Embed Size (px)

Citation preview

Cahier de recherche 2018-04

Is the Relation between CSR and Stock Market Valuation Subject to an Institutionalization

Process An International Perspective

Denis Cormier

Eacutecole des sciences de la gestion Universiteacute du Queacutebec agrave Montreacuteal

Chaire drsquoinformation financiegravere et organisationnelle ESG-UQAM

Michel Magnan

Telfer John Molson School of Business

Concordia University

CIRANO

The authors acknowledge financial support of the Social Sciences and Humanities

Research Council (SSHRC) the Chair in Financial and Organizational Performance

(ESG-UQAM) the Stephen A Jarislowsky Chair in Corporate Governance

(Concordia) the Autoriteacute des marcheacutes financiers and the Institute for the Governance

of Private and Public Organizations Helpful comments were received from

workshop participants at ESG-UQAM and Universiteacute de Nice-Sofia Antipolis

1

Is the Relation between CSR and Stock Market Valuation Subject to an

Institutionalization Process An International Perspective

Abstract

In this paper we analyze how similarity in Corporate Social Responsibility (CSR) disclosure

mediates the relation between CSR performance and a firmrsquos stock market valuation For our

purpose CSR disclosure encompasses environmental and social dimensions CSR disclosure

similarity reflects an institutionalization process that favours conformity within a firmrsquos own

national industry rather than distinctiveness We focus on three distinct institutional contexts

Canada France and Germany Our results show that CSR disclosure similarity has a mediating

effect on the relation between CSR performance and stock market valuation albeit higher for

environmental disclosure similarity than for social disclosure similarity Our results also suggest

that it is value relevant for a firm to adopt the institutionalized disclosure structures of its

reference group Finally the CSR disclosure isomorphism appears stronger in Canada than in

Germany and France most likely an outcome of lower coercive and normative pressures in

Canada

Key words Corporate governance corporate social responsibility sustainability environmental

disclosure institutional theory isomorphism social disclosure stock market value value

relevance

2

1 Introduction

This paper investigates how the institutional process that underlies the

formulation of Corporate Social Responsibility disclosure (CSR disclosure) affects the

relation between CSR performance and a firmrsquos stock market value For our purpose

CSR encompasses environmental and social dimensions (eg Gamerschlag Moumlller amp

Verbeeten 2011 Hummel amp Schlick 2016) Essentially we argue that CSR disclosure

mediates the relationship between CSR performance and a firmrsquos stock market value Our

argument rests on the premise that beyond raw CSR performance how a firm discloses

its CSR activities shapes the way that capital marketsrsquo participants read and interpret its

CSR performance Furthermore we argue that the CSR disclosure process has become

increasingly institutionalized which strongly affects its impact on stock market values

Our study builds upon the rise in societal expectations regarding the

environmental and social performance of corporations which has certainly been

spectacular in recent years (Porter amp Kramer 2007) Such pressures by various

stakeholders and society entail a greater scrutiny of corporate social and environmental

practices Feeding these rising expectations are concerns about health (eg Wilson amp

Tisdell 2001) sustainability of supply chains (eg De Brito Carbone amp Blanquart

2008 Linton Klassen amp Jayaraman 2007) climate change (eg Kolk amp Pinske 2008)

or labour working conditions (eg Van Tulder Van Wijk amp Kolk 2009) Ecological

disasters (Solomon Solomon Norton amp Joseph 2011) or human tragedies (eg

Sinkovics Hoque amp Sinkovics 2016 Siddiqui amp Uddin 2016) have also contributed to

putting corporationsrsquo environmental and social practices under the spotlight

Hence various stakeholders are asking firms to account for the social

responsibility of their actions (eg Cormier Gordon amp Magnan 2004 Fernandez-

3

Feijoo Romero amp Ruiz 2014) while investors are seeking to obtain assurance that such

potentially costly accidents do not lurk behind rosy financial reporting (eg Simons amp

De Wilde 2017)1 Over the years these pressures have become increasingly

institutionalized with the emergence of Corporate Social Responsibility (CSR)

environmental or sustainability rankings (eg Corporate Knights) stock market indices

(eg Dow Jones Sustainability Index) measurement and reporting metrics (such as the

Global Reporting Initiative ie GRI) CSR assurance experts (eg environmental

auditors) or management processes (eg ISO 14000)

The response of most corporations to these various pressures has been to enhance

both the quality (eg Marquis Toffel amp Zhou 2016) and the substance (eg Marquis amp

Qian 2014) of their disclosure on these matters (see also Deloitte 2013) emphasizing

social and environmental issues In terms of scale many corporations either listed or

privately-owned now provide extensive CSR or sustainability reports often anchored

within designated spaces within the corporate web site (Cooper amp Owen 2007 PwC

2015) In terms of scope what used to be a relatively simple exercise of listing some

awards and water or air pollution statistics is now a comprehensive data gathering and

communication exercise that encompasses a wide range of issues from CO2 emissions to

subcontractorsrsquo labour working conditions2

Consistent with neo-institutional theory (Scott 1995 DiMaggio amp Powell 1983)

we argue that firms disclosure practices change to isomorphism in a given country within

1Clifford Kraus and John Schwartzmay 2016 Exxon Investors Seek Assurance as Climate Shifts Along

With Attitudes The New York Times May 23 httpswwwnytimescom20160524scienceexxon-

investors-seek-assurance-as-climate-shifts-along-with-attitudeshtml_r=0 Retrieved May 22 2017 2 For example Nike had to take drastic actions following allegations that it relied on subcontractors with

sweatshot-like conditions in its supply chain (Hart amp Milstein 2003)

4

their industry motivated by institutional and competitive mechanisms There are three

types of institutional mechanisms of change towards isomorphism coercive normative

and mimetic (DiMaggio amp Powell 1983) that lead firms to adopt the institutionalized

disclosure structures As a result corporate disclosures become increasingly similar or

homogenous over time This similarity can arise for several reasons However a likely

explanation is the convergence between stakeholdersrsquo expectations about a firmrsquos social

responsibility posture and the need for a firmrsquos directors and managers to ensure that they

meet those expectations in a way that does not expose them to further demands doing the

same as what leaders are doing implies that there is safety in numbers Thus by

respecting institutionalized rules firms adopt similar behaviour as they are more

legitimate independently of their efficiency (Boxenbaum et al 2016) The

institutionalization of CSR disclosure potentially underlies the controversy surrounding

the nature and extent of the relation between CSR performance and a firmrsquos future

financial performance even after decades of research (Clarkson et al 2011 Lys et al

2015) By focusing on the mapping between CSR performance and a firmrsquos stock market

value but introducing CSR disclosure as a mediating variable we revisit the issue using a

comprehensive measure that reflects all salient aspects of a firmrsquos future financial

performance Under such conditions CSR performance as conveyed through CSR

disclosure should have a marginal economic impact In contrast management can use

CSR disclosure to convey useful and relevant information to key stakeholders including

investors further enhancing its quality by obtaining audit assurance on the information

being provided (eg Berthelot Cormier amp Magnan 2003 Moser amp Martin 2012)

5

Under such conditions CSR performance as conveyed through CSR disclosure should

have a positive economic impact

The analysis level of our paper is the organizational field as reflected by an

industry in a given country (Scott 1995) An organizational field is a group of

organizations that constitute a recognized area of institutional life eg organizations that

produce similar services or products (DiMaggio amp Powell 1983) In a complementary

fashion Larrinaga (2007) proposes the existence of some locally based sustainability

report fields (EMAS Triple bottom line ISO 14001 compliance-oriented approach

ldquoBilan Socialrdquo and compulsory environmental disclosure) Hence we examine the

relation between CSR performance and stock market value as mediated by CSR

disclosure in three countries with different institutionalization forces a compliance-

oriented context (Canada) an EMAS sustainability reporting context (Germany) and a

Bilan social context (France) Our data covers the 2012-2014 period We argue that CSR

disclosure follows an institutionalization process characterized by CSR disclosure

isomorphism becoming increasingly homogenous among firms within these countriesrsquo

industries as they strive to adopt the practices of the industry Moreover in light of the

critical importance that CSR disclosure has attained in Western world countries we also

consider how corporate governance public media pressures and a firmrsquos underlying CSR

performance interplay with CSR disclosure changes to isomorphism

Overall we observe a mediating effect of the CSR disclosure similarity process

on the relation between CSR (environmental social) performance and stock market

valuation Normative or coercive isomorphism forces organizations to comply with

changes spearheaded by external agents ie regulation concerning environmental and

6

social issues More specifically we find that the worse (better) a firmrsquos environmental

performance the less (greater) the stock market value as proxied by Tobinrsquos Q for

Canadian (German) firms with environmental disclosure isomorphism playing a

mediating role in Canada but not in Germany Environmental performance does not

directly relate to stock market value for French firms but through environmental

disclosure We also find that the worse (better) a firmrsquos social performance the less

(greater) its stock market value as proxied by Tobinrsquos Q in Canada (Germany) with

social disclosure isomorphism playing a mediating role in Canada but not in Germany

Social performance does not directly relate to stock market value for French firms

Our study provides the following contributions First the paper potentially sheds

some additional light on the debate regarding the debate on the relation between CSR

performance and financial performance We show that the relation is conditional on 1)

the institutional environment in which a firm evolves and the institutionalization forces

which predominate in that setting and 2) the mediating role played by CSR disclosure

similarity which may enhance or attenuate the relation Second our findings offer an

alternative explanation as to how and why firms elaborate their CSR disclosure In

contrast to prior research that focuses on managerial opportunism legitimization attempts

or economic incentives we show that most firms may be seeking anonymity through

uniformity As such by considering CSR disclosure by firms from three countries via the

lens of similarity we extend and further enrich prior work relying on institutional theory

to explain CSR disclosure (eg Archel et al 2011 Cannizzaro amp Weiner 2015) In this

regard we heed the call by Hahn and Kuhnen (2013) for further research to be grounded

in institutional theory to uncover deeper patterns in the determination of sustainability

7

disclosure Third we bring additional insights into the debate regarding global

institutional trends in CSR disclosure Our results show that there is similarity in CSR

disclosure at the international level but that similarities are prevalent at the country level

Hence we extend and formalize earlier work on CSR disclosure at the international level

(eg Maignan amp Ralston 2002) Moreover our results shed additional light into the

relative roles of international and domestic institutions in driving CSR disclosure For

instance Fortanier Kolk and Pinkse (2011) show increasing harmonization of CSR

activities of firms from different countries thus reducing the role of domestic institutions

while Chen and Bouvain (2009) find that firms from different countries exhibit

significant differences in their CSR disclosure the main cause being differences in

national institutional arrangements Finally our paper extends and broadens the scope of

Aerts et al (2006) by adding the similarity in corporate social disclosure and controlling

for different aspects affecting the propensity to similarity ie public media exposure

corporate governance environmentalsocial performance firm size competition

profitability and environmentally-sensitive industries

The next section provides the conceptual framework and related literature The

hypotheses are followed by the method results discussion conclusions and limitations

2 Background and Conceptual Framework

21 CSR Performance and a Firmrsquos Stock Market Value

While it relies on evidence from decades of empirical research the relation

between CSR performance (often labelled as corporate sustainability performance or

CSP) and measures of corporate financial performance (CFP) remains a contentious issue

8

(Clarkson et al 2011 Lys et al 2015) For instance Margolis Elfenbein and Walsh

(2009) review 251 prior studies on the matter and note that 59 percent of studies do not

report a significant relationship 28 percent report a positive relationship and 2 percent

report a negative relationship between CSP and CFP While studies finding a positive

relation dominate those reporting a negative one the predominant finding is that the vast

majority of studies do not find evidence of any relation In a comprehensive meta-

analysis Orlitzky Schmidt and Rynes (2003) find a positive relation between CSP and

CFP and observe that some early studies reporting negative relations suffer from poor

conceptualization or inadequate methodological choices However the positive relation is

largely driven by accounting-based measures of financial performance with the relation

between CSP and market-based measures of CFP being marginally positive Some also

argue that corporate CSR activities simply add noise and volatility to capital markets

(Orlitzky 2013) Lys et al (2015) posit and find empirical support that the direction of

causality between CSP and CFP is reversed in that CSR expenditures are signals of

private information about better future performance Hence according to Joshi and Li

(2016) the literature on the nature of the relation between CSP and CFP remains largely

inconclusive

22 CSR Disclosure similarity as a Mediator between CSR Performance and Stock

Market Value

The inconclusive evidence regarding the relation between CSR performance and a

firmrsquos financial performance as proxied by its stock market value raises the question as

to the source upon which investors relate to ascertain CSR performance In this regard in

9

addition to a firmrsquos disclosure several sources are potentially available (eg KLD

Bloomberg) However a firm itself ultimately provides a major portion of the

information regarding its CSR performance with alternative platforms such as KLD

essentially relaying content disclosed by the firm For instance in discussing its CSR

disclosure rankings of large firms listed on the worldrsquos stock markets Corporate Knights

mentions that ldquoThe overwhelming majority of sustainability data in the market today has

been reported voluntarilyrdquo (2014 p 14)

The saliency of CSR disclosure in assessing CSR performance thus puts the focus

on the ongoing debate regarding managementrsquos ultimate aims when providing CSR

disclosure (andor its components ie environmental and social disclosures) On the one

hand several studies argue and find evidence that is consistent with CSR disclosure being

strategically opportunistic either by trying to manage impressions (Neu Warsame amp

Pedwell 1998 Cho Roberts amp Patten 2010) enhance legitimacy among stakeholders

(Deegan 2002 Patten 1992 Chauvey Cho Giordano-Spring amp Patten 2015 Cormier

amp Magnan 2015 OrsquoDonovan 2002) or more extremely deceive public opinion by

putting up disclosure facades that distort and even misrepresent reality (Cho Laine

Roberts amp Rodrigue 2015)

On the other hand CSR disclosure (mostly in terms of environmental matters)

reflects information economics considerations the ultimate intent being to provide

investors and other stakeholders with a signal or information that is credible and useful

for decision-making (Aerts Cormier amp Magnan 2008 Cormier amp Magnan 2003

Clarkson Li Richardson amp Vasvari 2008 Dhaliwal Radhakrishnan Tsang ampYang

2012 Li Richardson ampThornton 1997) Thus both perspectives offer contrasting

10

findings further confounding our understanding of the nature of the mediating effect that

CSR disclosure plays in the relation between CSR performance and stock market value

In this regard OrsquoDwyer and Unerman (2016) reiterate the pleas by both

Hopwoods (2009) and Gray (2002) for further theorization of research into CSR or

sustainability issues especially its disclosure While they highlight the progress realized

over the years they note that environmental issues have received much more attention

than social ones such as human rights supply chain abuses and fair trade Moreover

they recognize that less focus should be devoted to the actual act of disclosing and that

more attention toward the processes via which disclosure evolves

However Campbell (2007) does offer a path forward in the investigation of CSR

disclosure While his work is more about CSR performance per se than about its

disclosure he argues that institutional conditions underlie the mapping between a firmrsquos

surrounding economic context and its actual CSR actions and ultimately drive its

disclosure Such conditions encompass regulations monitoring organizations

institutionalized norms with respect to corporate actions and imitation among

corporations themselves We now elaborate further as how CSR disclosure similarity can

be viewed as an institutionalized process and what it implies

23 CSR Disclosure as an Institutionalized Process

Institutional theory especially its neo-institutional version (Scott 1995) does

provide a comprehensive yet conceptually grounded approach to revisit the determination

of CSR disclosure and possibly a way to reconcile these disparate findings Chen and

Roberts (2010 p 652-653) state that ldquoWhile legitimacy theory itself does not specifically

express how to meet social expectation and gain social support institutional theory

11

strongly emphasizes that organizations can incorporate institutionalized norms and rules

to gain stability and enhance survival prospectsrdquo Therefore rather than assessing CSR

disclosure as either deceptive or informative and relying on legitimacy stakeholder or

signalling theories we consider that it has become institutionalized over time and is thus

driven by considerations beyond managerial incentives (to deceive or to convey useful

information) An advantage of using such an approach is that the institutionalization of

corporate disclosure has been the object of several theoretical developments over the

years highlighting how disclosure institutionalization arises and what are the

consequences for organizations (see DiMaggio amp Powell 1983 North 1990 Powell amp

DiMaggio 1991 Scott 1995)

However despite their appeal and applicability to disclosure decisions there is

little formal empirical evidence of these theoretical propositions with respect to CSR

disclosure in both its environmental and social dimensions For instance focusing on 36

mining firms from two countries De Villiers and Alexander (2014) argue and illustrate

that the dissemination of CSR disclosure around the world is consistent with its

institutionalization Comparing the corporate social responsibility reporting of Australia

and South Africa mining firms de Villiers and Alexander (2014) find similar overall

patterns of corporate social and environmental reporting in diverse settings while

differences at a more detailed level remain In another international comparison Chen

and Bouvain (2009) find that membership in the United Nationsrsquo Global Compact by

leading firms from the US UK Australia and Germany affect only certain aspects of

their CSR reporting relating to the environment and workers Firms differ extensively

across countries in their promotion of CSR and in the CSR issues that they choose to

12

emphasize in their reports Chen and Bouvain (2009) attribute these country differences

to different country-specific institutional arrangements In contrast Fortanier et al (2011)

find that firms comprising the Fortune Global list show upward harmonization in their

CSR reporting if they adhere to global CSR standards such as GRI However it appears

that stricter enforcement mechanisms do not increase harmonization Fortanier et al

(2011) conclude that such global harmonization in CSR disclosure reduces the influence

of domestic institutions (eg legislation societal concerns) In another context

Contrafatto (2014) examines how the social and environmental reporting of an Italian

corporation becomes increasingly institutionalized over time

Hence while it appears that an institutional perspective provides useful lens for

the analysis of CSR disclosure whether domestic or global institutions drive CSR

disclosure is still an unsettled issue Moreover at the country level the role played by

firm- and industry-specific factors in CSR disclosure is still undefined We now elaborate

further on the new institutional theory and on its isomorphism dimensions as the

foundation of our investigation

24 Isomorphism

Within an institutional perspective institutions constrain or exert pressures on

organizational agencies thus producing organizational structures and strategies that are

both stable and recognizable (Jepperson 1991 Zucker 1977) Such institutional

constraints or pressures and their interaction shape ldquothe potential wealth-maximizing

opportunities of entrepreneursrdquo (North 1990 p 73) Moreover by pursuing their wealth-

maximizing objectives organizations incrementally alter the current institutional context

(North 1990) Therefore the interaction between these firm objectives (like

13

environmental social and financial performance legitimacy and good governance) and

established institutions ultimately determines a firm`s value creation In this regard

North (1990) highlights how rules both formal and informal are important for the

efficiency of an institution and will ultimately define behavioural constraints Institutions

and the pressures they bring onto organizations also play a major role that underlies

corporate practice More specifically institutional rules or pressures facilitate economic

exchanges in situations of uncertainty as they minimize transaction costs for

organizations

Prior research identifies three core types of institutional pressures by which

convergence occurs (Heugens amp Lander 2009 Scott 2001) mimetic coercive and

normative (Martinez-Ferrero amp Garcia-Sanchez 2017) Each is expected to mediate the

relation between CSR performance and stock market value and is now discussed in turn

in the next section

3 Hypotheses - Mediating effect of disclosure similarity on stock market

valuation

Mimetic pressures exert a stabilizing influence on organizational behaviour and

outcomes as they stimulate the adoption of practices that are already widespread among

other organizations Therefore mimetic isomorphism is a process by which under

conditions of ambiguity or uncertainty organizational changes are imitated to gain

legitimacy (DiMaggio amp Powell 1983) thus allowing firms to solve complex problems

at low cost (Cyert amp March 1963) It also enhances their chances for survival when

14

maintaining legitimacy is critical (eg Meyer amp Rowan 1997 Westphal Gulati amp

Shortell 1997) In general firms will model their practice by identifying similar

organizations in their field perceived as the most legitimate or the best performing

(Barreto amp Baden‐Fuller 2006) Ultimately then as firms engage in mimetic

isomorphism their practices will tend toward uniformity

A relation between imitation and firm value is consistent with Northrsquos (1990)

argument that the institutionalization of corporate practices among firms facing a similar

context reduces transaction costs in situations of informational uncertainty We assert

and test that the level of uniformity in CSR disclosure mediates the relationship between

CSR performance has with stock market value Consequently the more a firm imitates

others in its organizational field the more its market value increases North D (2010)

By adopting institutionalized behaviours individuals or organizations save efforts that

can be invested in other aspects such as innovation (Berger amp Luckmann 1966)

Under normative pressures there is harmonization in the interpretation of the

surrounding context and events Such harmonization leads to convergence in the

understanding of what is happening Hence normative isomorphism stems mainly from

the professionalization of a particular field and the emergence of professional judgment

(Greenwood Suddaby amp Hinings 2002) Professions are a source of isomorphism

because of the immutability of formal education and cognitive legitimation produced by

academic specialists and the professionalrsquos networks that connect organizations Thus

within a country managers and key personnel who graduated from the same universities

and engaged with a common set of attributes will tend to approach problems and take

15

decisions in the same way and consider the same policies procedures and structures as

standardized and legitimized

Coercive pressures imply a standardization of behaviour because of the enactment

and application of rules compliance monitoring and sanctions In practice coercive

isomorphism results from formal and informal pressures exerted by other organizations

on which they depend and by the expectations of the society in which the organization

operates (Mizruchi amp Fein 1999) Organizations ceremonially adopt institutionalized

structures or standardized operating procedures when they are convinced by force (eg

by the state) or persuasion (eg more powerful firms) that such a response could improve

their access to required resources including legitimacy However over the long term

these responses affect the power relations within organizations to reflect gradually the

institutionalized and legitimized rules (eg a parent company that standardizes the

disclosure mechanisms of its subsidiaries)

Hypothesis 1

CSR disclosure similarity mediates the relationship between CSR performance and

stock market value

With respect to CSR disclosure coercive isomorphism and normative

isomorphism are more likely to arise at the country level National laws and regulations

typically determine CSR activities and disclosure which are then implemented by

professionals and managers evolving within such a national environment (ie

professionals and managers of firms within a country are typically graduates from

universities within that country are members of national professional bodies and evolve

in various national networks) Therefore when comparing firms from different countries

16

in terms of their CSR disclosure practices there is likely to be strong overlap between the

effects of the coercive and normative isomorphism rendering difficult any particular

attribution to one or another Such country-specific coercive and normative pressures are

thus likely to induce inter-country differences in CSR disclosure

We observe more environmentalsocial disclosure regulations in France and

Germany than in Canada3 For example Canada is just beginning to enforce regulations

to specific CSR issues like the Canadian Environmental Protection Act of 1999 that

requires firms to report on specific pollutant emissions Ioannou and Serafeim (2016)

thus conclude that after the adoption of mandatory disclosure laws and regulations

perceptions regarding the social responsibility of corporate executives improve Hence

their cognitive uncertainty with respect to CSR issues and societal expectations

decreases thus reducing the need for mimetic isomorphism to develop their social and

environmental disclosures In the presence of normative or coercive isomorphism firms

are forced to comply to external pressures ie regulation concerning environmental and

social issues thus implying less imitation Hence we expect a country effect in the

isomorphism process with less similarity in Germany and France than in Canada

However there is a countervailing institutional pressure with respect to CSR

disclosure at the international level with the advent of standards such as the GRI (Global

Reporting Initiative) or ISO 14000 which adoption and implementation imply normative

isomorphism across firms from different countries In this regard Chelli Durocher and

Fortin (2018) evaluate and compare environmental reporting practices in France and

3 For further information about each countryrsquos coercive and normative forces see Thomson Reuters

(2015a 2015b 2016) Government Canada (2017) and Wolniak (2013)

17

Canada through the lens of institutional legitimacy looking at both their mandatory and

voluntary aspects They examine how French and Canadian firms changed their reporting

practices in reaction to the enactment of laws and regulations in their respective

countries ie the NRE and Grenelle II Acts in France (Loi sur les Nouvelles Reacutegulations

Eacuteconomiques) and National Instrument 51-102 and CSA Staff Notice NR 51-333 issued

by the Canadian Securities Administrators They also investigate firmsrsquo voluntary

disclosures according to GRI guidelines Their results show that the French parliamentary

regime is more successful than the Canadian stock exchange regulation in triggering

environmental reporting and that the GRI combined with local regimes prompts

environmental disclosures However there is contrasting evidence that even with

mandatory requirements there is variance in how firms interpret and apply the mandatory

requirements especially if enforcement is lagging (eg Depoers and Jerome 2017)

Hence to some extent even disclosure items that appear mandatory may actually embed

an important voluntary dimension

In light of the tension between these two sources of pressures (coercive and

normative at the country level normative at the international level) we make the

following non-directional prediction

Hypothesis 2

The mediation effect of CSR disclosure similarity in the relationship between CSR

performance and with stock market value varies across countries

18

4 Method

41 Sample

Our sample comprises 1 401 firm-year observations covering 2012-2014 with

467 unique firms There are 239 unique Canadian firms (member firms of the SampPTSX

Index of the Toronto Stock Exchange) 119 unique French firms (member firms of the

SBF120 Index of the Paris Bourse) and 109 unique German firms (member firms of the

DAX30 MDAX50 and TecDAX30 Indices of the Deutsche Bourse) There are missing

values to compute similarity scores (28 observations for environmental disclosure and 29

for social disclosure) which gives 1 373 firm-year observations for environmental

similarity imitation and 1 372 for social similarity There are many missing values in

Bloomberg database for ESG social performance (272) ESG environmental performance

(481) and ESG corporate governance (101)

This gives a final sample of 753 firm-year observations for environmental

similarity model and 932 firm-year observations for social similarity disclosure

42 Empirical Model

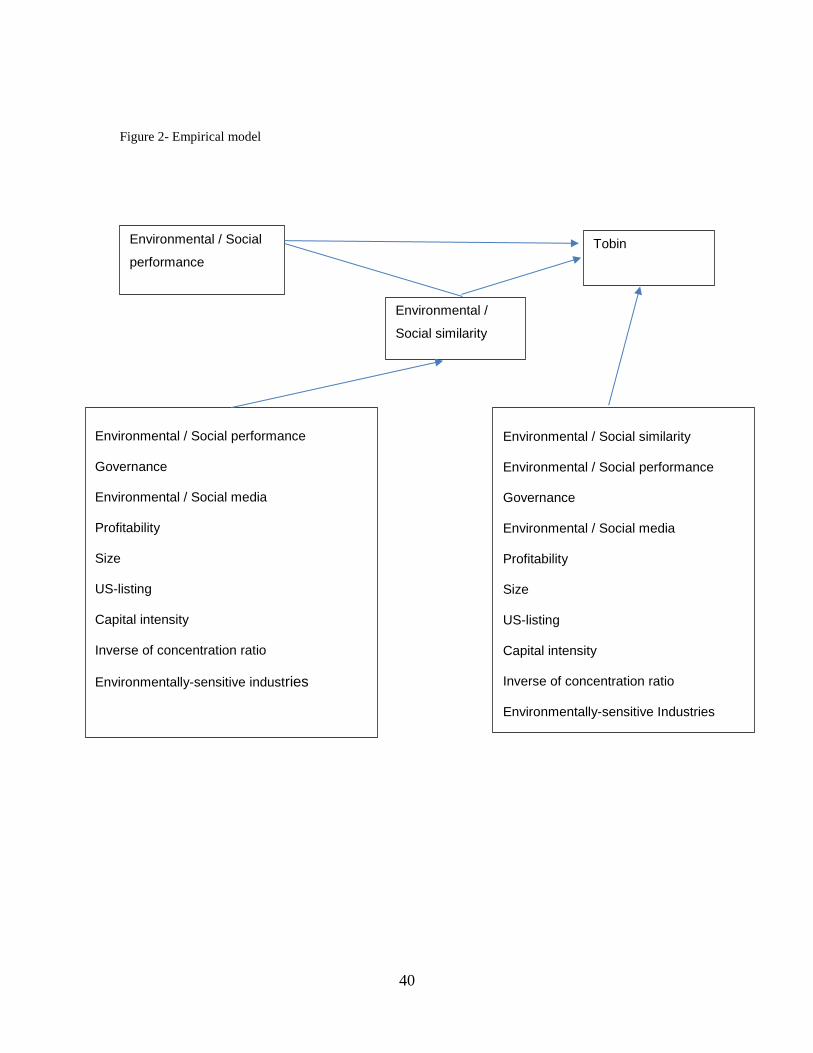

Figure 1 shows the relations being tested with our path analysis for environmental

(social) performance and disclosure

[Insert Figure 1]

Since our focus is the mediating effect of CSR disclosure similarity inducted by a

firmrsquos adoption of the institutions of its reference group on the relation between CSR

performance and stock market value we first estimate the level of uniformity within

national industries in either environmental or social disclosure Uniformity implies that

19

focal firms adopt disclosure practices that are similar to the practices of other firms

within their reference group (Deephouse 1996) For the purpose of our analyses CSR

comprises its environmental and social components for both performance and disclosure

In addition well-known determinants of corporate disclosure such as governance media

exposure firm size competition US-listing environmentally-sensitive industries and

profitability are added to the model

To test our hypotheses we use PROCESS path analysis with the objective of

enhancing the interpretation of relations Given that our variable of interest is a mediator

it is interesting to show the direct effect the indirect effect via mediation and the total

effect4 5

43 Measurement of Variables

Stock Market Value (Tobinrsquos Q)

Tobinrsquos Q is measured as the ratio of the market value of equity plus book value of debt

divided by total assets

4 In mediation and conditional process analysis under PROCESS many important statistics

useful for testing hypotheses such as conditional indirect effects and the index of moderated

mediation require the combination of parameter estimates across two or more equations in the

model Inference about these statistics is based on bootstrapping methods given that many of

these statistics have irregular sampling distributions Then making inferences using ordinary

methods problematic (Hayes 2013 Shrout and Bolger 2002)

5 According to Hayes (2013 p 80) ldquofor models that are based entirely on observed variables

investigators can rest assured that it generally makes no difference which is used [SEM or

PROCESS] as the results will be substantively identical The choice in that case is

inconsequentialrdquo

20

Environmental Disclosure and Social Disclosure Similarity Disclosure similarity is

measured within a reference group that is defined at the industry-country level as firms

within an industry are more likely to pursue strategies (Fiegenbaum amp Thomas 1995)

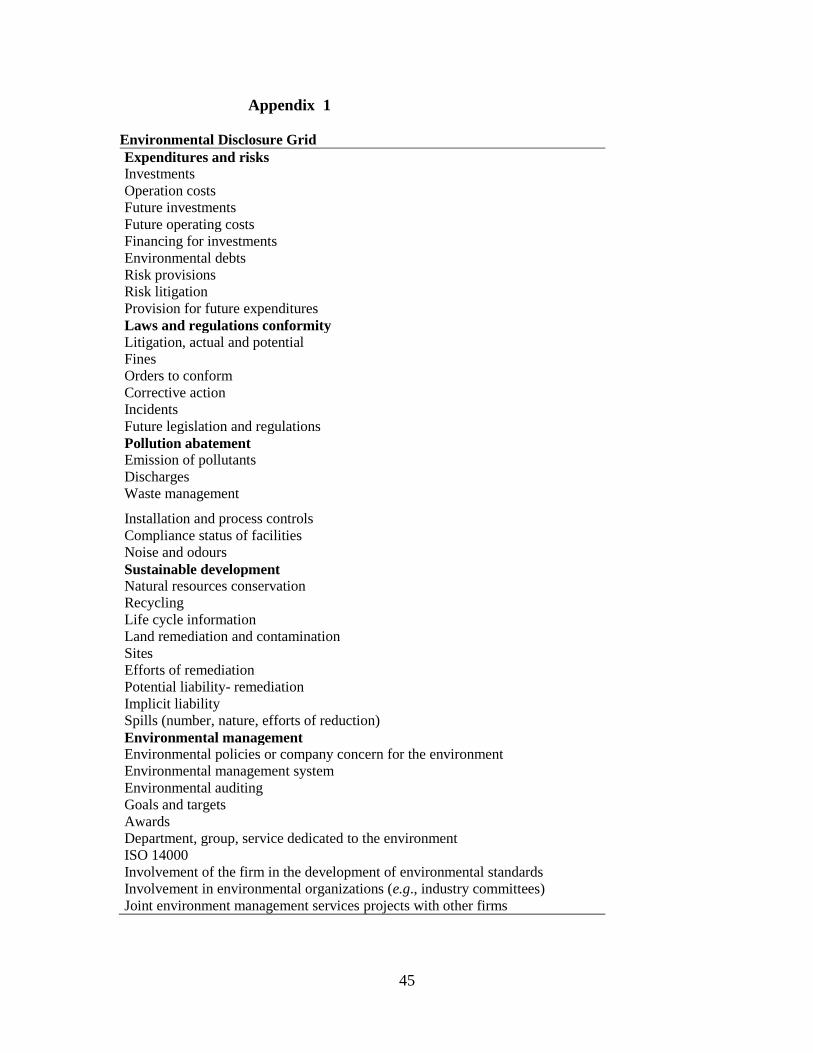

The starting point is the measurement of each firmrsquos environmental and social

disclosures which are captured through two coding grids designed by Cormier and

Magnan (2015) for environmental disclosure and Cormier Gordon and Magnan (2016)

for social disclosure The environmental disclosure coding grid comprises 40 items that

are grouped into six categories economic factors laws and regulations pollution

abatement sustainable development land remediation and contamination (including

spills) and environmental management The social disclosure coding grid comprises 35

items grouped into four categories Labour practices and decent work Human rights

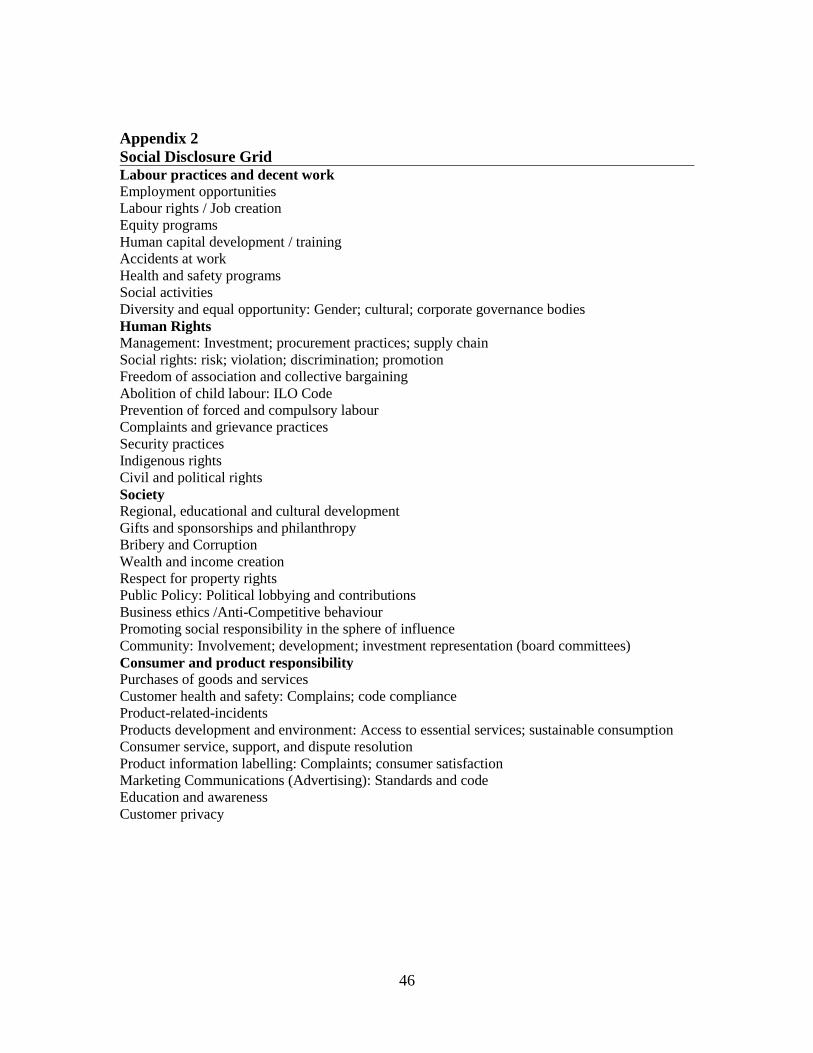

Society and Consumer and product responsibility (see Appendix 2)6 Disclosure content

is rated in terms of the presence (1) or absence (0) of the information

Once each firmrsquos disclosure is coded a dissimilarity score is then computed for

each firm

Environmental disclosure dissimilarity score =

ABS [environmental disclosureit ndash M (environmental disclosurejt)]

SD (environmental disclosurejt)

Social disclosure dissimilarity score =

ABS [(social disclosureit ndash M (social disclosurejt)] SD (social disclosurejt)

6 Two frameworks serve as examples for our disclosure grids The GRI framework (2014)

suggests sustainability reporting by all organizations The International Standards Organization

(ISO) offers voluntary standards that products are ldquosafe efficient and good for the environmentrdquo

(ISO 2014) Specific CSR standards include ISO 14000 (environment) ISO 26000 (social

responsibility) and ISO 20121(sustainable events)

21

Where i indicates a focal firm t a given year and j other firms besides the focal firm

within its reference group

ABS indicates an absolute value M and SD represent the mean and the standard

deviation for environmental and social disclosures in the firmrsquos reference group

(excluding the focal firm) Essentially the higher the dissimilarity score the more distant

a firmrsquos environmental disclosure or social disclosure is from the reference group The

reference group or organizational field comprises other firms within the same industry

for a given country To convert the disclosure dissimilarity score into a disclosure

similarity score we subtract each firmrsquos dissimilarity score from the highest dissimilarity

score in the industry

Environmentalsocial disclosure similarity scoreit =

Highest industry environmentalsocial dissimilarity scoret ndash environmentalsocial

dissimilarity scoreit

This approach provides a relative ranking of firms within a reference group while

retaining differences in similarity profiles between reference groups This approach is

consistent with earlier work by DiMaggio and Powell (1983 p 156) Scott (1995 p 76)

North (2010) and is used to indicate conformity to institutional norms

Environmentalsocial performance and governance For each firm three individual

scores for Environmental Performance Social Performance and Corporate Governance

are collected from the Bloomberg database Bloomberg rates firms based on their

22

disclosure of quantitative and policy-related ESG data relying on different sources

Annual reports sustainability reports press releases direct communication with

companies including meetings phone interviews email exchanges and survey responses

Bloomberg is on track to cover more than 13 000 firms with Environmental Social and

Governance data in 83 countries by the end of 2018 The aim is to assess a firms

management and performance in terms of CSR and governance Examples of issues

treated are

Environmental (environmental Policy environmental management systems

voluntary codes product stewardship and life cycle assessment sustainability

investing ndash commitment to ecologically sustainable development climate change

risk carbon emissions toxic waste treatment raw materials scarcity water

scarcity air pollution natural resources used environmental opportunities

Social (community investment human rights amp supply chain consumer rights and

empowerment stakeholder engagement and reporting workplace safety

employee development amp training child labour human capital product safety

social opportunities)

Governance (ethical business conduct ownership of organization organizational

structure and management risk management audit and compliance executive

compensation shareholder rights and reporting)

Environmentalsocial media exposure Media exposure is the number of news stories that

refer to a focal firmrsquos CSR activities in a given year Based on elements included in our

environmentalsocial disclosure grids we collect data (number of articles) related to

23

environmental and social issues from ABI Inform which provides access to corporate

information

Economic Variable We also introduce an economic variable as a proxy for coercive

pressures to reflect the interests of financial resources providers upon which a firm may

be dependent We expect that the more a firm is dependent upon financial resources

providers the less it will engage in disclosure similarity behaviour More specifically we

posit profitability (eg financial strength) as proxied by cash flow from operations on

assets reduces the need to imitate other firms in a given industry Coercive consequences

of similarity are lower for firms in financial health We expect a negative association

between profitability and similarity Large firms (LnAssets) are more likely to face

pressures from environmental groups than small firms thus inducing to isomorphism We

can also argue that US-listings may affect industry level isomorphism For instance a

Canadian firm cross-listed in the US may face increased pressures from the SEC (due to

higher disclosure requirements) to provide additional disclosures about its environmental

impact In a similar fashion competition as proxied by the inverse of concentration ratio

and Capital intensity (Fixed assetsTotal assets) may affect the isomorphism of CSR

disclosure Finally a firm operating in an Environmental-sensitive industry may see an

advantage to adopt the institutionalized disclosure patterns of its industry We consider

four sectors being members of environmentally-sensitive industries Construction

Manufacturing Mining and Transportation amp Public Utilities

5 Results

51 Descriptive Statistics

24

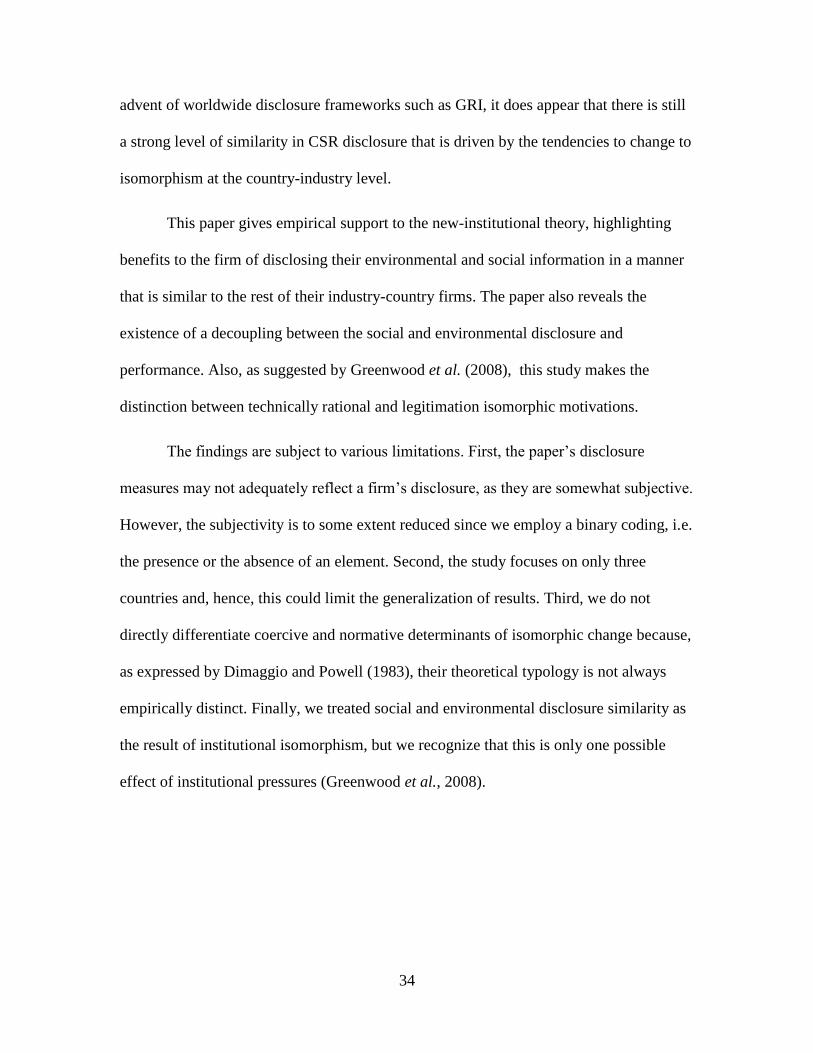

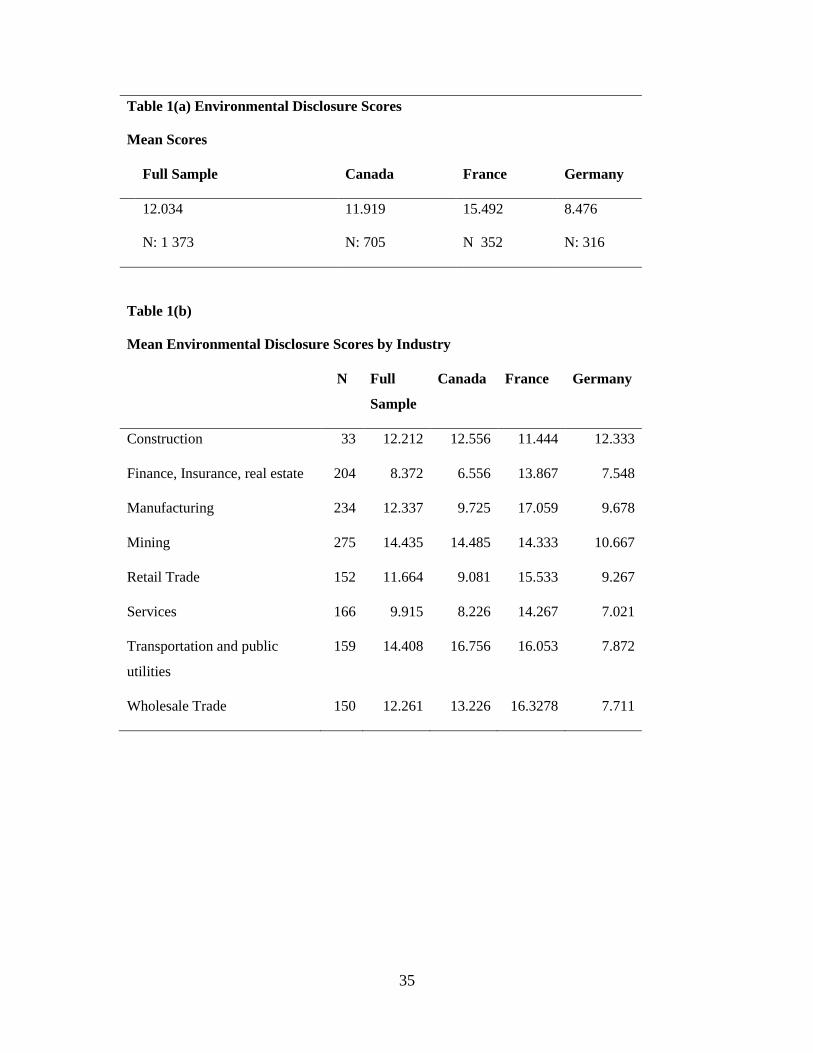

Tables 1 and 2 present Environmental disclosure scores and Social disclosure

scores France exhibits the highest mean score with 15492 followed Canada (11919)

and Germany (8476) For Social disclosure Germany exhibits the highest mean score

(17025) followed by France (15643) and Canada (11222)

[Insert Tables 1 and 2]

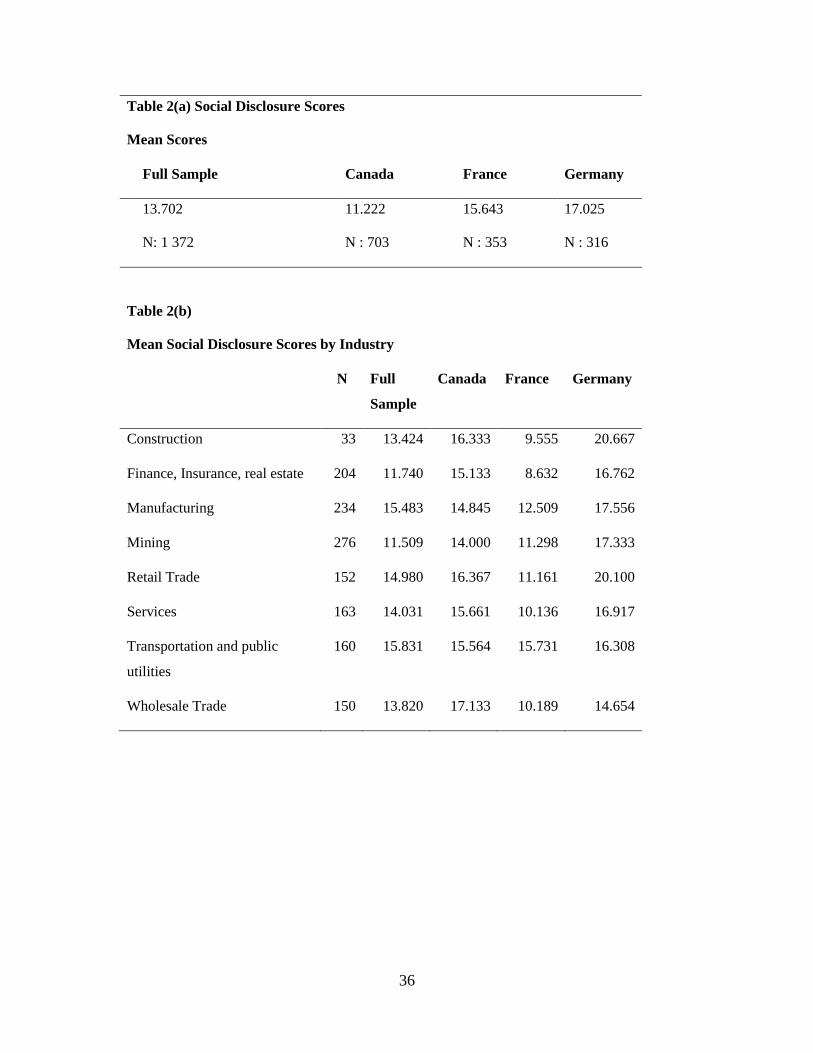

Table 3a presents descriptive statistics about environmental similarity scores for

the sample and by country As expected similarity scores are on average higher in

Canada (25873) than in France (22044) and Germany (18677) Table 3b shows that

similarity scores are on average lowest for the Finance Insurance and real estate

industry (17734)

[Insert Table 3]

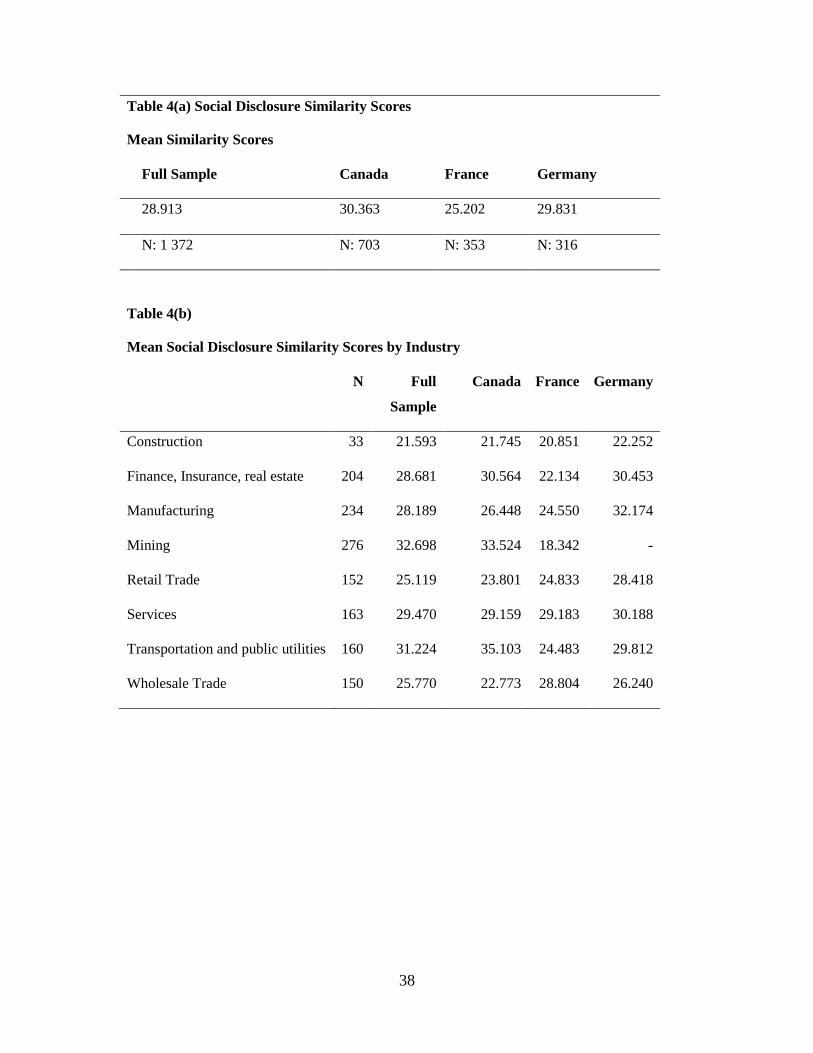

Table 4a provides mean social similarity scores Again similarity scores are on

average higher in Canada (30363) than in France (25202) and Germany (29831) The

construction industry exhibits the lowest average social similarity score (21593)

These country-level differences in both environmental and social similarity scores

are consistent with the view that organizations become aligned with their institutional

contexts in different ways Institutional contexts diverge in their completeness providing

scope for strategic choice Therefore isomorphism can be an institutional effect

motivated by the goal of legitimacy (ie institutional isomorphism) or it can be a strategic

choice of learning (competitive isomorphism) (Greenwood et al 2008) Results show

that in the presence of more normative or coercive forces as is the case in France and

Germany compared with Canada there is likely less similarity which leads to less

isomorphism among firms

25

[Insert Table 4]

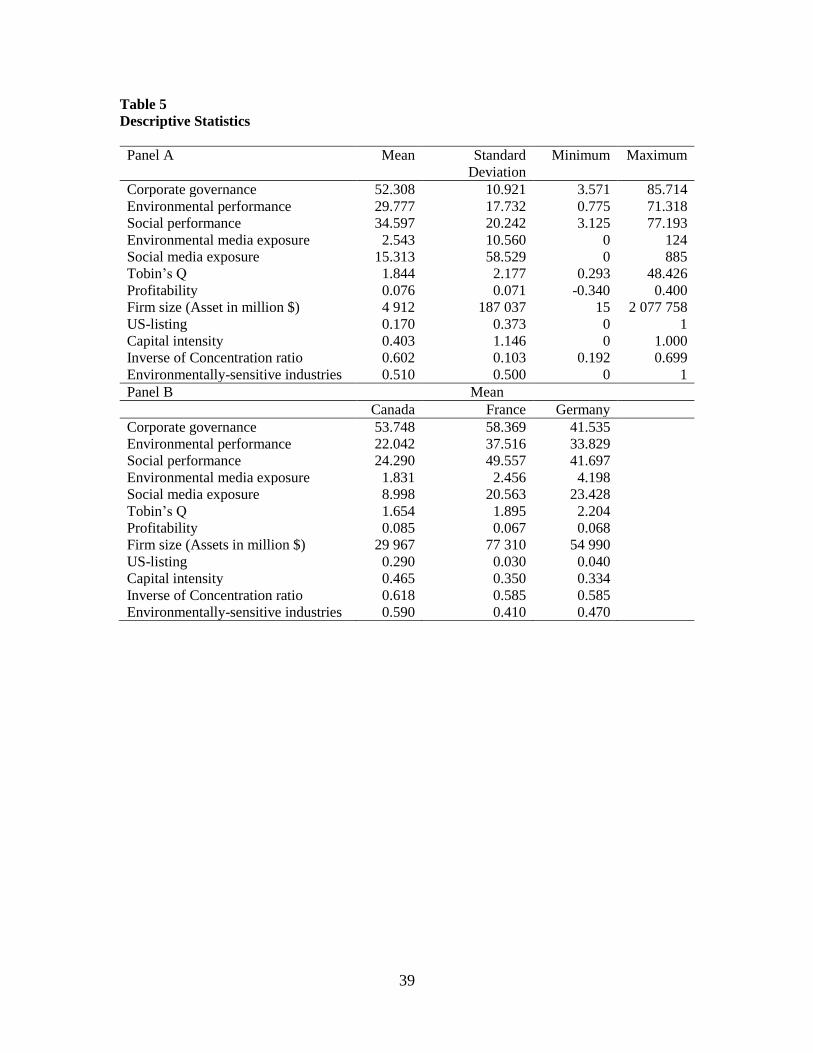

Table 5 provides some descriptive statistics about explanatory variables

Corporate governance seems weaker in Germany (mean score of 41534 versus 53748 in

Canada and 58369 in France) Environmental performance appears to be lower in

Canada (22042 versus 37516 for France and 33829 for Germany) We observe the same

pattern for social performance As discussed earlier environmentalsocial regulations are

more severe in France and Germany than in Canada Moreover environmental and social

media exposure is much higher in France and Germany compared with Canada We

observe that firm size is bigger in France Finally as expected more firms belong to

environmentally-sensitive industries in Canada compared with France and Germany

[Insert Table 5]

52 Multivariate Analyses ndash Environmental Disclosure Similarity and Firm Valuation

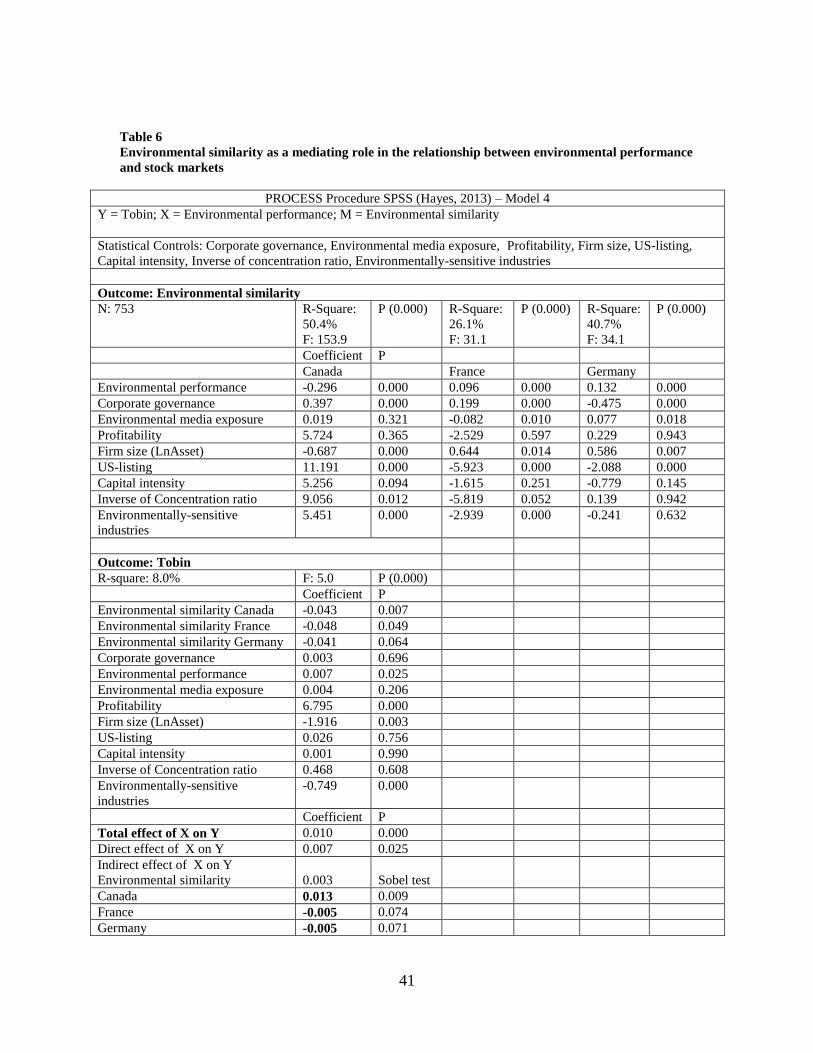

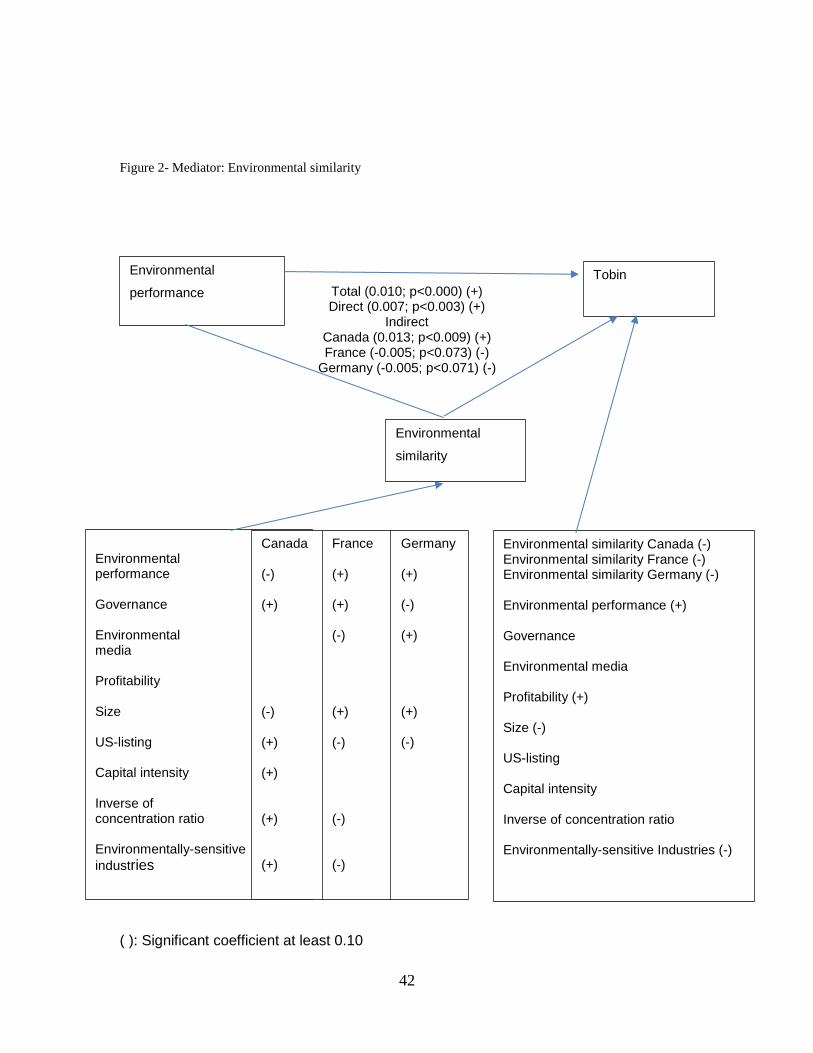

Table 6 provides results for Environmental similarity as a mediator that rely on

the PROCESS procedure from SPSS on mediation analysis (Hayes 2013) This path

procedure allows for testing our hypotheses Instead of X causing Y directly X is causing

the mediator M and M is in turn causing Y The causal relationship between X

(Environmental performance) and Y (Tobin) is said to be indirect The relationships

between the independent mediator (Environmental similarity) and the dependent

variables can be depicted in the form of a path model Bootstrapping is used to calculate

standard errors and confidence intervals

First Environmental performance (independent variable) is a significant predictor

of mediator (M) ie Environmental similarity The relation between the independent

variable and the dependent variable is hypothesized to include an indirect effect due to

26

the influence of a third variable (the mediator) Concerning the indirect effect on Tobin

(Y) the mediator Environmental similarity is significant and positive for Canada (0013

p lt 0009) and negative and significant for France (-0005 p lt 0074) and Germany (-

0005 p lt 0071) according to a Sobel test (Sobel 1982) Results suggest that

Environmental similarity enhances the relation between Environmental performance and

stock market value in Canada while we observe the opposite in France and Germany

This supports hypothesis 1 that environmental disclosure similarity mediates the

relationship between environmental performance and stock market value Coercive forces

in France and Germany concerning environmental issues lead firms to exhibit less

decoupling between performance and disclosure

Our results show that the worse environmental performance in Canada the more

environmental disclosure follows the institutionalized patterns of environmental

disclosure and the less this information is valued by the market This means that the

market views the institutionalized patterns of environmental disclosure in Canada as

uninformative about the environmental performance of firms Unlike Canada in both

France and Germany the better the environmental performance the more it follows the

institutionalized patterns of disclosure but the less the information is valued by the

market

Among determinants of Environmental similarity Environmental performance

has a negative direct effect on environmental disclosure similarity in Canada (-0296 p lt

0000) but a positive effect in France (0096 p lt 0000) and Germany (0132 p lt 0000)

It means that in Canada when firms exhibit a poor environmental performance they tend

to disclose environmental information consistent with their industry-country patterns

27

Coercive forces in France and Germany concerning environmental issues lead firms to

exhibit less decoupling between performance and disclosure It is also the case for firm

size Moreover we observe that a US-listing (11191 p lt 0000) and competition

(Inverse of Concentration ratio 9056 p lt 0012) and Environmentally-sensitive

industries (5451 p lt 0000) are factors leading to more isomorphism in Canada a

country with less coercive forces than France and Germany Firm size gives opposite

results It seems that CSR disclosure of large firms are induced to become more similar in

France and Germany but not in Canada Overall there is less decoupling in France and

Germany than in Canada

Concerning the determinants of stock market value (Tobin) Environmental

similarity (mediator) has a direct negative impact on Tobin (Canada -0043 p lt 0007

France -0048 0049 Germany -0041 p lt 0062) Furthermore in addition to

Environmental performance (0007 p lt 0025) profitability (6795 p lt 0000) Firm size

(-0198 p lt 0003) and Environmentally-sensitive industries (-0749 0000) have a

direct effect on Tobin

In Canada coercive and normative actors mostly the state and the professions

play a less important role than in France and Germany in enforcing cognitive

environmental and social issues Moreover constraints at the firm level such as

environmental performance and media pressures play a smaller role in Canada to

influence CSR disclosure isomorphism and its impact on stock markets This can be

observed in Canada by the direct effects of environmental performance on environmental

similarity Our results support hypothesis 2 arguing that the mediation effect of CSR

28

disclosure similarity in the relationship between CSR performance and stock market

value varies between countries

These results give empirical support to two important new-institutional

propositions 1) becoming isomorphic with their institutional context provides survival

benefits and 2) conformity is mostly ceremonial based on symbolic structures decoupled

from organizational performance (Greenwood et al 2008) The effect of environmental

similarity on the relation between firm-level constraints and stock market value is higher

in Canada than in either France or Germany may be because of decoupling between real

performance and environmental disclosure

The positive relation between the mediating effect of Environmental disclosure

similarity (in Canada) on the relation between Environmental performance and firm

valuation is consistent with Northrsquos view (1990) that the institutionalization of practices

within an organizational field which similarity represents is a transaction costs-reducing

choice by management In other words in a context of uncertainty to imitate other firmsrsquo

practices could be value enhancing

[Insert Tables 6 and Figure 2]

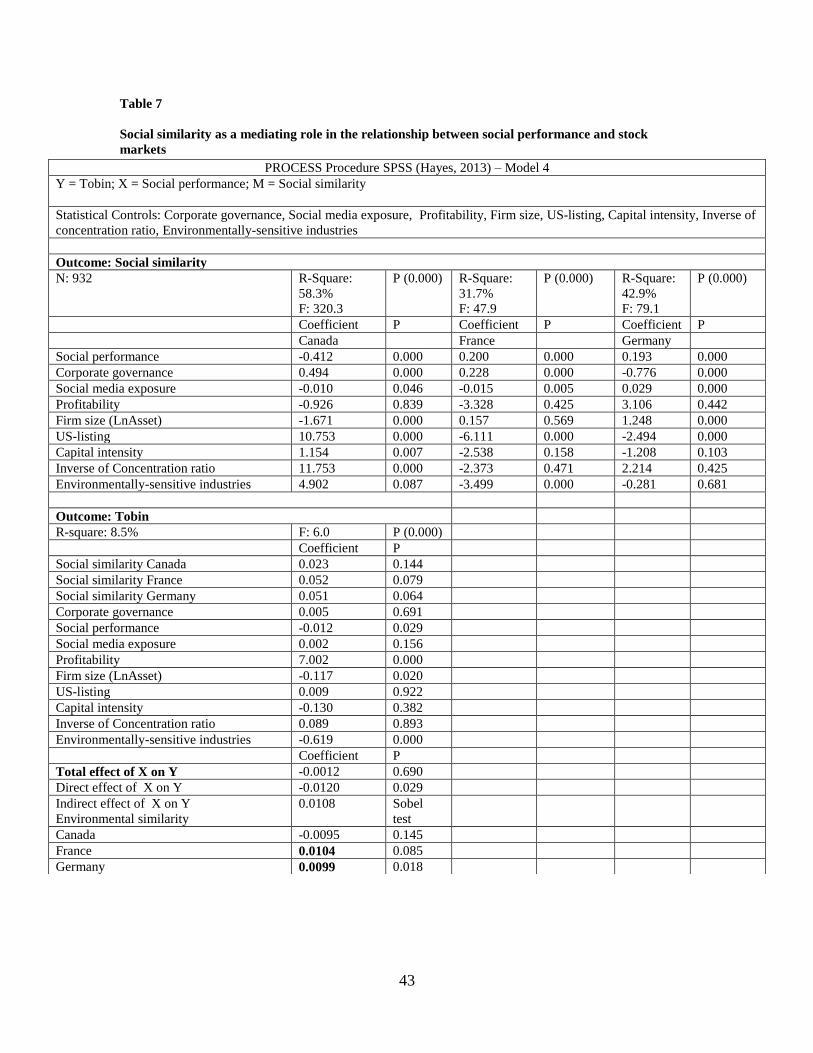

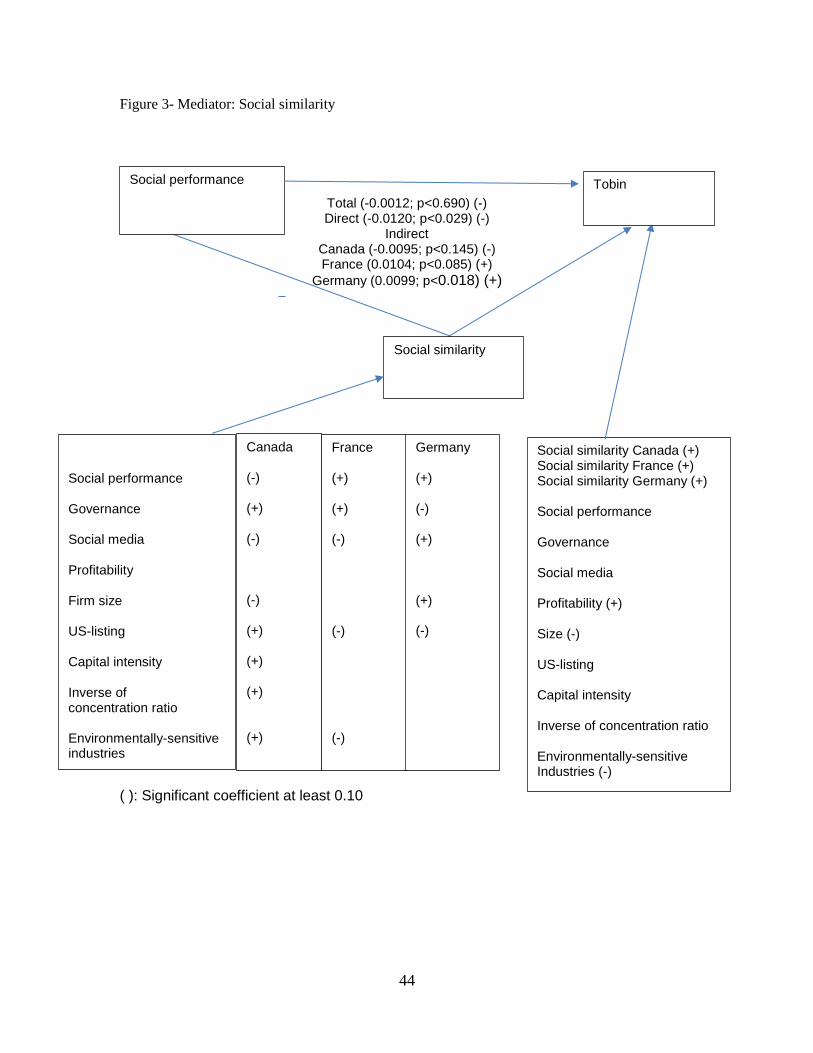

53 Multivariate Analyses ndash Social Disclosure Similarity and Stock Market Value

Results are qualitatively similar to environmental disclosure similarity for the

direct relation factors between social disclosure similarity and firm value However

contrary to environmental disclosure similarity social disclosure similarity has a negative

direct mediating effect on the relation between social performance and stock market

value The indirect effect is positive for France (00104 p lt 0085) and German (00099

29

p lt 0018) while not significant for Canada (0-00095 p lt 0145) Also contrary to

environmental disclosure similarity that exhibits a negative relation with Tobin for the

three countries social disclosure similarity is positively related to Tobin for the three

countries

Our results show that the worse a firmrsquos social performance in Canada the more

social disclosure follows institutionalized patterns of social disclosure and the more the

market values this information This means that unlike environmental disclosure the

market considers the institutionalized patterns of social disclosure in Canada as being

useful for informing about the social performance of firms In the same way as for

environmental disclosure in France and Germany the better the social performance the

more it follows the institutionalized patterns of disclosure However unlike

environmental disclosure the more social disclosure follows institutionalized patterns the

more this information is valued by the market This means that the market considers that

institutionalized social disclosure patterns in France and Germany are a good way to

communicate the social performance of firms

In general contrary to environmental similarity firm-level constraints on social

disclosure similarity are much higher in Canada than in France and Germany The only

exceptions are social media exposure that exhibits a positive association in Germany and

firm size in France and Germany It means that in Germany it is important to the public

opinion that firmsrsquo social disclosure respects their industry-country patterns

Our results are in line with hypothesis 2 arguing that the mediation effect of CSR

disclosure similarity on the relationship between CSR performance and stock market value

varies among countries

30

[Insert Table 7 and Figure 3]

54 Additional analyses

The organizational field level of analysis is sometimes considered to be too

narrow (Greenwood et al 2008) Results presented so far rely on a focal firmrsquos reference

group that is defined as the other firms in the same industry in the same country

However since our sample firms are large and often have international operations the

reference group could be defined at a global industry level Hence in an additional

analysis we compare differences in disclosure similarity at country-industry level versus

combined country and industry

The mediating effect (indirect) of environmental similarity on the relation

between environmental performance and Tobin (00107 p lt 0008) remains almost

equivalent to results presented in Table 6 for Canada while in for France (-00030 p lt

01183) and Germany (-00035 p lt 01938) the indirect effect is not statistically

significant anymore Concerning the indirect effect of Social similarity as a mediating

effect on the relation between Social performance and Tobin results are almost

equivalent to those presented in Table 7

Previous literature gives three explanations for the heterogeneity that drives

institutional changes imperfect copying regulatory pressures and field level competition

(Haunschild amp Chandler 2008) Imperfect copying is a process by which field-level

institutional change can occur the regulatory pressures of an organizational field can give

cognitive orientations to other fields and also lead to an institutional change and in

highly competitive industries firms are encouraged to innovate thus generating

institutional changes (Haunschild amp Chandler 2008) The most probable explanation to

31

less mediating effect of environmental disclosure similarities at the global industry level

is the commonality of coercive and normative forces at the country level thus leaving

only cognitive uncertainty about the same environmental aspects

With respect to social disclosure similarity our results suggest that social issues

operate in quite a similar manner at country level and international level Thus social

disclosure institutions are more globally diffused than environmental ones Overall this

result comforts our approach to address the industry similarity phenomenon

Results are consistent with Scotts (1995) view who argues that organizations

attempt to imitate structures and activity patterns of others having the same cultural

patterns However the possibility of doing so may vary According to Brammer et al

(2012) different institutional sets have different dominant institutions In the Anglo-

Saxon context CSR dominant institutions correspond to global policies and programs

most of which are essentially voluntary while in other contexts they correspond to legal

customary or religious institutions (Brammer et al 2012) Our results confirm this view

by showing more imitation in an Anglo-Saxon countryrsquos (Canada) industries

6 Conclusion

Overall our results indicate that environmentalsocial disclosure similarity is

higher in Canada than in France and Germany In Canada the lower the CSR

performance the more firms adopt institutionalized patterns of disclosure in search of

legitimacy This effort is valued by the market regarding social performance but not

environmental performance The adoption of patterns of social disclosure similar to those

of other firms does not necessarily mean that their performance is better but it shows that

32

the firm follows the rules of the game This increases its legitimacy Therefore investors

can expect the firm to survive long enough to secure their future gains

In Canada coercive and normative actors mostly the state and the professions

play a less important role than in France and Germany in enforcing cognitive

environmental and social issues Consequently the level of isomorphism among

Canadian firms appears higher than among French and German firms These results

confirm the institutional proposition that regulatory pressures can result in greater field-

level heterogeneity than similarities (Haunschild amp Chandler 2008) However the

resulting structural similarities are often evidence of an absence of substance (Shabana et

al 2016)

Unlike Canada in France and Germany when CSR performance is better firms

use more institutional CSR disclosure patterns These patterns seem to be sufficient to

inform the market of the social performance of firms but they prevent firms with better

environmental performance from communicating it to the market The mediating role of

CSR disclosure is more evident for France and Germany than for Canada This means

that the market considers that the CSR disclosure of Canadian firms does not reflect their

social and environmental performance in a reliable manner while in France and Germany

it is more credible

We also provide evidence that is consistent with a mediating effect of the CSR

disclosure similarity behaviour on the relation between CSR (environmental and social)

performance and stock market valuation The results show that the market values social

and environmental performance through social and environmental disclosure This means

that CSR disclosure is a useful source of information in the evaluation of firms by the

33

market However environmental disclosure is more relevant to the market than social

disclosure This may be due to the existence of more sources of information regarding the

social performance of firms (other than CSR disclosure)

CSR disclosure similarity also plays a mediating role on the relation between

other firm attributes (governance media exposure financial return firm size

environmentally-sensitive industries) and stock market value Thus CSR disclosure

similarity behaviour helps the market to evaluate the firm response their institutional

(governance and public media pressures) and technical pressures (environmental and

social performance) and hence their survival probabilities

We find that the convergence is stronger at the industry-country-level

Institutional mechanisms of change to isomorphism can result in heterogeneity

(Haunschild amp Chandler 2008) or similarities depending upon stakeholdersrsquo demands

The choice to satisfy or not these demands affects market compensation or punishments

Our results show that in different institutional contexts CSR disclosure similarity

can play different roles While institutionalized patterns in Canada help weak performers

to become legitimate in France and Germany they provide a good guide for social

disclosure and a barrier to the disclosure of good environmental performance Our

findings may be of interest to Canadian regulators if they aim to increase environmental

and social disclosure regulations since European evidence suggests that mandatory

corporate responsibility disclosure diminishes cognitive uncertainty and thus reduces

mimetic isomorphism tendencies

Results show the importance to disentangle between environmental and social

disclosure when assessing CSR disclosure similarity behaviour Finally despite the

34

advent of worldwide disclosure frameworks such as GRI it does appear that there is still

a strong level of similarity in CSR disclosure that is driven by the tendencies to change to

isomorphism at the country-industry level

This paper gives empirical support to the new-institutional theory highlighting

benefits to the firm of disclosing their environmental and social information in a manner

that is similar to the rest of their industry-country firms The paper also reveals the

existence of a decoupling between the social and environmental disclosure and

performance Also as suggested by Greenwood et al (2008) this study makes the

distinction between technically rational and legitimation isomorphic motivations

The findings are subject to various limitations First the paperrsquos disclosure

measures may not adequately reflect a firmrsquos disclosure as they are somewhat subjective

However the subjectivity is to some extent reduced since we employ a binary coding ie

the presence or the absence of an element Second the study focuses on only three

countries and hence this could limit the generalization of results Third we do not

directly differentiate coercive and normative determinants of isomorphic change because

as expressed by Dimaggio and Powell (1983) their theoretical typology is not always

empirically distinct Finally we treated social and environmental disclosure similarity as

the result of institutional isomorphism but we recognize that this is only one possible

effect of institutional pressures (Greenwood et al 2008)

35

Table 1(a) Environmental Disclosure Scores

Mean Scores

Full Sample Canada France Germany

12034

N 1 373

11919

N 705

15492

N 352

8476

N 316

Table 1(b)

Mean Environmental Disclosure Scores by Industry

N Full

Sample

Canada France Germany

Construction 33 12212 12556 11444 12333

Finance Insurance real estate 204 8372 6556 13867 7548

Manufacturing 234 12337 9725 17059 9678

Mining 275 14435 14485 14333 10667

Retail Trade 152 11664 9081 15533 9267

Services 166 9915 8226 14267 7021

Transportation and public

utilities

159 14408 16756 16053 7872

Wholesale Trade 150 12261 13226 163278 7711

36

Table 2(a) Social Disclosure Scores

Mean Scores

Full Sample Canada France Germany

13702

N 1 372

11222

N 703

15643

N 353

17025

N 316

Table 2(b)

Mean Social Disclosure Scores by Industry

N Full

Sample

Canada France Germany

Construction 33 13424 16333 9555 20667

Finance Insurance real estate 204 11740 15133 8632 16762

Manufacturing 234 15483 14845 12509 17556

Mining 276 11509 14000 11298 17333

Retail Trade 152 14980 16367 11161 20100

Services 163 14031 15661 10136 16917

Transportation and public

utilities

160 15831 15564 15731 16308

Wholesale Trade 150 13820 17133 10189 14654

37

Table 3(a) Environmental Disclosure Similarity Scores

Mean Similarity Scores

Full Sample Canada France Germany

22235 25873 22044 18677

N 1 373 N 705 N 352 N 316

Table 3(b)

Mean Environmental Disclosure Similarity Scores by Industry

N Full

Sample

Canada France Germany

Construction 33 19436 22550 16638 14292

Finance Insurance real estate 204 17734 18192 19257 14827

Manufacturing 234 21067 18446 20961 22302

Mining 275 30692 31505 16591 -

Retail Trade 152 22737 21817 26297 17521

Services 166 19717 21461 20268 16820

Transportation and public

utilities

159 25814 30513 23255 18427

Wholesale Trade 150 22929 25815 25271 17963

38

Table 4(a) Social Disclosure Similarity Scores

Mean Similarity Scores

Full Sample Canada France Germany

28913 30363 25202 29831

N 1 372 N 703 N 353 N 316

Table 4(b)

Mean Social Disclosure Similarity Scores by Industry

N Full

Sample

Canada France Germany

Construction 33 21593 21745 20851 22252

Finance Insurance real estate 204 28681 30564 22134 30453

Manufacturing 234 28189 26448 24550 32174

Mining 276 32698 33524 18342 -

Retail Trade 152 25119 23801 24833 28418

Services 163 29470 29159 29183 30188

Transportation and public utilities 160 31224 35103 24483 29812

Wholesale Trade 150 25770 22773 28804 26240

39

Table 5

Descriptive Statistics

Panel A Mean Standard

Deviation

Minimum Maximum

Corporate governance 52308 10921 3571 85714

Environmental performance 29777 17732 0775 71318

Social performance 34597 20242 3125 77193

Environmental media exposure 2543 10560 0 124

Social media exposure 15313 58529 0 885

Tobinrsquos Q 1844 2177 0293 48426

Profitability 0076 0071 -0340 0400

Firm size (Asset in million $) 4 912 187 037 15 2 077 758

US-listing 0170 0373 0 1

Capital intensity 0403 1146 0 1000

Inverse of Concentration ratio 0602 0103 0192 0699

Environmentally-sensitive industries 0510 0500 0 1

Panel B Mean

Canada France Germany

Corporate governance 53748 58369 41535

Environmental performance 22042 37516 33829

Social performance 24290 49557 41697

Environmental media exposure 1831 2456 4198

Social media exposure 8998 20563 23428

Tobinrsquos Q 1654 1895 2204

Profitability 0085 0067 0068

Firm size (Assets in million $) 29 967 77 310 54 990

US-listing 0290 0030 0040

Capital intensity 0465 0350 0334

Inverse of Concentration ratio 0618 0585 0585

Environmentally-sensitive industries 0590 0410 0470

40

Figure 2- Empirical model

Environmental Social

performance

Environmental

Social similarity

Tobin

Environmental Social performance Governance Environmental Social media Profitability Size US-listing Capital intensity Inverse of concentration ratio

Environmentally-sensitive industries

Environmental Social similarity Environmental Social performance Governance Environmental Social media Profitability Size US-listing Capital intensity Inverse of concentration ratio Environmentally-sensitive Industries

41

Table 6

Environmental similarity as a mediating role in the relationship between environmental performance

and stock markets

PROCESS Procedure SPSS (Hayes 2013) ndash Model 4

Y = Tobin X = Environmental performance M = Environmental similarity

Statistical Controls Corporate governance Environmental media exposure Profitability Firm size US-listing

Capital intensity Inverse of concentration ratio Environmentally-sensitive industries

Outcome Environmental similarity

N 753 R-Square

504

F 1539

P (0000) R-Square

261

F 311

P (0000) R-Square

407

F 341

P (0000)

Coefficient P

Canada France Germany

Environmental performance -0296 0000 0096 0000 0132 0000

Corporate governance 0397 0000 0199 0000 -0475 0000

Environmental media exposure 0019 0321 -0082 0010 0077 0018

Profitability 5724 0365 -2529 0597 0229 0943

Firm size (LnAsset) -0687 0000 0644 0014 0586 0007

US-listing 11191 0000 -5923 0000 -2088 0000

Capital intensity 5256 0094 -1615 0251 -0779 0145

Inverse of Concentration ratio 9056 0012 -5819 0052 0139 0942

Environmentally-sensitive

industries

5451 0000 -2939 0000 -0241 0632

Outcome Tobin

R-square 80 F 50 P (0000)

Coefficient P

Environmental similarity Canada -0043 0007

Environmental similarity France -0048 0049

Environmental similarity Germany -0041 0064

Corporate governance 0003 0696

Environmental performance 0007 0025

Environmental media exposure 0004 0206

Profitability 6795 0000

Firm size (LnAsset) -1916 0003

US-listing 0026 0756

Capital intensity 0001 0990

Inverse of Concentration ratio 0468 0608

Environmentally-sensitive

industries

-0749 0000

Coefficient P

Total effect of X on Y 0010 0000

Direct effect of X on Y 0007 0025

Indirect effect of X on Y

Environmental similarity

0003

Sobel test

Canada 0013 0009

France -0005 0074

Germany -0005 0071

42

Figure 2- Mediator Environmental similarity

Total (0010 plt0000) (+) Direct (0007 plt0003) (+)

Indirect Canada (0013 plt0009) (+) France (-0005 plt0073) (-)

Germany (-0005 plt0071) (-)

( ) Significant coefficient at least 010

Environmental

performance

Environmental

similarity

Tobin

Environmental performance Governance Environmental media Profitability Size US-listing Capital intensity Inverse of concentration ratio Environmentally-sensitive

industries

Environmental similarity Canada (-) Environmental similarity France (-) Environmental similarity Germany (-) Environmental performance (+) Governance Environmental media Profitability (+) Size (-) US-listing Capital intensity Inverse of concentration ratio Environmentally-sensitive Industries (-)

Canada (-) (+) (-) (+) (+) (+) (+)

France (+) (+) (-) (+) (-) (-) (-)

Germany (+) (-) (+) (+) (-)

43

Table 7

Social similarity as a mediating role in the relationship between social performance and stock

markets

PROCESS Procedure SPSS (Hayes 2013) ndash Model 4

Y = Tobin X = Social performance M = Social similarity

Statistical Controls Corporate governance Social media exposure Profitability Firm size US-listing Capital intensity Inverse of

concentration ratio Environmentally-sensitive industries

Outcome Social similarity

N 932 R-Square

583

F 3203

P (0000) R-Square

317

F 479

P (0000) R-Square

429

F 791

P (0000)

Coefficient P Coefficient P Coefficient P

Canada France Germany

Social performance -0412 0000 0200 0000 0193 0000

Corporate governance 0494 0000 0228 0000 -0776 0000

Social media exposure -0010 0046 -0015 0005 0029 0000

Profitability -0926 0839 -3328 0425 3106 0442

Firm size (LnAsset) -1671 0000 0157 0569 1248 0000

US-listing 10753 0000 -6111 0000 -2494 0000

Capital intensity 1154 0007 -2538 0158 -1208 0103

Inverse of Concentration ratio 11753 0000 -2373 0471 2214 0425

Environmentally-sensitive industries 4902 0087 -3499 0000 -0281 0681

Outcome Tobin

R-square 85 F 60 P (0000)

Coefficient P

Social similarity Canada 0023 0144

Social similarity France 0052 0079

Social similarity Germany 0051 0064

Corporate governance 0005 0691

Social performance -0012 0029

Social media exposure 0002 0156

Profitability 7002 0000

Firm size (LnAsset) -0117 0020

US-listing 0009 0922

Capital intensity -0130 0382

Inverse of Concentration ratio 0089 0893

Environmentally-sensitive industries -0619 0000

Coefficient P

Total effect of X on Y -00012 0690

Direct effect of X on Y -00120 0029

Indirect effect of X on Y

Environmental similarity

00108 Sobel

test

Canada -00095 0145

France 00104 0085

Germany 00099 0018

44

Figure 3- Mediator Social similarity

Total (-00012 plt0690) (-) Direct (-00120 plt0029) (-)

Indirect Canada (-00095 plt0145) (-) France (00104 plt0085) (+)

Germany (00099 plt0018) (+)

( ) Significant coefficient at least 010

Social performance Governance Social media Profitability Firm size US-listing Capital intensity Inverse of concentration ratio Environmentally-sensitive industries

Social similarity Canada (+) Social similarity France (+) Social similarity Germany (+) Social performance Governance Social media Profitability (+) Size (-) US-listing Capital intensity Inverse of concentration ratio Environmentally-sensitive Industries (-)

Social performance

Social similarity

Tobin

Canada (-) (+) (-) (-) (+) (+) (+) (+)

France (+) (+) (-) (-) (-)

Germany (+) (-) (+) (+) (-)

45

Appendix 1

Environmental Disclosure Grid

Expenditures and risks

Investments

Operation costs

Future investments

Future operating costs

Financing for investments

Environmental debts

Risk provisions

Risk litigation

Provision for future expenditures

Laws and regulations conformity

Litigation actual and potential

Fines

Orders to conform

Corrective action

Incidents

Future legislation and regulations

Pollution abatement

Emission of pollutants

Discharges

Waste management

Installation and process controls

Compliance status of facilities

Noise and odours

Sustainable development

Natural resources conservation

Recycling

Life cycle information

Land remediation and contamination

Sites

Efforts of remediation

Potential liability- remediation

Implicit liability

Spills (number nature efforts of reduction)

Environmental management

Environmental policies or company concern for the environment

Environmental management system

Environmental auditing

Goals and targets

Awards

Department group service dedicated to the environment

ISO 14000

Involvement of the firm in the development of environmental standards

Involvement in environmental organizations (eg industry committees)

Joint environment management services projects with other firms

46

Appendix 2

Social Disclosure Grid Labour practices and decent work

Employment opportunities

Labour rights Job creation

Equity programs

Human capital development training

Accidents at work

Health and safety programs

Social activities

Diversity and equal opportunity Gender cultural corporate governance bodies

Human Rights

Management Investment procurement practices supply chain

Social rights risk violation discrimination promotion

Freedom of association and collective bargaining

Abolition of child labour ILO Code

Prevention of forced and compulsory labour

Complaints and grievance practices

Security practices

Indigenous rights

Civil and political rights

Society Regional educational and cultural development

Gifts and sponsorships and philanthropy

Bribery and Corruption

Wealth and income creation

Respect for property rights

Public Policy Political lobbying and contributions

Business ethics Anti-Competitive behaviour

Promoting social responsibility in the sphere of influence

Community Involvement development investment representation (board committees)

Consumer and product responsibility Purchases of goods and services

Customer health and safety Complains code compliance

Product-related-incidents

Products development and environment Access to essential services sustainable consumption

Consumer service support and dispute resolution

Product information labelling Complaints consumer satisfaction

Marketing Communications (Advertising) Standards and code

Education and awareness

Customer privacy

47

References

Aerts W 2001 Inertia in the attributional content of annual accounting narratives

European accounting review 10(1) 3-32

Aerts W Cormier D Magnan M 2006 Intra-industry imitation in corporate

environmental reporting An international perspective Journal of Accounting and

public Policy 25(3) 299-331

Archel P Husillos J Spence C 2011 The institutionalization of unaccountability

Loading the dice of Corporate Social Responsibility discourse Accounting

Organizations and Society 36(6) 327-343

Barreto I Baden‐Fuller C 2006 To conform or to perform Mimetic behaviour

legitimacy‐based groups and performance consequences Journal of Management

Studies 43(7) 1559-1581

Berger PL Luckmann T 1966 The Social Construction of Reality A Treatise in the

Sociology of Knowledge New York Anchor Books Doubleday

Berthelot S Cormier D Magnan M 2003 Environmental disclosure research review

and synthesis Journal of Accounting Literature 22 1-44