Embed Size (px)

Citation preview

Les articles publiés dans la série "Économie et statistiques" n'engagent que leurs auteurs. Ils ne reflètent pas forcément les vues du STATEC et n'engagent en rien sa responsabilité.

87 Economie et Statistiques

Working papers du STATEC juin 2016

Auteur: Christian Glocker

Introducing a financial accelerator in Modux

Abstract

Many structural macroeconometric models used in policy circles fail in properly explaining the observed fluctuations surrounding the global financial crisis episode and its aftermath. In several instances this follows from the fact the macrofinancial interactions are left unexplained. In what follows I introduce a basic financial market structure into Modux - a model characterizing the Luxembourgish economy - with the intention of being able to better explain the aforementioned episode. The macrofinancial extension is limited to the machinery & equipment sector. The results show that the overall model fit improves noticeably once interactions between the financial sector and the real economy are allowed for. Moreover, the corresponding financial accelerator effects contribute significantly to magnifying the effects of structural disturbances.

INTRODUCING A FINANCIAL ACCELERATOR IN MODUX

Abstract. Many structural macroeconometric models used in policy cir-

cles fail in properly explaining the observed fluctuations surrounding the

global financial crisis episode and its aftermath. In several instances this

follows from the fact the macrofinancial interactions are left unexplained.

In what follows I introduce a basic financial market structure into Modux -

a model characterizing the Luxembourgish economy - with the intention of

being able to better explain the aforementioned episode. The macrofinancial

extension is limited to the machinery & equipment sector. The results show

that the overall model fit improves noticeably once interactions between the

financial sector and the real economy are allowed for. Moreover, the corre-

sponding financial accelerator effects contribute significantly to magnifying

the effects of structural disturbances.

1. Motivation

The following is a project report concerning the extension of Modux - a struc-

tural macroeconometric model used at Statec/Luxembourg - with a financial

accelerator block.

The project is motivated by the deficiencies of the current specification of

the equation for capital in Modux in explaining the episode surrounding the

financial crisis and its aftermath. The inability to properly explain the fluctua-

tions in this episode is in fact a drawback in many structural macroeconometric

models. These models perform sufficiently well in explaining the fluctuations

in capital until the outbreak of the global financial crisis; however, from then

onwards the model fit gets noticeably worse. In particular, these models dis-

play large residuals in the years surrounding the global financial crisis and its

aftermath. The failure in explaining the path of the capital stock is replicated

Project Report written by Christian Glocker, March 2016.

Les opinions exprimees dans la presente publication sont celles des auteurs et ne refletent

pas forceement les opinions du STATEC et de l’ANEC.

2 INTRODUCING A FINANCIAL ACCELERATOR IN MODUX

in an inadequate fit of investment. This does not only violate the normality

property of the residuals, it also introduces a high degree of autocorrelation

which all together is insufficient to meet the requirements for any further statis-

tical analysis. Still, the estimation could be improved by introducing dummy

variables in the form of time-dummies in order to get appropriate residuals

also for the financial crisis episode. Though this would support the fit of the

equation to the data, it would nevertheless not improve the fit of the model to

the data as the model continues to fail in explaining this episode.

One commonly used explanation for this is a technical one involving func-

tional forms - the global financial crisis is replicated in the data in the form of

a major irregularity in many macroeconomic time series. It shows up in the

form of a previously unobserved large and abrupt drop in output and many

series alike. It seems as if the volatility pattern is a complete different one over

the crisis years. Many consider this as a form of non-linearity. Since most of

the structural macroeconometric models at use are linear or log-linear in their

basic functional structure, their ability in explaining non-linearities in the data

is hence limited. As a result, these models perform poorly in explaining the

years surrounding the global financial crisis episode and its aftermath.

Another explanation commonly used addresses the pure structure of these

models. Many of these models have a structure too focused on the real econ-

omy involving the production, income and spending accounts, the fiscal sector,

labour markets and the interaction with foreign economies. However, what is

yet ignored in many of these models is the extent to which financial markets

and in particular the interaction of financial markets with the real economy

plays a role for economic fluctuations. As a matter of fact, the omission of the

financial sector and its interaction with the real economy might be an alter-

native explanation why these models fail in properly explaining the observed

economic fluctuations surrounding the global financial crisis episode.

INTRODUCING A FINANCIAL ACCELERATOR IN MODUX 3

Against this background I proceed by elaborating on the latter. So far

Modux does not feature any financial market structure. There are a few fi-

nancial variables in the model, as for instance short and long term government

bond rates and the eurostoxx50 - index, however, most of them are specified as

purely exogenous variables. Hence at this stage, the model does not allow for

any endogenous interaction between financial markets and the real economy -

that is to say, macrofinancial linkages are missing. Hence it does not come as

a big surprise that the model, and in particular the equations for capital and

investment, fail to adequately explain the financial crisis episode.

In what follows I introduce a basic financial market structure with the inten-

tion of being able to better explain the crisis episode. The analysis is restricted

to the sector of machinery & equipment. The model extension presented herein

is based on a version of Modux documented in Adam (2004) and implies an

extended model for the real economy that is furnished with a financial block.

The role of the financial block is to take account of the comovements and

procyclicality of credit, asset prices and real economic activity that typically

characterizes a financial accelerator. The model differs from optimizing rep-

resentative agent models in several respects, the main reason for this being a

wider and less stringent theoretical framework and the fact that data are given

a more central role in shaping the long- and short-run structure of the model.

In what follows I begin with an explanation and a review of the literature

concerning the financial accelerator (section 2). The block of equations com-

prising the financial accelerator is elaborated in sections 3.1 - 3.3 and sections

3.4 - 3.5 finally discuss some differences between the original model and the

extended one by means of impulse response functions, short and medium term

forecasts and root mean squared errors statistics. Appendix A summarizes the

data being used.

4 INTRODUCING A FINANCIAL ACCELERATOR IN MODUX

2. Financial frictions in macroeconomic models

The recent global financial crisis has highlighted that macroeconomic mod-

els need to allocate a higher weight to the financial sector for understanding

the dynamics of the business cycle. In contrast to what has repeatedly been

reported, there is a well-established series of publications in macroeconomics

concerning the incorporation of financial market frictions in standard macroe-

conomic models. Bernanke and Gertler (1989) is an early study in this respect.

Kiyotaki and Moore (1997) provide another approach to adding financial fric-

tions in a general equilibrium model of the macroeconomy. These contributions

are now key references for most of the work done in this area during the last

two decades. Even though these studies had a big influence in the academic

field, macroeconomic models which are used in policy circles have so far ig-

nored this branch of economic research to a large extent. That is why it is

worth to stress at this point that the recent approaches in this field are not

new. Rather they are based on ideas that have been formalized already a long

time ago, starting with the work of Bernanke and Gertler (1989).

There is much to show concerning the extent to which financial frictions

are capable of having an important impact on the transmission mechanism of

shocks. One motivating observation is that the flows of credit and debt in

general are highly procyclical. As shown in the top panel of Figure 15 in the

appendix, credit growth moves closely with the business cycle. In particular,

the growth rate of debt declines significantly during recessions.

The cyclical properties of financial markets can be seen not only by the

aggregate dynamics of credit flows, but also by indicators of tightening credit

standards (see for instance ECB, 2015 and reports alike). More and more

banks tend to tighten their credit standard during economic downturns.

As Quadrini (2011) highlights, if markets were complete, the financial struc-

ture of individual agents, be it financial intermediaries, firms or households

would be indeterminate. We would then be in a Modigliani and Miller (1958)

INTRODUCING A FINANCIAL ACCELERATOR IN MODUX 5

world and there would not be reasons for financial sector flows to be charac-

terized by some cyclical pattern. However, the fact that financial flows are

highly cyclical (for instance credit flows are highly procyclical whereas the in-

dex of credit standard tightening is highly countercyclical) suggests that the

complete-market paradigm has some limitations.

Of course, from contractions in credit one cannot identify whether it is a

recession in the real economy that causes the decline in credit growth or if

the credit fall causes or amplifies the macroeconomic contraction. Against this

background, it is convenient to distinguish three possible transmission channels

linking real activity and financial flows.

(1) Real activity causes movements in financial flows

(2) Amplification

(3) Financial shocks

Most of the literature in dynamic macrofinance has focused on the second

channel, that is, on the amplification mechanism caused by impediments in

the financial sector. In particular, the key hypothesis is that financial frictions

exacerbate a recession, however, they are not considered as the cause of the

recession. In this context, something wrong happens the real sector in the first

place. This could be caused by exogenous shocks to productivity, the terms-of-

trade, monetary aggregates, interest rates, preferences, etc. These structural

innovations would trigger a macroeconomic contraction even in the absence of

financial market frictions. When financial frictions are prevalent, however, the

magnitude of the contraction becomes more pronounced.

The third channel, that is, the analysis of financial shocks as a source of

real economic fluctuations, has received less attention in the academic litera-

ture (with the exception of the work of Hyman Philip Minski), though more

recently, more and more studies started to explore this possibility.

2.1. The financial accelerator in more detail. The role of a financial

sector block in macroeconomic models is to take account of the comovements

of credit, asset prices and real economic activity that typically characterizes a

6 INTRODUCING A FINANCIAL ACCELERATOR IN MODUX

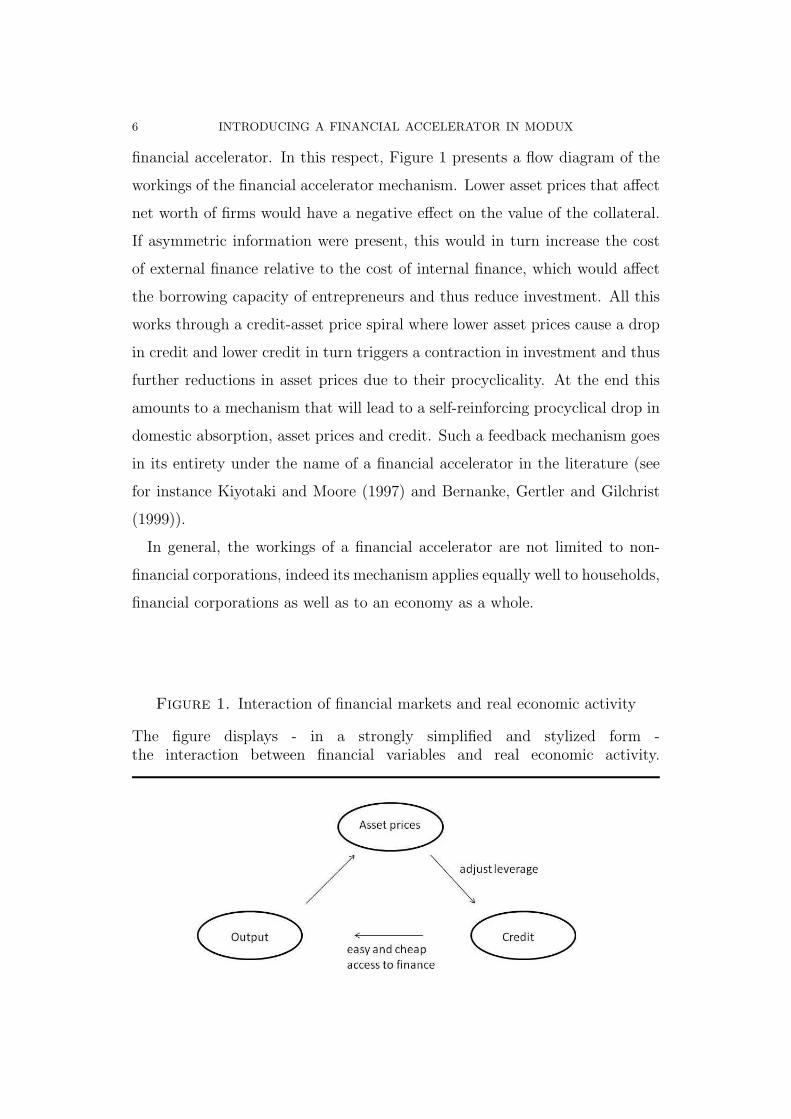

financial accelerator. In this respect, Figure 1 presents a flow diagram of the

workings of the financial accelerator mechanism. Lower asset prices that affect

net worth of firms would have a negative effect on the value of the collateral.

If asymmetric information were present, this would in turn increase the cost

of external finance relative to the cost of internal finance, which would affect

the borrowing capacity of entrepreneurs and thus reduce investment. All this

works through a credit-asset price spiral where lower asset prices cause a drop

in credit and lower credit in turn triggers a contraction in investment and thus

further reductions in asset prices due to their procyclicality. At the end this

amounts to a mechanism that will lead to a self-reinforcing procyclical drop in

domestic absorption, asset prices and credit. Such a feedback mechanism goes

in its entirety under the name of a financial accelerator in the literature (see

for instance Kiyotaki and Moore (1997) and Bernanke, Gertler and Gilchrist

(1999)).

In general, the workings of a financial accelerator are not limited to non-

financial corporations, indeed its mechanism applies equally well to households,

financial corporations as well as to an economy as a whole.

Figure 1. Interaction of financial markets and real economic activity

The figure displays - in a strongly simplified and stylized form -the interaction between financial variables and real economic activity.

INTRODUCING A FINANCIAL ACCELERATOR IN MODUX 7

Standard macroeconomic models usually embed the Modigliani-Miller as-

sumption about perfect capital markets. Hence there is no theoretical role for

modeling the interactions between real and financial factors. However, these

factors are explicitly interconnected in credit channel models where capital

markets are imperfect. An important result from the literature on the credit

channel is that under the presence of information asymmetries, firms are likely

to finance investment projects using internal funds (for instance retained earn-

ings) rather than drawing on external finance. Put differently, external finance

is more costly than internal finance. This difference is called the external fi-

nance premium, which is essentially a markup over the price of internal finance.

This premium arises due to various frictions, as for instance, external lenders

cannot perfectly observe nor control the risks that a project inherits to which

a bank supplies funds for to borrowers. Hence lenders require a compensation

for the expected agency costs. Borrowers using internal funds do not face the

problem of informational asymmetry. Agency costs on the one hand and the

external finance premium on the other are likely to vary with borrowers cred-

itworthiness. For instance, the stake of a borrower in a project - measured by

the degree to which the borrower is able to finance the project using internal

funds - can provide a signal of the unobserved risk of lending (the adverse se-

lection effect), which may affect the borrowers likely incentive to act diligently

(the moral hazard effect) and the incentive to report project outcomes truth-

fully. This relationship between financial health in the corporate sector and

expected agency costs in lending can provide a direct link between the overall

financial conditions and real economic activity.

The key innovation in financial accelerator models is that they embed the

problem of information asymmetries in a standard macroeconomic model. The

key element in these models is the introduction of entrepreneurial net worth,

which basically comes from retained earnings. Shocks to net worth relative to

total finance requirements generate endogenous changes in agency costs and in

the finance premia for external funds which are charged above risk-free rates.

8 INTRODUCING A FINANCIAL ACCELERATOR IN MODUX

In this set-up, any structural shock is likely to be amplified relative to a model

set-up where the financial accelerator extension is omitted. So far the literature

has focused on two key transmission mechanisms:

(1) Corporate cash flow. An unexpected rise in interest rates which reduces

output exerts downward pressure on corporate cash flow and increases the

share of a given investment project that has to be financed using external

funds. This raises expected agency (default) costs and hence also the external

finance premium. This in turns depresses investment and subsequently also

output, revenues and corporate cash flows.

(2) Asset prices and the value of collateral. Consider an unanticipated mon-

etary tightening which reduces the demand for capital and depresses asset

prices. This lowers the value of corporate collateral which is available to back

loans. This in turn raises the external finance premium which reduces current

investment and subsequently output, revenues and corporate cash flows. Any

expectations of future drops in cash flows can amplify the current movement

in (forward-looking) asset prices and hence exacerbate the downturn.

The model developed in Bernanke et al. (1999) incorporates both of these

transmission mechanisms in a standard new Keynesian model. In their set-up,

households work, consume and invest their savings in a financial intermediary.

The financial intermediary pools savings and lends to corporates. These cor-

porates produce goods which are sold in competitive markets using labour and

capital, with the capital stock being financed from internal funds (net worth

which is built up from retained earnings) and/or external funds. Production is

bought by retailers who differentiate goods and sell them in monopolistically

competitive markets which gives rise to price stickiness, as in Calvo (1983).

The monetary authority uses a simple forward-looking interest rate rule to

stabilize inflation.

Given the standard nature of many parts of the Bernanke et al. (1999)

model, I focus here exclusively on the key innovation in the capital/investment

block. In a standard model, without financial accelerator effects, firms would

INTRODUCING A FINANCIAL ACCELERATOR IN MODUX 9

increase their capital stock until the expected return on capital (Rkt+1) was

equal to the opportunity cost of funds (Rt+1). However, in the model with

the financial accelerator extension, the financial health of firms matters for the

cost of finance. In particular, it endogenously reacts to the level of corporate

internal funds (net worth, Nt) relative to total financing requirements (QtKt),

where Q and K are the price and quantity of capital respectively. Firms finance

the value of their capital stock QtKt out of their net worth Nt and with bank

loans Lt, which gives rise to the following balance sheet:

(1) QtKt = Lt + Nt

If a substantial share of corporate investment is funded internally - that is,

borrowing and capital gearing is low - then the external finance premium is

small (in fact, it would tend to zero if the capital stock were to be fully financed

internally or collateralized). However, if corporate investment is primarily

financed through external funds (gearing is high), then the premium is likely

to be high. This relationship is captured by the following equation:

(2) Et

!

Rk

t+1

"

= f

#

QtKt

Nt

$

Rt+1, with f ′(·) > 0

Equation (2) shows that the external finance premium f (QtKt/Nt) increases

with the share of debt in total financing. The intuition behind that is that

the intermediary’s participation constraint in the optimal financial contract

involving lenders and borrowers requires a premium sufficient so as to offset the

greater likelihood that the borrower will declare default. In this case the lender

will incur default costs from the loan. Moreover, the steady state position of the

corporate sector is essential for the responses of net worth, the cost of finance

and investment to structural shocks. For a highly-geared entrepreneur, a shock

to the project return will have a far more marked impact on internal funds and

hence on the external finance premium than for a firm that has low gearing.

This additional element introduces a higher amplitude and persistence of key

10 INTRODUCING A FINANCIAL ACCELERATOR IN MODUX

variables in reaction to structural shocks. The model therefore provides a

theoretical foundation for the observation that more indebted economies tend

to be more vulnerable to adverse shocks.

2.2. Implications of the financial accelerator. A good way of analyzing

the working of the financial accelerator is by means of a monetary policy shock

since this structural disturbance has produced a wide consensus of opinion

about how the macroeconomy is likely to react.

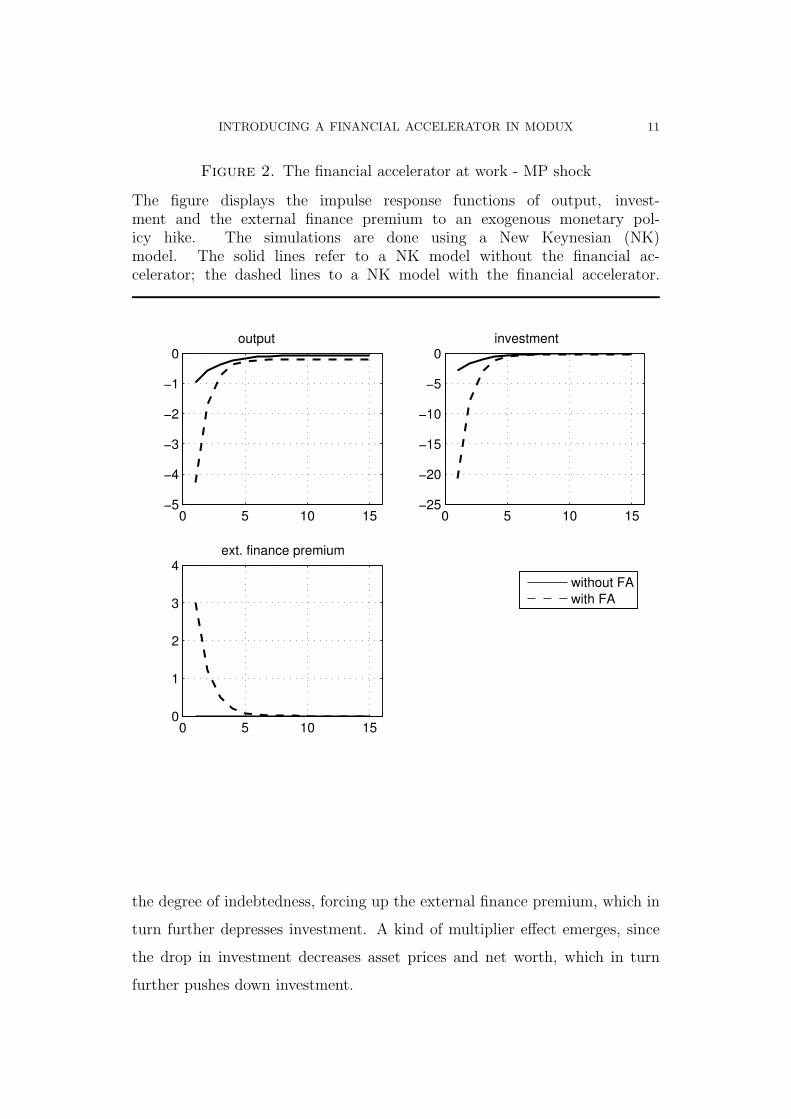

For this, Figure 2 reports the impulse response functions. The time units

in the figure are to be interpreted as quarters. In each picture the solid line

designates the baseline impulse response, generated by a model without the

financial accelerator extension. The dashed line in each picture indicates the

response observed in the model with the financial accelerator included.

The shock considered in Figure 2 is an unanticipated 25 basis point (on

an annual basis) increase in the nominal interest rate. The graphs show the

reaction of output, investment and the external finance premium. The first

thing to note is that although the extension of the basic model with credit-

market frictions does not affect the shape of the impulse response functions,

it does lead to a stronger response of the variables. In particular, with the

financial accelerator included, the initial reaction of output to the monetary

shock is about 50% higher, and the effect on investment is nearly twice as

high. Furthermore, the persistence of the real effects is notably larger in the

presence of the credit-market frictions, that is, output and investment in the

model with financial-market imperfections after four quarters are about where

they are in the base model already after two quarters.

The impact of the financial accelerator can be inspected by considering the

behavior of the external finance premium, which is passive in the baseline

model (by construction), however, it increases sharply in the extended model.

The unanticipated rise in the monetary policy rate dampens the demand for

capital and investment. This depresses investment and the price of capital.

The unanticipated decrease in asset prices lowers net worth and hence increases

INTRODUCING A FINANCIAL ACCELERATOR IN MODUX 11

Figure 2. The financial accelerator at work - MP shock

The figure displays the impulse response functions of output, invest-ment and the external finance premium to an exogenous monetary pol-icy hike. The simulations are done using a New Keynesian (NK)model. The solid lines refer to a NK model without the financial ac-celerator; the dashed lines to a NK model with the financial accelerator.

0 5 10 15−5

−4

−3

−2

−1

0output

0 5 10 15−25

−20

−15

−10

−5

0investment

0 5 10 150

1

2

3

4ext. finance premium

without FAwith FA

the degree of indebtedness, forcing up the external finance premium, which in

turn further depresses investment. A kind of multiplier effect emerges, since

the drop in investment decreases asset prices and net worth, which in turn

further pushes down investment.

12 INTRODUCING A FINANCIAL ACCELERATOR IN MODUX

Figure 3. The financial accelerator at work - demand shock

The figure displays the impulse response functions of output, invest-ment and the external finance premium to an expansionary demandshock. The simulations are done using a New Keynesian (NK) model.The solid lines refer to a NK model without the financial accelera-tor; the dashed lines to a NK model with the financial accelerator.

0 5 10 150

0.01

0.02

0.03output

0 5 10 15−0.05

0

0.05

0.1

0.15

0.2investment

0 5 10 15−15

−10

−5

0

5x 10

−3 ext. finance premium

without FAwith FA

Figure 3 shows the working of the financial accelerator to a classical demand

shock in the form of an increase in government spending which is deficit fi-

nanced. Also in this case the model extension is associated with a stronger

reaction of the model’s variables in response to the structural innovation.

The financial accelerator tends to augment economic fluctuations in both

directions - contractionary shock lead to a more pronounced decline in output

whereas expansionary shocks trigger a stronger positive reaction in output

INTRODUCING A FINANCIAL ACCELERATOR IN MODUX 13

compared to a model without the financial accelerator extension. The key

mechanism behind that is the countercyclical nature of the external finance

premium. It increases in downswings which gives an additional impetus to

the contraction as it increases the cost of financing. The external finance

premium decreases instead in response to an expansionary shock, which exerts

downward pressure on the cost of finance. This in turn spurs investment and

hence capital and output.

3. Methodology: equation specification and estimation

As far as the specification of the financial block’s equations is concerned, the

approach followed here closely relates to Hendry (1993), though it clearly is

more restrictive than indicated by a completely a-theoretical modeling strat-

egy. Thus, as a backdrop for model design it was sought to start out with the

most general specification given support by what a priori was perceived to be

reasonably adequate, and then to simplify down to a parsimonious represen-

tation. In an ideal set-up, the process of reduction should take place within

the framework of a simultaneous equation system. However, a general lack of

degrees of freedom due to short time series makes such an approach unfeasible

and limits the modeling strategies.

The model extension discussed here has been designed and estimated by

following a pragmatic view. Thus, I have neither adopted a pure top-down

approach where data is allowed to determine the outcome of the new equation

system all alone, nor a pure bottom-up approach where a structure motivated

by economic theory is imposed on the equations system without taking proper

account of data. Instead I undertake something in between, where the data

and the theory are combined in an attempt of identifying the structure that

best explains the observed fluctuation of the data. In this set-up, theory

contributes by constructing a theoretical possibility set, while the data play a

role in choosing among the alternatives spanned by the theoretically motivated

possibility set.

14 INTRODUCING A FINANCIAL ACCELERATOR IN MODUX

The starting point is the equation for the real capital stock in the sector for

machinery and equipment that has so far been used in Modux. The equation

is replicated here once more for convenience.

The stock of capital - original equation

∆ log(capbmeq rt) = −0.007[−1.67]

+ 0.41[2.57]

· ∆ log(capbmeq rt−1) + 0.06[1.28]

· ∆ log(vabprvo rt)(3)

− 0.05[−3.31]

·

%

log

#

capbmeq rt−1

vabprvo rt−1

$

+ 0.6 · log(pucmeqt−1/p vabprvot−1)

&

− 0.02[−1.96]

· ∆(pucmeqt−1/p vabprvot−1) + ϵcapbmeq rt

OLS, R2 = 0.81, σcapbmeq r = 0.01

T = 1980 : 2014, DW = 2.39

The values in brackets are t-statistics. The fit of this specification can be

judged graphically in Figure 8. The overall capability of the equation in ex-

plaining the variation in the capital stock is good, the adjusted R-squared is

sufficiently high and the independent variables’ coefficients are all statistically

different form zero with high probability. Of course all this has to be taken

with caution as the degrees of freedom are rather small. This critique also

applies to the upcoming regressions. Nevertheless, the equation is incapable of

explaining the change in the capital stock in several episodes sufficiently well.

One of these episodes is the one of the global financial crisis episode. Once

using dummies for the outliers in the year 2011 and onwards, the fit of the

equation can be significantly improved, however, at the cost of loosing degrees

of freedom.

Moreover, the extent to which the fit of the equation for capital can be

improved by adding dummy variables does not imply that the fit of the overall

model improves - the unexplainable episodes have simply been dummied out.

Hence equation (3) will be substituted by a new set-up involving financial

variables. This implies that the model will feature additional equations which

are not yet part of the equation system.

INTRODUCING A FINANCIAL ACCELERATOR IN MODUX 15

3.1. The equations comprising the financial accelerator extension.

The key aspect of the financial accelerator is its characterization of an asset-

credit spiral which mutually reinforce each other. This implies that assets - in

the following specification asset will be measured by the value of the capital

stock - will depend on credit and the stock of credit in turn will be affected

by the capital stock. Ideally this simultaneous equations system consisting of

the capital stock and the corporate credit stock would be estimated within a

simultaneous equations set-up. This would establish a consistent estimation

of the block of equations comprising the financial accelerator. However, the

lack of sufficiently long time-series does not allow for this approach. Instead I

proceed by estimating each equation individually.

The extension of Modux comprises three equations of which two are in fact

new, whereas the one for the real capital stock is only modified. The following

lists the equations in their VECM representation.

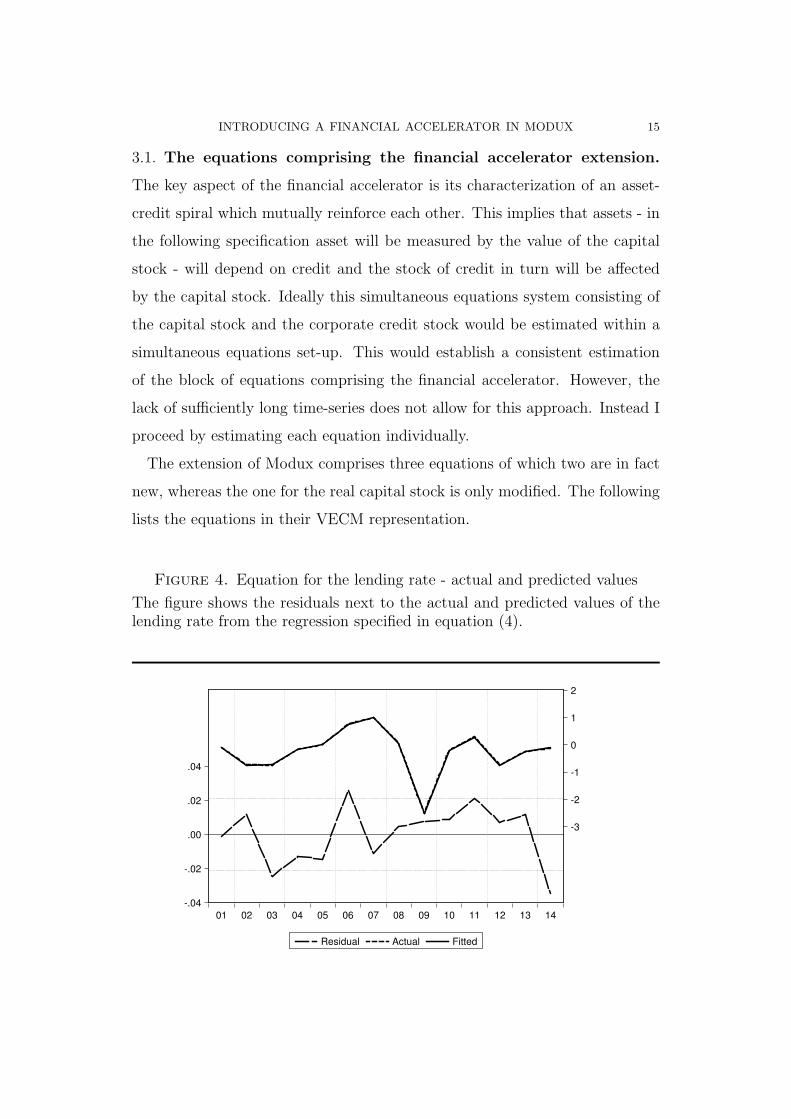

Figure 4. Equation for the lending rate - actual and predicted values

The figure shows the residuals next to the actual and predicted values of thelending rate from the regression specified in equation (4).

-.04

-.02

.00

.02

.04

-3

-2

-1

0

1

2

01 02 03 04 05 06 07 08 09 10 11 12 13 14

Residual Actual Fitted

16 INTRODUCING A FINANCIAL ACCELERATOR IN MODUX

The lending rate

∆credit ratet = 0.73[26.3]

· ∆ticteurt − 0.10[−3.07]

· ∆(credit ratet−1) − 0.14[−2.19]

· cwKt(4)

− 0.12[−2.28]

·!

credit ratet−1 − ticteurt−1 − 1.32 + 0.15 · cwKt−2

"

+ ϵcredit ratet

OLS, R2 = 0.99, σcredit rate = 0.08,

T = 1999 : 2014, DW = 1.98,

The credit rate is modeled as a vector-error-correction equation involving

the short term government bond rate (ticteur) and a measure for the credit-

worthiness in the machinery & equipment sector (cwKt ) given by:

(5) cwK

t :=capbmeq rt · p imeqt

credit nfct/1000

The cointegration relation implies that in the long term, the credit rate

moves one to one with short term rates; however, there is a constant markup

of around 1.3 percentage points which can be considered as an exogenous

lending margin which is supposed to be time-invariant. Moreover, a leverage

being too high also exerts upward pressure on the lending rate in the long

term. An increase in the degree of indebtedness implies a fall in cwKt . While

there is full pass-through of changes in short term-rates on lending rates in the

long run, the short run pass-through is 0.73. Still, the short term dynamics

are driven to a large extent by the short term rate, however at a limited degree

compared to the long-run trade off. Besides that, also the lagged lending rate

as well as the degree of indebtedness play a role in explaining the variation in

the credit rate. Figure 4 shows the fit of the model graphically.

Equation (4) is estimated. In several models (Hammerland et al., 2014;

Bardsen and Nymoen, 2009; Bardasen et al., 2006 and Bardsen et al., 2005)

this equation is calibrated instead. Still the estimated parameters here are

similar to those approaches where they were calibrated instead.

INTRODUCING A FINANCIAL ACCELERATOR IN MODUX 17

The stock of credit for non-financial corporations

∆ log(credit nfct/p imeqt) = 0.63[3.69]

+ 0.01[1.97]

· ogt − 0.32[−4.27]

· ∆(credit ratet − ticteurt)(6)

− 0.36[−3.54]

· [log(credit nfct−1/p imeqt−1) − 2.21 · log(capbmeq rt−1)

+ 0.96 · (credit ratet−1 − ticteurt−1)] + ϵcredit nfct

OLS, R2 = 0.84, σcredit nfc = 0.05

T = 1999 : 2014, DW = 1.67

The stock of credit is modeled using a risk spread involving the credit and the

short term rate (credit rate− ticteur), the capital stock used in the machinery

& equipment sector (capbmeq r) as well as the overall output gap (og). In the

long term an increase in the capital stock of one percent implies a rather

strong increase in (real) credit of around two percent. However, high credit

rates, as well as an overall high level of risk, captured by the spread between

credit and short term rates, dampen the demand for credit. The risk measure

also matters for short term dynamics - high risk exerts downward pressure on

credit demand, though the effect tends to be a bit weaker here than within the

long term relationship. Finally, the output gap also contributes significantly

to explaining the variation in the stock of real credit. A high output gap -

implying that the economy is operating above its potential - triggers upward

pressure on the credit stock.

Figure 5 shows the fit of the equation for the credit stock graphically.

The stock of capital

∆ log(capbmeq rt) = 0.05[28.1]

− 0.02[−2.58]

· ∆(credit ratet − ticteurt)(7)

− 0.07[−4.35]

·

%

log

#

capbmeq rt−1

vabprvo rt−1

$

− 0.09 · log(credit nfct−1/p imeqt−1)

&

+ ϵcapbmeq rt

OLS, R2 = 0.62, σcapbmeq r = 0.006

T = 1999 : 2014, DW = 1.44

18 INTRODUCING A FINANCIAL ACCELERATOR IN MODUX

Figure 5. Equation for the credit stock - actual and predicted values

The figure shows the residuals next to the actual and predicted values of thecredit stock from the regression specified in equation (6).

-.12

-.08

-.04

.00

.04

.08

-.2

-.1

.0

.1

.2

.3

.4

00 01 02 03 04 05 06 07 08 09 10 11 12 13 14

Residual Actual Fitted

The equation for the capital stock (capbmeq r) involves the value added from

the private, non financial sector (vabprvo r), the stock of credit measured in

real terms (credit nfc) as well as the spread between the credit rate and the

short term rate (credit rate− ticteur). The cointegration relationship implies

that in the long term, the real capital stock moves one-to-one with the output

produced in this sector. This trade-off has not been estimated but imposed on

the long term interaction. A full estimation of the cointegration relationship

would yield a value of 0.83 rather than unity for the output variable. The

cointegration relationship also involves the real stock of credit. An increase in

credit of one percent implies a rise in the capital stock of 0.09 percent. The

effect seems weak, though, it is reasonable. Considering that the yearly growth

rate of the capital stock is in the range of 2% to 6% and that of the real stock

of credit of -12% to 36%, then the seemingly small parameter estimate for the

credit stock still turns out to be economically important.

INTRODUCING A FINANCIAL ACCELERATOR IN MODUX 19

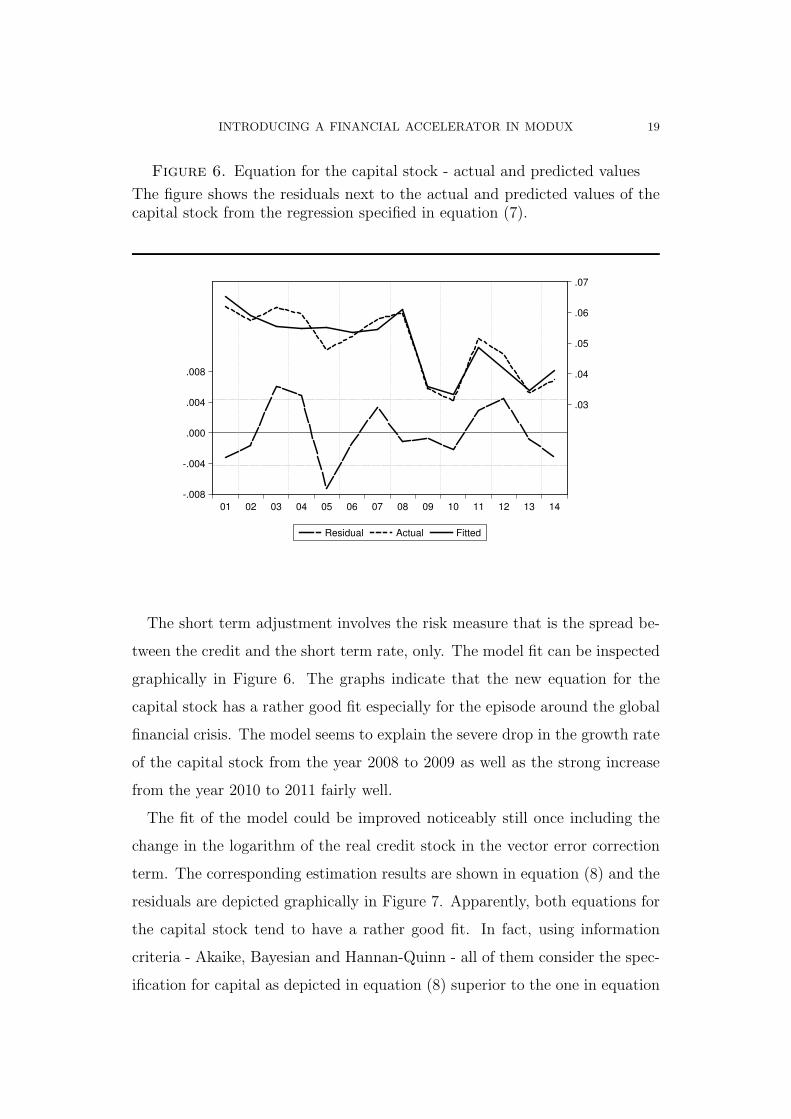

Figure 6. Equation for the capital stock - actual and predicted values

The figure shows the residuals next to the actual and predicted values of thecapital stock from the regression specified in equation (7).

-.008

-.004

.000

.004

.008

.03

.04

.05

.06

.07

01 02 03 04 05 06 07 08 09 10 11 12 13 14

Residual Actual Fitted

The short term adjustment involves the risk measure that is the spread be-

tween the credit and the short term rate, only. The model fit can be inspected

graphically in Figure 6. The graphs indicate that the new equation for the

capital stock has a rather good fit especially for the episode around the global

financial crisis. The model seems to explain the severe drop in the growth rate

of the capital stock from the year 2008 to 2009 as well as the strong increase

from the year 2010 to 2011 fairly well.

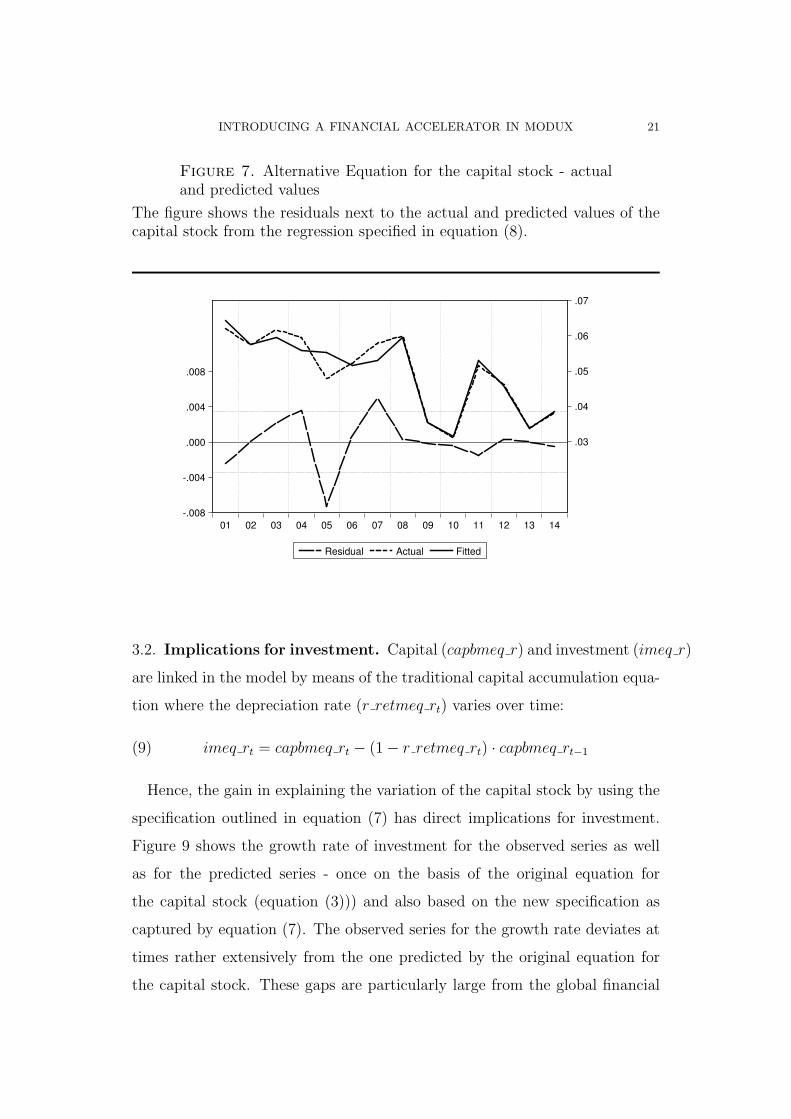

The fit of the model could be improved noticeably still once including the

change in the logarithm of the real credit stock in the vector error correction

term. The corresponding estimation results are shown in equation (8) and the

residuals are depicted graphically in Figure 7. Apparently, both equations for

the capital stock tend to have a rather good fit. In fact, using information

criteria - Akaike, Bayesian and Hannan-Quinn - all of them consider the spec-

ification for capital as depicted in equation (8) superior to the one in equation

20 INTRODUCING A FINANCIAL ACCELERATOR IN MODUX

(7). The better fit can also be motivated by the higher adjusted R-squared

of the specification in equation (8). However, I give preference to equation

(7) since its alternative, equation (8), involves two additional exogenous vari-

ables. Against the background that the sample size is rather small, equation

(7) is hence considered as the new equation for the capital stock involving the

financial accelerator.

The stock of capital - alternative equation

∆ log(capbmeq rt) = 0.05[36.3]

− 0.02[−5.44]

· ∆(credit ratet − ticteurt)(8)

− 0.10[−8.27]

·

%

log

#

capbmeq rt−1

vabprvo rt−1

$

− 0.09 · log(credit nfct−1/p imeqt−1)

&

− 0.01[−2.17]

· ∆(credit ratet−1 − ticteurt−1)

− 0.02[−1.83]

· ∆ log(credit nfct/p imeqt) + ϵcapbmeq rt

OLS, R2 = 0.91, σcapbmeq r = 0.003

T = 1999 : 2014, DW = 2.29

The fit of the different models in terms of their overall fit can also be judged

graphically by means of the corresponding residuals, depicted in Figure 8. The

specifications for capital as outlined in equations (7)-(8) imply rather similar

errors in terms of their time pattern as well as in terms of their standard

deviation. The difference to the residuals to the original specification - outlined

in equation (3) - is particularly large in the years from 2008 and onwards.

Before that episode the path of the residuals of the three specifications is

fairly similar, except maybe for the year 2005. However, from 2008 onwards,

the difference in the residuals of the original equation to the ones of the two

new specifications is remarkable. It highlights the extent to which the overall

fit can be improved by introducing financial variables, even by the specification

as outlined in equation (7) which estimates only three parameters compared

to five as is the case in the original specification.

INTRODUCING A FINANCIAL ACCELERATOR IN MODUX 21

Figure 7. Alternative Equation for the capital stock - actualand predicted values

The figure shows the residuals next to the actual and predicted values of thecapital stock from the regression specified in equation (8).

-.008

-.004

.000

.004

.008

.03

.04

.05

.06

.07

01 02 03 04 05 06 07 08 09 10 11 12 13 14

Residual Actual Fitted

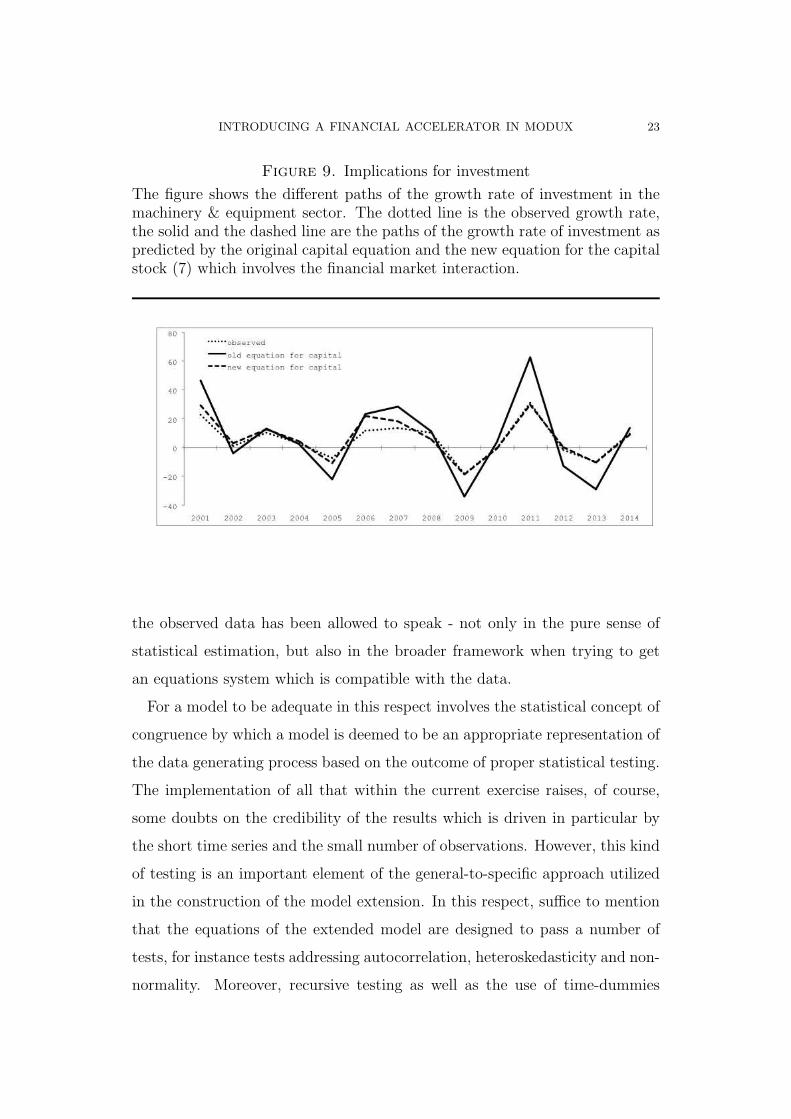

3.2. Implications for investment. Capital (capbmeq r) and investment (imeq r)

are linked in the model by means of the traditional capital accumulation equa-

tion where the depreciation rate (r retmeq rt) varies over time:

(9) imeq rt = capbmeq rt − (1 − r retmeq rt) · capbmeq rt−1

Hence, the gain in explaining the variation of the capital stock by using the

specification outlined in equation (7) has direct implications for investment.

Figure 9 shows the growth rate of investment for the observed series as well

as for the predicted series - once on the basis of the original equation for

the capital stock (equation (3))) and also based on the new specification as

captured by equation (7). The observed series for the growth rate deviates at

times rather extensively from the one predicted by the original equation for

the capital stock. These gaps are particularly large from the global financial

22 INTRODUCING A FINANCIAL ACCELERATOR IN MODUX

Figure 8. Comparing the residuals of the different specifications

The figure shows the residuals of the original specification for capital (equation(3)) as well as the residuals for the specification in (7) as well as equation (8).

2000 2002 2004 2006 2008 2010 2012 2014−0.015

−0.01

−0.005

0

0.005

0.01

0.015

0.02

based on equation (8)based on equation (7)original equation (3)

crisis onwards. Before that episode the gap is moderate. The series of the

growth rate of investment based on the new equation for the capital stock

behaves as good as the old growth series for investment until the global financial

crisis came up. In fact, the difference between the two predicted series is

fairly small until and including the year 2008. However, from the year 2009

onwards, the investment growth rate based on the new equation - using eye-

ball-econometrics at this stage - tends to have a better fit.

To summarize, the model extension developed in this section has been de-

signed and estimated by relying extensively on the general-to-specific approach

of Hendry (1993) and using a classical estimation methodology without impos-

ing a priori restrictions on the parameters of the model. Against this back-

ground the model can thus be considered to be the outcome of a process where

INTRODUCING A FINANCIAL ACCELERATOR IN MODUX 23

Figure 9. Implications for investment

The figure shows the different paths of the growth rate of investment in themachinery & equipment sector. The dotted line is the observed growth rate,the solid and the dashed line are the paths of the growth rate of investment aspredicted by the original capital equation and the new equation for the capitalstock (7) which involves the financial market interaction.

the observed data has been allowed to speak - not only in the pure sense of

statistical estimation, but also in the broader framework when trying to get

an equations system which is compatible with the data.

For a model to be adequate in this respect involves the statistical concept of

congruence by which a model is deemed to be an appropriate representation of

the data generating process based on the outcome of proper statistical testing.

The implementation of all that within the current exercise raises, of course,

some doubts on the credibility of the results which is driven in particular by

the short time series and the small number of observations. However, this kind

of testing is an important element of the general-to-specific approach utilized

in the construction of the model extension. In this respect, suffice to mention

that the equations of the extended model are designed to pass a number of

tests, for instance tests addressing autocorrelation, heteroskedasticity and non-

normality. Moreover, recursive testing as well as the use of time-dummies

24 INTRODUCING A FINANCIAL ACCELERATOR IN MODUX

shows that the sub-system as well as the individual equations of the model

extension are stable and not subject to structural breaks.

3.3. The working of the financial accelerator. The mechanism of the

financial accelerator within the new equations system can best be seen once

the steady state of the three new equations is considered - they are replicated

here once more for convenience:

credit rate = 1.32 + ticteur − 0.15 · cwK(10)

where cwK ∝capbmeq r · p imeq

credit nfc

log

#

credit nfc

p imeq

$

= 2.21 · log(capbmeq r)(11)

−0.96 · (credit rate − ticteur)

log(capbmeq r) = log(vabprvo r) + 0.09 · log

#

credit nfc

p imeq

$

(12)

The essential element of a financial accelerator is a continuous dynamic

interaction between financial variables and those of the real macroeconomy.

This is replicated in the above equations system by means of the capital stock

- the variable of the real economic sector - and the credit stock as the variable

from the financial market sector. An increase in the credit stock implies a

higher capital stock as stated by equation (12) and in turn a higher capital

stock implies a higher credit stock as implied by equation (11). This interaction

implies a direct dynamic feedback effect within the model with the consequence

of an overall increase in the volatility of the predicted series. In more details,

a higher volatility could be achieved by both an increase in the periodicity

as well as in the amplitude of the predicted cycles. As far as the financial

accelerator is concerned, the increase in the overall volatility is caused by an

increase in the amplitude of the cycles, whereas the periodicity is basically left

unchanged.

INTRODUCING A FINANCIAL ACCELERATOR IN MODUX 25

The equations set-up given by equations (4)-(7) and their steady state rep-

resentations given by equations (10)-(12) essentially give rise to two distinct

feedback loops. Consider a hike in capital (capbmeq r) in each case. A higher

capital stock implies an increase in value added in the machinery & equipment

sector and hence in GDP. This in turn implies a higher output gap (og) since

potential output tends to react with a lag to increases in the capital stock.

The higher output gap exerts upward pressure on the credit stock as given by

equation (6) which in turn again increases the capital stock and the loop starts

again from the beginning.

(13) capbmeq r ↑→ (vabprvo r, GDP ) ↑→ og ↑→ credit nfc ↑→ capbmeq r ↑

The second loop operates by means of equations (2) and (4). Again consider

an increase in the capital stock. A higher capital stock implies a higher cred-

itworthiness of borrowers from the point of view of lenders. Hence lenders are

willing to offer new credit at a lower price which is characterized by equation

(4). The lower lending rate exerts upward pressure on credit demand which in

turn pushes up the capital stock and the loop starts from the beginning again.

(14) capbmeq r ↑→ cwK ↑→ credit rate ↓→ credit nfc ↑→ capmeq r ↑

Within the dynamic interaction, the risk measure - as captured by the spread

between the lending and the short government bond rate - plays a key role as

it strongly affects both the credit stock as well as the capital stock. Equation

(11) is an attempt to empirically replicate equation (2) from the theory on

financial frictions. The credit spread hence can be considered as the empirical

pendant to the theoretically motivated concept of the external finance pre-

mium. The external finance premium is generally positive, as is the spread

between lending and short term government bond rates as depicted in Figure

15. Moreover, the theory predicts that the external finance premium that a

borrower must pay should depend inversely on the strength of the borrower’s

26 INTRODUCING A FINANCIAL ACCELERATOR IN MODUX

financial position, measured in terms of factors such as net worth, liquidity, and

current and future expected cash flows. Fundamentally, a financially strong

borrower has more skin in the game, so to speak, and consequently has greater

incentives to make well-informed investment choices and to take the actions

needed to ensure good financial outcomes. Because of the good incentives that

flow from the borrower’s having a significant stake in the enterprise and the

associated reduction in the need for intensive evaluation and monitoring by the

lender, borrowers in good financial condition generally pay a lower premium

for external finance.

The inverse relationship of the external finance premium and the financial

condition of borrowers creates a channel through which otherwise short-lived

economic shocks may have long-lasting effects. The borrowers’ financial con-

dition is empirically modeled by the ratio of the capital stock to the credit

stock; Figure 15 shows its path over time. An increase in capital relative to

the credit stock triggers a fall in the credit spread. This in turn exerts up-

ward pressure on credit and hence on the capital stock, which together will

cause further changes in the credit spread. This dynamic interaction of credit

spreads, the credit stock and the capital stock comprise the essence of the

financial accelerator, replicated in a structural macroeconometric model.

The persistence in the spreads provides an additional source of dynamics.

An increase in the risk premium - triggered either by an increase in the credit

rate or by a fall in the short term rate - implies an immediate negative impact

on the credit stock. This is passed on the capital stock in the form of a

decline therein. To the extent that credit is procyclical, the external finance

premium will be countercyclical, enhancing the swings in borrowing and thus

in investment, spending, and production.

The model’s extension by means of a financial accelerator as motivated by

the previous equations has been done using real variables, e.g. the real value of

the credit stock and the capital stock. This is in accordance with other studies

that use a Bernanke et al. (1999) framework and debt contracts which are

INTRODUCING A FINANCIAL ACCELERATOR IN MODUX 27

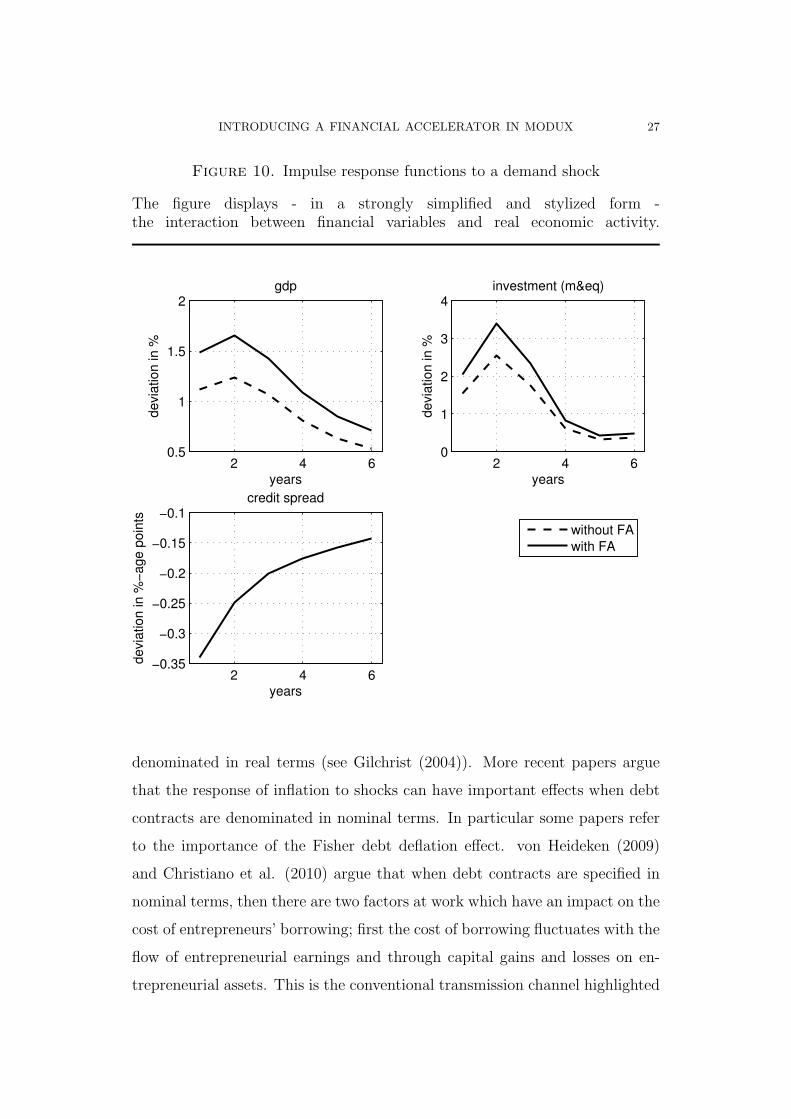

Figure 10. Impulse response functions to a demand shock

The figure displays - in a strongly simplified and stylized form -the interaction between financial variables and real economic activity.

2 4 60.5

1

1.5

2

years

devi

atio

n in

%

gdp

2 4 60

1

2

3

4

years

devi

atio

n in

%

investment (m&eq)

2 4 6−0.35

−0.3

−0.25

−0.2

−0.15

−0.1

years

devi

atio

n in

%−

age p

oin

ts

credit spread

without FAwith FA

denominated in real terms (see Gilchrist (2004)). More recent papers argue

that the response of inflation to shocks can have important effects when debt

contracts are denominated in nominal terms. In particular some papers refer

to the importance of the Fisher debt deflation effect. von Heideken (2009)

and Christiano et al. (2010) argue that when debt contracts are specified in

nominal terms, then there are two factors at work which have an impact on the

cost of entrepreneurs’ borrowing; first the cost of borrowing fluctuates with the

flow of entrepreneurial earnings and through capital gains and losses on en-

trepreneurial assets. This is the conventional transmission channel highlighted

28 INTRODUCING A FINANCIAL ACCELERATOR IN MODUX

in the Bernanke et al. (1999) framework which tends to amplify the economic

impact of a structural disturbance. However, they also point to a further mech-

anism where entrepreneurs’ obligation to pay debt varies because inflation can

ex post change the real debt burden. This second effect is referred to as a

Fisher debt deflation impact. The Fisher debt deflation and accelerator type

mechanisms tend to reinforce each other in the case of shocks that move the

inflation rate and output in the same direction, and they tend to be offsetting

in the presence of shocks which move the inflation rate and output in opposite

directions. The presence of a Fisher debt deflation channel tends to cancel out

the amplification impact of the financial accelerator mechanism1. This implies

that the specification of the debt contract has important consequences for the

size of the amplification effect that results from financial impediments when

the economy is subject to supply shocks. Using an approach where capital and

credit are used in nominal terms instead would imply an amplification effect

that is weaker, moreover the overall model fit would be worse than in the case

of using the real measures for the two variables2. For this reason the equations

involving the capital and credit stock have been denominated in real terms in

each case.

3.4. Impulse response function analysis. This section is to show in how

far the model with the financial accelerator extension compares with the orig-

inal one once impulse response functions are considered. In the vein of the

structural shocks which are shown in Figure 2 and 3 by means of a DSGE

model, I proceed by considering a demand shock within Modux (the shock

1Consider a negative productivity shock which triggers a contraction in aggregate supplyand pushes inflation and output in opposite directions. The fall in output pulls down onasset prices and entrepreneurial earnings which pushes up on the cost of borrowing but this isoffset by the impact of inflation on entrepreneurs’ real debt burden which reduces the cost ofborrowing. If debt contracts are agreed in nominal terms the rise in inflation in response tothe shock reduces the real value of entrepreneurs’ outstanding debt. As a result, the externalfinance premium falls because entrepreneurs’ leverage declines as their real debt levels areeroded because of higher inflation. The fall in the external finance premium pushes downon borrowing costs and dampens the negative impact of the supply shock on investment.Thus, the Fisher deflation effect offsets the amplification effect of the financial accelerator.2The results for the regressions of equation (4) - (7) are not shown here but available uponrequest.

INTRODUCING A FINANCIAL ACCELERATOR IN MODUX 29

considered is a (variance weighted) foreign demand shock (output in the Euro-

area)). Figure 10 shows the impulse response functions of real GDP, real

investment in the machinery & equipment sector as well as the credit spread

in response to a surprise demand innovation. As expected, the shock causes a

rise in output and investment alike. The investment hike triggers an increase

in the capital stock which then exerts upward pressure on the creditworthiness

resulting in a decline in the credit spread. This in turn spurs additional up-

ward pressure on investment and GDP. As a consequence of that, the reaction

of investment and output is stronger in the case the financial accelerator ex-

tension is included relative to the version of Modux where the financial market

interaction is omitted.

The difference in the impulse response functions of the empirical model are

moderate as far as GDP is concerned - the gap is around 0.3 percentage points

in the first two years and declines continuously with the horizon. The difference

in the reaction of (real) investment in the machinery & equipment sector is,

however, more pronounced, in particular in the second year, the gap is around

0.9 percentage points.

Care has to be taken in comparing the impulse response functions of the

DSGE model with those of the empirical model. The DSGE model is calibrated

using standard values. It is not specifically targeted towards the Luxembour-

gish economy. Hence the comparison of the impulse response functions is, if

anything, only valid as far as it concerns their shape. A quantitative judgment

would require estimating at least those parameters of the DGSE model which

address the financial accelerator, as they are usually difficult to calibrate.

The empirical model basically replicates the shape of the theoretical model

fairly well, even though the DSGE model’s impulse response functions do not

have a hump-shaped pattern. This could be introduced theoretically by, for

instance, extensions in the form of investment delays or frictions alike address-

ing the accumulation of capital (see for instance Bernanke et al. (1999) for

further details).

30 INTRODUCING A FINANCIAL ACCELERATOR IN MODUX

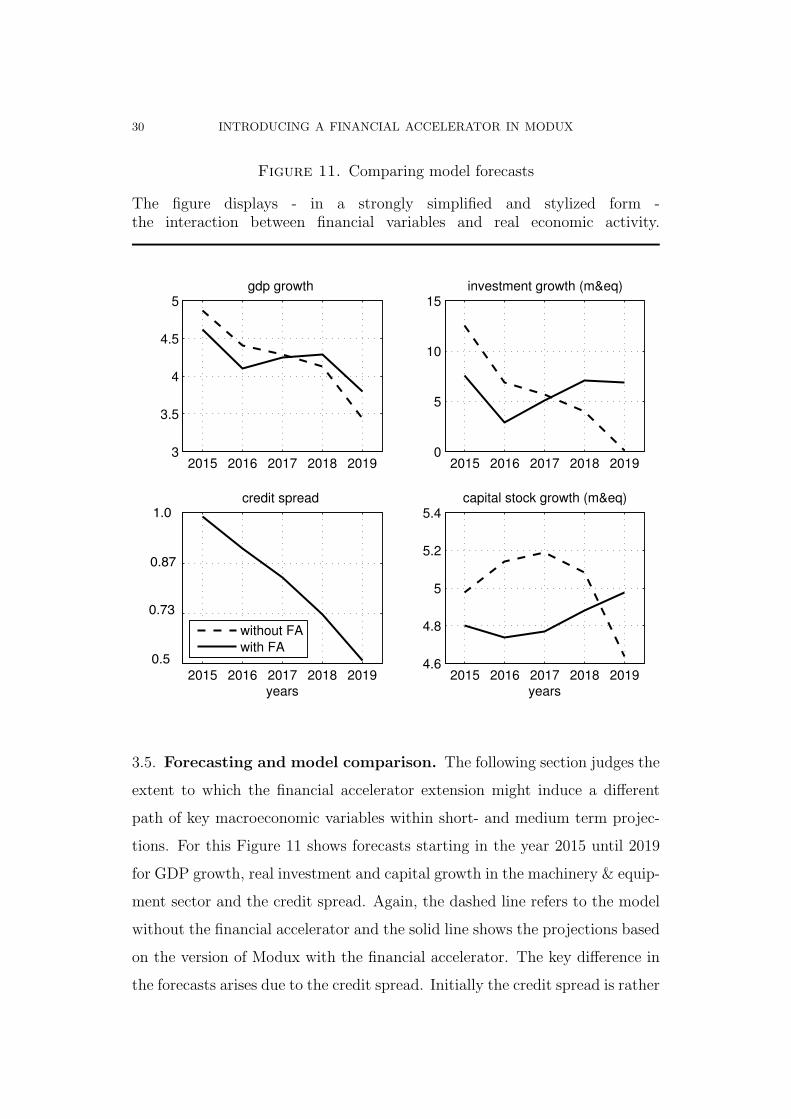

Figure 11. Comparing model forecasts

The figure displays - in a strongly simplified and stylized form -the interaction between financial variables and real economic activity.

2015 2016 2017 2018 20193

3.5

4

4.5

5gdp growth

2015 2016 2017 2018 20190

5

10

15investment growth (m&eq)

2015 2016 2017 2018 20192.5

3

3.5

4

years

credit spread

without FAwith FA

2015 2016 2017 2018 20194.6

4.8

5

5.2

5.4

years

capital stock growth (m&eq)

3.5. Forecasting and model comparison. The following section judges the

extent to which the financial accelerator extension might induce a different

path of key macroeconomic variables within short- and medium term projec-

tions. For this Figure 11 shows forecasts starting in the year 2015 until 2019

for GDP growth, real investment and capital growth in the machinery & equip-

ment sector and the credit spread. Again, the dashed line refers to the model

without the financial accelerator and the solid line shows the projections based

on the version of Modux with the financial accelerator. The key difference in

the forecasts arises due to the credit spread. Initially the credit spread is rather

1.01.0

0.87

0.73

0.5

INTRODUCING A FINANCIAL ACCELERATOR IN MODUX 31

high which causes investment and capital growth to be significantly lower com-

pared to the projections where the financial accelerator has been ignored. The

high credit spread exerts downward pressure on the growth rate of the credit

stock, which in turn implies lower dynamics in capital and investment. This

is replicated also in GDP growth, though the gap between the two models is

low - the growth rates differ by around 0.3 percentage points within the first

three years. However, the continuous decline in the credit spread over time

triggers upward pressure on capital and investment growth. Especially from

2017 onwards the decline in the spread is more pronounced than within the

initial period. As a result this finally triggers a turnaround in the path of the

capital and investment growth rates. After having passed a trough in 2016,

both investment and capital tend to accelerate from 2017 onwards. The gap

in the growth rate comprises a steady increase and tends to be particularly

pronounced in 2019. From then onwards, the gap declines again (not shown

in Figure 11).

The previous discussion compares the dynamic path of the projections with

and without the financial accelerator. However, it does not say anything about

the precision of the forecasts. For this Figures 12 - 14 give some insights in

terms of root-mean-squared-error (rmse) statistics. They show forecast rel-

evant statistics to judge the models in terms of their forecast precision. A

root-mean-squared-error of around 0.8 from the original equation compares to

a value of this statistic of 0.3 for the specification of capital from equation (7)

and a value of 0.1 from the alternative capital equation outlined in equation

(8). In all cases, the extension by means of financial variables tends to im-

prove the forecast precision where the gain is particularly pronounced with the

specification of equation (8).

4. Summary

What has been studied here is an extension to a macroeconometric model

with a block of equations that allows for self-reinforcing comovements between

32 INTRODUCING A FINANCIAL ACCELERATOR IN MODUX

Figure 12. RMSE - original equation for capital

30

40

50

60

70

80

00 01 02 03 04 05 06 07 08 09 10 11 12 13 14

CAPBMEQ_RF – 2 S.E.

Forecast: CAPBMEQ_RF

Actual: CAPBMEQ_R

Forecast sample: 2000 2014

Included observations: 15

Root Mean Squared Error 0.805465

Mean Absolute Error 0.624396

Mean Abs. Percent Error 1.154804

Theil Inequality Coefficient 0.007990

Bias Proportion 0.524076

Variance Proportion 0.282248

Covariance Proportion 0.193675

Figure 13. RMSE - equation (7) for capital

32

36

40

44

48

52

56

60

64

68

72

00 01 02 03 04 05 06 07 08 09 10 11 12 13 14

CAPBMEQ_RF – 2 S.E.

Forecast: CAPBMEQ_RF

Actual: CAPBMEQ_R

Forecast sample: 2000 2014

Included observations: 15

Root Mean Squared Error 0.314124

Mean Absolute Error 0.261552

Mean Abs. Percent Error 0.582673

Theil Inequality Coefficient 0.003098

Bias Proportion 0.005592

Variance Proportion 0.495591

Covariance Proportion 0.498817

Figure 14. RMSE - equation (8) for capital

30

35

40

45

50

55

60

65

70

01 02 03 04 05 06 07 08 09 10 11 12 13 14

CAPBMEQ_RF – 2 S.E.

Forecast: CAPBMEQ_RF

Actual: CAPBMEQ_R

Forecast sample: 2001 2014

Included observations: 14

Root Mean Squared Error 0.102482

Mean Absolute Error 0.084414

Mean Abs. Percent Error 0.180969

Theil Inequality Coefficient 0.000990

Bias Proportion 0.021608

Variance Proportion 0.055842

Covariance Proportion 0.922550

INTRODUCING A FINANCIAL ACCELERATOR IN MODUX 33

the financial sector and real economic activity, often denominated in the liter-

ature as a financial accelerator. The model extension considered here has tried

to integrate a financial accelerator mechanism in a full-fledged macroeconomic

model framework. The working of the financial accelerator has been limited to

the non-financial corporate sector, in particular the machinery & equipment

sector.

Noteworthy, the shape of the impulse response functions of the empirical

model are very much in line with those of DSGE models. This applies both

to the corresponding models with as well as without the financial accelerator

extension. The results for the empirical model show that once the model allows

for macrofinancial interactions, the corresponding financial accelerator effects

contribute to magnify the effects of shocks to the economy. Taken at face

value, this suggests that in the absence of the macrofinancial block, the model

could underestimate the effects of shocks on the macroeconomic level.

As far as economic projection properties are concerned, the extended model

tends to outperform the model without the financial accelerator. In addition

to that the projections of the model with macrofinancial interaction turn out

to be richer in their path. This, of course, at times renders their interpretation

a bit more difficult.

An extension to the work presented here could be the introduction of macro-

financial linkages to sectors other than the one considered here. In particular,

financial accelerator mechanisms could be specified at the household level as

well as for financial corporations.

34 INTRODUCING A FINANCIAL ACCELERATOR IN MODUX

References

[1] Adam, Ferdy, 2004. Modeling a small open economy: What is different? The case of

Luxembourg, available at:

http://www.statistiques.public.lu/en/methodology/definitions/M/Modux/Modux.pdf

[2] Bardsen, G., Ø. Eitrheim, E. S. Jansen and R. Nymoen, 2005. The econometrics of

macroeconomic modelling. Oxford University Press.

[3] Bardsen, G., Lindquist, K. G. and D. P. Tsomocos, 2006. Evaluation of macroeconomic

models for financial stability analysis, Working Paper No. 1, Norges Bank.

[4] Bardsen, G. and R. Nymoen, 2009. Macroeconometric modelling for policy, Ch 17,

Palgrave Handbook of Econometrics Vol. 2, Palgrave Mac-Millan.

[5] Bernanke, Ben and Gertler, Mark, 1989. Agency Costs, Net Worth, and Business

Fluctuations, American Economic Review, American Economic Association, vol. 79(1),

pages 14-31, March.

[6] Bernanke, Ben S., Gertler, Mark and Gilchrist, Simon, 1999. The financial accelerator

in a quantitative business cycle framework, Handbook of Macroeconomics, in: J. B.

Taylor and M. Woodford (ed.), Handbook of Macroeconomics, edition 1, volume 1,

chapter 21, pages 1341-1393 Elsevier.

[7] Calvo, Guillermo A., 1983. Staggered prices in a utility-maximizing framework, Journal

of Monetary Economics, Elsevier, vol. 12(3), pages 383-398, September.

[8] Christiano, Lawrence, Rostagno, Massimo and Motto, Roberto, 2010. Financial factors

in economic fluctuations, Working Paper Series 1192, European Central Bank.

[9] ECB, 2015. The euro area bank lending survey, Third quarter of 2015, available at:

https://www.ecb.europa.eu/stats/pdf/blssurvey 201510.pdf

[10] Gilchrist, S., 2004. Financial Markets and Financial Leverage in a Two-Country World

Economy, Central Banking, Analysis, and Economic Policies Book Series, in: Luis

Antonio Ahumada & J. Rodrigo Fuentes & Norman Loayza (Series Editor) & Klaus

Schmidt-Hebbel (Se (ed.), Banking Market Structure and Monetary Policy, edition 1,

volume 7, chapter 2, pages 027-058 Central Bank of Chile.

[11] Kiyotaki, Nobuhiro and Moore, John, 1997. Credit Cycles, Journal of Political Economy,

University of Chicago Press, vol. 105(2), pages 211-48, April.

[12] Hammersland, Roger and Træe, Cathrine Bolstad, 2014. The financial accelerator and

the real economy: A small macroeconometric model for Norway with financial frictions,

Economic Modelling, Elsevier, vol. 36(C), pages 517-537.

[13] Hammersland, R. and D. H. Jacobsen, 2008. The Financial Accelerator: Evidence using

a procedure of Structural Model Design, Discussion Paper No. 569, Statistics Norway.

INTRODUCING A FINANCIAL ACCELERATOR IN MODUX 35

[14] Hendry, D. F., 1993. Econometrics: Alchemy or Science?, Essays in Econometric

Methodology, Blackwell Publishers, Oxford.

[15] Modigliani, Franco, and Miller, 1958. The Cost of Capital, Corporation Finance and

the Theory of Investment, American Economic Review 48 (3), pages 261-297.

[16] Quadrini, Vincenzo, 2011. Financial frictions in macroeconomic fluctuations, Economic

Quarterly, vol. 97(3), pages 209-254.

[17] von Heideken, V. Q., 2009. How Important are Financial Frictions in the United States

and the Euro Area?, Scandinavian Journal of Economics, Wiley Blackwell, vol. 111(3),

pages 567-596, 09.

36 INTRODUCING A FINANCIAL ACCELERATOR IN MODUX

Appendix A. The data

The following provides some details concerning the data. The extension with

the financial accelerator introduces two new time series into Modux. These are

a measure for the stock of credit to the non financial sector (volume measure)

and a lending rate as the corresponding price measure. The stock of credit

(Credits accordes par les etablissements de credit par contreparties et durees

initiales) is obtained from the following webpage (Banque Central du Luxem-

bourg):

http://www.bcl.lu/fr/statistiques/series statistiques luxembourg/

11 etablissements credit/index.html

and graphically displayed in Figure 15.

The data for the lending rate are obtained from the data-platform www.euro-

area-statistics.org. The chosen credit rate is the short term rate of lending of

large loans to non-financial corporations (Euro-denominated loans over 1 mil-

lion Euros; floating rate or initial rate fixation of up to one years to euro area

non-financial corporations (percentages per annum, rates on new business))

and can be accessed to by:

https://www.euro-area-statistics.org/bank-interest-rates-loans.

The reason for using the short term rate on large loans is due to the fact

that it comprises a time series dating back to the year 1999, whereas all the

alternatives, which at times would indeed be more adequate, begin in the year

2003. Against the background that the horizon covered by the credit stock is

short, I did not want to additionally cut the sample by considering 2003 as the

starting year. Note, however, since all the different measures for the lending

rate are highly correlated (on average above 0.96), the use of any alternative

measure for the lending rate should lead to similar point estimates.

The time series for both the credit rate as well as for the stock of credit are

available on a monthly frequency. I constructed yearly averages for the lending

rate by taking the arithmetic mean across the months of the corresponding

INTRODUCING A FINANCIAL ACCELERATOR IN MODUX 37

years. The credit stock is aggregated to the annual frequency by constructing

the sum over the months which comprise a year.

In addition to that the Figure 15 shows the spread between the credit rate

and the short term government bond rate (subplot no. 4). Finally, the last

subplot shows the path of the measure of the creditworthiness as defined in

equation (5).

Figure 15. The data

2000 2005 2010 20158

9

10credit stock (log−level)

2000 2005 2010 2015−20

0

20

40credit stock growth rate (in %)

2000 2005 2010 20150

2

4

6lending rate (percent per annum)

2000 2005 2010 20150

0.5

1

1.5credit spread (percent per annum)

2000 2005 2010 20153

4

5

6creditworthiness