Embed Size (px)

Citation preview

8/3/2019 Siddhartha Final 2007

http://slidepdf.com/reader/full/siddhartha-final-2007 1/29

Automobile (Four Wheeler) Subject: - Statistics

H.L. Institute of

Commerce

Section: - 2nd

Group: - 201-210

8/3/2019 Siddhartha Final 2007

http://slidepdf.com/reader/full/siddhartha-final-2007 2/29

2

Automobile (Four Wheeler)

Subject: - Statistics

H.L. Institute of Commerce

Section: - 2nd

Group: - 201-210

Name Roll No.

Siddhartha Mistry 201

Nisarg Modh 202

Sejal Modhwadia 203

Aesha Modi 204

Darshil Modi 205

Deep Modi 206

Naiya Modi 207

Nilesh Modi 208

Surbhi Modi 209

Darshil Mody 210

8/3/2019 Siddhartha Final 2007

http://slidepdf.com/reader/full/siddhartha-final-2007 3/29

3

Acknowledgement

We owe a great many thanks to a great many people who helped and supported

me during the Making of this Project.

Our deepest thanks to Mr.Dinesh Barot, the Guide of the project for guiding and

correcting various documents of mine with attention and care. He has taken pain

to go through the project and make necessary correction as and when needed.

We would also thank our Institution and our faculty members without whom this

project would have been a distant reality. We also extend our heartfelt thanks to

our family and well wishers.

And Last but not the least to Mr. Bill Gates for making Microsoft Office starting

from word to excel and spelling checks and Find and replace, without which this

project report would have taken days to complete.

Thanking You,

Group: 201-210.

8/3/2019 Siddhartha Final 2007

http://slidepdf.com/reader/full/siddhartha-final-2007 4/29

4

Index:

Sr.

No.

Particulars Page No.

1. Introduction 5

2. Scope of the sector in India 6

3 Automobile Industry’s Contribution to Emplyment

Generation and India’s GDP

7

4. Growth of the Sector in India 8

5 Acknowledgement 3

6 Major Player in Sector 9

7 Market Share 9

8 Maruti Suzuki India Limited 11

8/3/2019 Siddhartha Final 2007

http://slidepdf.com/reader/full/siddhartha-final-2007 5/29

5

9 TATA Motors 11

10 Ashok Leyland 12

11 Mahindra& Mahindra 13

12 Analysis Of Sales 14

13 Analysis of Profit 15

14 Correlation Regression 16

15 Conclusion 27

8/3/2019 Siddhartha Final 2007

http://slidepdf.com/reader/full/siddhartha-final-2007 6/29

6

Introduction:-

Only three decades back, Indian car buyers had just two models to choose from. Both were

local reproductions of European models that had disappeared from the western markets soon

after World War II. Irrespective of market demand, manufacturing capacity was restricted

through government licenses, and buyers had to wait several months after paying cash up

front to get delivery. Imports were discouraged through very high duties, which remain high

even now, and foreign-made cars were prized possessions of only the most affluent.

The early 1900s saw many automobile manufacturing companies coming into existence in

a number of European countries and the United States. The first mass produced automobile

in the United States was the curved-dash Oldsmobile. It was a three-horsepower machine and

sold 5,000 units by 1904. The economics of the US car market was disrupted by the arrival of

Henry Ford and his Model T car. The Model T was the world's first mass produced vehicle-

a million units were sold by 1920- a space of 10 years.

The introduction of a tiny hatchback in 1983 by Maruti Suzuki, jointly promoted by the

Indian government and Japanese small car manufacturer Suzuki, was in many ways a

defining moment in the development of the Indian automobile industry. Though very small,

the Maruti 800, as it was called, was modern and much more reliable than its competitors.

After a relatively slow start, the car endeared itself to the growing Indian middle class andremained the best seller for the next two decades. Until recently, it was the most

inexpensively produced car in the world, and today remains popular in the semi-urban and

rural markets of India.

More significantly, Maruti Suzuki introduced more efficient manufacturing practices and

developed a number of local component suppliers. This industrial eco-system with vastly

improved capabilities eased the entry of several foreign car manufacturers, after industrial

licensing was abandoned in the 1990s. The growth of component suppliers also enabled

select domestic automobile firms, with no prior experience in car manufacturing, to add

passenger vehicles to their product range. Though several foreign manufacturers have

struggled to expand their foothold, the growing purchasing power of the middle class

continues to attract new entrants to the Indian passenger car markers.

8/3/2019 Siddhartha Final 2007

http://slidepdf.com/reader/full/siddhartha-final-2007 7/29

7

Scope of the sector in India:-

The Indian automobile industry is going through a phase of rapid change and high growth.

With new projects coming up on a regular basis, the industry is undergoing technological

change. The major players are expanding their plants and focusing on mass customization, mass

production, etc.

Indian car industry has undergone tremendous change in recent times in terms of innovative

designs, concepts and technology. The efforts of the car manufacturers in India also started

reflecting in the sales figures. In 2009, the festive season brought cheers in the car market for

major players like Honda Siel Cars India (HSCI), General Motors India (GMI) and Hyundai

India boosting their sales records. The trend is still ticking in the same spirit and the year 2010 is

also expected to yield good results for the automobile industry in India with touching 10 to 12%

growth.

Early 2000 however saw globalization of Indian auto industry. Several policy changes were

introduced with focus on boosting the auto exports. A Core Group on Automotive Research and

Development (CAR) was established in 2003 for encouraging R&D activities. Foreign

manufactures started looking at India for sourcing auto components. The buyers started ruling

the market due to the availability of choices in the form of models, price points and brands. A

vibrant economy meant an increase in the GDP and per capita income. These factors turned out

to be significant contributors in pushing up the domestic demand. The vast geographic spread of

India attracted foreign investments. The marquee brands from all over the world started courting

Indian consumers aggressively. The mature markets in the developed countries paled in

comparison to the sheer numbers and the growth phase of the Indian auto industry.

8/3/2019 Siddhartha Final 2007

http://slidepdf.com/reader/full/siddhartha-final-2007 8/29

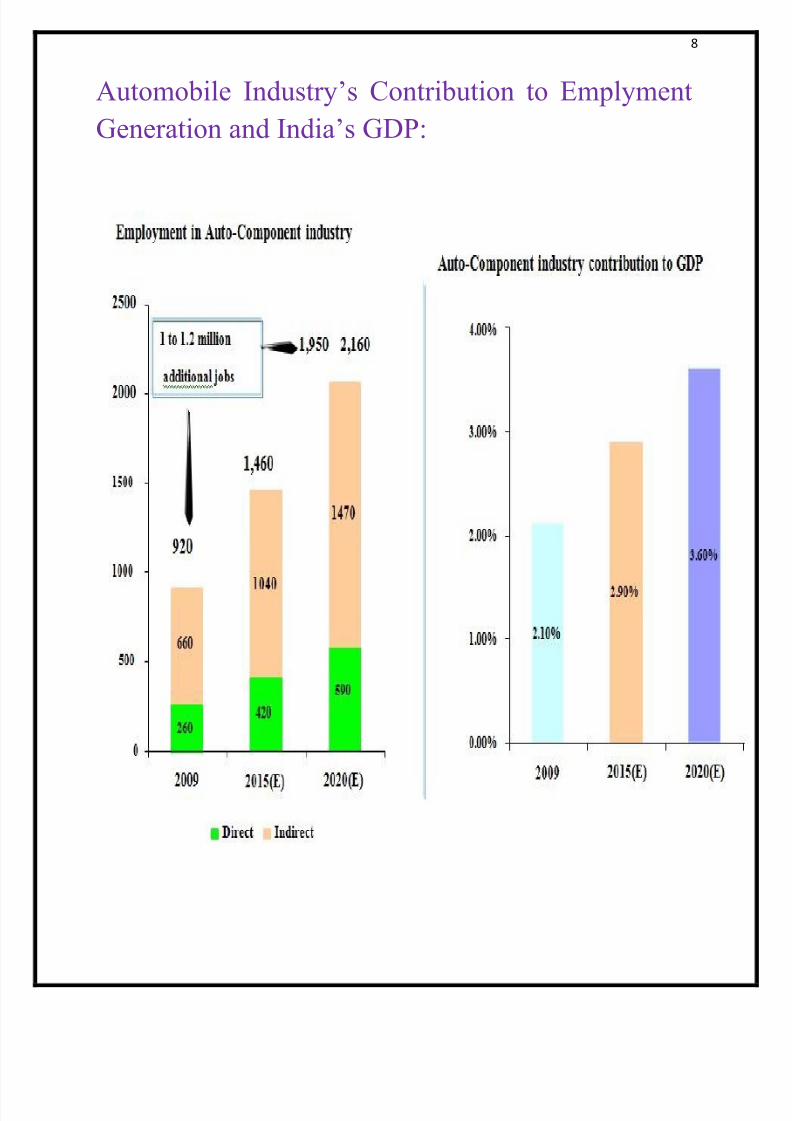

8

Automobile Industry’s Contribution to Emplyment

Generation and India’s GDP:

8/3/2019 Siddhartha Final 2007

http://slidepdf.com/reader/full/siddhartha-final-2007 9/29

9

Growth of the Sector in India.

At present the industry is enjoying a growth rate of 14-17% per annum, with

domestic sales growth at 12.8%. The growth rate is predicted to double by 2015.

As it is seen, the total sales of passenger vehicles - cars, utility vehicles and multi-

utility vehicles - in the year 2005 reached the mark of 1.06 million. The current

growth rate indicates that by 2012 India will overtake Germany and Japan in sales

volumes.

Financing schemes have become an important factor in the growth of automobile

sales. More and more financial schemes are coming up with easy instalment plans

to lure the customers.

Apart from domestic production, the industry is consistently focusing on the

automobile exports. The auto component segment is contributing a lot in the export

arena. The liberalized policies of the government are now making the companies

go for more and more exports.

8/3/2019 Siddhartha Final 2007

http://slidepdf.com/reader/full/siddhartha-final-2007 10/29

10

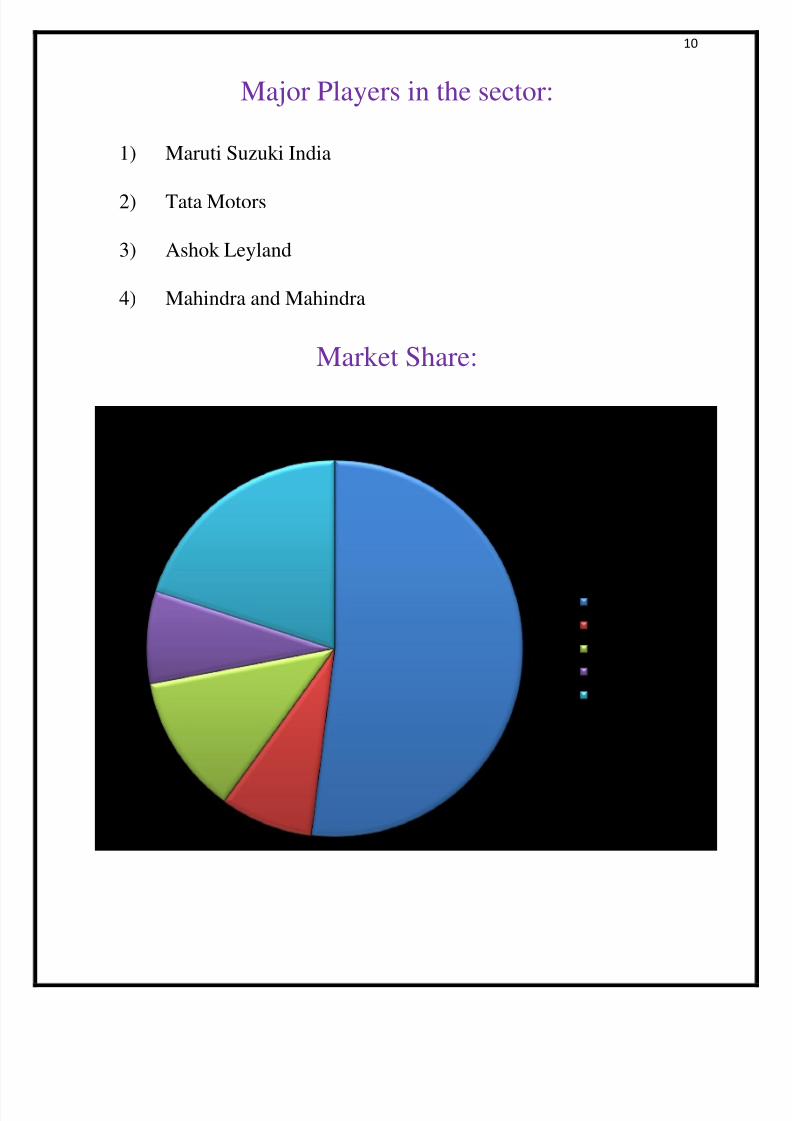

Major Players in the sector:

1) Maruti Suzuki India

2) Tata Motors

3) Ashok Leyland

4) Mahindra and Mahindra

Market Share:

Market Share %

Maruti Suzuki

Ashok Leyland

Tata Motors

Mahindra &Mahindra

Others

8/3/2019 Siddhartha Final 2007

http://slidepdf.com/reader/full/siddhartha-final-2007 11/29

11

Maruti Suzuki India Limited:

Maruti Suzuki India Limited (MSIL, formerly

known as Maruti Udyog Limited) is a

subsidiary of Suzuki Motor Corporation,

Japan. MSIL has been the leader of the Indian car market for over two and a half

decades. The company has two manufacturing facilities located at Gurgaon and

Manesar, south of New Delhi, India. Both the facilities have a combined capability

to produce over a 1.2 million (1,200,000) vehicles annually.

The company plans to expand its manufacturing capacity to 1.75 million by 2013.

The company offers a wide range of cars across different segments. It offers 15

brands and over 150 variants - Maruti 800, people movers, Omni and Eeco,

international brands Alto, Alto-K10, A-star, WagonR, Swift, Ritz and Estilo, off-

roader Gypsy, SUV Grand Vitara, sedans SX4, Swift DZire and Kizashi. In an

environment friendly initiative, in August 2010 Maruti Suzuki introduced factory

fitted CNG option on 5 models across vehicle segments. These include Eeco, Alto,

Estilo Wagon-R and SX4.

In fiscal 2009-10 Maruti Suzuki became the only Indian company to manufacture

and sell One Million cars in a year.

Maruti Suzuki's revenue has grown consistently over the years.

8/3/2019 Siddhartha Final 2007

http://slidepdf.com/reader/full/siddhartha-final-2007 12/29

12

Tata Motors:

Tata Motors Limited is India’s largest

automobile company, with consolidated

revenues of Rs.1, 23,133 cores (USD 27 billion)

in 2010-11. It is the leader in commercial

vehicles in each segment, and among the top

three in passenger vehicles with winning products in the compact, midsize car and

utility vehicle segments. The Company is the world's fourth largest truck

manufacturer, and the world's third largest bus manufacturer.

The Company's over 25,000 employees are guided by the vision to be "best in the

manner in which we operate, best in the products we deliver, and best in our value

system and ethics."

Tata Motors also distributes and markets Fiat branded cars in India.

8/3/2019 Siddhartha Final 2007

http://slidepdf.com/reader/full/siddhartha-final-2007 13/29

13

Ashok Leyland:

The origin of Ashok Leyland can be

traced to the urge for self-reliance, felt

by independent India. Pandit

Jawaharlal Nehru, India's first Prime

Minister persuaded Mr. Raghunandan Saran, an industrialist, to enter automotive

manufacture. In 1948, Ashok Motors was set up in what was then Madras, for the

assembly of Austin Cars. The Company's destiny and name changed soon with

equity participation by British Leyland and Ashok Leyland commenced

manufacture of commercial vehicles in 1955

Access to international technology enabled the Company to set a tradition to be

first with technology. Be it full air brakes, power steering or rear engine busses,

Ashok Leyland pioneered all these concepts. Responding to the operating

conditions and practices in the country, the Company made its vehicles strong,

over-engineering them with extra metallic muscles. "Designing durable products

that make economic sense to the consumer, using appropriate technology", became

the design philosophy of the Company, which in turn has moulded consumer

attitudes and the brand personality.

The blueprint prepared for the future reflected the global ambitions of the

company, captured in four words: Global Standards, Global Markets. This was at a

time when liberalisation and globalisation were not yet in the air. Ashok Leyland

embarked on a major product and process upgradation to match world-class

standards of technology.

8/3/2019 Siddhartha Final 2007

http://slidepdf.com/reader/full/siddhartha-final-2007 14/29

14

Mahindra & Mahindra ltd:

Founded in 1945 as a steel trading company,

we entered automotive manufacturing in

1947 to bring the iconic Willys Jeep onto

Indian roads. Over the years, we’ve

diversified into many new businesses in order to better meet the needs of our

customers. We follow a unique business model of creating empowered companies

that enjoy the best of entrepreneurial independence and Group-wide synergies.

This principle has led our growth into a US $12.5 billion multinational group with

more than 137,000 employees in over 100 countries across the globe.

Today, their operations span 18 key industries that form the foundation of every

modern economy: aerospace, aftermarket, agribusiness, automotive, components,

construction equipment, consulting services, defense, energy, farm equipment,

finance and insurance, industrial equipment, information technology, leisure and

hospitality, logistics, real estate, retail, and two wheelers.

Their federated structure enables each business to chart its own future and

simultaneously leverage synergies across the entire Group’s competencies. In this

way, the diversity of our expertise allows us to bring our customers the best in

many fields.

8/3/2019 Siddhartha Final 2007

http://slidepdf.com/reader/full/siddhartha-final-2007 15/29

15

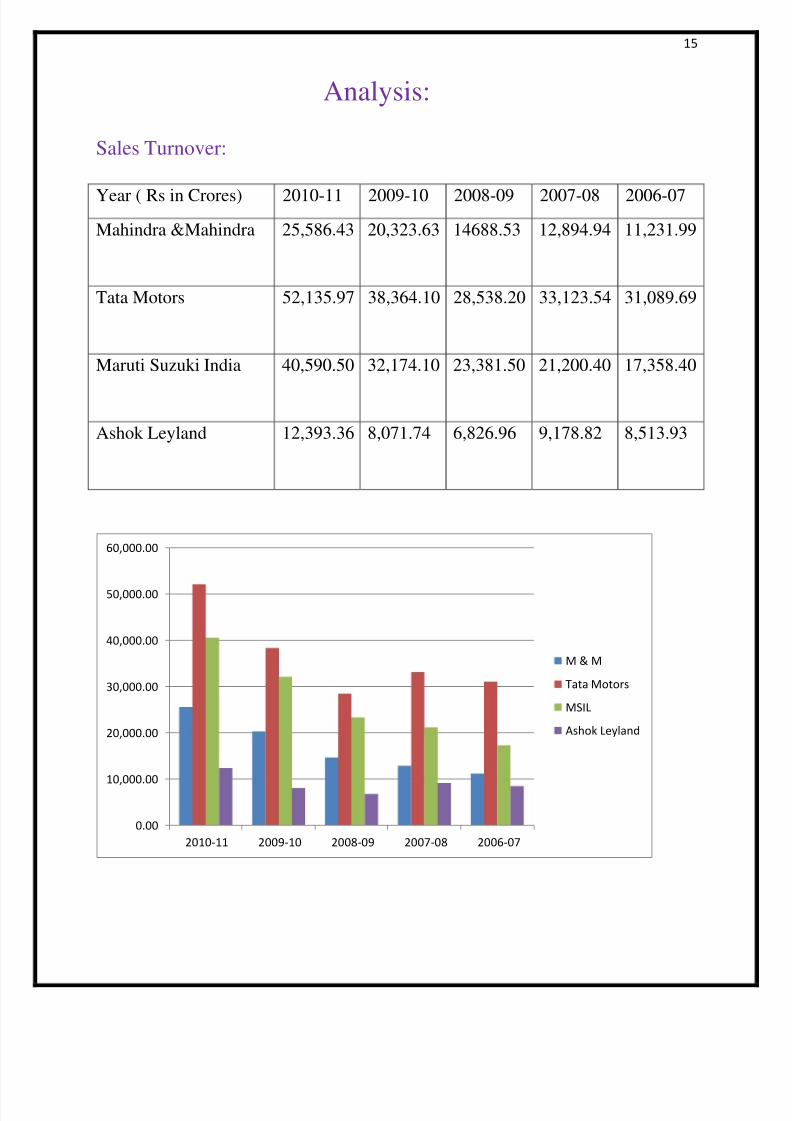

Analysis:

Sales Turnover:

Year ( Rs in Crores) 2010-11 2009-10 2008-09 2007-08 2006-07

Mahindra &Mahindra 25,586.43 20,323.63 14688.53 12,894.94 11,231.99

Tata Motors 52,135.97 38,364.10 28,538.20 33,123.54 31,089.69

Maruti Suzuki India 40,590.50 32,174.10 23,381.50 21,200.40 17,358.40

Ashok Leyland 12,393.36 8,071.74 6,826.96 9,178.82 8,513.93

0.00

10,000.00

20,000.00

30,000.00

40,000.00

50,000.00

60,000.00

2010-11 2009-10 2008-09 2007-08 2006-07

M & M

Tata Motors

MSIL

Ashok Leyland

8/3/2019 Siddhartha Final 2007

http://slidepdf.com/reader/full/siddhartha-final-2007 16/29

16

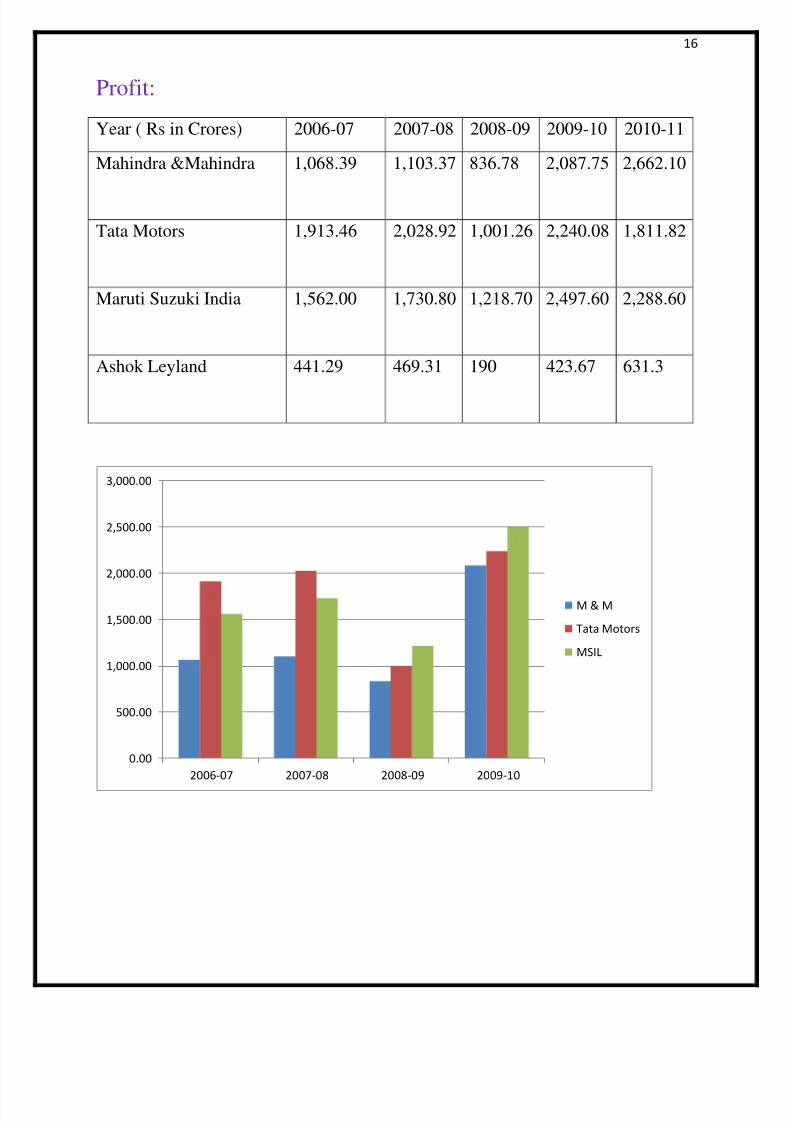

Profit:

Year ( Rs in Crores) 2006-07 2007-08 2008-09 2009-10 2010-11

Mahindra &Mahindra 1,068.39 1,103.37 836.78 2,087.75 2,662.10

Tata Motors 1,913.46 2,028.92 1,001.26 2,240.08 1,811.82

Maruti Suzuki India 1,562.00 1,730.80 1,218.70 2,497.60 2,288.60

Ashok Leyland 441.29 469.31 190 423.67 631.3

0.00

500.00

1,000.00

1,500.00

2,000.00

2,500.00

3,000.00

2006-07 2007-08 2008-09 2009-10

M & M

Tata Motors

MSIL

8/3/2019 Siddhartha Final 2007

http://slidepdf.com/reader/full/siddhartha-final-2007 17/29

17

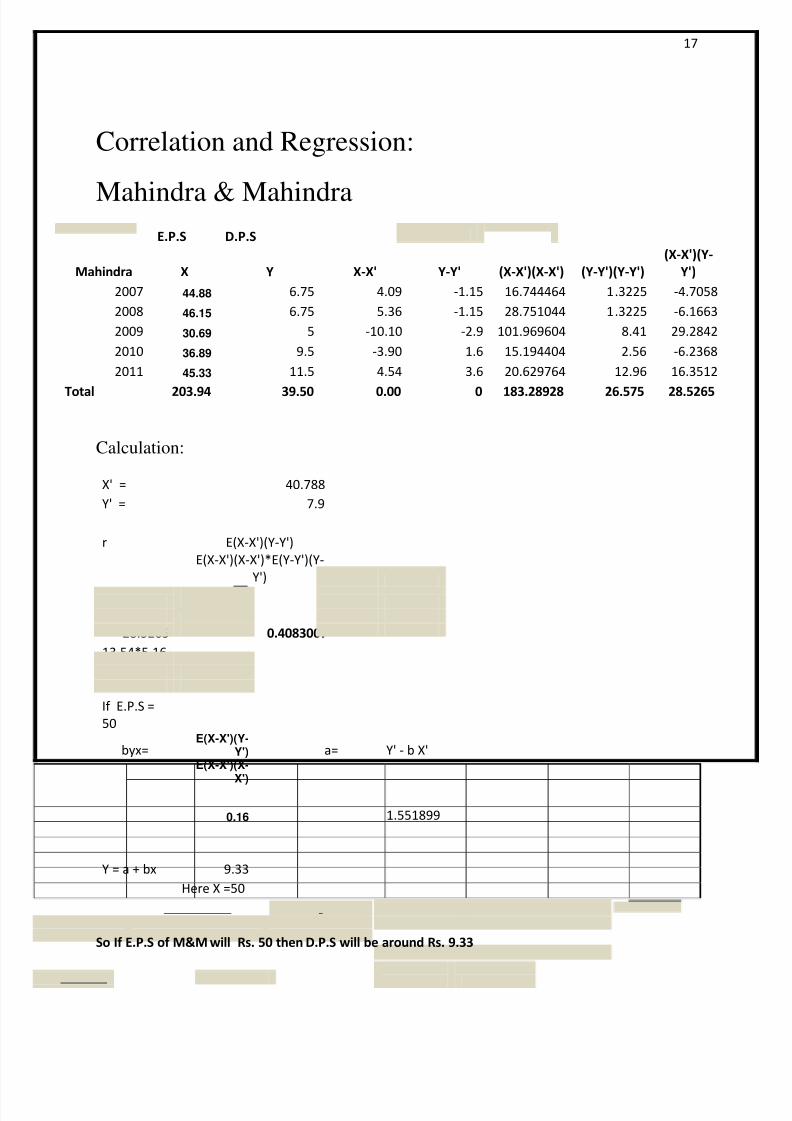

Correlation and Regression:

Mahindra & Mahindra

Mahindra

E.P.S D.P.S

X Y X-X' Y-Y' (X-X')(X-X') (Y-Y')(Y-Y')

(X-X')(Y-

Y')

2007 44.88 6.75 4.09 -1.15 16.744464 1.3225 -4.7058

2008 46.15 6.75 5.36 -1.15 28.751044 1.3225 -6.1663

2009 30.69 5 -10.10 -2.9 101.969604 8.41 29.2842

2010 36.89 9.5 -3.90 1.6 15.194404 2.56 -6.2368

2011 45.33 11.5 4.54 3.6 20.629764 12.96 16.3512

Total 203.94 39.50 0.00 0 183.28928 26.575 28.5265

Calculation:

X' = 40.788

Y' = 7.9

r E(X-X')(Y-Y')

E(X-X')(X-X')*E(Y-Y')(Y-

Y')

28.5265 0.4083007

13.54*5.16

If E.P.S =

50

byx=E(X-X')(Y-

Y') a= Y' - b X'E(X-X')(X-

X')

0.16 1.551899

Y = a + bx 9.33

Here X =50

So If E.P.S of M&M will Rs. 50 then D.P.S will be around Rs. 9.33

8/3/2019 Siddhartha Final 2007

http://slidepdf.com/reader/full/siddhartha-final-2007 18/29

18

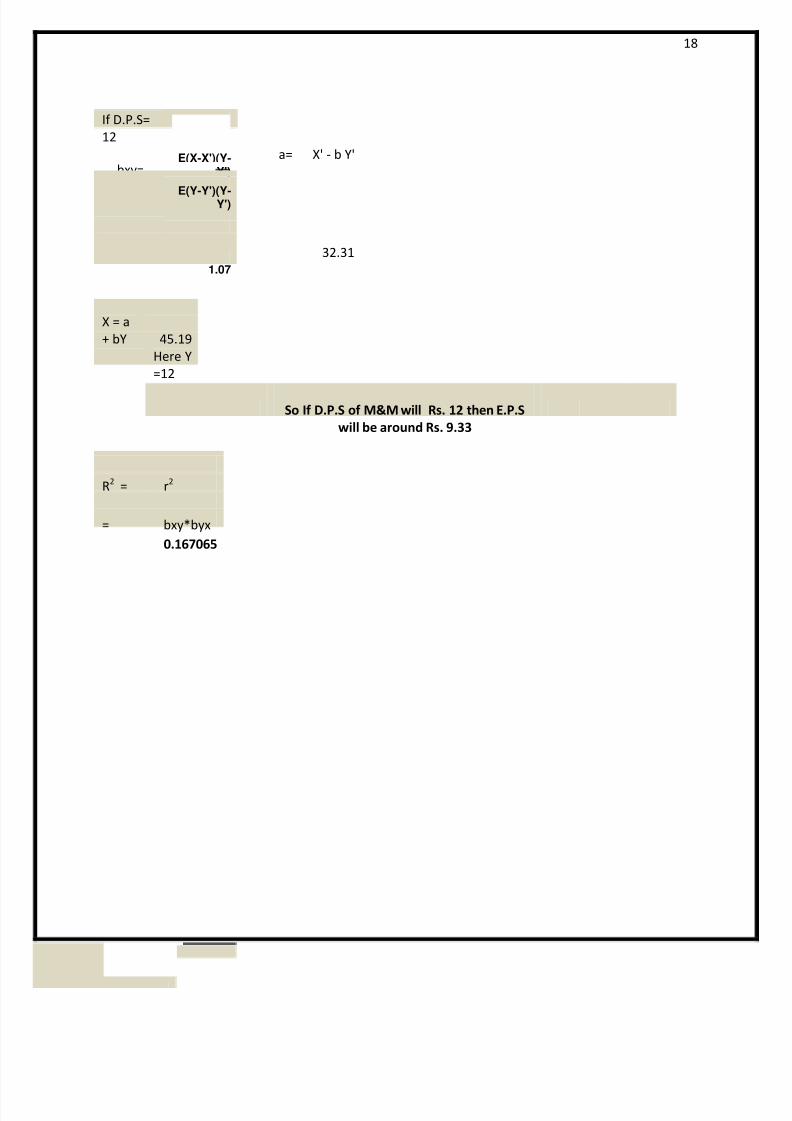

If D.P.S=

12

bxy=E(X-X')(Y-

Y')

a= X' - b Y'

E(Y-Y')(Y-Y')

1.07

32.31

X = a

+ bY 45.19

Here Y

=12

So If D.P.S of M&M will Rs. 12 then E.P.S

will be around Rs. 9.33

R2

= r2

= bxy*byx

0.167065

8/3/2019 Siddhartha Final 2007

http://slidepdf.com/reader/full/siddhartha-final-2007 19/29

19

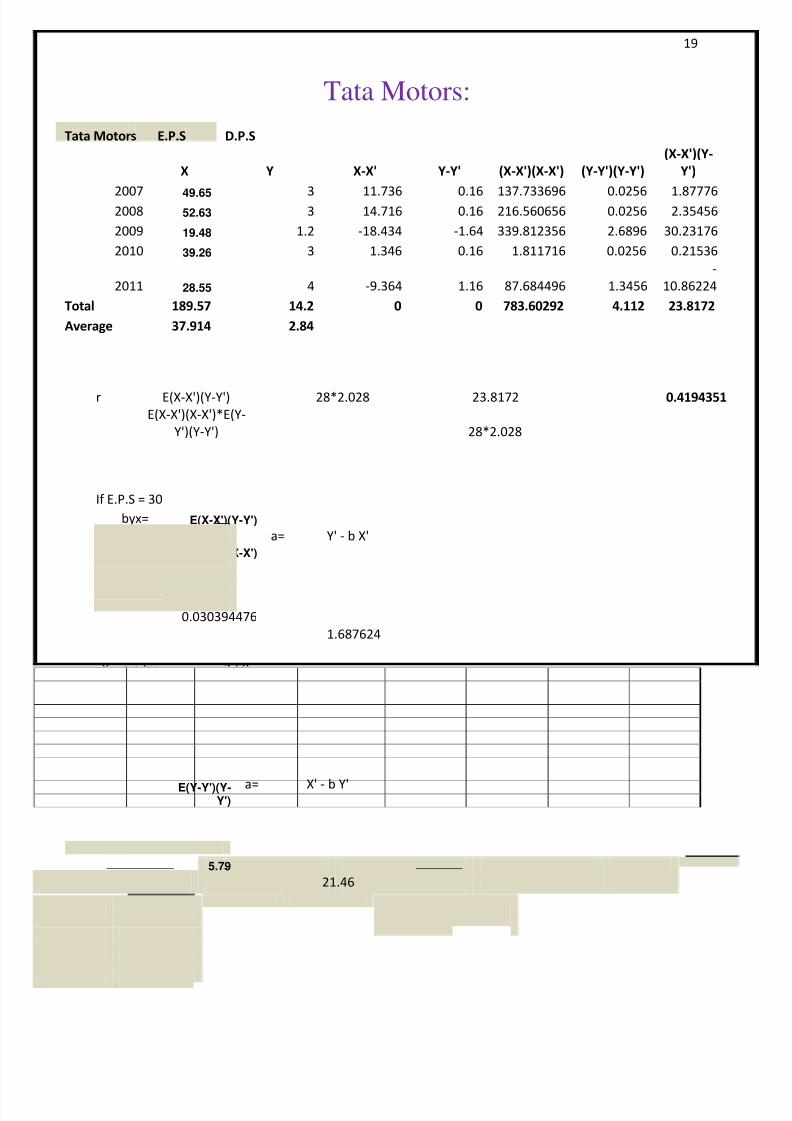

Tata Motors:

Tata Motors E.P.S D.P.S

X Y X-X' Y-Y' (X-X')(X-X') (Y-Y')(Y-Y')

(X-X')(Y-

Y')

2007 49.65 3 11.736 0.16 137.733696 0.0256 1.877762008 52.63 3 14.716 0.16 216.560656 0.0256 2.35456

2009 19.48 1.2 -18.434 -1.64 339.812356 2.6896 30.23176

2010 39.26 3 1.346 0.16 1.811716 0.0256 0.21536

2011 28.55 4 -9.364 1.16 87.684496 1.3456

-

10.86224

Total 189.57 14.2 0 0 783.60292 4.112 23.8172

Average 37.914 2.84

r E(X-X')(Y-Y') 28*2.028 23.8172 0.4194351

E(X-X')(X-X')*E(Y-

Y')(Y-Y') 28*2.028

If E.P.S = 30

byx= E(X-X')(Y-Y')

E(X-X')(X-X')

a= Y' - b X'

0.030394476

1.687624

Y = a + bx 2.60

Here X =30

So If E.P.S of Tata Motors will Rs. 30 then D.P.S will be around Rs. 2.60

If D.P.S=

5

bxy=E(X-X')(Y-

Y')

E(Y-Y')(Y-Y')

a= X' - b Y'

5.79

21.46

8/3/2019 Siddhartha Final 2007

http://slidepdf.com/reader/full/siddhartha-final-2007 20/29

20

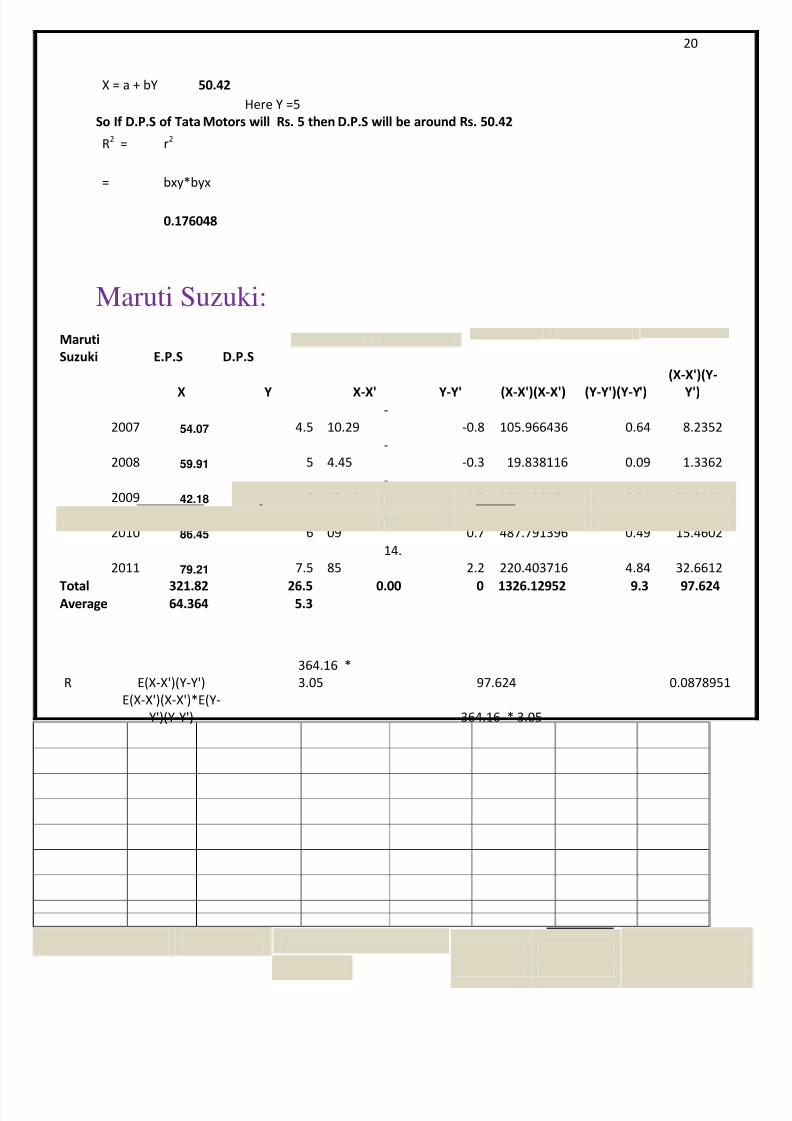

X = a + bY 50.42

Here Y =5

So If D.P.S of Tata Motors will Rs. 5 then D.P.S will be around Rs. 50.42

Maruti Suzuki:

Maruti

Suzuki E.P.S D.P.S

X Y X-X' Y-Y' (X-X')(X-X') (Y-Y')(Y-Y')

(X-X')(Y-

Y')

2007 54.07 4.5

-

10.29 -0.8 105.966436 0.64 8.2352

2008 59.91 5

-

4.45 -0.3 19.838116 0.09 1.3362

2009 42.18 3.5

-

22.18 -1.8 492.129856 3.24 39.9312

2010 86.45 6

22.

09 0.7 487.791396 0.49 15.4602

2011 79.21 7.5

14.

85 2.2 220.403716 4.84 32.6612

Total 321.82 26.5 0.00 0 1326.12952 9.3 97.624Average 64.364 5.3

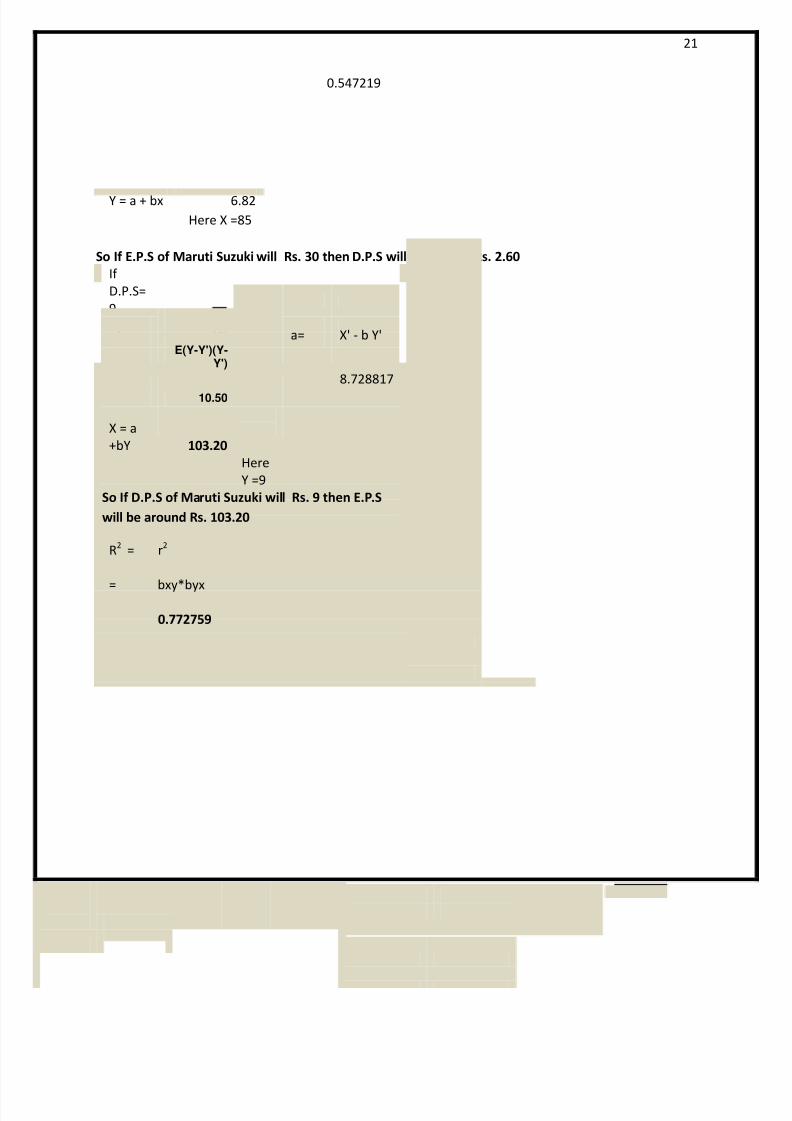

If E.P.S =85

byx= E(X-X')(Y-Y')

E(X-X')(X-X')

a= Y' - b X'

0.073615736

R2

= r2

= bxy*byx

0.176048

R E(X-X')(Y-Y')

364.16 *

3.05 97.624 0.0878951

E(X-X')(X-X')*E(Y-

Y')(Y-Y') 364.16 * 3.05

8/3/2019 Siddhartha Final 2007

http://slidepdf.com/reader/full/siddhartha-final-2007 21/29

21

0.547219

Y = a + bx 6.82

Here X =85

So If E.P.S of Maruti Suzuki will Rs. 30 then D.P.S will be around Rs. 2.60

If

D.P.S=

9

bxy=E(X-X')(Y-

Y') a= X' - b Y'E(Y-Y')(Y-

Y')

8.728817

10.50

X = a

+bY 103.20

Here

Y =9

So If D.P.S of Maruti Suzuki will Rs. 9 then E.P.S

will be around Rs. 103.20

R2

= r2

= bxy*byx

0.772759

8/3/2019 Siddhartha Final 2007

http://slidepdf.com/reader/full/siddhartha-final-2007 22/29

22

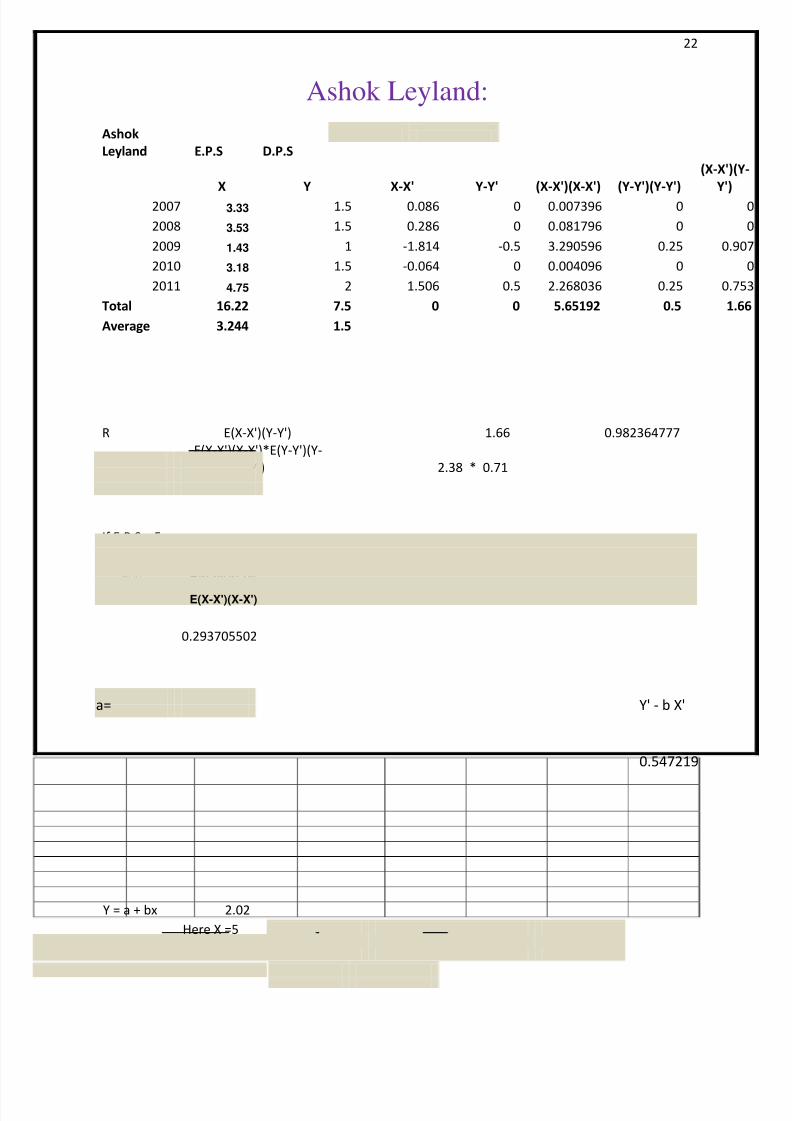

Ashok Leyland:

Ashok

Leyland E.P.S D.P.S

X Y X-X' Y-Y' (X-X')(X-X') (Y-Y')(Y-Y')

(X-X')(Y

Y')

2007 3.33 1.5 0.086 0 0.007396 0

2008 3.53 1.5 0.286 0 0.081796 0

2009 1.43 1 -1.814 -0.5 3.290596 0.25 0.90

2010 3.18 1.5 -0.064 0 0.004096 0

2011 4.75 2 1.506 0.5 2.268036 0.25 0.75

Total 16.22 7.5 0 0 5.65192 0.5 1.6

Average 3.244 1.5

R E(X-X')(Y-Y') 1.66 0.982364777

E(X-X')(X-X')*E(Y-Y')(Y-

Y') 2.38 * 0.71

If E.P.S = 5

byx= E(X-X')(Y-Y')

E(X-X')(X-X')

0.293705502

a= Y' - b X'

0.547219

Y = a + bx 2.02

Here X =5

8/3/2019 Siddhartha Final 2007

http://slidepdf.com/reader/full/siddhartha-final-2007 23/29

23

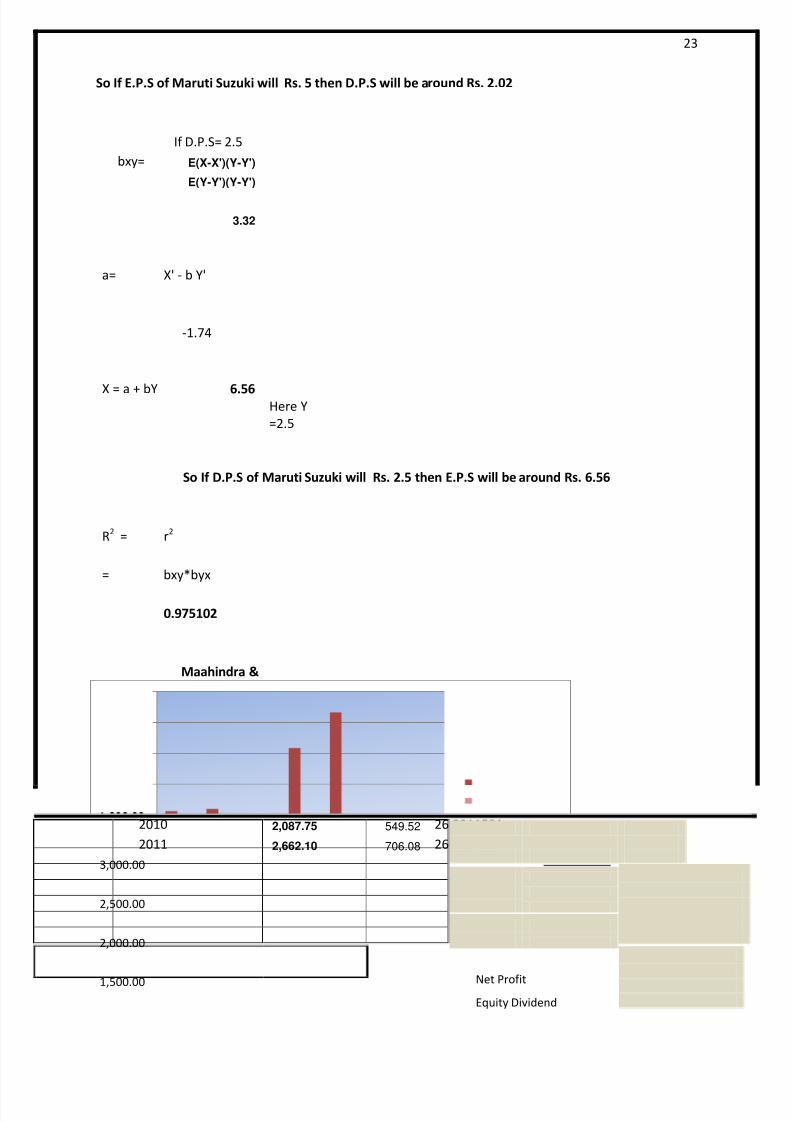

So If E.P.S of Maruti Suzuki will Rs. 5 then D.P.S will be around Rs. 2.02

If D.P.S= 2.5

bxy= E(X-X')(Y-Y')

E(Y-Y')(Y-Y')

3.32

a= X' - b Y'

-1.74

X = a + bY 6.56Here Y

=2.5

So If D.P.S of Maruti Suzuki will Rs. 2.5 then E.P.S will be around Rs. 6.56

R2

= r2

= bxy*byx

0.975102

Maahindra &

Mahindra

Net Profit

Equity

Dividend %

2007 1,068.39 282.23 26.4163835

2008 1,103.37 282.61 25.61334822009 836.78 278.83 33.3217811

2010 2,087.75 549.52 26.3211591

2011 2,662.10 706.08 26.5234214

1,500.00

2,000.00

2,500.00

3,000.00

Net Profit

Equity Dividend

8/3/2019 Siddhartha Final 2007

http://slidepdf.com/reader/full/siddhartha-final-2007 24/29

24

From the above graph we can conclude that company constantly gives

dividend yet there is change in Net Profit.

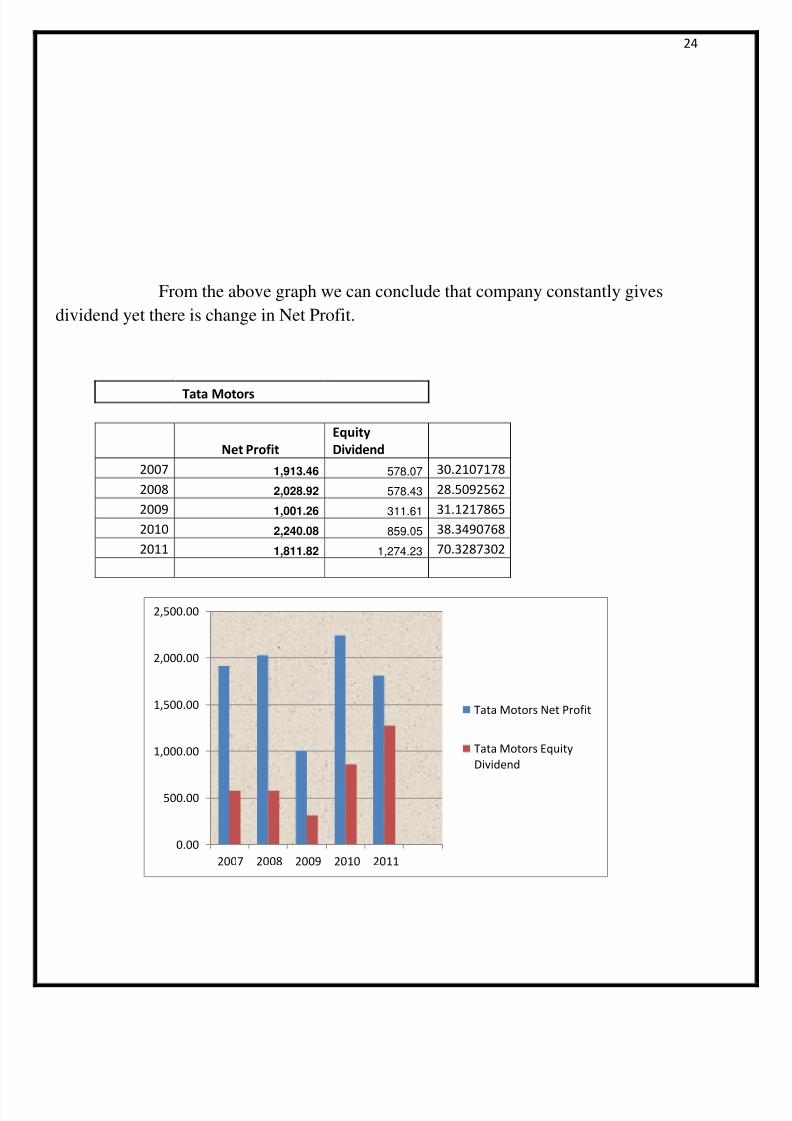

Tata Motors

Net Profit

Equity

Dividend

2007 1,913.46 578.07 30.2107178

2008 2,028.92 578.43 28.5092562

2009 1,001.26 311.61 31.1217865

2010 2,240.08 859.05 38.3490768

2011 1,811.82 1,274.23 70.3287302

0.00

500.00

1,000.00

1,500.00

2,000.00

2,500.00

2007 2008 2009 2010 2011

Tata Motors Net Profit

Tata Motors Equity

Dividend

8/3/2019 Siddhartha Final 2007

http://slidepdf.com/reader/full/siddhartha-final-2007 25/29

25

From the above graph company gives around 35% dividend but in company gave 70%

dividend of Net Profit.So, the major effect on share price was seen during the period of

book Closure.

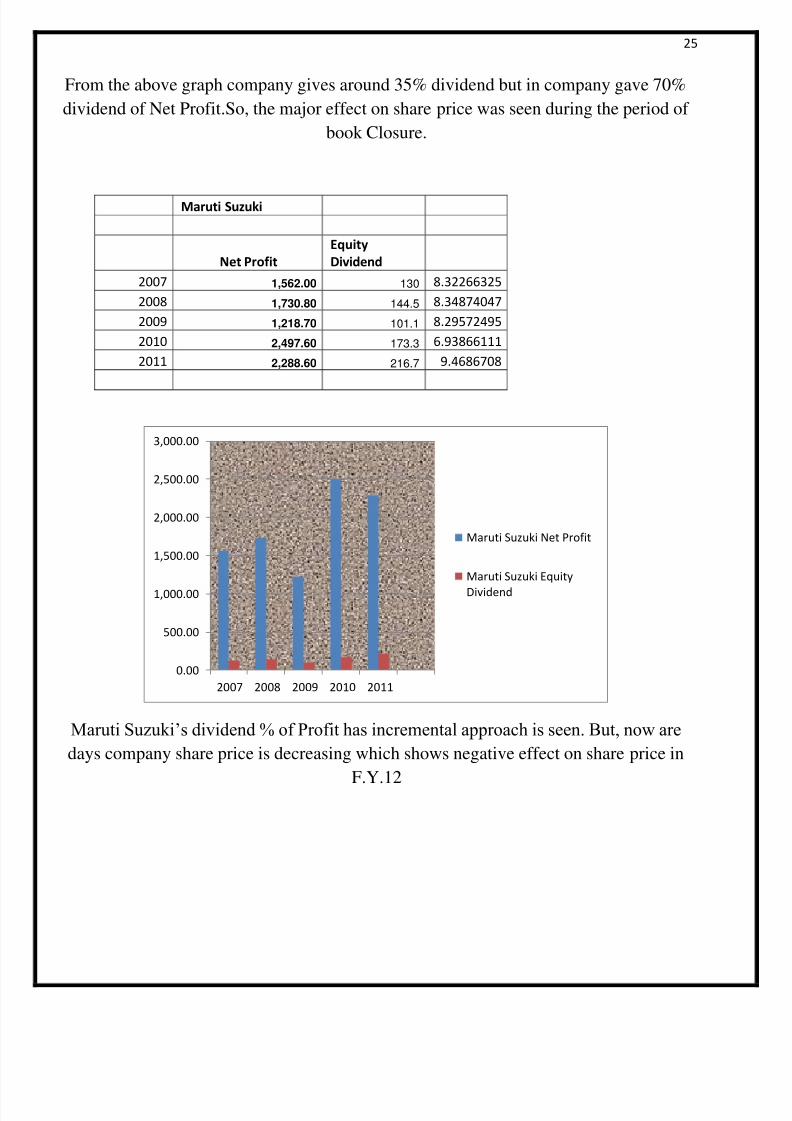

Maruti Suzuki

Net Profit

Equity

Dividend

2007 1,562.00 130 8.32266325

2008 1,730.80 144.5 8.34874047

2009 1,218.70 101.1 8.29572495

2010 2,497.60 173.3 6.93866111

2011 2,288.60 216.7 9.4686708

Maruti Suzuki’s dividend % of Profit has incremental approach is seen. But, now are

days company share price is decreasing which shows negative effect on share price in

F.Y.12

0.00

500.00

1,000.00

1,500.00

2,000.00

2,500.00

3,000.00

2007 2008 2009 2010 2011

Maruti Suzuki Net Profit

Maruti Suzuki Equity

Dividend

8/3/2019 Siddhartha Final 2007

http://slidepdf.com/reader/full/siddhartha-final-2007 26/29

26

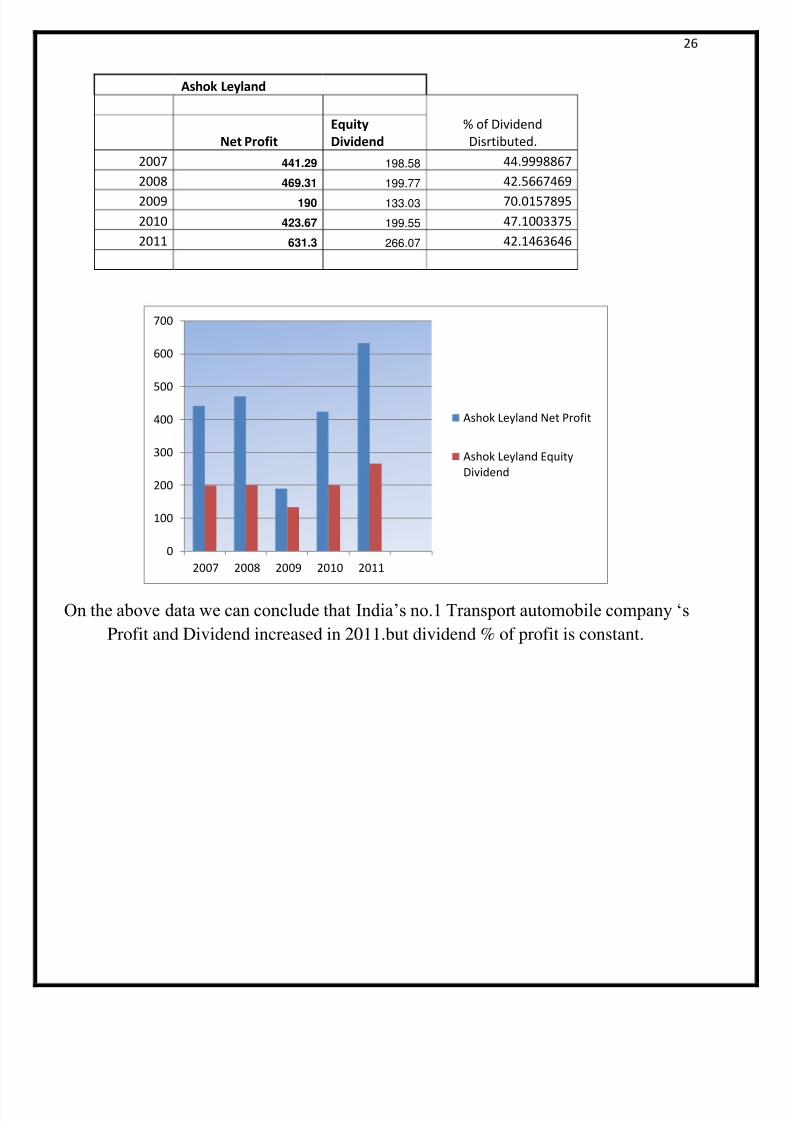

Ashok Leyland

% of Dividend

Disrtibuted.Net Profit

Equity

Dividend

2007 441.29 198.58 44.9998867

2008 469.31 199.77 42.5667469

2009 190 133.03 70.0157895

2010 423.67 199.55 47.1003375

2011 631.3 266.07 42.1463646

On the above data we can conclude that India’s no.1 Transport automobile company ‘s

Profit and Dividend increased in 2011.but dividend % of profit is constant.

0

100

200

300

400

500

600

700

2007 2008 2009 2010 2011

Ashok Leyland Net Profit

Ashok Leyland Equity

Dividend

8/3/2019 Siddhartha Final 2007

http://slidepdf.com/reader/full/siddhartha-final-2007 27/29

27

Conclusion:

Infrastructure Deficit

Talent Crunch

Scaling-Up the industry

Access to World-class Technology and Quality Practices

Remaining cost competitive

Access to and availability of cost-effective capital

Trade Policy

As Indian Automobile Sector is Continuously growing but as compare toWorld market our growth is restricted. Our Automobile sector is with middleclass . The Technology and interior is not much competitive. One interesting

thing that Gujarat is becoming Auto Hub as TATA ,Ford, Mercedes,NISSAN, MARUTI SUZUKI,VolksWagon welcomed by GujaratGovernment.So, its good strategy to welcome the World Auto mobileCompany for the development on our country.

8/3/2019 Siddhartha Final 2007

http://slidepdf.com/reader/full/siddhartha-final-2007 28/29

28

Bibliography:

Reference

http://www.rbi.org.in

Central statistical organisation

Economic Times

Indiatimes.com

8/3/2019 Siddhartha Final 2007

http://slidepdf.com/reader/full/siddhartha-final-2007 29/29

29

![DOSSIER 10 9 WiRES Annex - moodle.adaptland.it · [628 final 28.02.2005]. 0 Communication from [627 final 28 2006] 0 Decision 1639/2006/EC 24 Framework Programme(2007 2013). 0 Communication](https://img.pdfslide.fr/doc/110x75/5f4cff979584e561884169d3/dossier-10-9-wires-annex-628-final-28022005-0-communication-from-627-final.jpg)