over ten years.

13

Market shares acquired are not amortized. They are, however,periodically subjected to an impairment test based on the valua-tion of the benefits arising from the competitive position held.

As for insurance activities, the fair value of the contracts portfolio,which corresponds to the estimated present value of future dis-tributable profits attributable to the portfolio at the time of theacquisition, is amortized for like groups of contracts using aschedule that is updated regularly and reflects the likelihood offuture profits over a reasonable period.

As a general rule, software is written off over three years (maxi-mum of five years).

Forests are subject to provisions for impairment as required. Inthe event of an irreversible loss, a non-recurring impairment lossis recognized for the full amount.

7 – Investment property risks

Caisse des Dépôts owns a large portfolio of rental propertiesheld as long-term investments.

Market values are determined regularly by independent appraisers. A provision is made for any material impairment invalue of these properties, representing the difference betweencarrying value and market value.

8 – Advances and loans from financial institutions and customer deposits

These liabilities include deposits, loans and securities sold undercollateralized and uncollateralized fixed repurchase agreements.

LoansLoans are recorded in the balance sheet at repayment value andaccrued interest is charged to income over the life of the loan.

Securities sold under collateralized fixed repurchase agreementsThe debt is recorded under liabilities. The securities are main-tained in their original portfolio and valued according to the rulesapplicable to that portfolio. The corresponding interest is recog-nized through the income statement as it is accrued.

9 – Debt securitiesDebt securities are reported according to the type of security:interbank and negotiable debt securities (commercial paper,certificates of deposit and medium-term notes), bonds and similar debt securities.

Accrued interest is recorded on the same balance sheet line asthe debt security and is charged to income.

Commissions on the issue of debt securities and any premiumson their issue or redemption are charged to income over the lifeof the securities.

10 – Provisions for risks and charges

This heading includes in particular:

• provisions for country risk, which are determined based on anappraisal of the risk carried by the group in the respectivecountries or on borrowers in those countries; the appraisal cri-teria are generally based on an assessment of the country’seconomic, financial and socio-political situation;

• provisions for sector risks and general provisions to coverlosses whose realization and valuation is uncertain;

• provisions for employee-related commitments correspondingmainly to retirement benefits and expenses related to theestablishment of framework agreements to organize phasedand other early-retirement plans within various group entities;

• provisions for risks and charges not related to banking trans-actions, established in accordance with the terms of CRCStandard 2000-06 regarding the accounting for liabilities.These provisions are intended to cover risks and charges thatare clearly defined but whose amount or timing remainsuncertain. The establishment of these provisions is subject tothe existence of an obligation to a third party at year-end, andthe absence of at least an equivalent consideration from thethird party. This regulation does not cover, in particular, bank-ing transactions, financial instruments and insurance con-tracts in force;

• provisions for default risks established among the real estatedivision’s subsidiaries. They cover the scope of sound com-mitments entered on the balance sheet or as off-balancesheet commitments, for which statistical information is avail-able that makes it possible to assess default probabilities.These provisions are determined by applying multiples seg-mented by rating category and residual term, and weighted byrecovery assumptions in the event of a default. In particular,they cover potential risks on the real etate sector, credit institu-tions, the local and regional public sector and structuredfinancing;

• provisions for major repairs established in accordance withCRC Standard 2002-10 related to asset depreciation, amorti-zation and impairment and whose application methods aredescribed in section 6 above, “Tangible and intangible fixedassets”.

14 /// Annual Report 2004 Caisse des Dépôts

CONSOLIDATED FINANCIAL STATEMENTS

11 – Pension and related commitments

In France, pension liabilities are generally covered by contribu-tions taken as expenses and paid to retirement or insurancefunds, which then handle pension payments, or paid to the gov-ernment in the case of civil servants.

When not covered by insurance contracts, provisions are madefor employee retirement benefits for each category of employeesbased on collective bargaining agreements. These provisions arecalculated using an actuarial method taking into account the ageand seniority of the personnel, the mortality rate and probableremaining service with the group until retirement age and esti-mated future salary levels. This provision is adjusted on eachclosing date based on changes in the actuarial liabilities.

When these commitments are covered by an insurance policy,the annual premiums paid to the insurance company areincluded in expenses for the period.

In countries other than France, there are various compulsoryretirement plans to which employers and employees pay contri-butions. Depending on each case, the corresponding commit-ments are paid to company pension funds or recognized in theindividual accounts of the companies concerned. No adjust-ments are made in this respect in the consolidated financialstatements.

Commitments related to statutory long-service awards orCaisse des Dépôts long-service awards are calculated using thesame method as it is used to determine commitments for retire-ment benefits.

12 – Subordinated debt

This category includes debts whose repayment in the event ofliquidation of the debtor would occur only after other creditorshave been repaid.

Accrued interest payable is recorded in an accruals account andcharged against income.

13 – Fund for General Banking Risks

This fund is constituted to cover operational risks and lossesarising from banking activities and the management of financialassets that are not covered by general or specific provisions.Transfers are made to and from this fund on a regular basis tocover these risks.

14 – Other information

Some of the previous year’s figures have been adjusted from thefigures reported in 2003.

Principal accounting and presentation policies – Insurance business

Accounting policies and valuation methods specific to insuranceactivities have been maintained in the consolidated financialstatements of Caisse des Dépôts.

Caisse des Dépôts group applies CRC Standard 2000-05regarding rules for consolidating companies governed by theInsurance Code.

Constituent items of the consolidated financial statements ofinsurance companies are presented on the lines of the balancesheet, income statement and off-balance sheet that are of thesame nature, with the exception of the following items:

Investments of insurance companiesInsurance company investments include real estate, invest-ments representing unit-linked policies and various otherinvestments.

Real estate investments are shown in the balance sheet atacquisition cost, net of acquisition expenses, but increased toreflect the cost of improvements and certain taxes. Propertiesare depreciated over their estimated useful life. The estimatedvalue of properties is based on reports produced by independ-ent appraisers. A provision is recognized in the event of perma-nent impairment in value.

Investments allocated to unit-linked policies are reassessed atthe year end by reference to variations in related unrealized cap-ital gains or losses. Technical reserves relating to these policiesare similarly reassessed.

Equities and other variable income securities are recorded atcost excluding expenses. A provision for impairment is estab-lished to cover lasting impairment in the value of the securities,determined relative to the estimated recovery value.

Marketable securities and other fixed-income securities arerecorded at cost excluding accrued income. The differencebetween the redemption value of these securities and their cost,excluding accrued income, is allocated on an actuarial basisover the remaining term to maturity. A provision is established inthe event of a default risk on the part of the issuer.

Moreover, when the net book value of the real estate invest-ments and variable income securities exceeds the realizablevalue of these assets, a liquidity risk reserve, which is equal tothe difference between these two amounts, must be estab-lished.

Technical reserves of insurance companiesTechnical reserves correspond to commitments to policyholdersand beneficiaries.

15

Life insuranceFor policies including death cover, technical reserves comprise the share of written premiums not earned in the periodconcerned.

The mathematical reserves relating to premiums on non-unit-linked policies correspond to the difference between the presentvalue of the liabilities of the policyholder and of the insurer.

Life insurance reserves are set aside using a discount rate notexceeding the expected return, cautiously estimated, on theassets representing these reserves.

Liabilities are discounted applying a rate that is at the most equalto the rate of the policy concerned, and using published mortal-ity tables or actual mortality rates if these are more prudent.

An overall reserve is made for the amount of the total futuremanagement expenses of policies not covered by the premiumor management loading.

When remuneration in excess of the minimum guaranteed rate,based on the results of technical and financial management, isdue to the policyholders and has not been distributed to themduring the period, this remuneration is included in the policy-holder surplus reserve.

The reserve for claims payable includes outstanding claims andcapital due at the year-end.

Mathematical reserves in respect of unit-linked policies areassessed on the basis of the assets underlying these policies.

Disability, accident and health insuranceA reserve is taken for incremental risks to cover timing differ-ences between the time when guarantees are acquired by poli-cyholders and when they are financed by insurance premiums.

Reserves for claims are based on the estimated value of fore-seeable expenses net of any recoveries.

Non-life insuranceNon-life insurance technical reserves comprise reserves forunearned premiums (share of premiums issued that correspondto subsequent years) and reserve for claims payable.

Gross margin on insurance activitiesThe gross margin on insurance activities comprises earned pre-miums, the cost of benefits (including changes in technicalreserves) and net investment income.

Principal accounting and presentation policies –Service sector businesses

Accounting policies and valuation methods specific to servicesector businesses have been maintained in the consolidatedfinancial statements of Caisse des Dépôts group.

Constituent items of the financial statements of service compa-nies are presented on the lines of the consolidated balancesheet, income statement and off-balance sheet that are of thesame nature.

One specific line only has been added, entitled “Net incomefrom other activities” as an income statement subtotal. Netincome from other activities comprises mainly sales and otheroperating income, less purchases consumed.

16 /// Annual Report 2004 Caisse des Dépôts

CONSOLIDATED FINANCIAL STATEMENTS

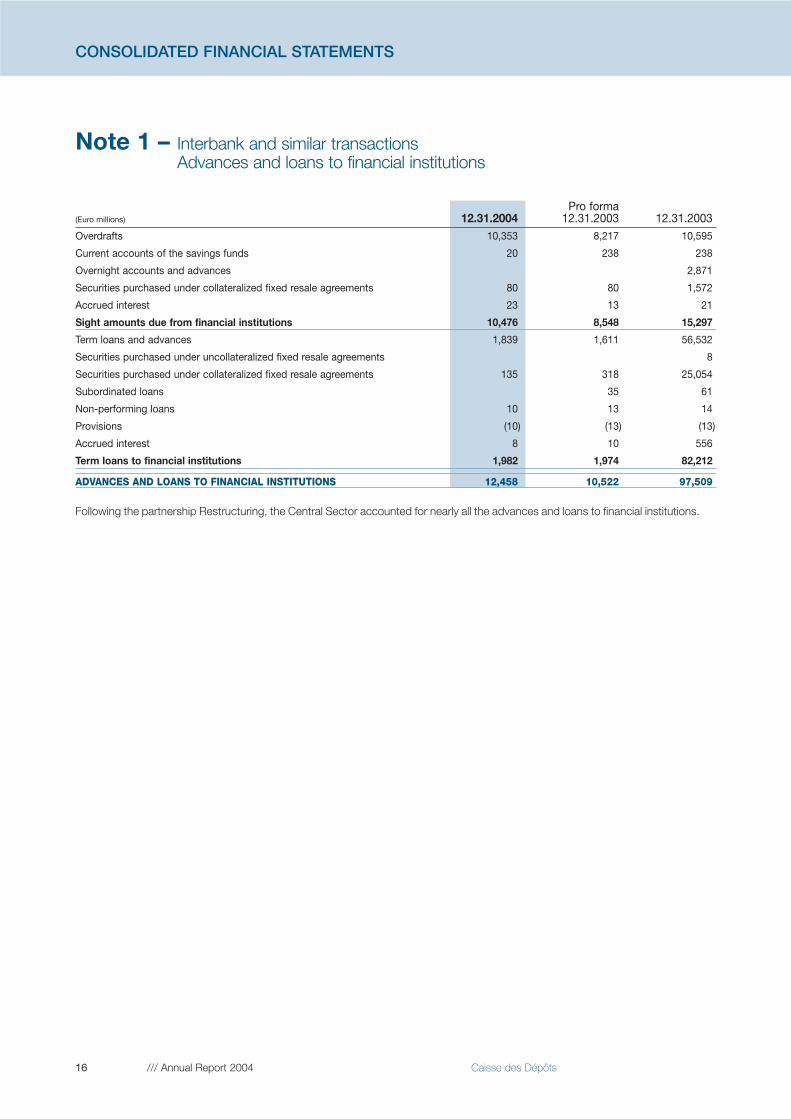

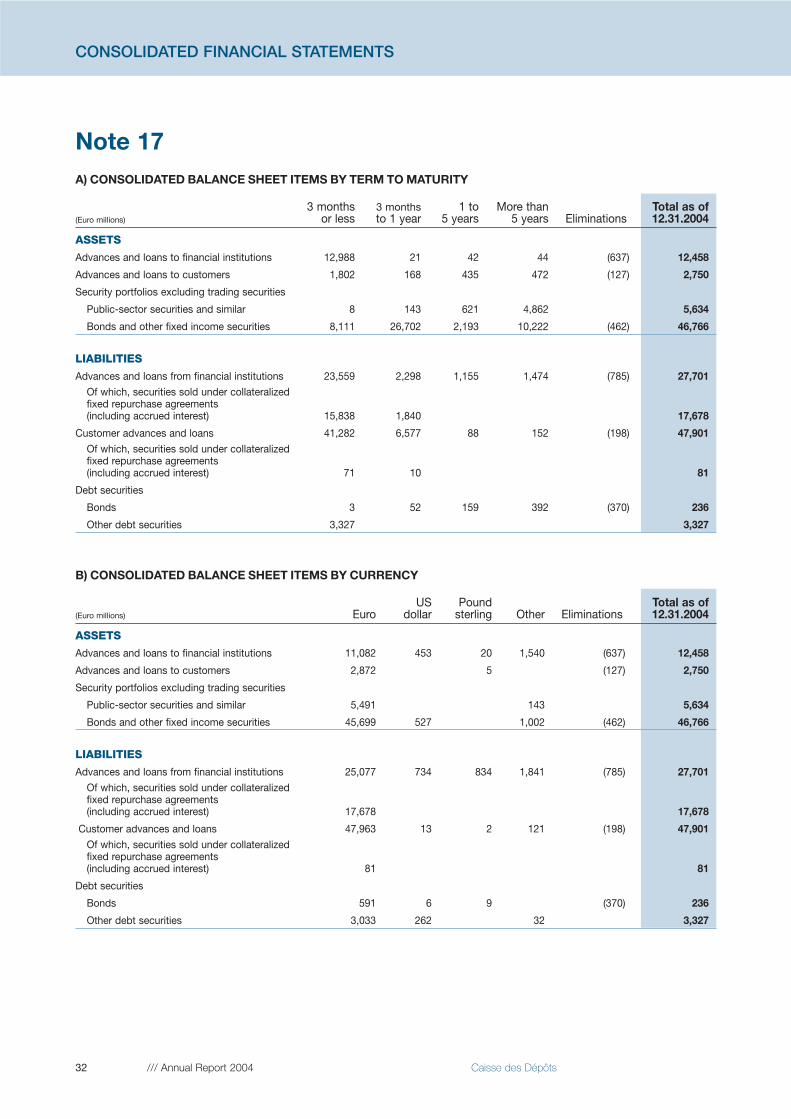

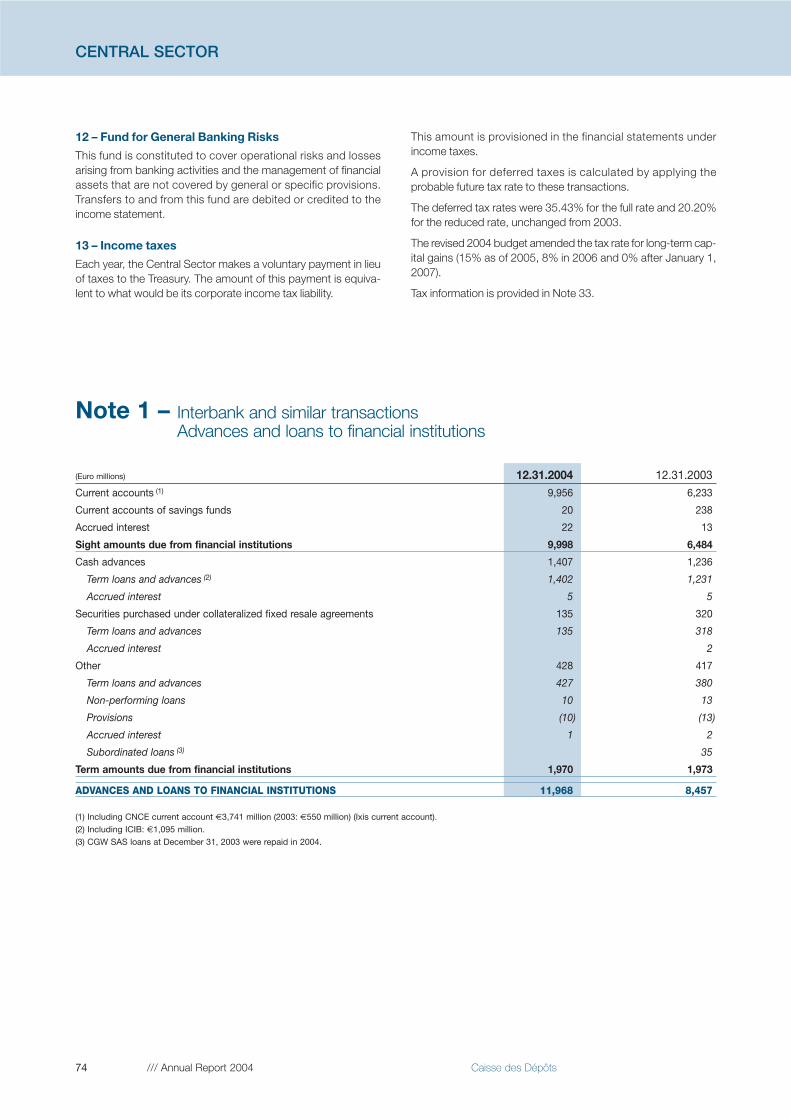

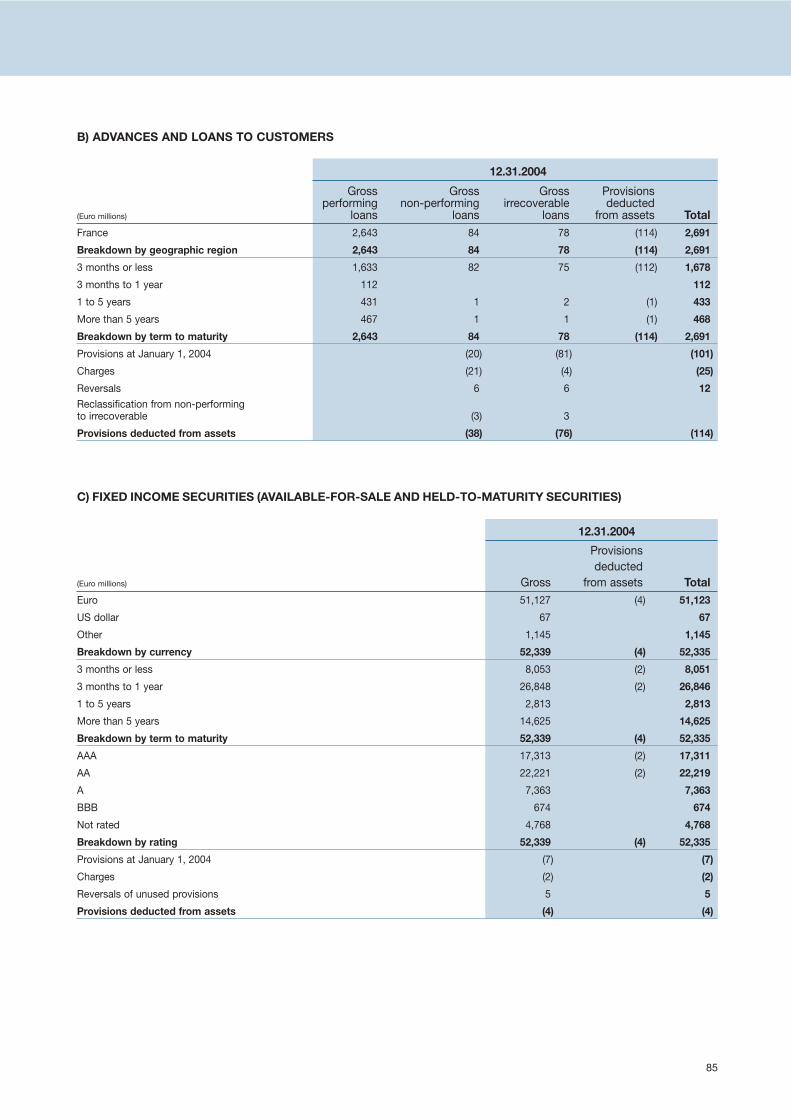

Note 1 – Interbank and similar transactions Advances and loans to financial institutions

Pro forma (Euro millions) 12.31.2004 12.31.2003 12.31.2003Overdrafts 10,353 8,217 10,595

Current accounts of the savings funds 20 238 238

Overnight accounts and advances 2,871

Securities purchased under collateralized fixed resale agreements 80 80 1,572

Accrued interest 23 13 21

Sight amounts due from financial institutions 10,476 8,548 15,297

Term loans and advances 1,839 1,611 56,532

Securities purchased under uncollateralized fixed resale agreements 8

Securities purchased under collateralized fixed resale agreements 135 318 25,054

Subordinated loans 35 61

Non-performing loans 10 13 14

Provisions (10) (13) (13)

Accrued interest 8 10 556

Term loans to financial institutions 1,982 1,974 82,212

ADVANCES AND LOANS TO FINANCIAL INSTITUTIONS 12,458 10,522 97,509

Following the partnership Restructuring, the Central Sector accounted for nearly all the advances and loans to financial institutions.

17

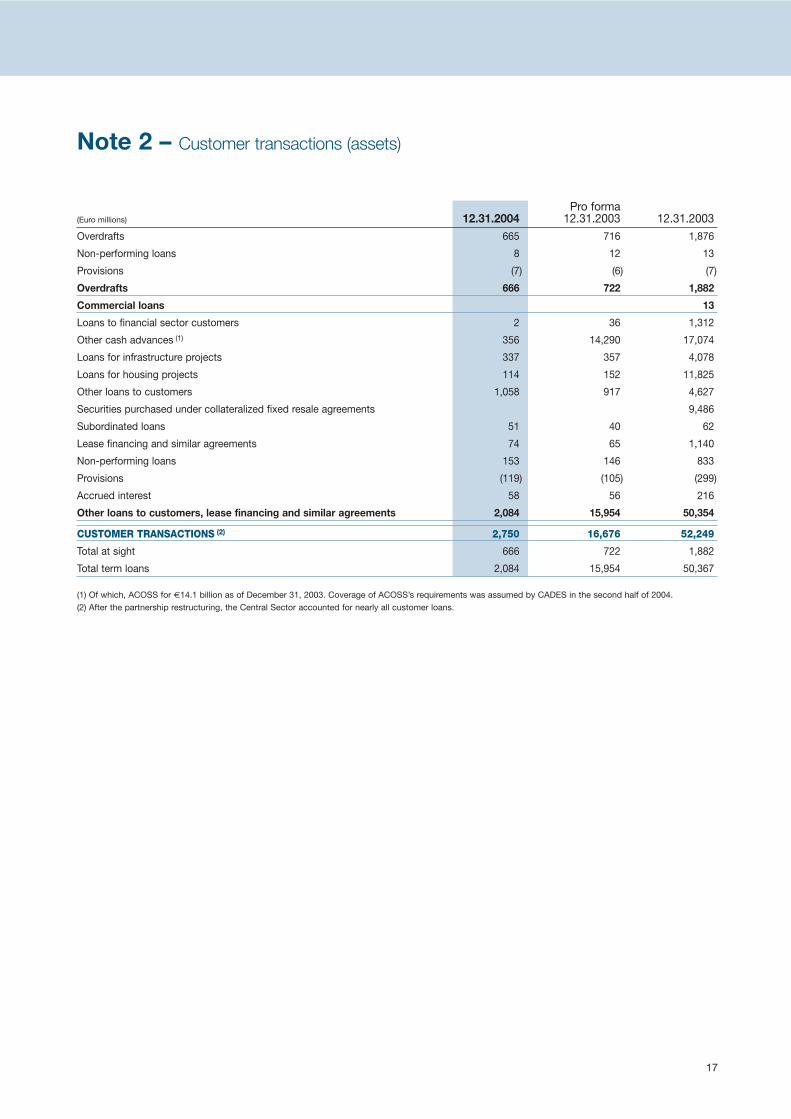

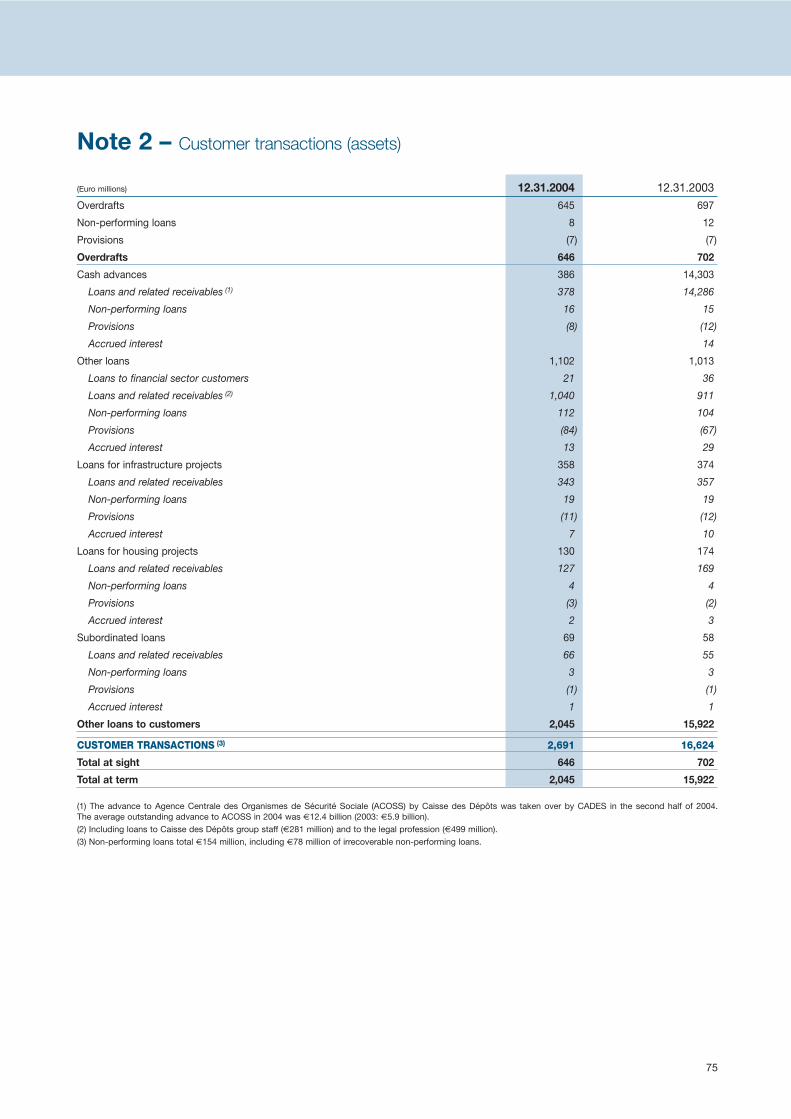

Note 2 – Customer transactions (assets)

Pro forma (Euro millions) 12.31.2004 12.31.2003 12.31.2003Overdrafts 665 716 1,876

Non-performing loans 8 12 13

Provisions (7) (6) (7)

Overdrafts 666 722 1,882

Commercial loans 13

Loans to financial sector customers 2 36 1,312

Other cash advances (1) 356 14,290 17,074

Loans for infrastructure projects 337 357 4,078

Loans for housing projects 114 152 11,825

Other loans to customers 1,058 917 4,627

Securities purchased under collateralized fixed resale agreements 9,486

Subordinated loans 51 40 62

Lease financing and similar agreements 74 65 1,140

Non-performing loans 153 146 833

Provisions (119) (105) (299)

Accrued interest 58 56 216

Other loans to customers, lease financing and similar agreements 2,084 15,954 50,354

CUSTOMER TRANSACTIONS (2) 2,750 16,676 52,249

Total at sight 666 722 1,882

Total term loans 2,084 15,954 50,367

(1) Of which, ACOSS for €14.1 billion as of December 31, 2003. Coverage of ACOSS’s requirements was assumed by CADES in the second half of 2004.(2) After the partnership restructuring, the Central Sector accounted for nearly all customer loans.

18 /// Annual Report 2004 Caisse des Dépôts

CONSOLIDATED FINANCIAL STATEMENTS

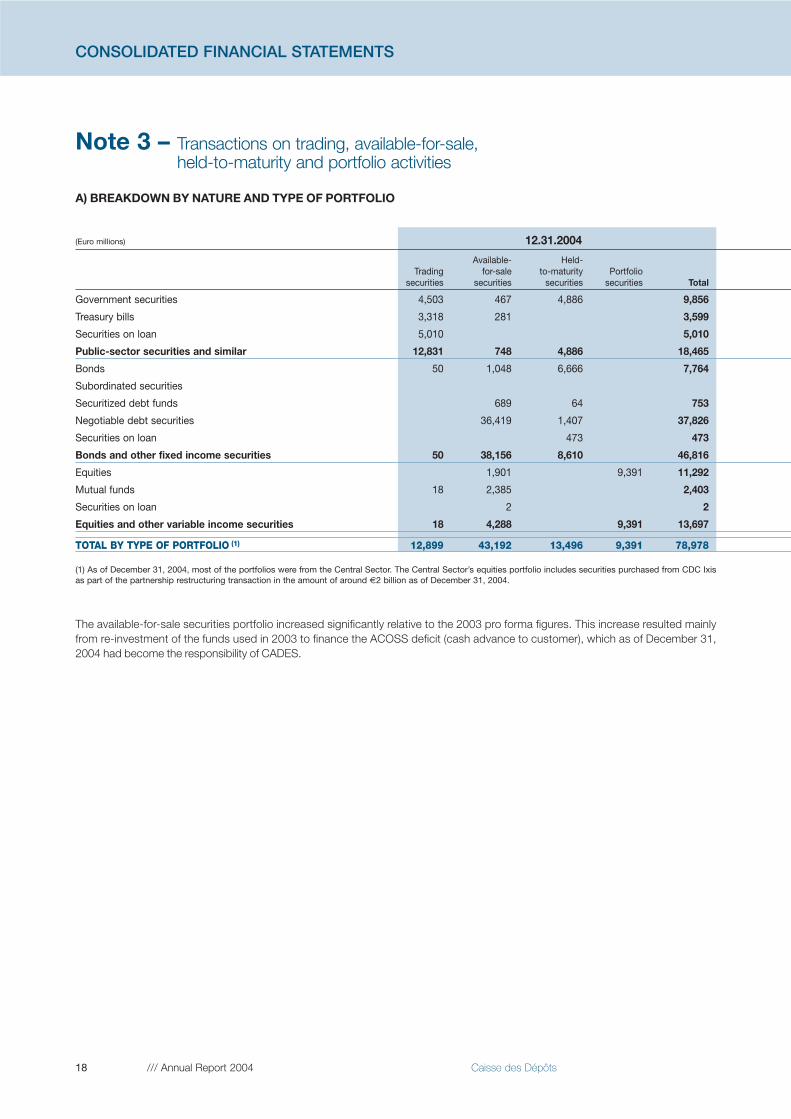

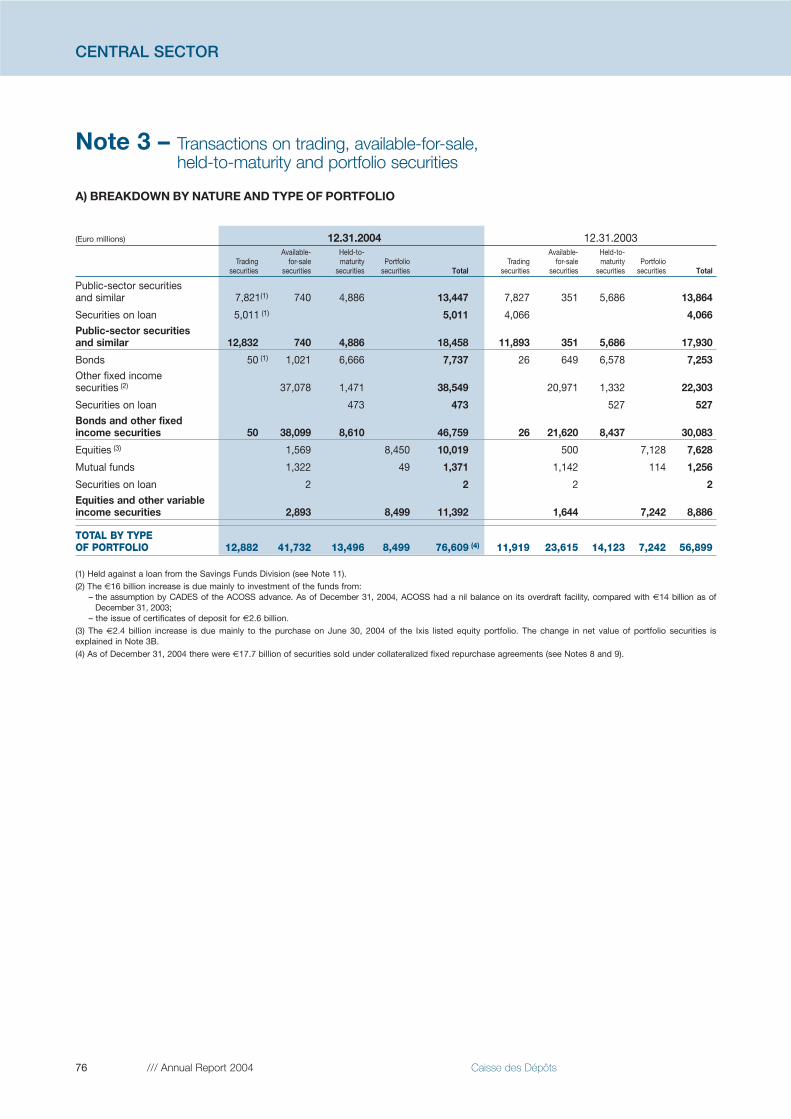

Note 3 – Transactions on trading, available-for-sale, held-to-maturity and portfolio activities

A) BREAKDOWN BY NATURE AND TYPE OF PORTFOLIO

(Euro millions) 12.31.2004

Available- Held-Trading for-sale to-maturity Portfolio

securities securities securities securities Total

Government securities 4,503 467 4,886 9,856

Treasury bills 3,318 281 3,599

Securities on loan 5,010 5,010

Public-sector securities and similar 12,831 748 4,886 18,465

Bonds 50 1,048 6,666 7,764

Subordinated securities

Securitized debt funds 689 64 753

Negotiable debt securities 36,419 1,407 37,826

Securities on loan 473 473

Bonds and other fixed income securities 50 38,156 8,610 46,816

Equities 1,901 9,391 11,292

Mutual funds 18 2,385 2,403

Securities on loan 2 2

Equities and other variable income securities 18 4,288 9,391 13,697

TOTAL BY TYPE OF PORTFOLIO (1) 12,899 43,192 13,496 9,391 78,978

(1) As of December 31, 2004, most of the portfolios were from the Central Sector. The Central Sector’s equities portfolio includes securities purchased from CDC Ixisas part of the partnership restructuring transaction in the amount of around €2 billion as of December 31, 2004.

The available-for-sale securities portfolio increased significantly relative to the 2003 pro forma figures. This increase resulted mainlyfrom re-investment of the funds used in 2003 to finance the ACOSS deficit (cash advance to customer), which as of December 31,2004 had become the responsibility of CADES.

19

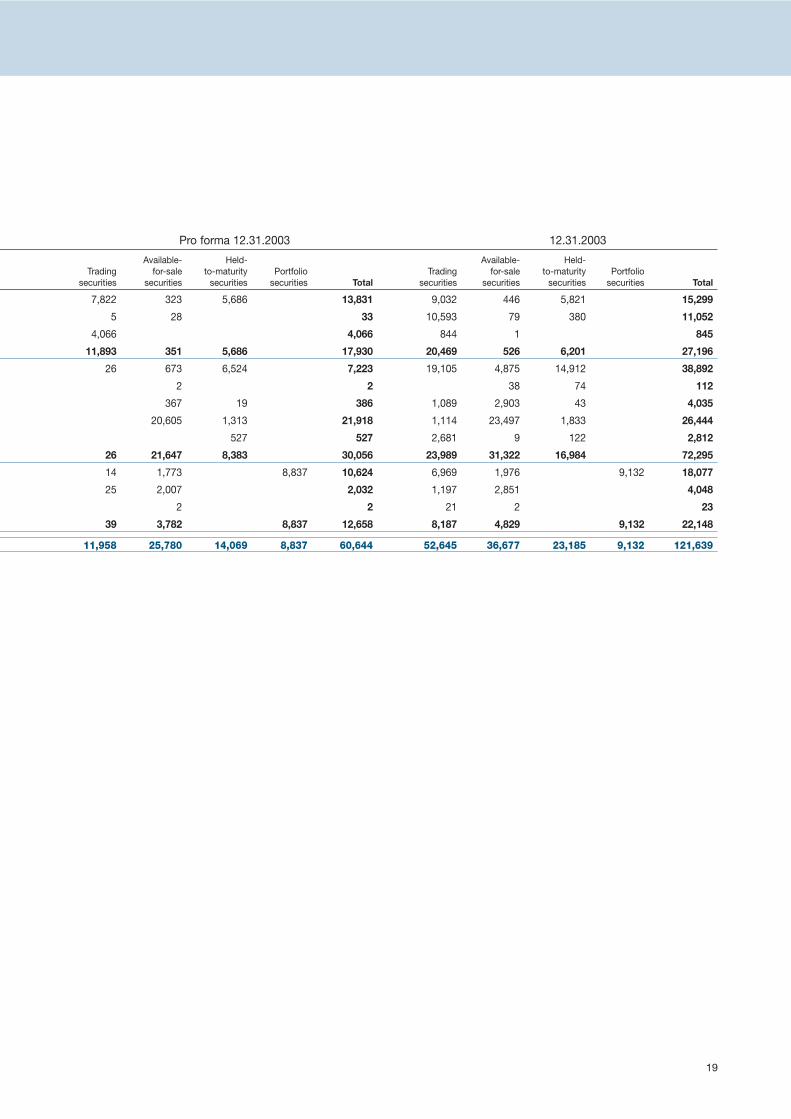

Pro forma 12.31.2003 12.31.2003

Available- Held- Available- Held-Trading for-sale to-maturity Portfolio Trading for-sale to-maturity Portfolio

securities securities securities securities Total securities securities securities securities Total

7,822 323 5,686 13,831 9,032 446 5,821 15,299

5 28 33 10,593 79 380 11,052

4,066 4,066 844 1 845

11,893 351 5,686 17,930 20,469 526 6,201 27,196

26 673 6,524 7,223 19,105 4,875 14,912 38,892

2 2 38 74 112

367 19 386 1,089 2,903 43 4,035

20,605 1,313 21,918 1,114 23,497 1,833 26,444

527 527 2,681 9 122 2,812

26 21,647 8,383 30,056 23,989 31,322 16,984 72,295

14 1,773 8,837 10,624 6,969 1,976 9,132 18,077

25 2,007 2,032 1,197 2,851 4,048

2 2 21 2 23

39 3,782 8,837 12,658 8,187 4,829 9,132 22,148

11,958 25,780 14,069 8,837 60,644 52,645 36,677 23,185 9,132 121,639

20 /// Annual Report 2004 Caisse des Dépôts

CONSOLIDATED FINANCIAL STATEMENTS

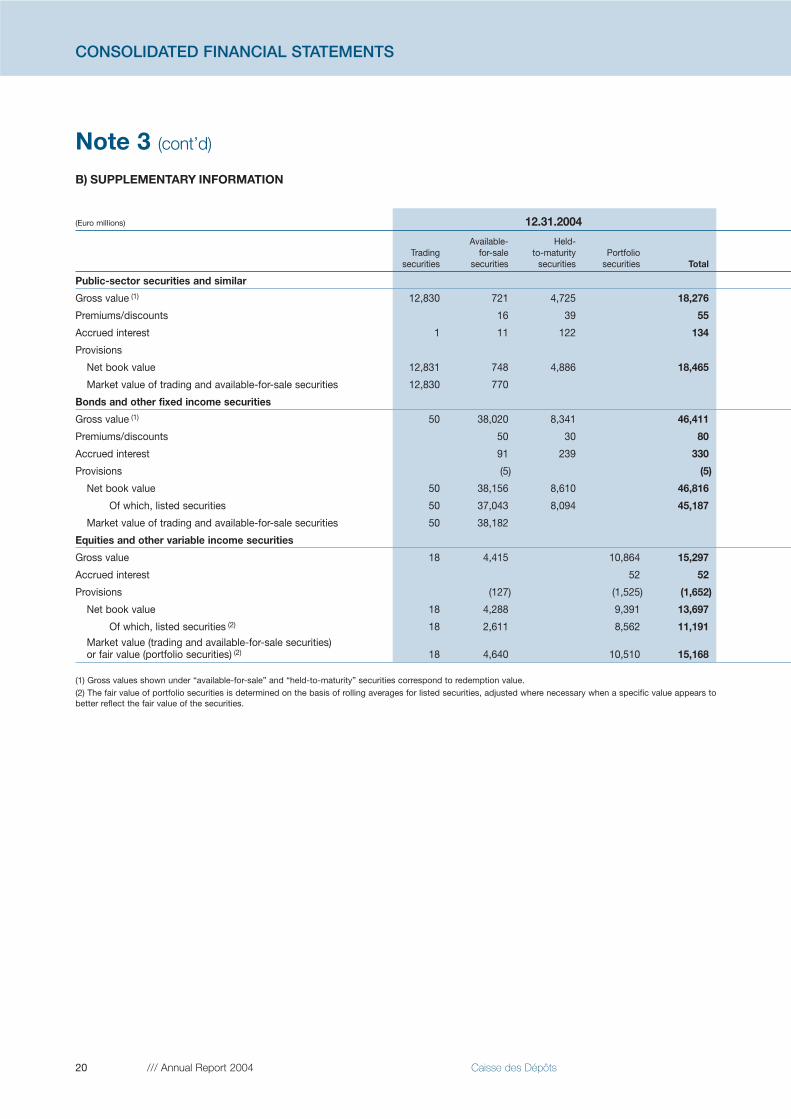

Note 3 (cont’d)

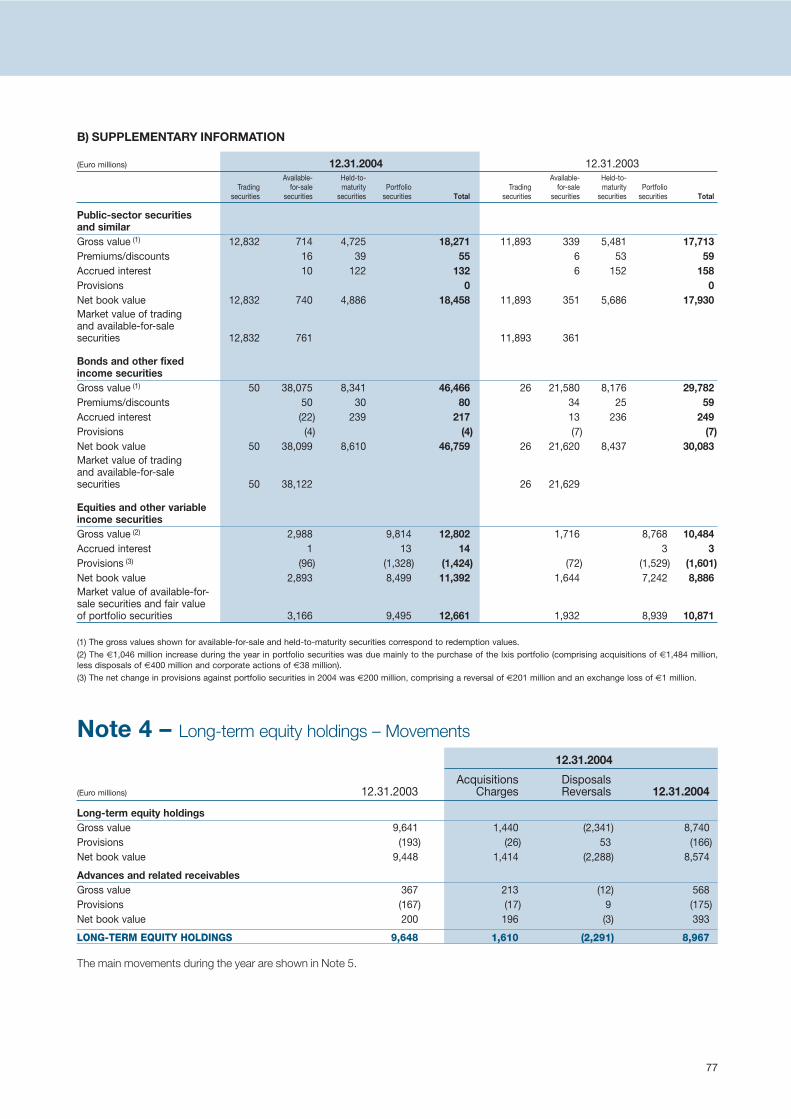

B) SUPPLEMENTARY INFORMATION

(Euro millions) 12.31.2004

Available- Held-Trading for-sale to-maturity Portfolio

securities securities securities securities Total

Public-sector securities and similar

Gross value (1) 12,830 721 4,725 18,276

Premiums/discounts 16 39 55

Accrued interest 1 11 122 134

Provisions

Net book value 12,831 748 4,886 18,465

Market value of trading and available-for-sale securities 12,830 770

Bonds and other fixed income securities

Gross value (1) 50 38,020 8,341 46,411

Premiums/discounts 50 30 80

Accrued interest 91 239 330

Provisions (5) (5)

Net book value 50 38,156 8,610 46,816

Of which, listed securities 50 37,043 8,094 45,187

Market value of trading and available-for-sale securities 50 38,182

Equities and other variable income securities

Gross value 18 4,415 10,864 15,297

Accrued interest 52 52

Provisions (127) (1,525) (1,652)

Net book value 18 4,288 9,391 13,697

Of which, listed securities (2) 18 2,611 8,562 11,191Market value (trading and available-for-sale securities) or fair value (portfolio securities) (2) 18 4,640 10,510 15,168

(1) Gross values shown under “available-for-sale” and “held-to-maturity” securities correspond to redemption value.(2) The fair value of portfolio securities is determined on the basis of rolling averages for listed securities, adjusted where necessary when a specific value appears tobetter reflect the fair value of the securities.

21

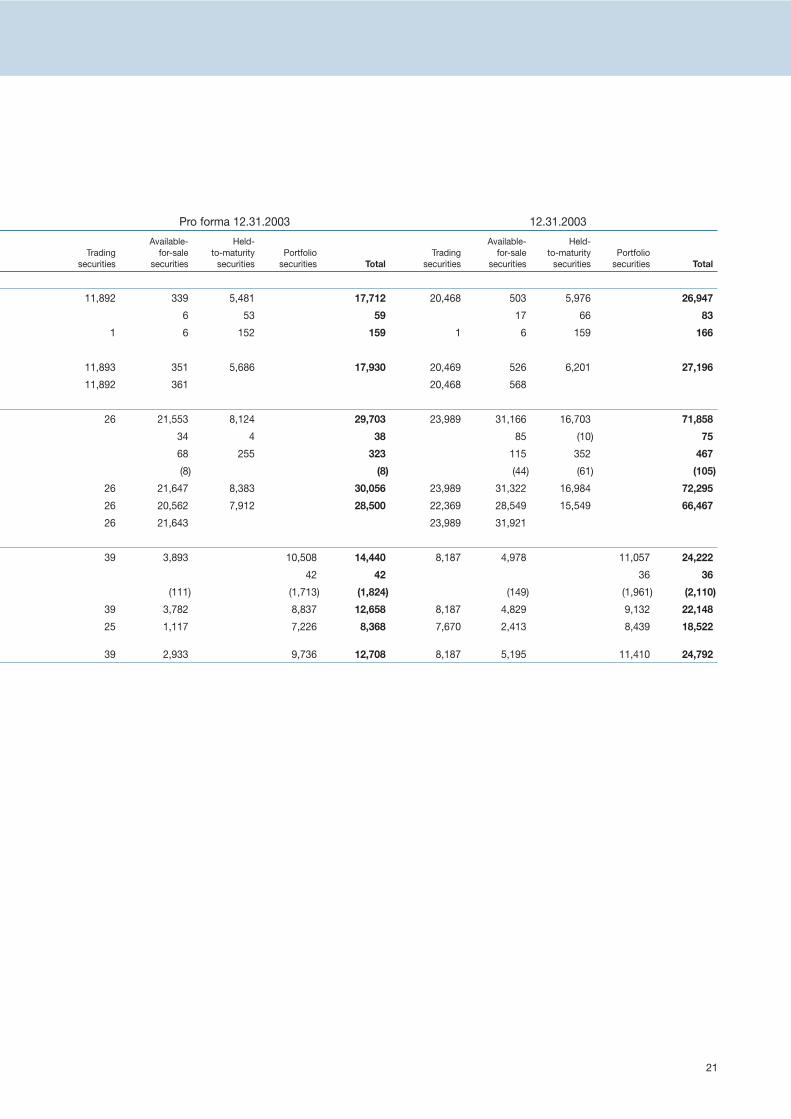

Pro forma 12.31.2003 12.31.2003

Available- Held- Available- Held-Trading for-sale to-maturity Portfolio Trading for-sale to-maturity Portfolio

securities securities securities securities Total securities securities securities securities Total

11,892 339 5,481 17,712 20,468 503 5,976 26,947

6 53 59 17 66 83

1 6 152 159 1 6 159 166

11,893 351 5,686 17,930 20,469 526 6,201 27,196

11,892 361 20,468 568

26 21,553 8,124 29,703 23,989 31,166 16,703 71,858

34 4 38 85 (10) 75

68 255 323 115 352 467

(8) (8) (44) (61) (105)

26 21,647 8,383 30,056 23,989 31,322 16,984 72,295

26 20,562 7,912 28,500 22,369 28,549 15,549 66,467

26 21,643 23,989 31,921

39 3,893 10,508 14,440 8,187 4,978 11,057 24,222

42 42 36 36

(111) (1,713) (1,824) (149) (1,961) (2,110)

39 3,782 8,837 12,658 8,187 4,829 9,132 22,148

25 1,117 7,226 8,368 7,670 2,413 8,439 18,522

39 2,933 9,736 12,708 8,187 5,195 11,410 24,792

22 /// Annual Report 2004 Caisse des Dépôts

CONSOLIDATED FINANCIAL STATEMENTS

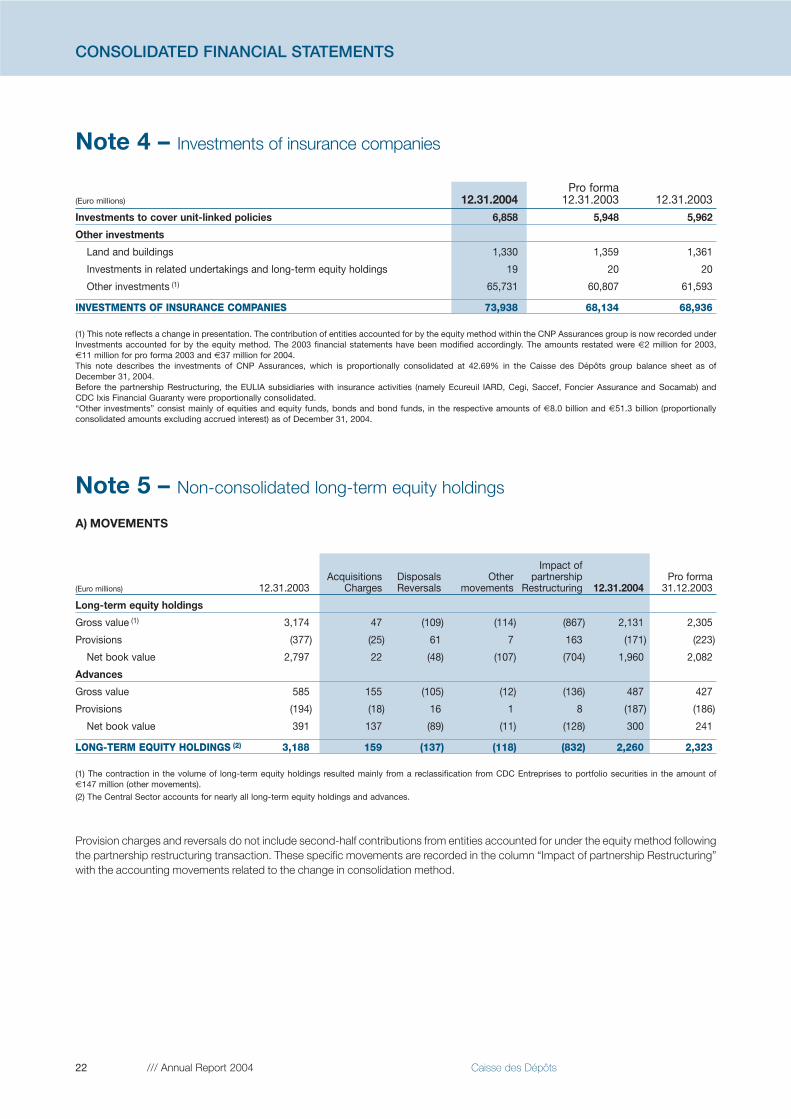

Note 4 – Investments of insurance companies

Pro forma (Euro millions) 12.31.2004 12.31.2003 12.31.2003Investments to cover unit-linked policies 6,858 5,948 5,962

Other investments

Land and buildings 1,330 1,359 1,361

Investments in related undertakings and long-term equity holdings 19 20 20

Other investments (1) 65,731 60,807 61,593

INVESTMENTS OF INSURANCE COMPANIES 73,938 68,134 68,936

(1) This note reflects a change in presentation. The contribution of entities accounted for by the equity method within the CNP Assurances group is now recorded underInvestments accounted for by the equity method. The 2003 financial statements have been modified accordingly. The amounts restated were €2 million for 2003, €11 million for pro forma 2003 and €37 million for 2004. This note describes the investments of CNP Assurances, which is proportionally consolidated at 42.69% in the Caisse des Dépôts group balance sheet as of December 31, 2004. Before the partnership Restructuring, the EULIA subsidiaries with insurance activities (namely Ecureuil IARD, Cegi, Saccef, Foncier Assurance and Socamab) and CDC Ixis Financial Guaranty were proportionally consolidated.“Other investments” consist mainly of equities and equity funds, bonds and bond funds, in the respective amounts of €8.0 billion and €51.3 billion (proportionallyconsolidated amounts excluding accrued interest) as of December 31, 2004.

Note 5 – Non-consolidated long-term equity holdings

A) MOVEMENTS

Impact of Acquisitions Disposals Other partnership Pro forma

(Euro millions) 12.31.2003 Charges Reversals movements Restructuring 12.31.2004 31.12.2003

Long-term equity holdings

Gross value (1) 3,174 47 (109) (114) (867) 2,131 2,305

Provisions (377) (25) 61 7 163 (171) (223)

Net book value 2,797 22 (48) (107) (704) 1,960 2,082

Advances

Gross value 585 155 (105) (12) (136) 487 427

Provisions (194) (18) 16 1 8 (187) (186)

Net book value 391 137 (89) (11) (128) 300 241

LONG-TERM EQUITY HOLDINGS (2) 3,188 159 (137) (118) (832) 2,260 2,323

(1) The contraction in the volume of long-term equity holdings resulted mainly from a reclassification from CDC Entreprises to portfolio securities in the amount of €147 million (other movements).(2) The Central Sector accounts for nearly all long-term equity holdings and advances.

Provision charges and reversals do not include second-half contributions from entities accounted for under the equity method followingthe partnership restructuring transaction. These specific movements are recorded in the column “Impact of partnership Restructuring”with the accounting movements related to the change in consolidation method.

23

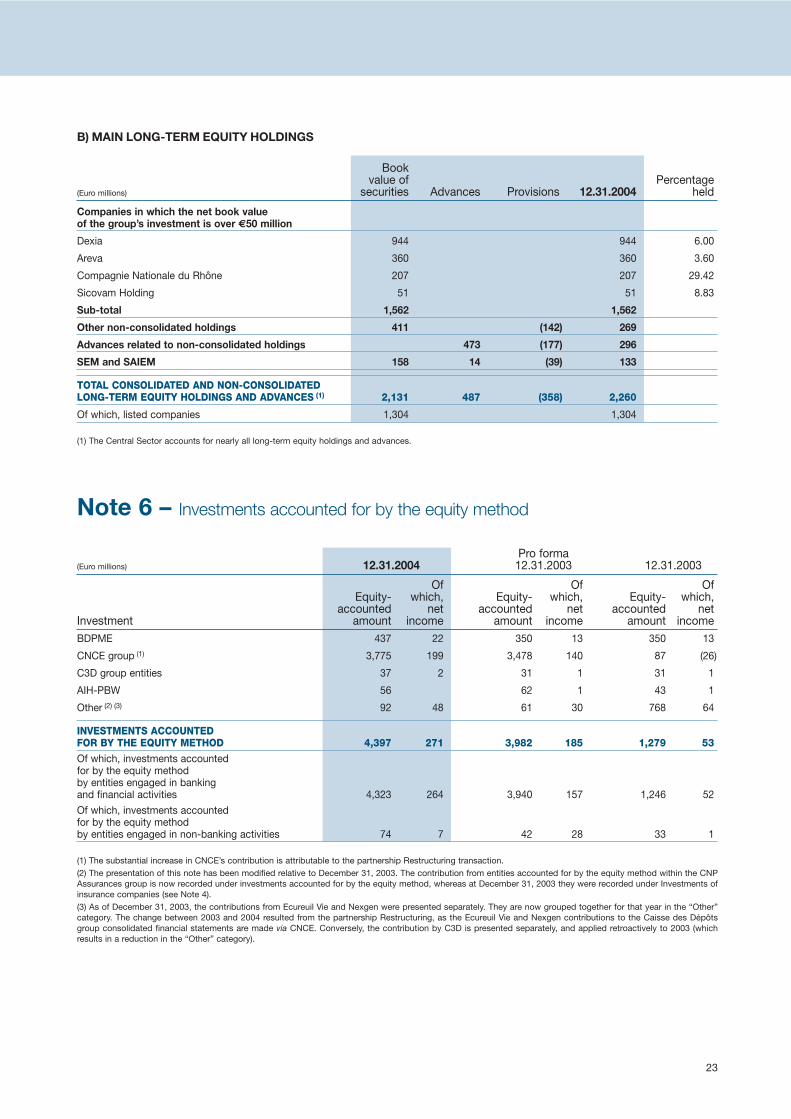

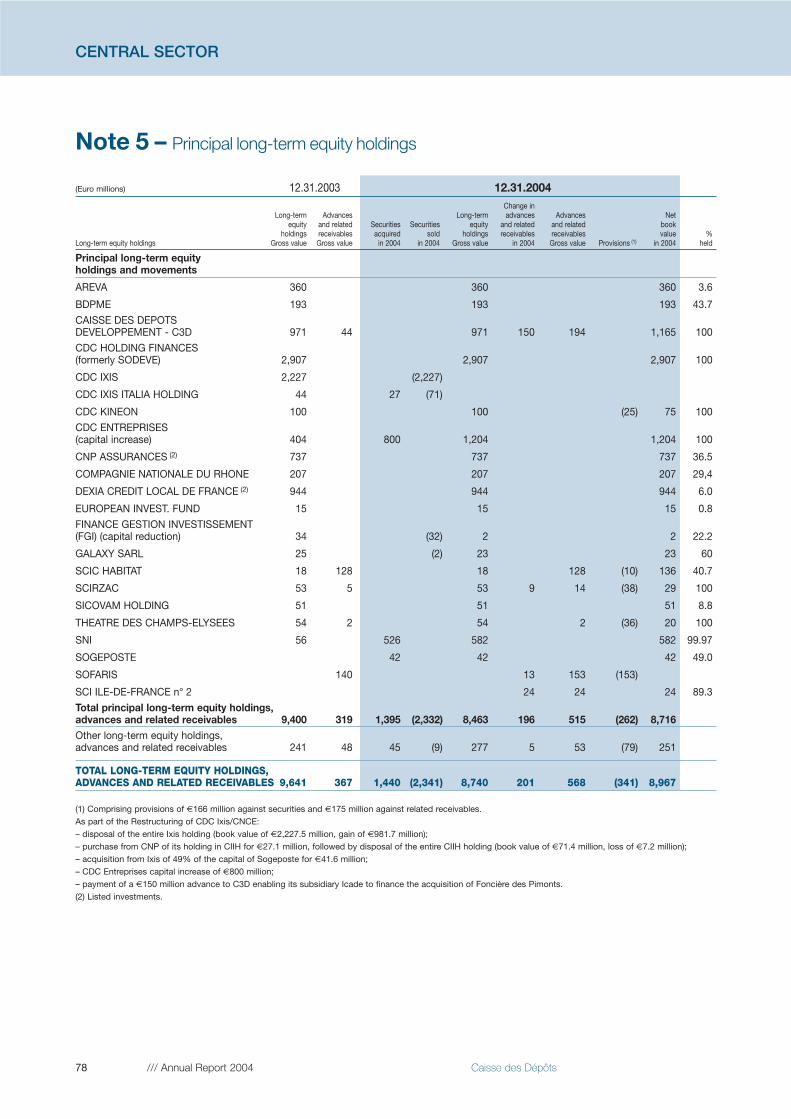

B) MAIN LONG-TERM EQUITY HOLDINGS

Bookvalue of Percentage

(Euro millions) securities Advances Provisions 12.31.2004 held

Companies in which the net book value of the group’s investment is over €50 million

Dexia 944 944 6.00

Areva 360 360 3.60

Compagnie Nationale du Rhône 207 207 29.42

Sicovam Holding 51 51 8.83

Sub-total 1,562 1,562

Other non-consolidated holdings 411 (142) 269

Advances related to non-consolidated holdings 473 (177) 296

SEM and SAIEM 158 14 (39) 133

TOTAL CONSOLIDATED AND NON-CONSOLIDATED LONG-TERM EQUITY HOLDINGS AND ADVANCES (1) 2,131 487 (358) 2,260

Of which, listed companies 1,304 1,304

(1) The Central Sector accounts for nearly all long-term equity holdings and advances.

Note 6 – Investments accounted for by the equity method

Pro forma(Euro millions) 12.31.2004 12.31.2003 12.31.2003

Of Of OfEquity- which, Equity- which, Equity- which,

accounted net accounted net accounted net Investment amount income amount income amount incomeBDPME 437 22 350 13 350 13

CNCE group (1) 3,775 199 3,478 140 87 (26)

C3D group entities 37 2 31 1 31 1

AIH-PBW 56 62 1 43 1

Other (2) (3) 92 48 61 30 768 64

INVESTMENTS ACCOUNTED FOR BY THE EQUITY METHOD 4,397 271 3,982 185 1,279 53Of which, investments accounted for by the equity method by entities engaged in banking and financial activities 4,323 264 3,940 157 1,246 52

Of which, investments accounted for by the equity method by entities engaged in non-banking activities 74 7 42 28 33 1

(1) The substantial increase in CNCE’s contribution is attributable to the partnership Restructuring transaction.(2) The presentation of this note has been modified relative to December 31, 2003. The contribution from entities accounted for by the equity method within the CNPAssurances group is now recorded under investments accounted for by the equity method, whereas at December 31, 2003 they were recorded under Investments ofinsurance companies (see Note 4). (3) As of December 31, 2003, the contributions from Ecureuil Vie and Nexgen were presented separately. They are now grouped together for that year in the “Other”category. The change between 2003 and 2004 resulted from the partnership Restructuring, as the Ecureuil Vie and Nexgen contributions to the Caisse des Dépôtsgroup consolidated financial statements are made via CNCE. Conversely, the contribution by C3D is presented separately, and applied retroactively to 2003 (whichresults in a reduction in the “Other” category).

24 /// Annual Report 2004 Caisse des Dépôts

CONSOLIDATED FINANCIAL STATEMENTS

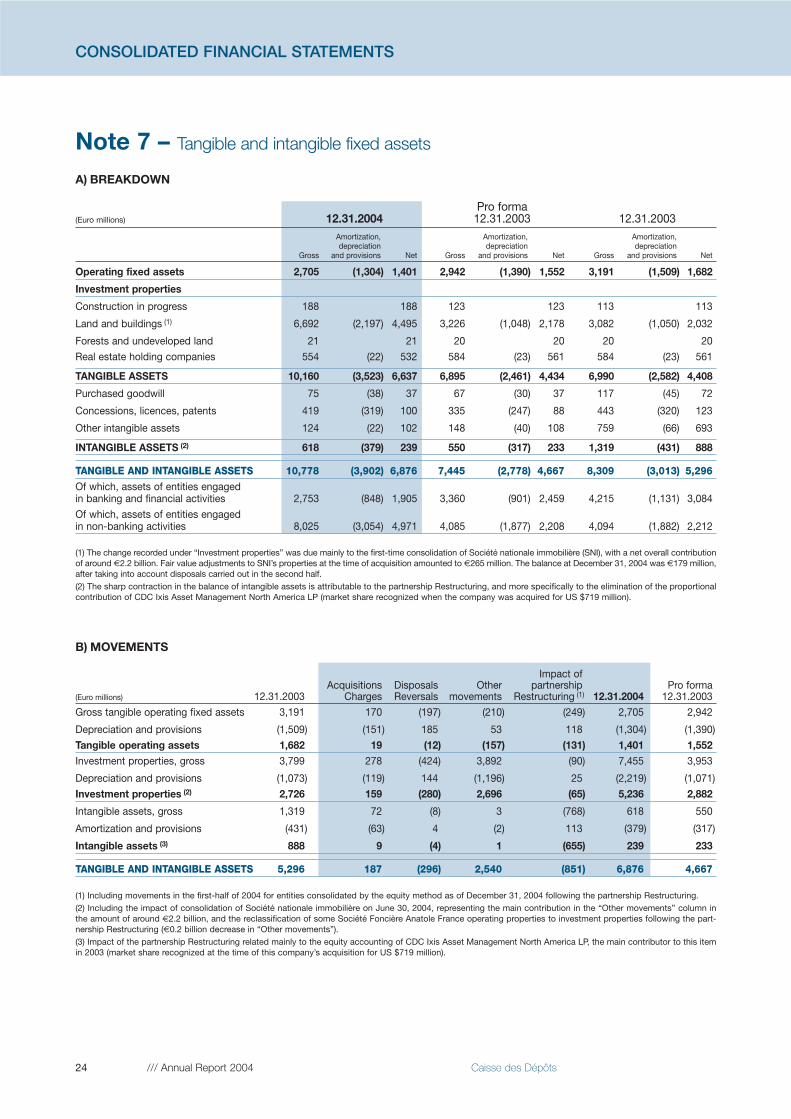

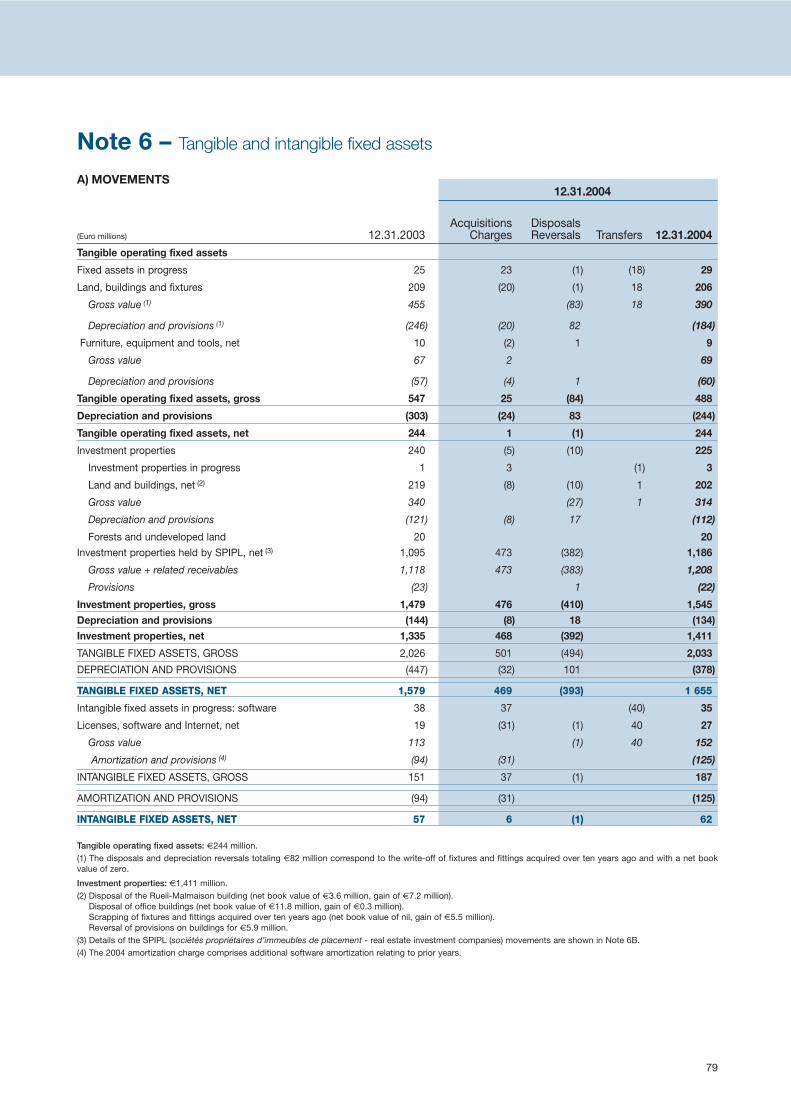

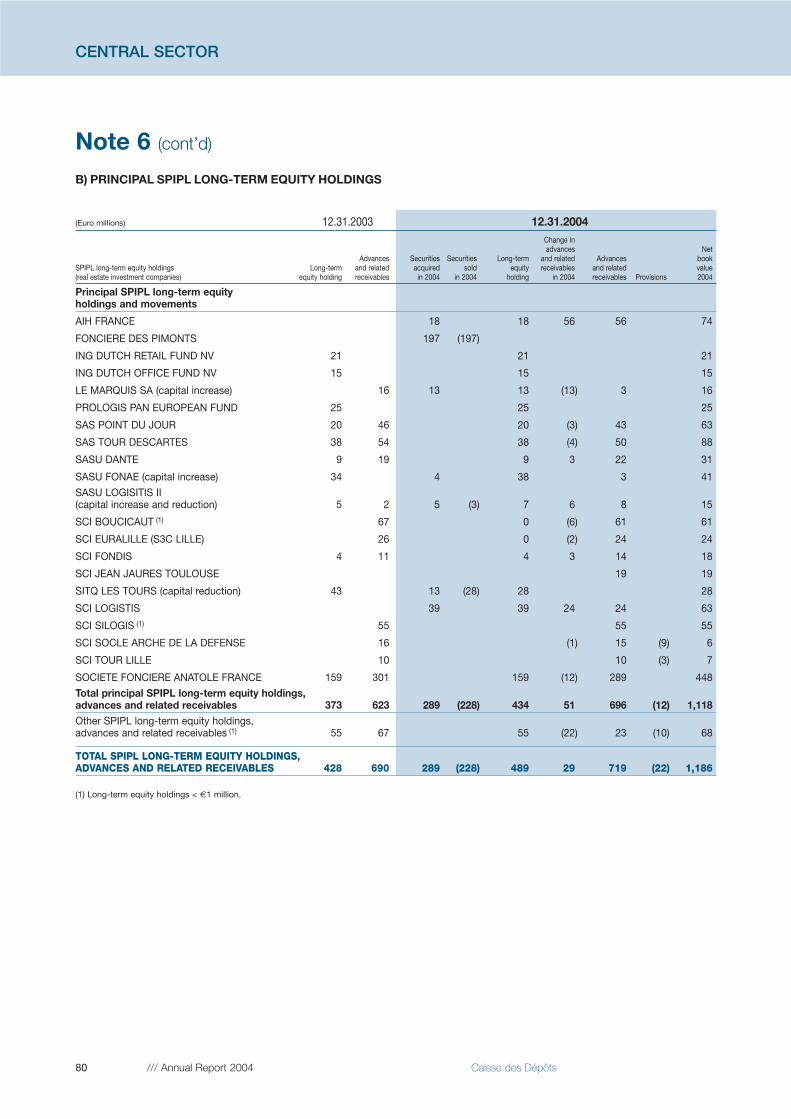

Note 7 – Tangible and intangible fixed assets

A) BREAKDOWN

Pro forma (Euro millions) 12.31.2004 12.31.2003 12.31.2003

Amortization, Amortization, Amortization,depreciation depreciation depreciation

Gross and provisions Net Gross and provisions Net Gross and provisions Net

Operating fixed assets 2,705 (1,304) 1,401 2,942 (1,390) 1,552 3,191 (1,509) 1,682

Investment properties

Construction in progress 188 188 123 123 113 113

Land and buildings (1) 6,692 (2,197) 4,495 3,226 (1,048) 2,178 3,082 (1,050) 2,032

Forests and undeveloped land 21 21 20 20 20 20

Real estate holding companies 554 (22) 532 584 (23) 561 584 (23) 561

TANGIBLE ASSETS 10,160 (3,523) 6,637 6,895 (2,461) 4,434 6,990 (2,582) 4,408

Purchased goodwill 75 (38) 37 67 (30) 37 117 (45) 72

Concessions, licences, patents 419 (319) 100 335 (247) 88 443 (320) 123

Other intangible assets 124 (22) 102 148 (40) 108 759 (66) 693

INTANGIBLE ASSETS (2) 618 (379) 239 550 (317) 233 1,319 (431) 888

TANGIBLE AND INTANGIBLE ASSETS 10,778 (3,902) 6,876 7,445 (2,778) 4,667 8,309 (3,013) 5,296Of which, assets of entities engaged in banking and financial activities 2,753 (848) 1,905 3,360 (901) 2,459 4,215 (1,131) 3,084

Of which, assets of entities engaged in non-banking activities 8,025 (3,054) 4,971 4,085 (1,877) 2,208 4,094 (1,882) 2,212

(1) The change recorded under “Investment properties” was due mainly to the first-time consolidation of Société nationale immobilière (SNI), with a net overall contributionof around €2.2 billion. Fair value adjustments to SNI’s properties at the time of acquisition amounted to €265 million. The balance at December 31, 2004 was €179 million,after taking into account disposals carried out in the second half.(2) The sharp contraction in the balance of intangible assets is attributable to the partnership Restructuring, and more specifically to the elimination of the proportionalcontribution of CDC Ixis Asset Management North America LP (market share recognized when the company was acquired for US $719 million).

B) MOVEMENTS

Impact ofAcquisitions Disposals Other partnership Pro forma

(Euro millions) 12.31.2003 Charges Reversals movements Restructuring (1) 12.31.2004 12.31.2003

Gross tangible operating fixed assets 3,191 170 (197) (210) (249) 2,705 2,942

Depreciation and provisions (1,509) (151) 185 53 118 (1,304) (1,390)

Tangible operating assets 1,682 19 (12) (157) (131) 1,401 1,552Investment properties, gross 3,799 278 (424) 3,892 (90) 7,455 3,953

Depreciation and provisions (1,073) (119) 144 (1,196) 25 (2,219) (1,071)

Investment properties (2) 2,726 159 (280) 2,696 (65) 5,236 2,882

Intangible assets, gross 1,319 72 (8) 3 (768) 618 550

Amortization and provisions (431) (63) 4 (2) 113 (379) (317)

Intangible assets (3) 888 9 (4) 1 (655) 239 233

TANGIBLE AND INTANGIBLE ASSETS 5,296 187 (296) 2,540 (851) 6,876 4,667

(1) Including movements in the first-half of 2004 for entities consolidated by the equity method as of December 31, 2004 following the partnership Restructuring.(2) Including the impact of consolidation of Société nationale immobilière on June 30, 2004, representing the main contribution in the “Other movements” column inthe amount of around €2.2 billion, and the reclassification of some Société Foncière Anatole France operating properties to investment properties following the part-nership Restructuring (€0.2 billion decrease in “Other movements”).(3) Impact of the partnership Restructuring related mainly to the equity accounting of CDC Ixis Asset Management North America LP, the main contributor to this itemin 2003 (market share recognized at the time of this company’s acquisition for US $719 million).

25

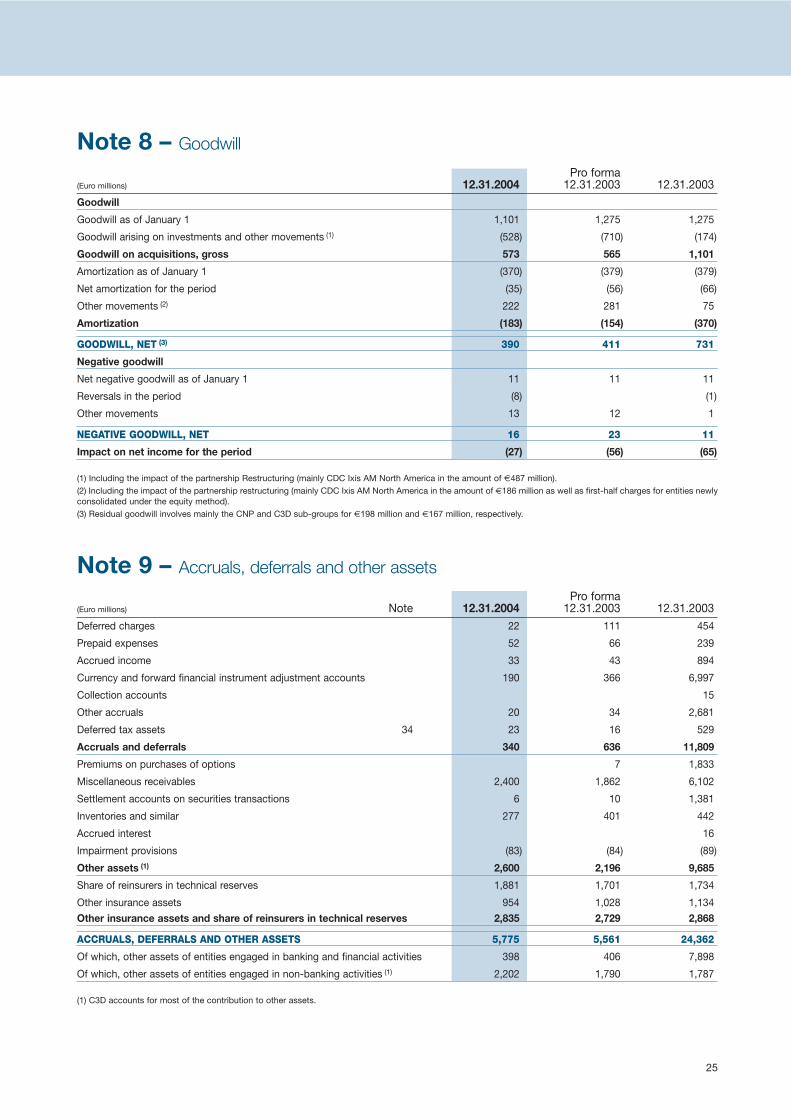

Note 8 – Goodwill

Pro forma (Euro millions) 12.31.2004 12.31.2003 12.31.2003Goodwill

Goodwill as of January 1 1,101 1,275 1,275

Goodwill arising on investments and other movements (1) (528) (710) (174)

Goodwill on acquisitions, gross 573 565 1,101

Amortization as of January 1 (370) (379) (379)

Net amortization for the period (35) (56) (66)

Other movements (2) 222 281 75

Amortization (183) (154) (370)

GOODWILL, NET (3) 390 411 731

Negative goodwill

Net negative goodwill as of January 1 11 11 11

Reversals in the period (8) (1)

Other movements 13 12 1

NEGATIVE GOODWILL, NET 16 23 11

Impact on net income for the period (27) (56) (65)

(1) Including the impact of the partnership Restructuring (mainly CDC Ixis AM North America in the amount of €487 million).(2) Including the impact of the partnership restructuring (mainly CDC Ixis AM North America in the amount of €186 million as well as first-half charges for entities newlyconsolidated under the equity method).(3) Residual goodwill involves mainly the CNP and C3D sub-groups for €198 million and €167 million, respectively.

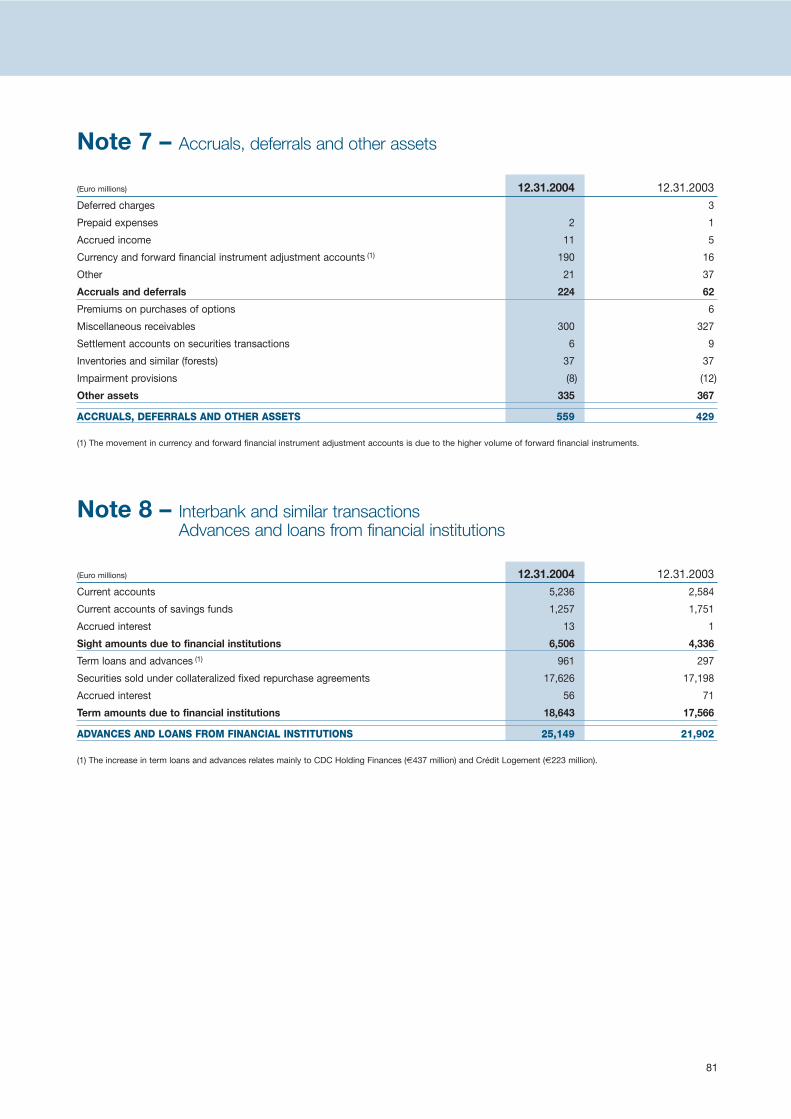

Note 9 – Accruals, deferrals and other assets

Pro forma (Euro millions) Note 12.31.2004 12.31.2003 12.31.2003Deferred charges 22 111 454

Prepaid expenses 52 66 239

Accrued income 33 43 894

Currency and forward financial instrument adjustment accounts 190 366 6,997

Collection accounts 15

Other accruals 20 34 2,681

Deferred tax assets 34 23 16 529

Accruals and deferrals 340 636 11,809

Premiums on purchases of options 7 1,833

Miscellaneous receivables 2,400 1,862 6,102

Settlement accounts on securities transactions 6 10 1,381

Inventories and similar 277 401 442

Accrued interest 16

Impairment provisions (83) (84) (89)

Other assets (1) 2,600 2,196 9,685

Share of reinsurers in technical reserves 1,881 1,701 1,734

Other insurance assets 954 1,028 1,134

Other insurance assets and share of reinsurers in technical reserves 2,835 2,729 2,868

ACCRUALS, DEFERRALS AND OTHER ASSETS 5,775 5,561 24,362

Of which, other assets of entities engaged in banking and financial activities 398 406 7,898

Of which, other assets of entities engaged in non-banking activities (1) 2,202 1,790 1,787

(1) C3D accounts for most of the contribution to other assets.

26 /// Annual Report 2004 Caisse des Dépôts

CONSOLIDATED FINANCIAL STATEMENTS

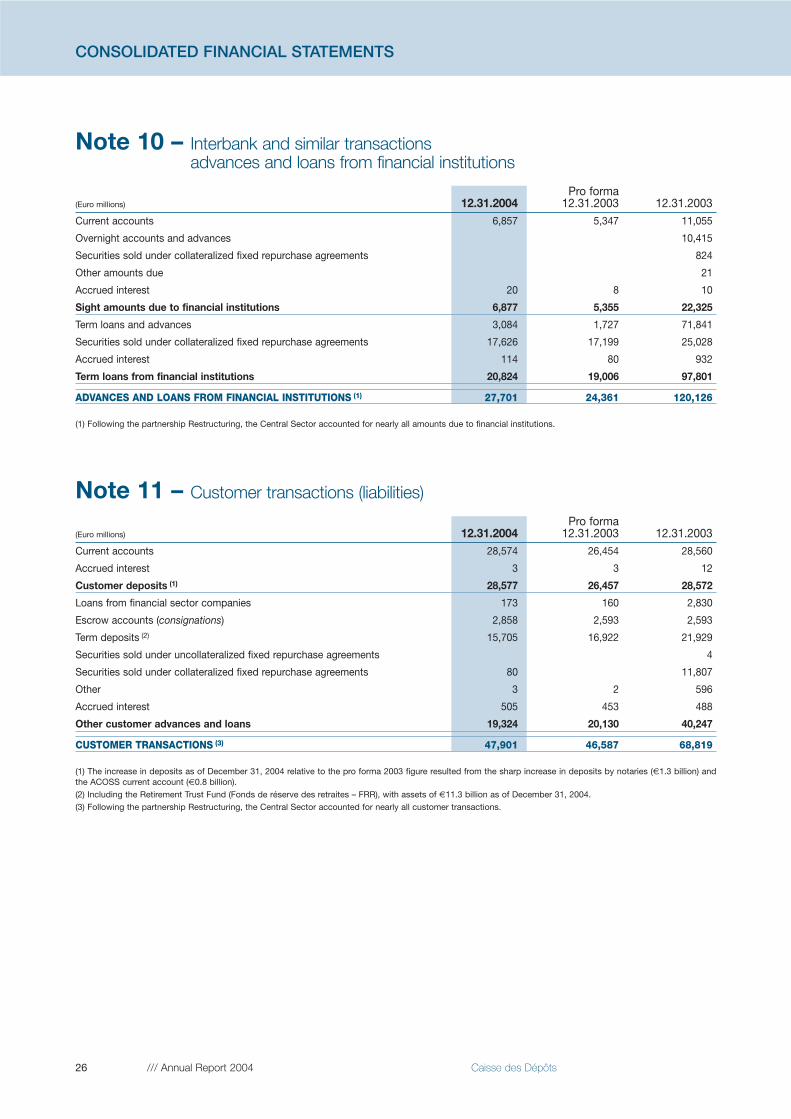

Note 10 – Interbank and similar transactionsadvances and loans from financial institutions

Pro forma (Euro millions) 12.31.2004 12.31.2003 12.31.2003Current accounts 6,857 5,347 11,055

Overnight accounts and advances 10,415

Securities sold under collateralized fixed repurchase agreements 824

Other amounts due 21

Accrued interest 20 8 10

Sight amounts due to financial institutions 6,877 5,355 22,325

Term loans and advances 3,084 1,727 71,841

Securities sold under collateralized fixed repurchase agreements 17,626 17,199 25,028

Accrued interest 114 80 932

Term loans from financial institutions 20,824 19,006 97,801

ADVANCES AND LOANS FROM FINANCIAL INSTITUTIONS (1) 27,701 24,361 120,126

(1) Following the partnership Restructuring, the Central Sector accounted for nearly all amounts due to financial institutions.

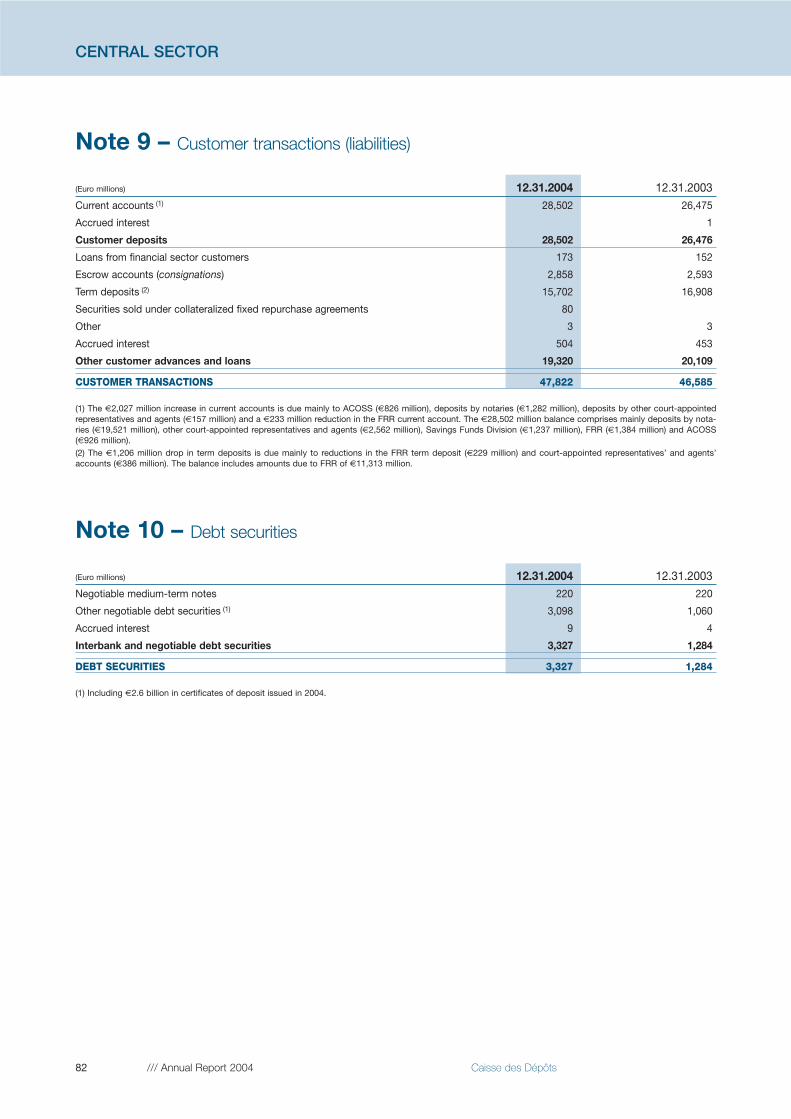

Note 11 – Customer transactions (liabilities)

Pro forma (Euro millions) 12.31.2004 12.31.2003 12.31.2003Current accounts 28,574 26,454 28,560

Accrued interest 3 3 12

Customer deposits (1) 28,577 26,457 28,572

Loans from financial sector companies 173 160 2,830

Escrow accounts (consignations) 2,858 2,593 2,593

Term deposits (2) 15,705 16,922 21,929

Securities sold under uncollateralized fixed repurchase agreements 4

Securities sold under collateralized fixed repurchase agreements 80 11,807

Other 3 2 596

Accrued interest 505 453 488

Other customer advances and loans 19,324 20,130 40,247

CUSTOMER TRANSACTIONS (3) 47,901 46,587 68,819

(1) The increase in deposits as of December 31, 2004 relative to the pro forma 2003 figure resulted from the sharp increase in deposits by notaries (€1.3 billion) andthe ACOSS current account (€0.8 billion).(2) Including the Retirement Trust Fund (Fonds de réserve des retraites – FRR), with assets of €11.3 billion as of December 31, 2004.(3) Following the partnership Restructuring, the Central Sector accounted for nearly all customer transactions.

27

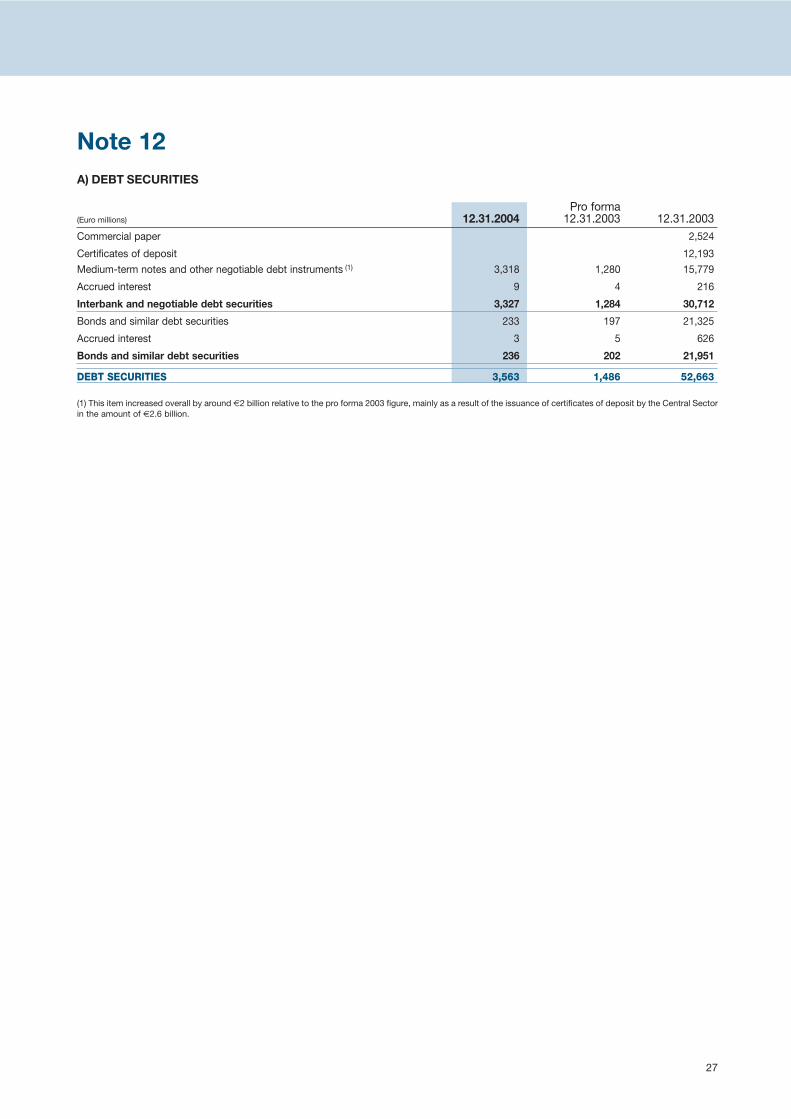

Note 12 A) DEBT SECURITIES

Pro forma (Euro millions) 12.31.2004 12.31.2003 12.31.2003Commercial paper 2,524

Certificates of deposit 12,193

Medium-term notes and other negotiable debt instruments (1) 3,318 1,280 15,779

Accrued interest 9 4 216

Interbank and negotiable debt securities 3,327 1,284 30,712

Bonds and similar debt securities 233 197 21,325

Accrued interest 3 5 626

Bonds and similar debt securities 236 202 21,951

DEBT SECURITIES 3,563 1,486 52,663

(1) This item increased overall by around €2 billion relative to the pro forma 2003 figure, mainly as a result of the issuance of certificates of deposit by the Central Sectorin the amount of €2.6 billion.

28 /// Annual Report 2004 Caisse des Dépôts

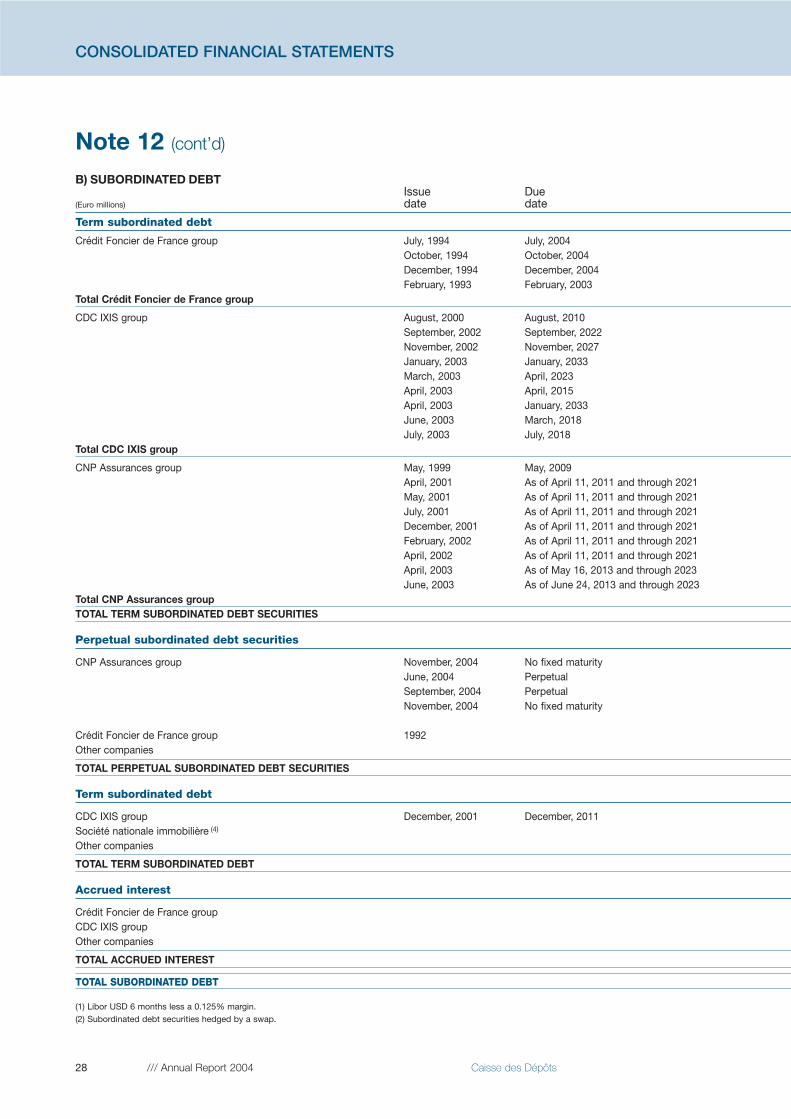

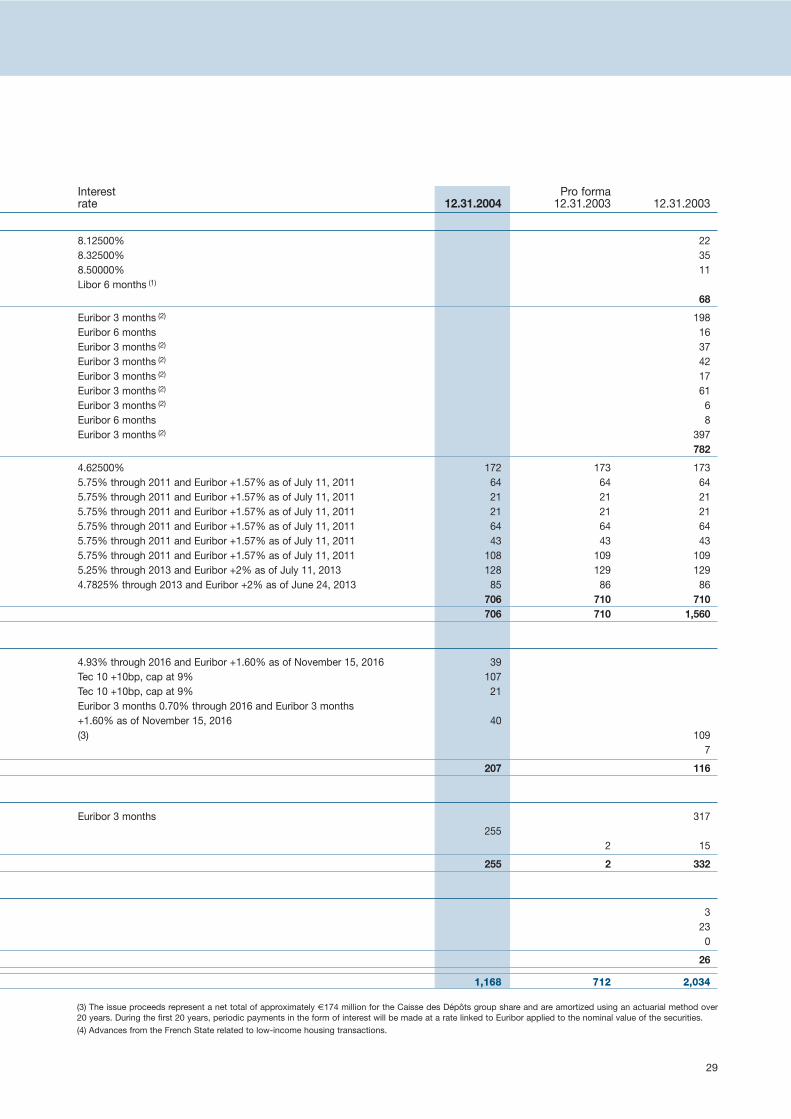

Note 12 (cont’d)

B) SUBORDINATED DEBTIssue Due

(Euro millions) date date

Term subordinated debt

Crédit Foncier de France group July, 1994 July, 2004October, 1994 October, 2004December, 1994 December, 2004February, 1993 February, 2003

Total Crédit Foncier de France group

CDC IXIS group August, 2000 August, 2010September, 2002 September, 2022November, 2002 November, 2027January, 2003 January, 2033March, 2003 April, 2023April, 2003 April, 2015April, 2003 January, 2033June, 2003 March, 2018July, 2003 July, 2018

Total CDC IXIS group