Embed Size (px)

Citation preview

8/3/2019 Raymond Cp 11

http://slidepdf.com/reader/full/raymond-cp-11 1/25

Corporate Presentation

July 2011

8/3/2019 Raymond Cp 11

http://slidepdf.com/reader/full/raymond-cp-11 2/25

DISCLAIMER

1. Numbers mentioned in this note in respect of consolidated revenues and results and additional

information including but not limited to retail sales, branded sales etc. but other than Raymond Ltd.

Standalone financial results have been compiled by the management and are being provided only by

way of additional information. These are not to be construed as being provided under any legal or

regulatory requirements. The accuracy of this information and provisional quarterly consolidated

numbers have neither been vetted nor approved by the Audit Committee and the Board of Directors

of Raymond Ltd., nor have they been vetted or reviewed by the Auditors, and therefore may differ

significantly from the actual. The Company assumes no responsibility for the use of informationmentioned herein.

2. Statements in this “Presentation” describing the Company’s objectives, projections, estimates,

expectations or predictions may be “forward looking statements” within the meaning of applicable

securities laws and regulations. Actual results could differ materially from those expressed or implied.

Important factors that could make a difference to the Company’s operations include global and Indian

demand supply conditions, finished goods prices, input material availability and prices, cyclical

demand and pricing in the Company’s principal markets, changes in Government regulations, taxregimes, economic developments within India and the countries within which the company conducts

business and other factors such as litigation and labor negotiations. The Company assumes no

responsibility to publicly amend, modify or revise any forward looking statement, on the basis of any

subsequent development, information or events, or otherwise.

2

8/3/2019 Raymond Cp 11

http://slidepdf.com/reader/full/raymond-cp-11 3/25

ABOUT RAYMOND GROUP

3

One of India's largest branded fabric and fashion retailer, with some of thebest brands in its portfolio

Eight decades old group, in operation since 1925

Integrated across the value chain

One of the largest exclusive retail networks in the textile and fashion spacein India

8/3/2019 Raymond Cp 11

http://slidepdf.com/reader/full/raymond-cp-11 4/25

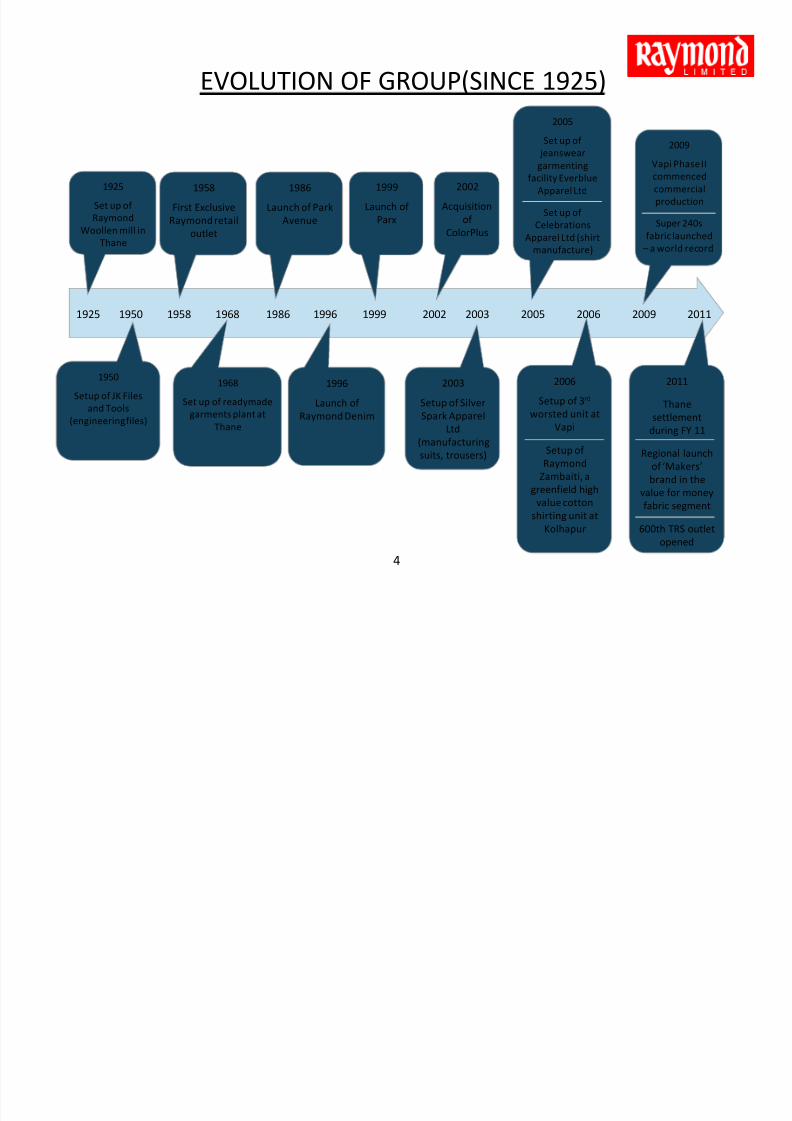

EVOLUTION OF GROUP(SINCE 1925)

1925 1950 1958 1968 1986 1996 2002 2003 2005 2006 2009 2011

1950

Setup of JK Files

and Tools

(engineering files)

1925

Set up of

Raymond

Woollen mill in

Thane

1958

First Exclusive

Raymond retail

outlet

1968

Set up of readymade

garments plant atThane

1996

Launch of

Raymond Denim

2003

Setup of Silver

Spark ApparelLtd

(manufacturing

suits, trousers)

2006

Setup of 3rd

worsted unit atVapi

Setup of

Raymond

Zambaiti, a

greenfield high

value cotton

shirting unit at

Kolhapur

1986

Launch of Park

Avenue

2002

Acquisition

of

ColorPlus

2011

Thane

settlementduring FY 11

Regional launch

of ‘Makers’

brand in the

value for money

fabric segment

600th TRS outlet

opened

2005

Set up of jeanswear

garmenting

facility Everblue

Apparel Ltd

Set up of

Celebrations

Apparel Ltd (shirt

manufacture)

2009

Vapi Phase II

commenced

commercial

production

Super 240s

fabric launched

– a world record

1999

1999

Launch of

Parx

4

8/3/2019 Raymond Cp 11

http://slidepdf.com/reader/full/raymond-cp-11 5/25

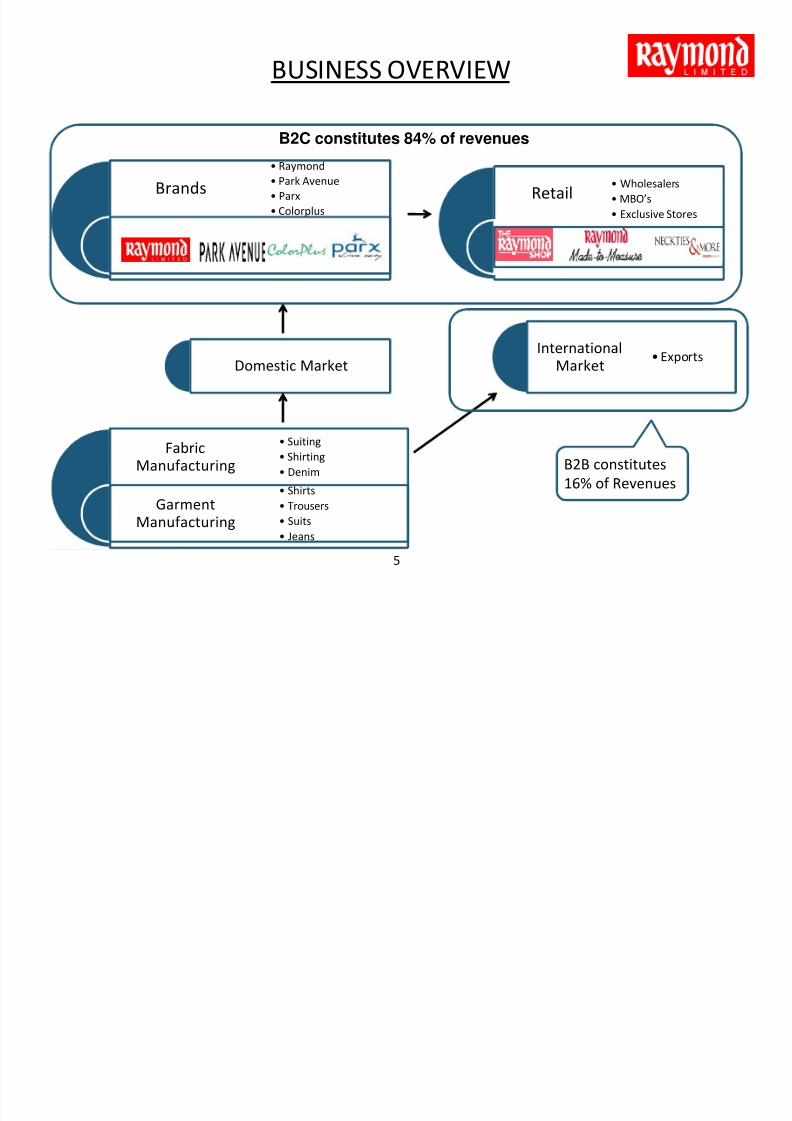

FabricManufacturing

GarmentManufacturing

• Suiting

• Shirting

• Denim

• Shirts

• Trousers

• Suits

• Jeans

InternationalMarket

• Exports

Brands

• Raymond

• Park Avenue

• Parx

• Colorplus

Domestic Market

B2C constitutes 84% of revenues

B2B constitutes

16% of Revenues

BUSINESS OVERVIEW

5

Retail• Wholesalers

• MBO’s

• Exclusive Stores

8/3/2019 Raymond Cp 11

http://slidepdf.com/reader/full/raymond-cp-11 6/25

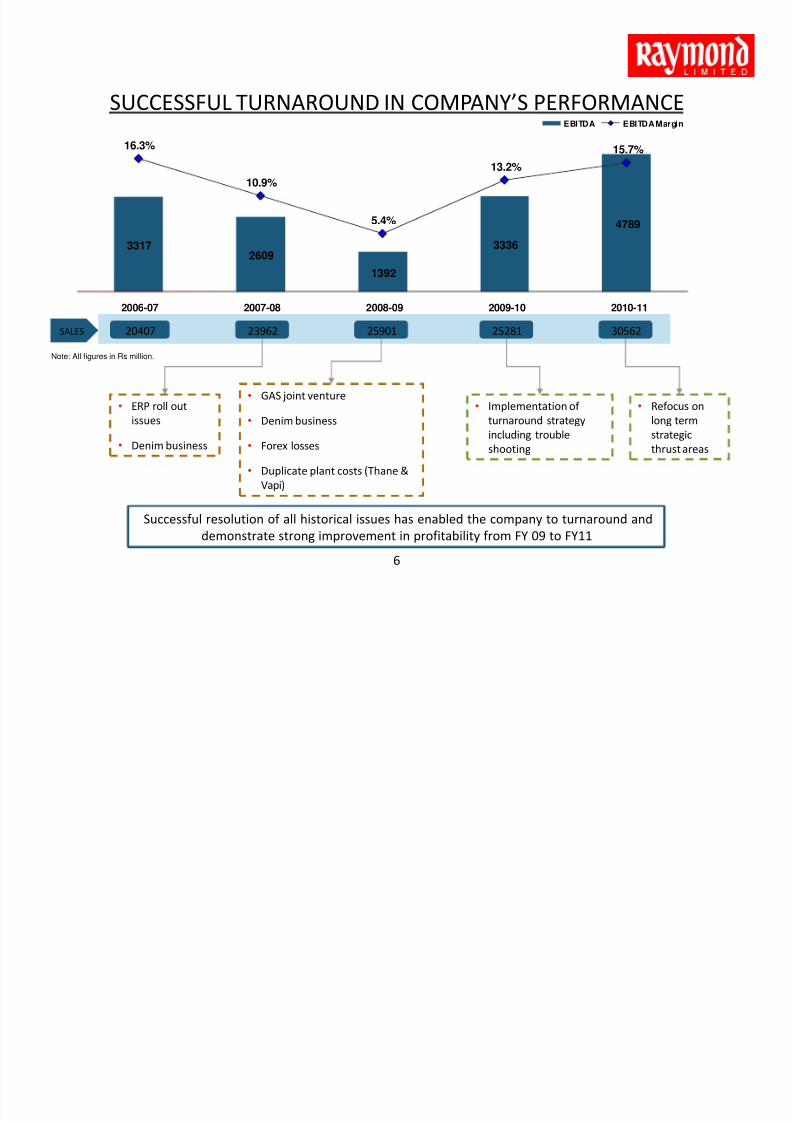

33172609

1392

3336

4789

16.3%

10.9%

5.4%

13.2%

15.7%

2006-07 2007-08 2008-09 2009-10 2010-11

EBITDA EBITDA Margin

SUCCESSFUL TURNAROUND IN COMPANY’S PERFORMANCE

• ERP roll out

issues

• Denim business

• Refocus on

long term

strategic

thrust areas

• GAS joint venture

• Denim business

• Forex losses

• Duplicate plant costs (Thane &

Vapi)

• Implementation of

turnaround strategy

including trouble

shooting

Note: All figures in Rs million.

20407 23962 25901 25281 30562SALES

Successful resolution of all historical issues has enabled the company to turnaround and

demonstrate strong improvement in profitability from FY 09 to FY11

6

8/3/2019 Raymond Cp 11

http://slidepdf.com/reader/full/raymond-cp-11 7/25

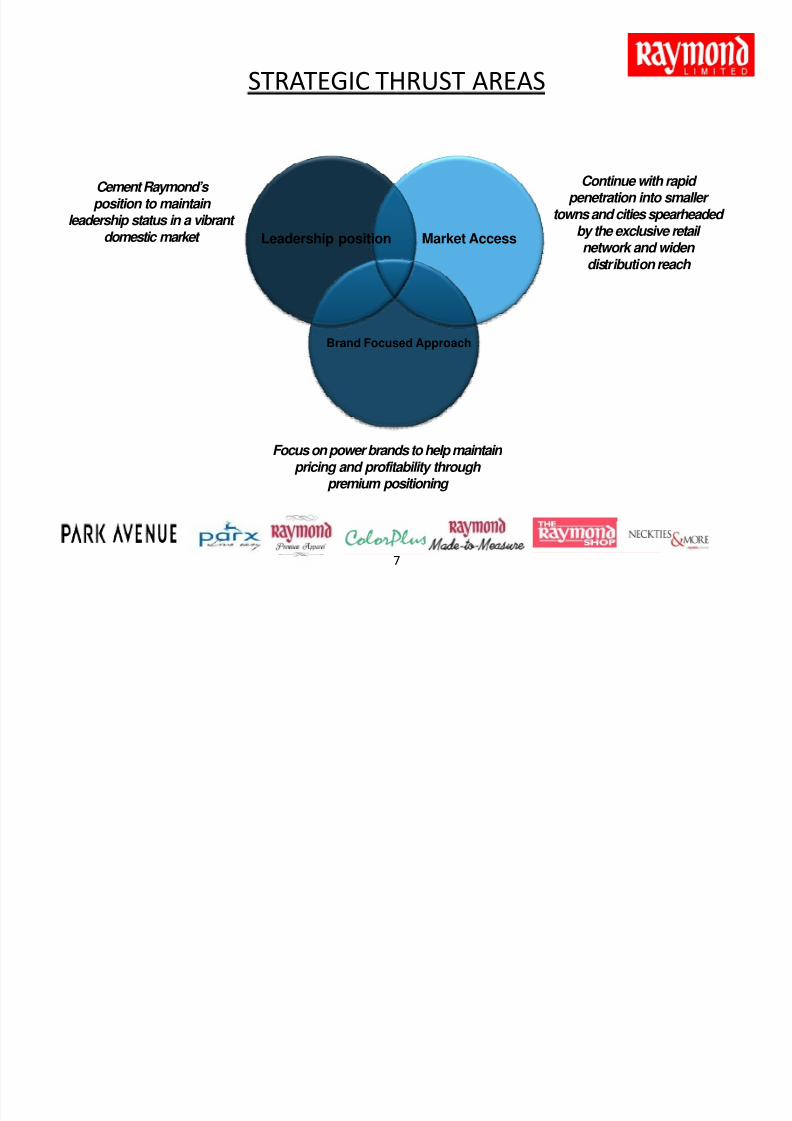

STRATEGIC THRUST AREAS

Focus on power brands to help maintain pricing and profitability through

premium positioning

Continue with rapid penetration into smaller

towns and cities spearheaded by the exclusive retail network and widen distribution reach

Cement Raymond’s position to maintain

leadership status in a vibrant domestic market

7

Brand Focused Approach

Market AccessLeadership position

8/3/2019 Raymond Cp 11

http://slidepdf.com/reader/full/raymond-cp-11 8/25

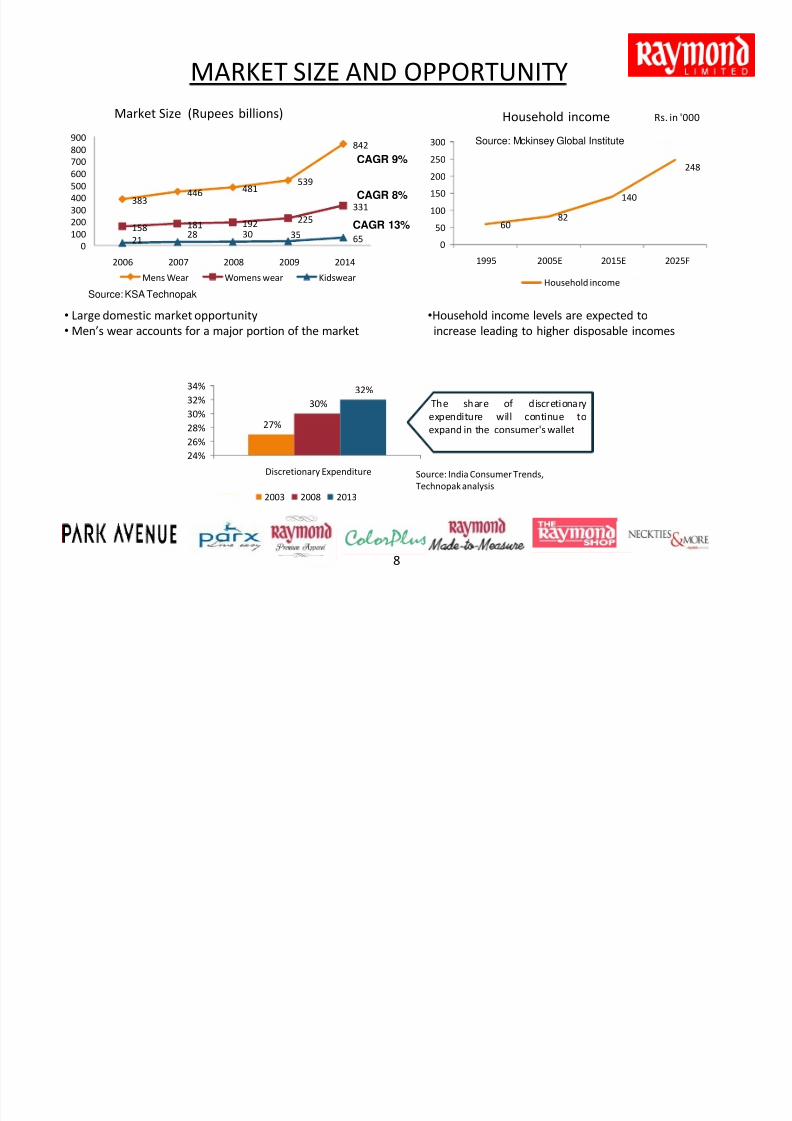

MARKET SIZE AND OPPORTUNITY

8

6082

140

248

0

50

100

150

200

250

300

1995 2005E 2015E 2025F

Household income

Household income

Rs. in '000

•Household income levels are expected to

increase leading to higher disposable incomes

Source: Mckinsey Global Institute

• Large domestic market opportunity

• Men’s wear accounts for a major portion of the market

Market Size (Rupees billions)

Source: KSA Technopak

383446 481

539

842

158 181 192 225

331

2128 30 35 65

0

100

200

300

400

500

600

700

800900

2006 2007 2008 2009 2014

Mens Wear Womens wear Kidswear

CAGR 13%

CAGR 9%

CAGR 8%

The share of discretionary

expenditure will continue toexpand in the consumer's wallet

Source: India Consumer Trends,

Technopak analysis

27%

30%

32%

24%

26%

28%30%

32%

34%

Discretionary Expenditure

2003 2008 2013

8/3/2019 Raymond Cp 11

http://slidepdf.com/reader/full/raymond-cp-11 9/25

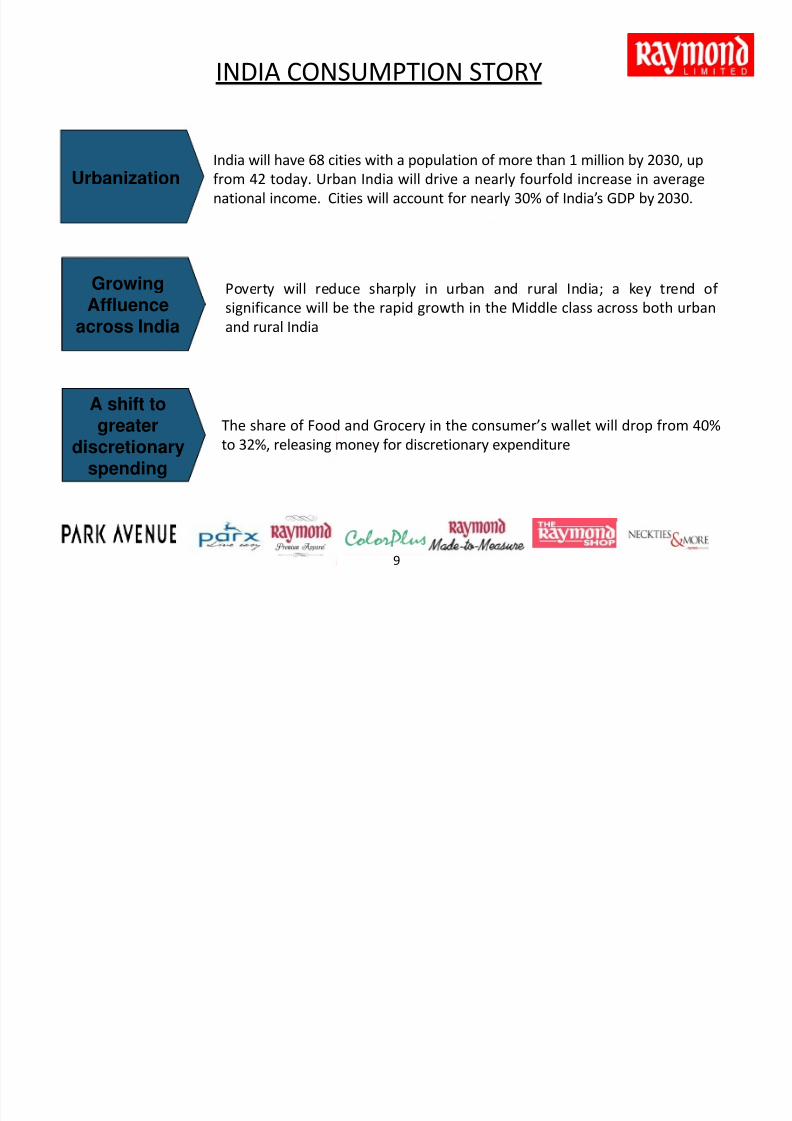

India will have 68 cities with a population of more than 1 million by 2030, up

from 42 today. Urban India will drive a nearly fourfold increase in average

national income. Cities will account for nearly 30% of India’s GDP by 2030.

Urbanization

A shift togreater

discretionaryspending

The share of Food and Grocery in the consumer’s wallet will drop from 40%

to 32%, releasing money for discretionary expenditure

INDIA CONSUMPTION STORY

9

GrowingAffluence

across India

Poverty will reduce sharply in urban and rural India; a key trend of

significance will be the rapid growth in the Middle class across both urban

and rural India

8/3/2019 Raymond Cp 11

http://slidepdf.com/reader/full/raymond-cp-11 10/25

BRAND STRENGTH

Source: TNS Global Market research

10

0

10

20

30

40

50

60

Raymond Vimal Gwalior Siyaram Reid &

Taylor

Mayur Dinesh

May-June’09 Jul- Sept’09 Oct – Dec’09 Jan – Mar’10

Brand salience - Top of mind recall

0

20

40

60

80

100120

Raymond Vimal Gwalior Siyaram Reid &

Taylor

Mayur Dinesh

May-June’09 Jul-Sept’09 Oct – Dec’09 Jan – Mar’10

Brand salience - Spontaneous recall

Source: TNS Global Market research

‘Raymond’ has maintained its leadership position in brand track studies as compared to its

competitors

‘Park Avenue’ won the award for ‘Most Admired Menswear Brand 2009’ at Images Fashion

Have recently launched the new ‘Park Avenue’ mnemonic and logo which has a young,

contemporary, global appeal.

8/3/2019 Raymond Cp 11

http://slidepdf.com/reader/full/raymond-cp-11 11/25

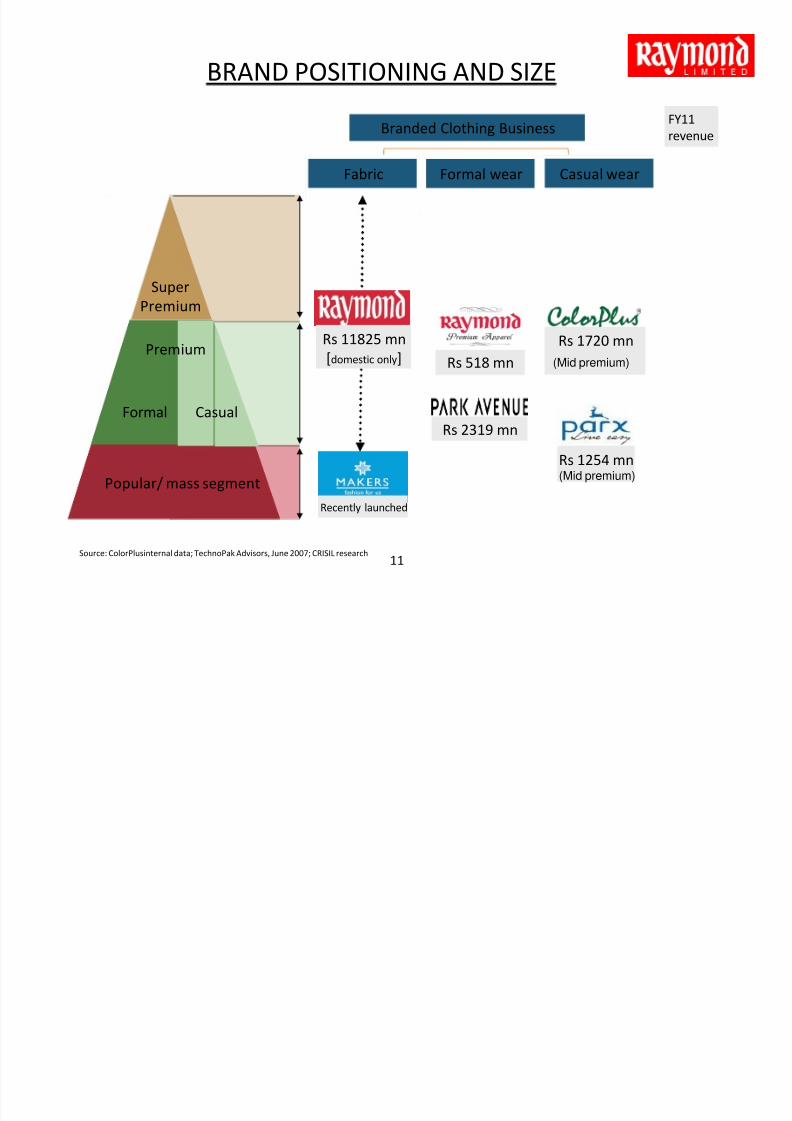

BRAND POSITIONING AND SIZE

Formal wear

Source: ColorPlusinternal data; TechnoPak Advisors, June 2007; CRISIL research

Popular/ mass segment

Formal

Super

Premium

Casual wear

Rs 1254 mn

FY11

revenue

Fabric

Rs 11825 mn

[domestic only]

Casual

Premium

Branded Clothing Business

11

Rs 2319 mn

Rs 518 mn

Rs 1720 mn

(Mid premium)

(Mid premium)

Recently launched

8/3/2019 Raymond Cp 11

http://slidepdf.com/reader/full/raymond-cp-11 12/25

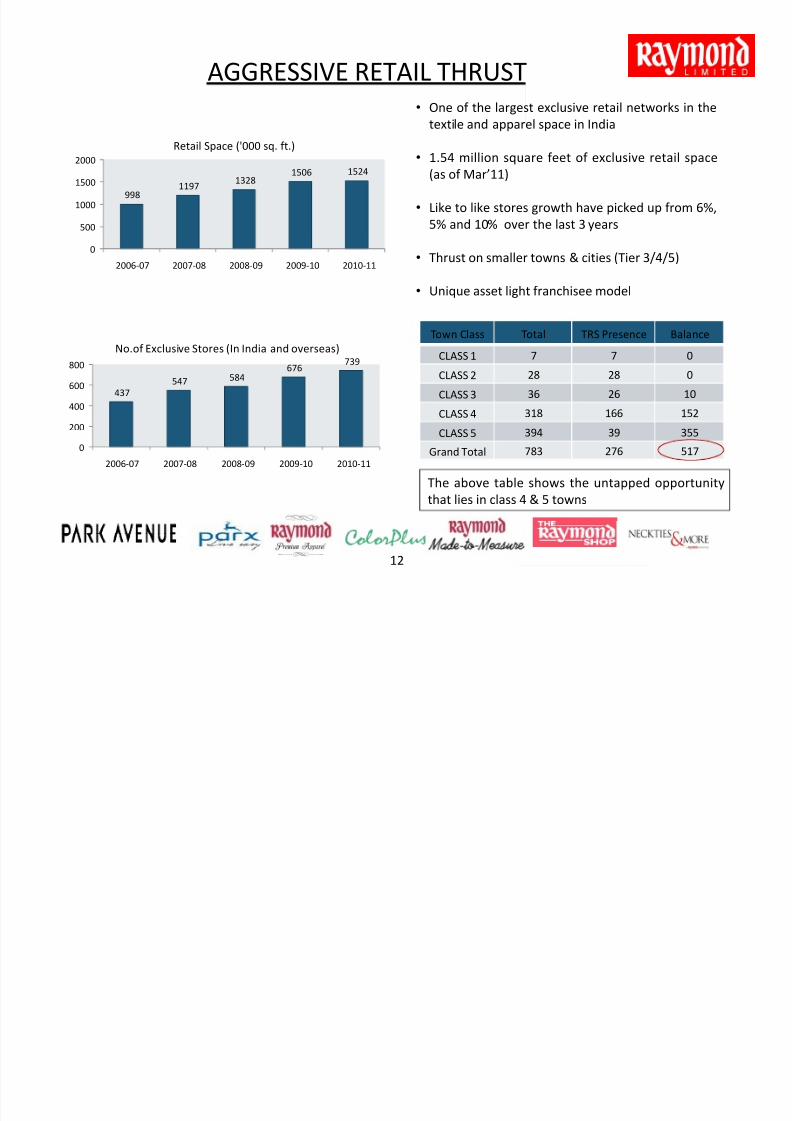

AGGRESSIVE RETAIL THRUST• One of the largest exclusive retail networks in the

textile and apparel space in India

• 1.54 million square feet of exclusive retail space

(as of Mar’11)

• Like to like stores growth have picked up from 6%,

5% and 10% over the last 3 years

• Thrust on smaller towns & cities (Tier 3/4/5)

• Unique asset light franchisee model

12

Town Class Total TRS Presence Balance

CLASS 1 7 7 0

CLASS 2 28 28 0

CLASS 3 36 26 10

CLASS 4 318 166 152CLASS 5 394 39 355

Grand Total 783 276 517

9981197

13281506 1524

0

500

1000

1500

2000

2006-07 2007-08 2008-09 2009-10 2010-11

Retail Space ('000 sq. ft.)

The above table shows the untapped opportunity

that lies in class 4 & 5 towns

437

547 584676

739

0

200

400

600

800

2006-07 2007-08 2008-09 2009-10 2010-11

No.of Exclusive Stores (In India and overseas)

8/3/2019 Raymond Cp 11

http://slidepdf.com/reader/full/raymond-cp-11 13/25

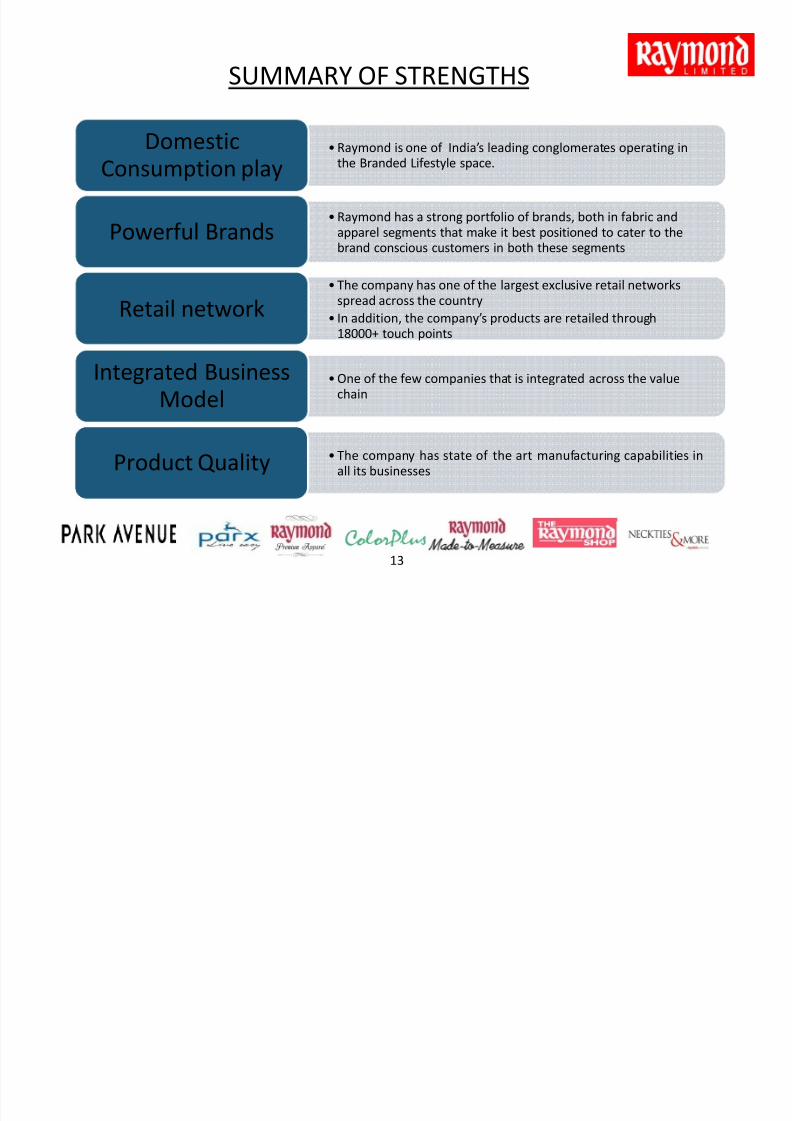

SUMMARY OF STRENGTHS

13

• Raymond is one of India’s leading conglomerates operating inthe Branded Lifestyle space.

DomesticConsumption play

• Raymond has a strong portfolio of brands, both in fabric andapparel segments that make it best positioned to cater to thebrand conscious customers in both these segments

Powerful Brands

• The company has one of the largest exclusive retail networksspread across the country

• In addition, the company’s products are retailed through18000+ touch points

Retail network

• One of the few companies that is integrated across the valuechain

Integrated BusinessModel

• The company has state of the art manufacturing capabilities inall its businessesProduct Quality

8/3/2019 Raymond Cp 11

http://slidepdf.com/reader/full/raymond-cp-11 14/25

2164

2622

3675

0

500

1000

1500

2000

2500

3000

3500

4000

FY09 FY10 FY11

EBITDA (Rs million)

1137912229

14854

0

2000

4000

6000

8000

10000

12000

14000

16000

FY09 FY10 FY11

Sales (Rs million)

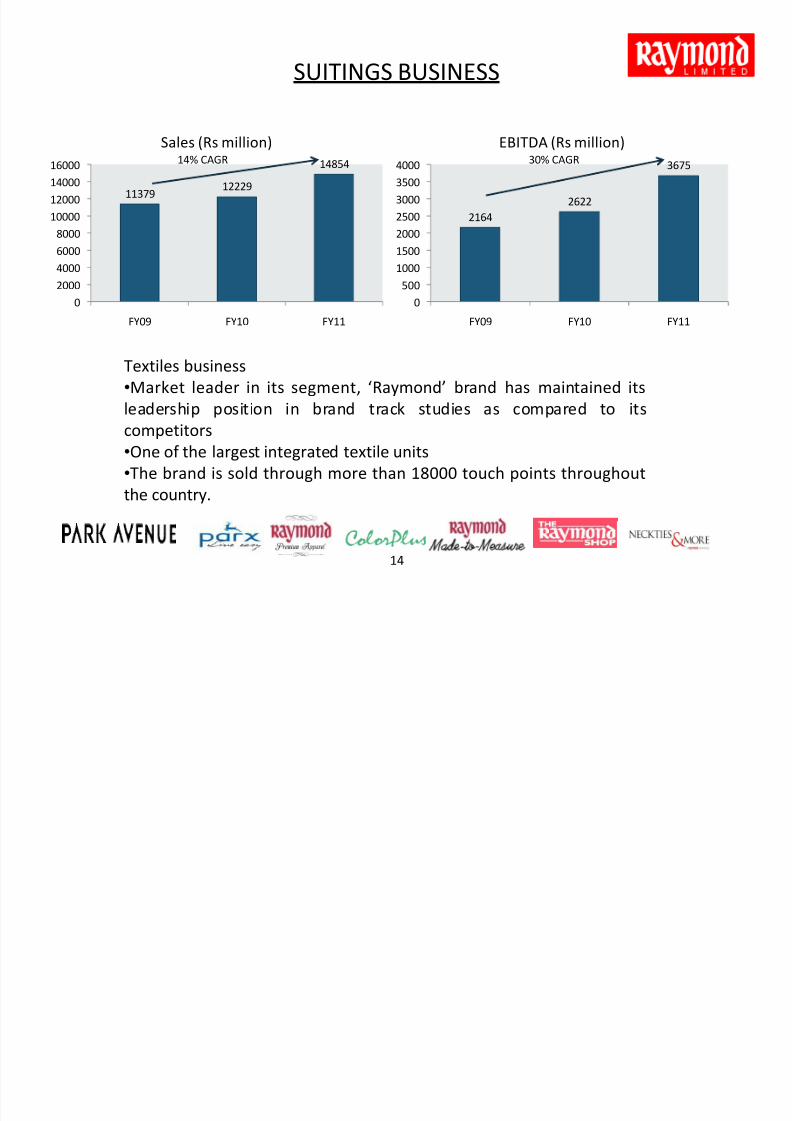

SUITINGS BUSINESS

14

Textiles business

•Market leader in its segment, ‘Raymond’ brand has maintained its

leadership position in brand track studies as compared to itscompetitors

•One of the largest integrated textile units

•The brand is sold through more than 18000 touch points throughout

the country.

14

14% CAGR 30% CAGR

8/3/2019 Raymond Cp 11

http://slidepdf.com/reader/full/raymond-cp-11 15/25

56935562

6408

5000

5200

5400

5600

5800

6000

6200

6400

6600

FY09 FY10 FY11

Sales (Rs million)

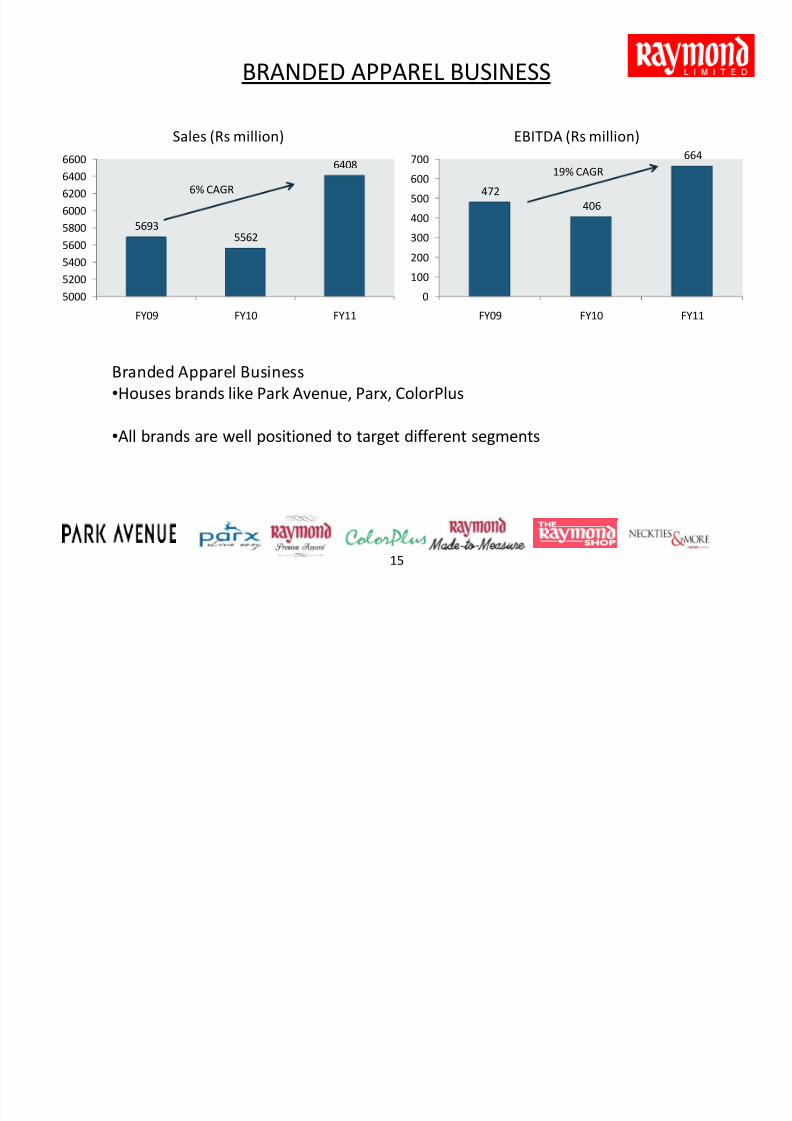

BRANDED APPAREL BUSINESS

15

Branded Apparel Business

•Houses brands like Park Avenue, Parx, ColorPlus

•All brands are well positioned to target different segments

15

472

406

664

0

100

200

300

400

500

600

700

FY09 FY10 FY11

EBITDA (Rs million)

6% CAGR

19% CAGR

8/3/2019 Raymond Cp 11

http://slidepdf.com/reader/full/raymond-cp-11 16/25

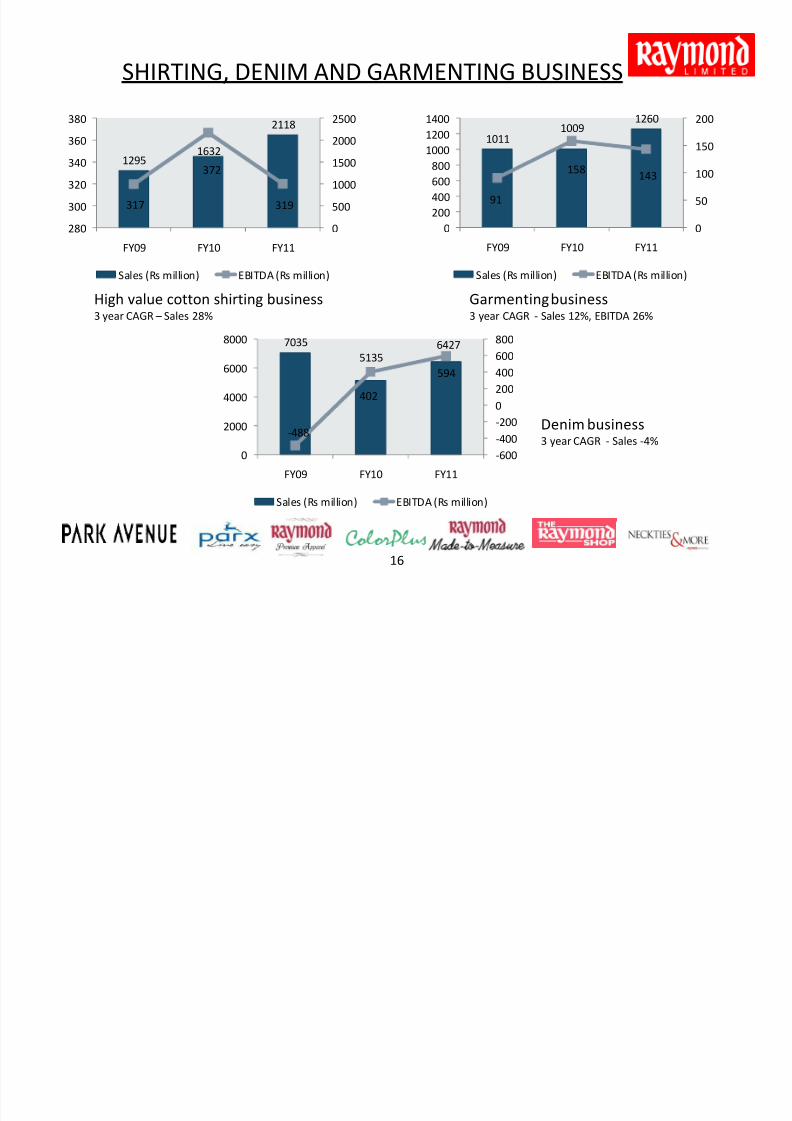

SHIRTING, DENIM AND GARMENTING BUSINESS

16

16

12951632

2118

317

372

319

0

500

1000

1500

2000

2500

280

300

320

340

360

380

FY09 FY10 FY11

Sales (Rs million) EBITDA (Rs million)

1011

10091260

91

158143

0

50

100

150

200

0

200

400

600

800

10001200

1400

FY09 FY10 FY11

Sales (Rs million) EBITDA (Rs million)

High value cotton shirting business3 year CAGR – Sales 28%

Garmenting business3 year CAGR - Sales 12%, EBITDA 26%

Denim business3 year CAGR - Sales -4%

7035

51356427

-488

402

594

-600

-400

-200

0

200

400

600

800

0

2000

4000

6000

8000

FY09 FY10 FY11

Sales (Rs million) EBITDA (Rs million)

8/3/2019 Raymond Cp 11

http://slidepdf.com/reader/full/raymond-cp-11 17/25

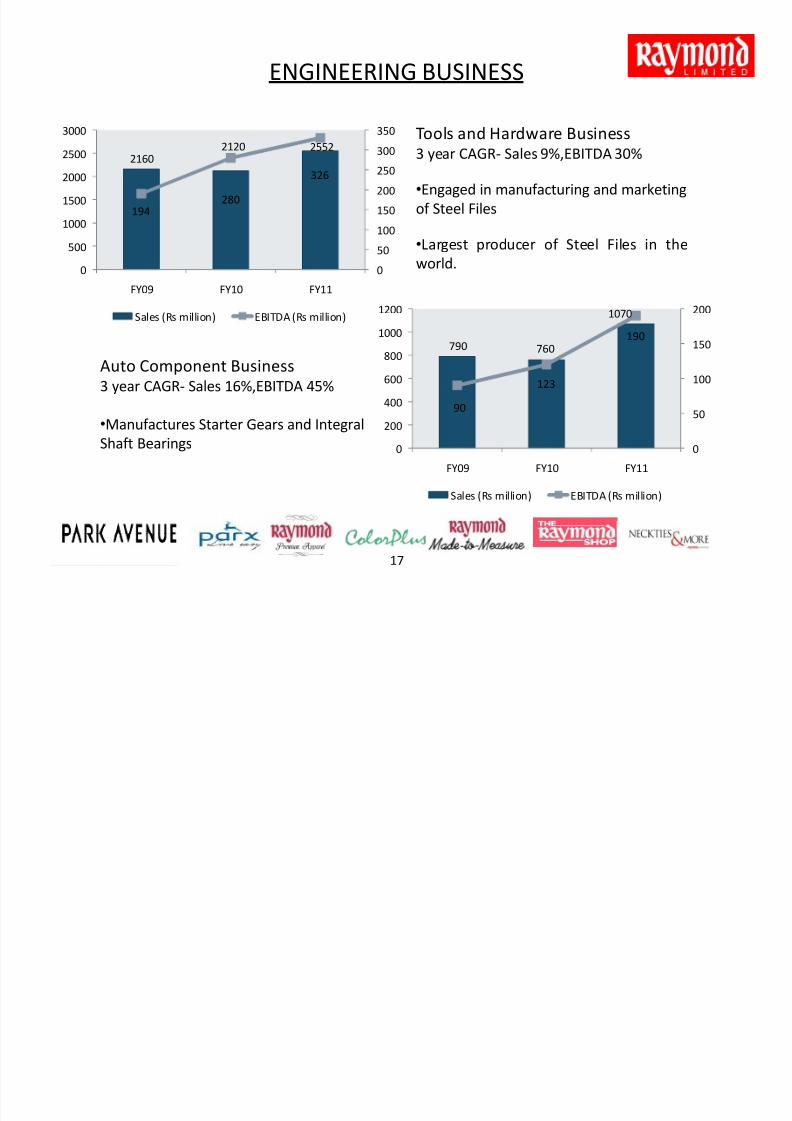

ENGINEERING BUSINESS

21602120 2552

194280

326

0

50

100

150

200

250

300

350

0

500

1000

1500

2000

2500

3000

FY09 FY10 FY11

Sales (Rs million) EBITDA (Rs million)

Tools and Hardware Business3 year CAGR- Sales 9%,EBITDA 30%

•Engaged in manufacturing and marketing

of Steel Files

•Largest producer of Steel Files in the

world.

790 760

1070

90

123

190

0

50

100

150

200

0

200

400

600

800

1000

1200

FY09 FY10 FY11

Sales (Rs million) EBITDA (Rs million)

Auto Component Business3 year CAGR- Sales 16%,EBITDA 45%

•Manufactures Starter Gears and Integral

Shaft Bearings

17

8/3/2019 Raymond Cp 11

http://slidepdf.com/reader/full/raymond-cp-11 18/25

ANNEXURES

18

8/3/2019 Raymond Cp 11

http://slidepdf.com/reader/full/raymond-cp-11 19/25

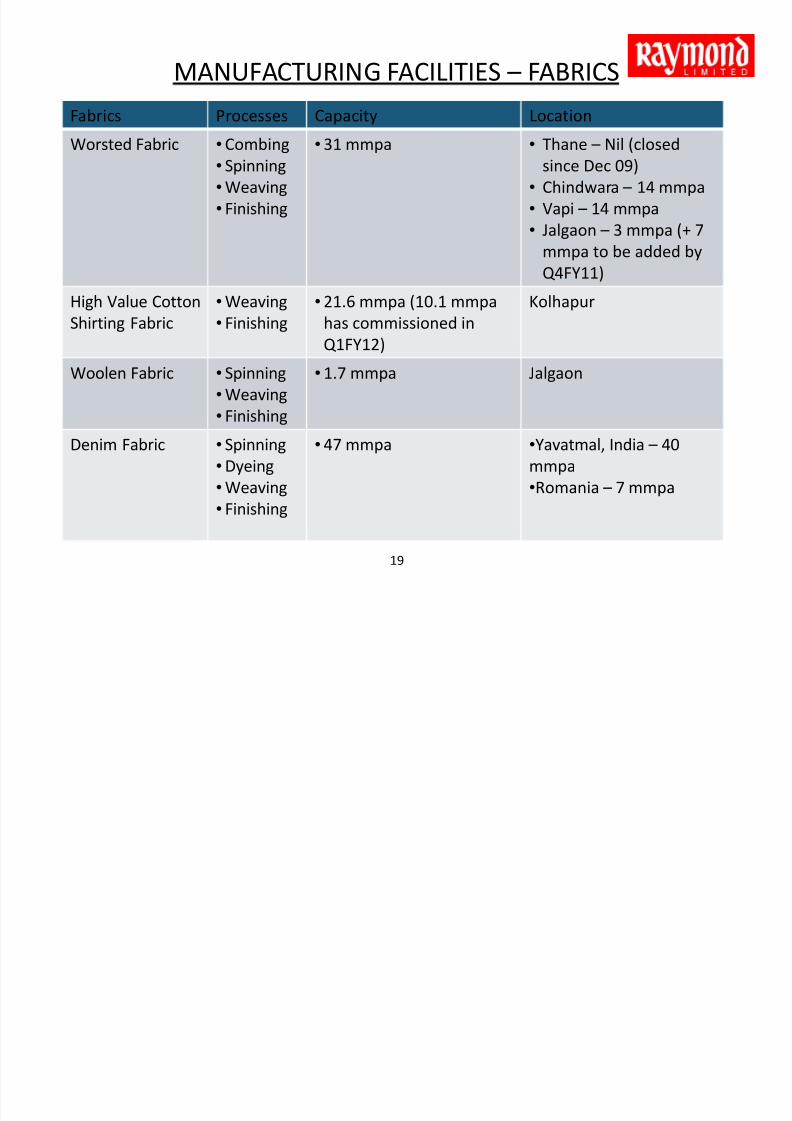

MANUFACTURING FACILITIES – FABRICS

Fabrics Processes Capacity Location

Worsted Fabric • Combing• Spinning

• Weaving

• Finishing

• 31 mmpa • Thane – Nil (closedsince Dec 09)

• Chindwara – 14 mmpa

• Vapi – 14 mmpa

• Jalgaon – 3 mmpa (+ 7

mmpa to be added by

Q4FY11)High Value Cotton

Shirting Fabric

• Weaving

• Finishing

• 21.6 mmpa (10.1 mmpa

has commissioned in

Q1FY12)

Kolhapur

Woolen Fabric • Spinning

• Weaving

• Finishing

• 1.7 mmpa Jalgaon

Denim Fabric • Spinning

• Dyeing

• Weaving

• Finishing

• 47 mmpa •Yavatmal, India – 40

mmpa

•Romania – 7 mmpa

19

8/3/2019 Raymond Cp 11

http://slidepdf.com/reader/full/raymond-cp-11 20/25

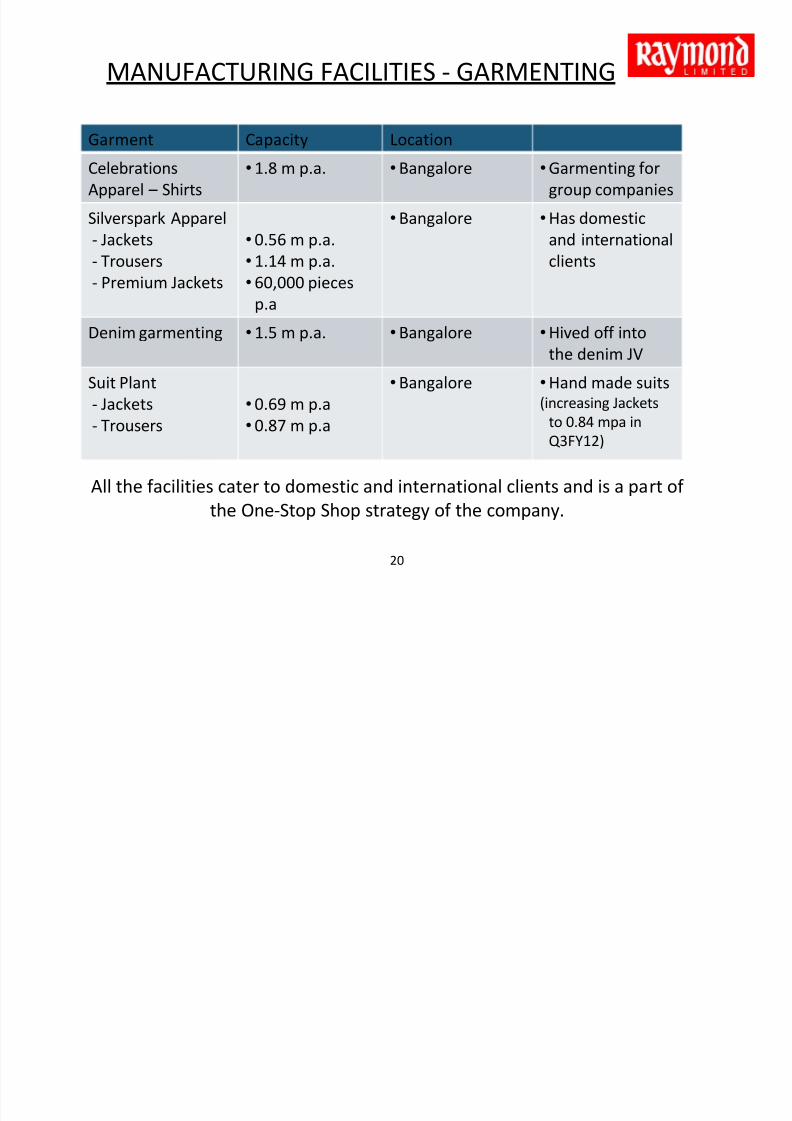

MANUFACTURING FACILITIES - GARMENTING

Garment Capacity Location

Celebrations

Apparel – Shirts

• 1.8 m p.a. • Bangalore • Garmenting for

group companies

Silverspark Apparel

- Jackets

- Trousers

- Premium Jackets

• 0.56 m p.a.

• 1.14 m p.a.

• 60,000 piecesp.a

• Bangalore • Has domestic

and international

clients

Denim garmenting • 1.5 m p.a. • Bangalore • Hived off into

the denim JV

Suit Plant

- Jackets

- Trousers

• 0.69 m p.a

• 0.87 m p.a

• Bangalore • Hand made suits(increasing Jackets

to 0.84 mpa inQ3FY12)

All the facilities cater to domestic and international clients and is a part of

the One-Stop Shop strategy of the company.

20

8/3/2019 Raymond Cp 11

http://slidepdf.com/reader/full/raymond-cp-11 21/25

SOME RECENT INITIATIVESBelow are some of the opened The Raymond Shops (TRS ) by the company.

21

Zaheerabad ,Andhra Pradesh

Ujjain

(Madhya Pradesh)

8/3/2019 Raymond Cp 11

http://slidepdf.com/reader/full/raymond-cp-11 22/25

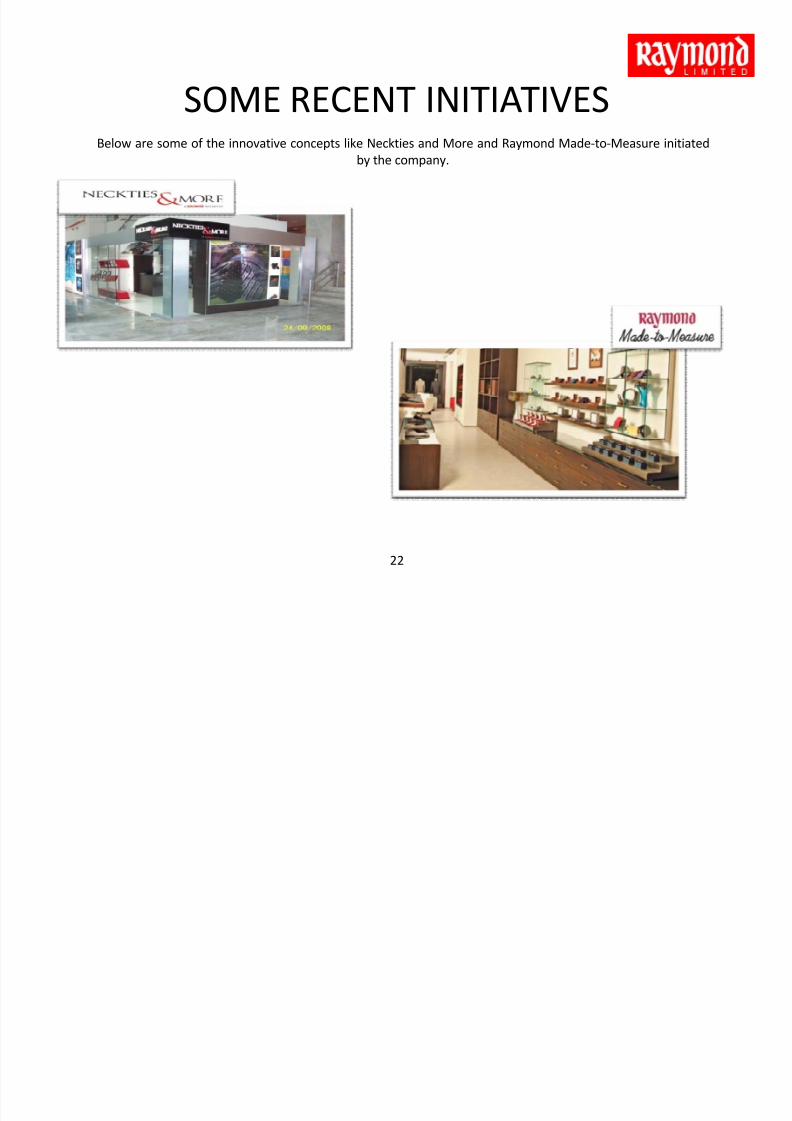

SOME RECENT INITIATIVESBelow are some of the innovative concepts like Neckties and More and Raymond Made-to-Measure initiated

by the company.

22

8/3/2019 Raymond Cp 11

http://slidepdf.com/reader/full/raymond-cp-11 23/25

BOARD OF DIRECTORS

• Mr Gautam Hari Singhania, Chairman & Managing Director

– Was appointed the Wholetime Director on the Board of Raymond Ltd. in 1990 and was elevated to the position of Managing Director in mid-1999

– Has steered Raymond Limited with a single-minded focus of being the best brand in India

• Dr Vijaypat Singhania, Chairman Emeritus

– Has nearly four decades of experience in the management of several industrial units as the Chief Executive, evenbefore his current position

– Has been instrumental for the successful growth and diversification plans of the Company

• Mr. H. Sunder, Whole-time Director

– Has over 26 years of experience in finance, taxation, accounts, legal, secretarial areas, international business andgeneral corporate management

– He is the President – Finance and Group Chief Financial Officer of the Company since 2006. He has been with theCompany for over 14 years.

• Mr I D Agarwal, Independent Director

– Has 37 years of experience in Banking, Finance and Currency, Former Executive Director, Reserve Bank of India, wasan Advisor to the United Nations and has been the Director of Small Industries Development Bank of India

• Mr Pradeep Guha, Independent Director – Has recently finished a very successful stint as the CEO of India's largest satellite broadcasting network, Zee

Entertainment Enterprises Ltd

– Associated with the print medium for 29 years and was President of The Times of India group

23

8/3/2019 Raymond Cp 11

http://slidepdf.com/reader/full/raymond-cp-11 24/25

BOARD OF DIRECTORS• Mr P K Bhandari, Non Executive Director

– Has over 25 years of experience in the field of project finance, industry, business and corporate management

– Joined the Company in 1989, played a key role in strategizing and implementing the Company's restructuring program

• Mr Nabankur Gupta, Independent Director

– Joined the Company as Group President on August 1, 2000 and was co-opted on the Board of Directors of the

Company as Wholetime Director and Group President effective January 15, 2001.

– Was the first Indian to receive recognition by the Advertising Age International, New York, in 1995 with the title of

‘Marketing Superstar‘

• Mr Sailesh Haribhakti, Independent Director

– A renowned Chartered Accountant, Director on the Board of 20 highly acclaimed public and private companies

holding the position of Chairman or Member of Audit Committee in ten of them

– Was a member of the ICAI's Group on Implementation of Convergence with IFRS, has been awarded "The Best Non

Executive Independent Director Award 07" by Asian Centre for Corporate Governance

• Mr Akshay Chudasama, Independent Director (wef 21.04.2011)

– Partner in JSA, a reputed Law Firm.

– He specializes in Mergers & Acquisitions, Joint Ventures, Cross Border Investments, Private Equity, Real Estate,

Hospitality, Franchising and Media & Entertainment law

• Mr Boman R Irani, Independent Director (wef 21.04.2011)

– He is the chairman of Rustomjee Group.

– Leading Real estate developer and leader in construction industry. He is a first generation developer and an

entrepreneur.

24

8/3/2019 Raymond Cp 11

http://slidepdf.com/reader/full/raymond-cp-11 25/25

THANK YOU

25