Embed Size (px)

Citation preview

Direction des Études et Synthèses Économiques

G 2013 / 15

Which size and evolution of the government expenditure multiplier in France (1980-2010)?

Guillaume CLÉAUD*, Matthieu LEMOINE#

et Pierre-Alain PIONNIER*

Document de travail

Institut National de la Statistique et des Études Économiques

INSTITUT NATIONAL DE LA STATISTIQUE ET DES ÉTUDES ÉCONOMIQUES

Série des documents de travail de la Direction des Études et Synthèses Économiques

DÉCEMBRE 2013

Nous remercions pour leurs commentaires Frédérique BEC, Éric DUBOIS, Luca GAMBETTI, Emmanuel JESSUA, Julien MATHERON, Michel NORMANDIN, Vladimir PASSERON, Corinne PROST, les participants aux séminaires du département des études économiques de l’INSEE, du CREST-LMA et de la Banque de France, ainsi que les participants aux conférences T2M 2013 et ISF 2013. Nous remercions également Sophie GAIGNON d’avoir constitué la base de données des prévisions d’investissement public.

_____________________________________________ * Au moment de la rédaction de l’étude : Département des Études Économiques - Division « Études Macroéconomiques » Timbre G220 -

15, bd Gabriel Péri - BP 100 - 92244 MALAKOFF CEDEX et CREST-LMA -15, bd Gabriel Péri - 92245 MALAKOFF CEDEX # Banque de France - Direction générale des Études et des Relations Internationales - 31, rue Croix des Petits Champs - 75049

Paris CEDEX 01. The views expressed in this paper do not necessarily reflect those of Banque de France.

Département des Études Économiques - Timbre G201 - 15, bd Gabriel Péri - BP 100 - 92244 MALAKOFF CEDEX - France - Tél. : 33 (1) 41 17 60 68 - Fax : 33 (1) 41 17 60 45 - CEDEX - E-mail : [email protected] - Site Web Insee : http://www.insee.fr

Ces documents de travail ne reflètent pas la position de l’Insee et n'engagent que leurs auteurs.

Working papers do not reflect the position of INSEE but only their author's views.

G 2013 / 15

Which size and evolution of the government expenditure multiplier in France (1980-2010)?

Guillaume CLÉAUD*, Matthieu LEMOINE#

et Pierre-Alain PIONNIER*

Which size and evolution of the government expenditure multiplier in France (1980-2010)?

Abstract The importance of the stimulus packages that were injected in most advanced economies from the start of the financial crisis and the speed at which budgets are now being consolidated in Europe has revived the long-lasting debate on the size of fiscal multipliers. In this study, we focus on government expenditures on goods and services. Our conclusion following Blanchard and Perotti (2002) for the identification of government spending shocks is that the multiplier is significant and not far from 1 on impact and becomes statistically insignificant after about 3 years in France. We provide numerous robustness checks concerning the definition of expenditures, assumptions about data stationarity, the role of expectations and the choice of the sample. Moreover, using a time-varying SVAR model, our main findings are (1) that the multiplier did not evolve significantly at any horizon since the beginning of the 1980s and (2) that the variance of shocks hitting the economy evolves a lot more than the model autoregressive parameters. Even in alternative specifications where the Bayesian priors are pushed towards time-variation, the main evolution that we uncover is a (non-significant) decrease of the medium term expenditure multiplier, partly linked to a more aggressive monetary policy since the 1990s. We do not find evidence of an increase of the multiplier during every recession in France, contrary to the finding of Auerbach and Gorodnichenko (2012) for the United States. At least, business cycle conditions do not seem to be the main driver of the evolution of the expenditure multiplier in the last 30 years in France. JEL-codes: E62, C54 Keywords: Government expenditure multiplier, Evolution, TV-SVAR

Quelle amplitude et quelle évolution du multiplicateur de dépenses publiques en France (1980-2010) ?

Résumé L'importance des plans de relance budgétaire mis en œuvre dans la plupart des économies avancées depuis le déclenchement de la crise financière et la vitesse à laquelle les budgets des États sont maintenant consolidés en Europe a donné une nouvelle actualité au débat sur le multiplicateur de dépenses publiques. Cette étude est centrée sur l'effet des dépenses publiques en biens et services. En utilisant la procédure d'identification des chocs de dépenses publiques proposée par Blanchard et Perotti (2002), nous parvenons à la conclusion que le multiplicateur est statistiquement significatif et peu éloigné de 1 à l'impact et qu'il devient non significatif après environ 3 ans en France. Nous effectuons de nombreux tests de robustesse liés à la définition des dépenses publiques, aux hypothèses de stationnarité des variables considérées, à l'effet des anticipations et au choix de l'échantillon de données. Par ailleurs, en estimant un modèle VAR structurel à coefficients variables dans le temps, nous trouvons (1) que le multiplicateur n'a pas significativement évolué, quel que soit l'horizon temporel considéré, depuis le début des années 1980 et (2) que la variance des chocs affectant l'économie évolue bien davantage que les coefficients autorégressifs du modèle. Même avec des spécifications alternatives où les a priori bayésiens favorisent l'évolution des coefficients dans le temps, l'évolution principale est une réduction (non significative) du multiplicateur de moyen terme, en lien avec une politique monétaire plus réactive depuis les années 1990. Nous ne trouvons pas d'indice d'une augmentation systématique du multiplicateur de dépenses publiques lors de chaque récession en France, contrairement à la conclusion d'Auerbach et Gorodnichenko (2012) pour les États-Unis. En tout cas, la position dans le cycle économique ne semble pas être le facteur principal ayant influencé le multiplicateur de dépenses publiques en France au cours des 30 dernières années. Codes JEL : E62, C54 Mots clés : Multiplicateur de dépenses publiques, Évolution, TV-SVAR

1 Introduction

The importance of the stimulus packages that were injected in most advanced economiesfrom the start of the financial crisis and the speed at which budgets are now beingconsolidated in Europe has revived the long-lasting debate on the size of fiscal multipliers.There is no clear theoretical answer to this question. These multipliers may depend,among other factors, on the expenditures, transfers and taxes that are being considered,on the degree of openness of the economy, and on the reaction of monetary policy. Forthese reasons, these multipliers may not be unique and may change over time.

This paper focuses on the evolution of the expenditure multiplier in France during thelast 30 years. Our definition of expenditures is more restrictive than the sum of govern-ment consumption and investment computed in national accounts. It only correspondsto the purchase of goods and services by the government and does not include the com-pensation of civil servants (see Appendix B). Although the statistical model developedin this paper entails a measure of government net receipts, the focus on expenditures ismotivated by two reasons. First, government net receipts include very different kinds oftaxes and their evolution may be explained by modifications of marginal tax rates or oftax bases, whose effect on economic activity could be very different. Second, a shockon government expenditures is easier to identify than a shock on government receipts,especially in a time-varying context (see infra).

Very few papers try to assess if the size of fiscal multipliers has evolved over time.Our work is closely related to Kirchner et al. (2010) and to Auerbach and Gorodnichenko(2012) which are the two main contributions in this field. Kirchner et al. (2010) estimate atime-varying structural VAR (TV-SVAR) on Euro-Area data starting in 1980Q1 whereasAuerbach and Gorodnichenko (2012) estimate a regime-switching VAR model on U.S.post-WWII quarterly data1. Both of these studies also focus on the evolution of theexpenditure multiplier.

Kirchner et al. (2010) conclude that the short run effectiveness of government spend-ing in stimulating GDP in the Euro-Area (as a whole) increased until the end-1980s andcontinuously decreased afterwards. Their impact spending multiplier has a value of 0.7in 1980 and 0.5 in 2008, with an intermediary value slightly above 1 at the end of the1980s. Their long run spending multiplier continuously decreases from -0.7 to -1.7: thiscontinuous evolution in the long run is the main evolution that they uncover. At thisstage, we can already notice that the multipliers computed by Kirchner et al. (2010)reach their lowest value at the beginning of the Great Recession. However, they do not

1Auerbach and Gorodnichenko (2012) impose that the regimes are linked to the state of the businesscycle (expansion or recession)

3

report the shape of the probability distribution around their median estimates.Auerbach and Gorodnichenko (2012) report that the spending multiplier in the United

States is significantly higher during recessions (2.2 after 5 years) than it is during expan-sions (-0.3 after 5 years). However, this result is driven by defense expenditures onlywhose share in total government expenditures is much higher in the United Stated thanin France2. The non-defense spending multipliers estimated by Auerbach et al. (2012) arenot significantly different during recessions and expansions3 4. Moreover, using a longersample (1890q1-2010q4) and relying on a different econometric methodology (local pro-jections rather than VARs), Owyang et al. (2013) do not observe higher multipliers duringtimes of slack in the United States. Given that VARs cannot be considered as alwayssuperior to local projections from a theoretical point of view (Jorda (2005)), there seemsto be room for further econometric studies on the evolution of governement spendingmultipliers.

There are arguments in favor of a continuous evolution of the size of the multiplier,independently of business cycle conditions. For instance, the French economy has becomemore open since the beginning of the 1980s and this could have led to a growing leakageeffect, an argument often heard in the French public debate on the effectiveness of a fiscalstimulus. Moreover, the monetary policy reaction to a fiscal stimulus might have changed.Disinflation became a priority of the French central bank at the beginning of the 1990s,in order for France to qualify for the euro; the French central bank became independentin 1993 and its prerogatives were partly transferred to the European Central Bank (ECB)in 1999. Finally, opposite effects may have influenced the size of the multiplier during theGreat Recession: on the one hand, the zero lower bound may have muted the responseof monetary policy and pushed multipliers above one (Christiano et al. 2011, Woodford2011) but on the other hand, the rapid increase of French public debt may have ledconsumers to behave in a more Ricardian way (Sutherland 1997). Hence, we do not

2In the United States, defense expenditures represent 25% of government consumption and investmentfrom 1995 to 2010 and 35% from 1960 to 1994 (NIPA, Table 3.15.5). The breakdown of governmentexpenditures by function is only available since 1995 in France. From 1995 to 2010, defense expendituresrepresent only 6% of all government expenditures in France. This share is roughly the same for thecompensation of civil servants (D1) and for the expenditures on goods and services (P2+P51+D631A).

3When they focus on non-defense spending, Auerbach et al. (2012) compute a multiplier after 5 yearsequal to 1.0 during expansions and to 1.1 during recessions.

4For France, Bouthevillain and Dufrénot (2011) adopt a similar approach and find that the shortrun elasticity of output growth to government spending is 13 percentage points higher during recessionsthan they are during expansions, but this difference is not significant. Using a Neo-Keynesian macro-econometric model with time-varying hysteresis effects, Creel et al. (2011) find for France that theshort run expenditure multiplier is slightly above one whatever the cycle position, whereas the long runmultiplier would stay above one for a shock impulsed at a trough and would fall close to zero for a shockimpulsed at a peak.

4

impose a priori, like Auerbach and Gorodnichenko (2012), that the value of multipliersshould only depend on whether the economy is in a recessionary or in an expansionarystate.

Since time-variation could come from multiple sources, a flexible non-linear modelis the appropriate tool to use. Here, we rely on a time-varying structural VAR (TV-SVAR) model (see Appendix D). The same kind of model has been used by Cogley andSargent (2001), Cogley and Sargent (2005) and Primiceri (2005) to assess the evolutionof monetary policy in the United States and its impact on the economy. All coefficientsof the model, including those of the variance-covariance matrix, are left free to vary overtime. This means that the size of the policy shocks identified by the model, as well astheir contemporaneous and lagged impacts on the economy, are time-dependent. Sincethis model contains a lot of parameters, it is estimated using Bayesian techniques. Indeed,the likelihood function in highly-parameterized models tends to be very complicated. Ittypically contains many narrow peaks, possibly in regions where parameter values areincredible, so that it is difficult for a maximization algorithm to discriminate betweenthem. The use of Bayesian priors allows focusing particularly on certain regions of thelikelihood function.

We rely on a quarterly VAR with five variables (real government expenditures, realgovernment net receipts5, real GDP, GDP deflator and nominal 3-month interest rate).The first three variables are those proposed by Blanchard and Perotti (2002). Like(Perotti 2002), we add the other two variables (GDP deflator and short term interestrate), in order to take into account the feedback of prices and monetary policy. For theidentification of the structural shocks, we assume that government spending does notreact to activity nor to net receipts or interest rates within a quarter. This assumption ismotivated by the fact that there is no evidence of an automatic response of governmentspending to business cycle conditions and that any discretionary response is necessarilydelayed due to the existence of decision and implementation lags6. Finally, we assumethat government spending is fixed in nominal terms, so that the volume of expendituresreacts negatively, with a unitary elasticity, to unexpected inflation within a quarter. Thisis the only difference with Blanchard and Perotti (2002), motivated by the fact that weinclude prices and interest rates in our model7.

5Government net receipts are defined as the sum of government financing capacity and governmentexpenditures (see Appendix B). Hence, for instance, unemployment benefits are treated as a negativereceipt.

6Net receipts can react contemporaneously to business cycle conditions due to the existence of au-tomatic stabilizers but the same lags explain why they cannot react to business cycle conditions in adiscretionary manner within a quarter. However, these considerations would only be important if wetried to identify structural shocks on government net receipts (see Appendix C).

7This identification scheme has already been implemented on French data using a fixed coefficients

5

Two main objections have been raised in the literature against the use of aggregatedata and SVAR models in order to assess the effectiveness of fiscal policy.

First of all, the effect of government spending may vary from one kind of expendituresto another. For instance, government consumption as measured by national accounts iscomposed of both direct purchases of goods and services and compensation of civil ser-vants, two expenditures that do not affect the rest of the economy in the same way. Somegoods and services, if they generate externalities (e.g.: education or research expendi-tures) may also have an indirect impact on the utility of consumers or on the productionfunction of firms. This is why some authors favor the use of defense expenditures only(Barro and Redlick 2009). Another advantage generally put forth to support the use ofdefense expenditures is the fact that they depend on geostrategic considerations ratherthan on business cycle conditions. Thus, they are more easily considered as exogenous.

However, this particular choice of data has two drawbacks. First, it is not sure thatresults obtained with defense expenditures can be extended to non-defense spending.Second, these results, on U.S. data, are mainly driven by what happened during WWIIor the Korean war (Hall 2009) and are not necessarily relevant in the present context(e.g.: goods rationing and capacity constraints during wars, cf. Perotti (2011)). More-over, a multivariate model can effectively address the issue of endogeneity, contrary tothe univariate regressions used by Barro and Redlick (2009). The only identifying as-sumption we need is to suppose that the value of government spending cannot adjustto business conditions within a quarter, which seems reasonable. Finally, we distinguishdirect purchases of goods and services from compensation of civil servants, hence limitingthe heterogeneity issue.

The second objection raised against the use of SVAR models in the context of fis-cal policy concerns the identification scheme and the treatment of expectations. Ramey(2011b) shows that government spending shocks identified following a Blanchard andPerotti procedure on U.S. data are Granger-caused by forecasts based on exogenous in-formation. She relies on the median forecast from the Survey of Professional Forecasters(SPF) available since 1969 or on a military spending news variable constructed from pressreleases and available since 19398. In other words, innovations computed by an econome-

SVAR model in a study by Biau and Girard (2005). Their results are compatible with ours althoughthey define government spending as the sum of public consumption and public investment and theirestimation sample ends up in 2003. They compute that a government spending shock has a positiveshort term effect on GDP, with an impact multiplier of 1.4, and a statistically non significant effect inthe medium term.

8The defense news variable is based on episodes where Business Week began to forecast large rises indefense spending: the Ramey-Shapiro variable identifies three major episodes (the Korean war, the Viet-nam war and the Carter-Reagan buildup); another richer variable contains, for 31 dates, the magnitudeof increase in spending for the next years.

6

trician who estimates a SVAR model à la Blanchard and Perotti are not innovations foreconomic agents because their information set is larger than the set of past and presentvalues of the variables included in the model. In this case, estimated parameters andimpulse-response functions (IRF) computed using them are inconsistent.

In order to address this issue, Ramey (2011b) embeds one of her news variable into astandard SVAR used for the analysis of fiscal policy. This news variable is ordered firstin the model, just before government spending, and a Cholesky identification scheme isused. In practice, this identification scheme amounts to regress reduced-form residualsfrom the government spending equation on residuals from the news equation in order toidentify unanticipated government spending shocks. When she compares responses to ausual government spending shock (Blanchard and Perotti 2002, Perotti 2007) and to anunanticipated government spending shock, Ramey (2011b) identifies two main differences.Private consumption increases and private investment decreases on impact in the firstcase but the opposite result holds in the second case. A recent controversy (Ramey 2011a,Perotti 2011) highlighted that these results were sensitive to the inclusion of particularobservations9 and that IRFs for private consumption and GDP in the two cases wereprobably not significantly different from each other (see Figure 1 in Ramey (2011a)).Using European data and relying on forecasts from the European Commission, Beetsmaand Giuliodori (2011) do not find significant evidence of an anticipation effect either.

Although the empirical relevance of anticipation effects remains controversial, con-trolling for these effects provides a good robustness check. A first way to deal withanticipation effects, advocated by Sims (2009) and by Forni and Gambetti (2010), isto include forward-looking variables, like short term interest rates, consumer prices andstock prices, in the model. In our paper, short term interest rates and prices (GDPdeflator) are actually included in the model. Following Ramey’s methodology, we havealso assembled a database of government investment forecasts made by the forecastingdepartment of the French statistical institute (INSEE)10. We use it in order to controlfor expectations not already absorbed by the VAR model. However, its impact on theestimation of the government investment multiplier is only marginal.

Our conclusion using a TV-SVAR model and following Blanchard and Perotti (2002)for the identification of government expenditure shocks is that the size of the expendituremultiplier in France did not evolve statistically significantly at any horizon since thebeginning of the 1980s. The impact multiplier is significant and not far from 1 whereasthe medium term multiplier is not significantly different from 0. The variance of shocks

9For example, Perotti (2011) shows that the results of Ramey (2011b) are reversed by dummyingout two quarters (1950Q4 and 1951Q1) following a wave of panic buying and corresponding to theintroduction of specific regulations by the Federal Reserve.

10The same could not be done for governement consumption of goods and services.

7

hitting the economy evolves a lot more than the model autoregressive parameters. Thesame kind of conclusion has also been reached by Primiceri (2005) with a TV-SVARfocusing on monetary policy in the United States11.

Even in alternative specifications where the Bayesian priors are pushed towards time-variation, the main evolution that we uncover is a (non significant) decrease of the mediumterm expenditure multiplier, partly linked to a more aggressive monetary policy since the1990s. We do not find evidence of an increase of the multiplier during every recessionin France, contrary to the finding of Auerbach and Gorodnichenko (2012) for the UnitedStates. At least, business cycle conditions do not seem to be the main driver of theevolution of the expenditure multiplier in the last 30 years in France. One possibleexplanation could be that the unemployment rate, generally considered as an indicatorof slack, remained high in France since the middle of the 1980s12. But if one thinks thatthe last 30 years of data only enable measuring the government spending multiplier in badtimes for France, the practical relevance of conclusions reached on U.S. data regardingthe evolution of the expenditure multiplier seems to be limited for the French economy.

11His main findings are the following: 1. Time-variation is mostly located in the variance of shockshitting the economy: shocks to inflation and unemployment but also discretionary monetary policyshocks; 2. Impulse response functions of inflation and unemployment to a monetary policy shock arehardly modified since the beginning of the 1970s; 3. Even if the systematic part of monetary policy (i.e.:the parameters of the Taylor rule) displays some time-variation, this evolution does not explain at allwhy inflation rose and fell in the United States in the 1970s and 1980s.

12France is not an isolated case: Owyang et al. (2013) who estimate expenditure multipliers in goodand bad times on U.S. and Canadian data consider that Canada was characterized by a very long periodof slack from 1975 to 2005. This is due to the steadily high Canadian unemployment rate - over 7% - onthis period.

8

2 Constant parameter OLS estimates

2.1 Benchmark specification

The model that we consider is a quarterly VAR with 5 variables and l lags13. This modelcan be written as:

yt =(I5 I5 ⊗ y′t−1 ... I5 ⊗ y′t−l

)· β + A−1idtfA

−1Σ · εt= Zt · β + A−1idtfA

−1Σ · εt

where εt ∼ NID(0, 1) are structural innovations and the (25l + 5)× 1 vector β containscoefficients of constants and lags.

The five variables of the VAR are government expenditures, government net receipts,GDP, GDP deflator and the 3-month interest rate, ordered in this way. The first 3variables are expressed in real terms, deflated by the GDP deflator14. Depending onthe case, the first 4 variables may be considered in log-levels or in log-differences. The3-month interest rate is always expressed in percentage points.

A is a lower triangular matrix and the Aidtf matrix implements the identificationscheme. We assume that government spending is fixed in nominal terms, so that thevolume of expenditures reacts negatively, with a unitary elasticity, to unexpected inflationwithin a quarter. We also assume that government spending does not react to any othershock within a quarter. Perotti (2002) makes similar assumptions. So, the first line ofthe Aidtf matrix is (1 0 0 1 0). No further assumption regarding the identification ofother shocks has to be made in order to identify contemporaneous and lagged effects ofgovernment spending shocks (see Appendix C).

Aidtf =

1 0 0 1 0

0 1 0 0 0

0 0 1 0 0

0 0 0 1 0

0 0 0 0 1

13In practice, AIC and BIC criteria indicate that the optimal number of lags is never higher than 2 forany of the constant parameter specifications considered in the following. Hence, we will always choosel = 2.

14Using the GDP deflator to express these variables in real term allows us to compute the impulseresponses as shares of GDP. Blanchard and Perotti (2002), as well as Auerbach and Gorodnichenko(2012), made the same choice.

9

Here and in the remainder of this paper, the government spending multiplier Mt

following a shock equal to 115 at date 1 is defined, at date t, as a ratio between the cumu-lated increase in GDP from date 1 to date t and the cumulated increase in governmentspending from date 1 to date t :

Mt =

t∑i=1

Yi

t∑i=1

Gi

=

t∑i=1

i∑j=1

∆Yj

t∑i=1

i∑j=1

∆Gj

This definition is also used by Auerbach and Gorodnichenko (2012) but they only reportthe value of the multiplier at a 5-year horizon (i.e.: M20) in their paper.

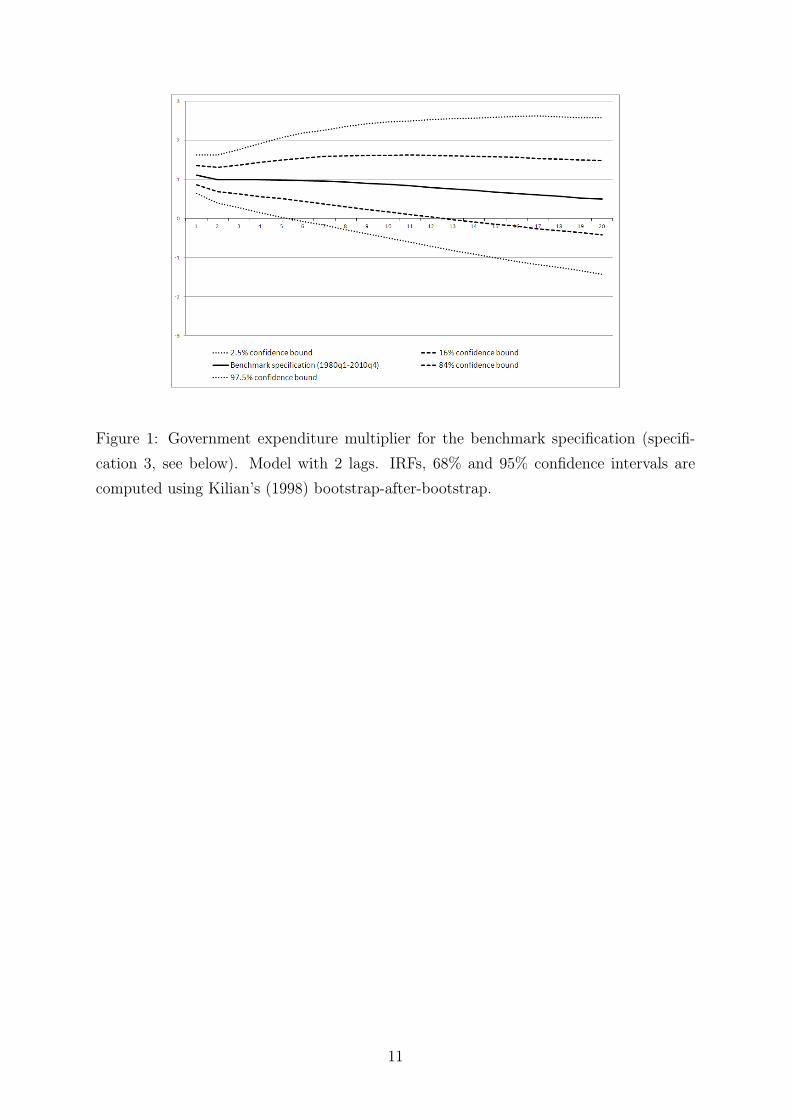

In the benchmark case, we estimate this 5-variable SVAR model with the followingspecification: we log-difference the first 4 variables and filter out low frequencies of allvariables (specification 3 below), we exclude the compensation of civil servants from gov-ernment expenditures, we assume that government expenditures shocks are unexpectedand VAR parameters are constant over the whole sample (1980Q1-2010Q4).

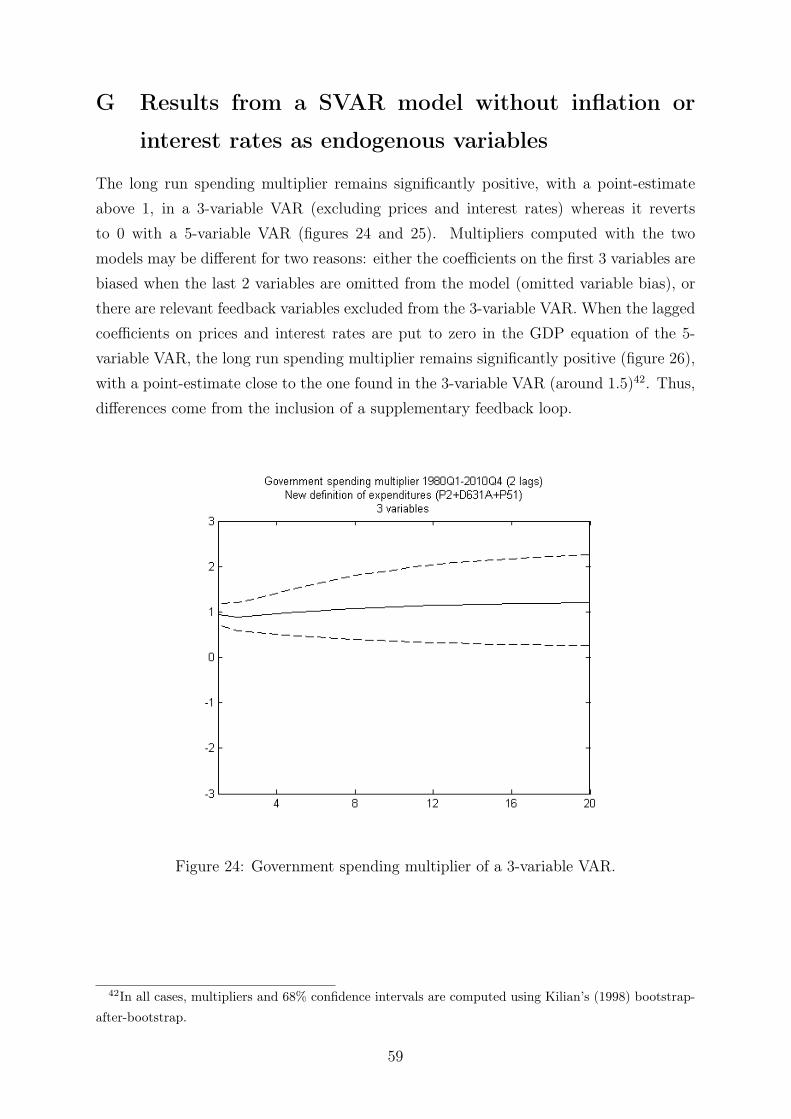

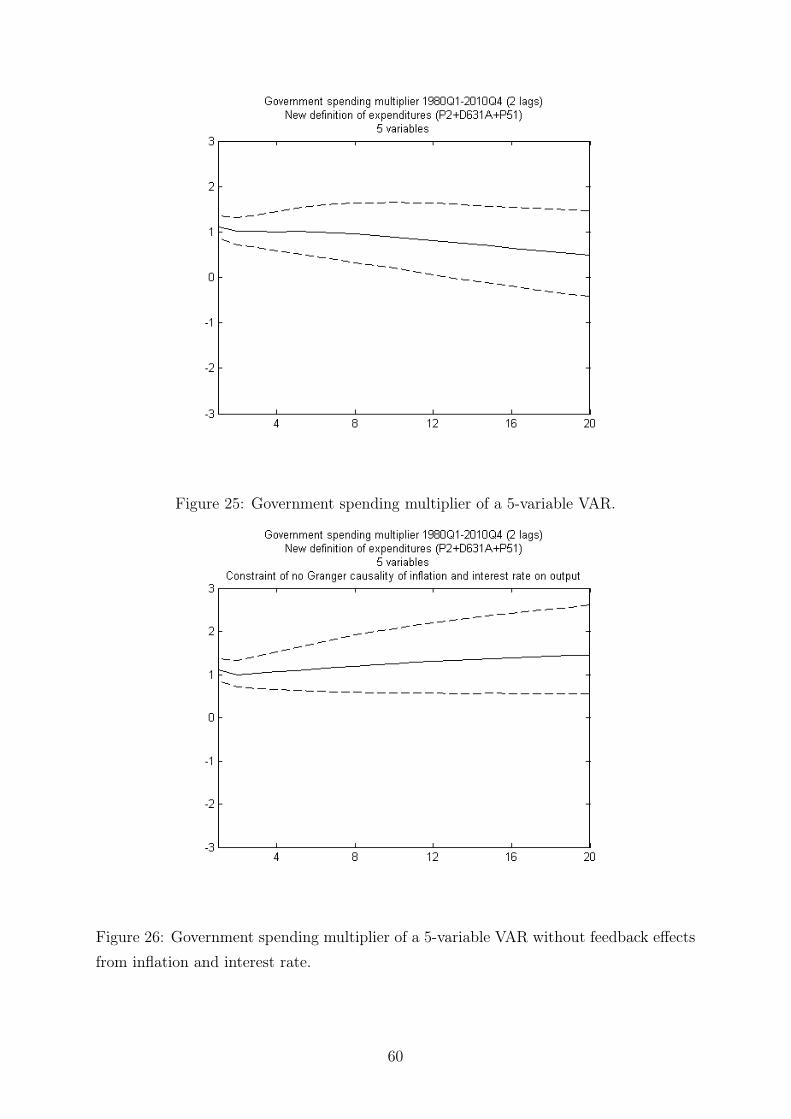

We will explain these assumptions and check their impact on our results in the fol-lowing sections. With this specification, the point-estimate of the government multiplieris equal to 1.1 on impact and to 0.5 after 20 quarters (figure 1). The impact multiplieris significantly positive, but it is not the case of the medium run one. Appendix Gshows that the medium run expenditure multiplier remains significantly positive (with apoint-estimate above 1) in a SVAR model without prices or interest rates as endogenousvariables, while it reverts to zero with our 5-variable VAR. This medium run behavior ofthe 3-variable SVAR model is due to the omission of a feedback loop. For various OECDcountries over the period 1980-2000, Perotti (2002) also finds that 3-variable models tendto deliver larger government spending multipliers than 5-variable ones in the mediumrun.

15The unit of measurement is the percentage point of GDP. We convert increases in G into percentagepoints of GDP using the average share of public expenditures in GDP over the sample (about 14%).

10

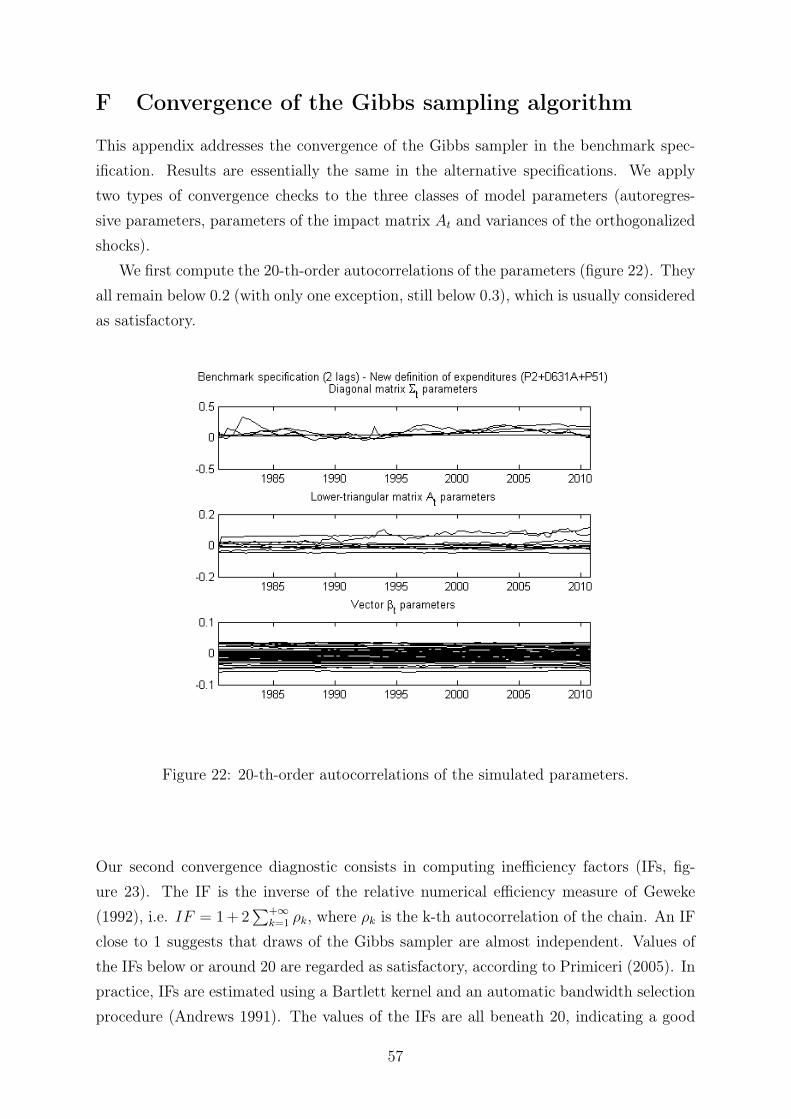

Figure 1: Government expenditure multiplier for the benchmark specification (specifi-cation 3, see below). Model with 2 lags. IRFs, 68% and 95% confidence intervals arecomputed using Kilian’s (1998) bootstrap-after-bootstrap.

11

2.2 Data handling: to difference or not, to detrend or not

2.2.1 Data persistence

Auerbach and Gorodnichenko (2012) estimate the equations of their model with (U.S.)data in log-levels, without differencing or filtering them although they are nonstationaryor, at least, very persistent16. They consider it as a simple way to preserve possiblecointegrating relationships among the variables. They acknowledge that an alternative,but more difficult, way of handling data would have been to estimate the equations inlog differences and to include error correction terms. In fact, there is a long tradition ofestimating SVAR models, especially those measuring the effects of monetary policy, withall data in log-levels17.

Another reason could justify the practice of estimating VAR models in log-levels. Eventhough there is a spurious regression problem when one regresses a nonstationary variableon another independent nonstationary variable, leading to a regression coefficient thatconverges to a stochastic variable rather than to 0, the same problem does not necessarilyoccur in VAR models. Sims et al. (1990) show that some linear combinations of the VARcoefficients have the usual asymptotic distribution: standard theory applies if coefficientsof interest can be rewritten as coefficients on stationary, mean zero, variables. A practicalconsequence of this result, when the vector of autoregressive coefficients in equation i atlag l is noted φil, is that

√T(

Φ̂il − Φil

)is asymptotically Gaussian for each p as long as

the number of lags in the model is sufficient. The asymptotic distribution of the VARcoefficients does not have any bias in this case.

However, small sample results, with sample sizes usually available in macroeconomics,may be noticeably different from what these asymptotic results suggest. For instance, theestimation of autoregressive coefficients in (V)AR models when data are very persistentis affected by finite sample bias. Kilian (1998) proposes a way to deal with this issuefor the computation of IRFs. In the following, whenever we do not rely on Bayesian

16The variables considered by Auerbach and Gorodnichenko (2012) are real government purchases(consumption + investment), real government net receipts and real GDP.

17Here we name just a few prominent examples in this field. Sims (1992) estimates a 6-variable VARmodel for different countries including a short term interest rate, a monetary aggregate, a consumer priceindex, an industrial production index, an index of the foreign exchange value of domestic currency and acommodity price index. All variables but the interest rate enter the model as log-levels while this variableis entered as a percent. Bernanke and Gertler (1995) estimate a 4-variable VAR model including the logof real GDP, the log of the GDP deflator, the log of an index of commodity prices and the federal fundsrate in percentage points. Finally, Eichenbaum and Evans (1995) estimate a 5-variable VAR model thatincludes the U.S. industrial production index, the U.S. consumer price index, the ratio of non-borrowedto total reserves, a measure of the difference between U.S. and foreign short term interest rates and thereal exchange rate. All variables are in log-levels except the interest rates.

12

estimation techniques, we always adopt his bootstrap-after-bootstrap method to computeIRFs and the corresponding confidence intervals. Concerning IRFs, Kilian and Chang(2000) show that confidence bands may have poor coverage properties in small samplesin the presence of very persistent variables, even if standard methods of inference arejustified asymptotically. In the following, we follow their recommendation to discountinterval estimates for higher horizons and report IRFs at a horizon of only 20 quarters (theminimum required to compare our results with those of Auerbach and Gorodnichenko2012).

2.2.2 Low-frequency evolutions: the case of the 1980s in France

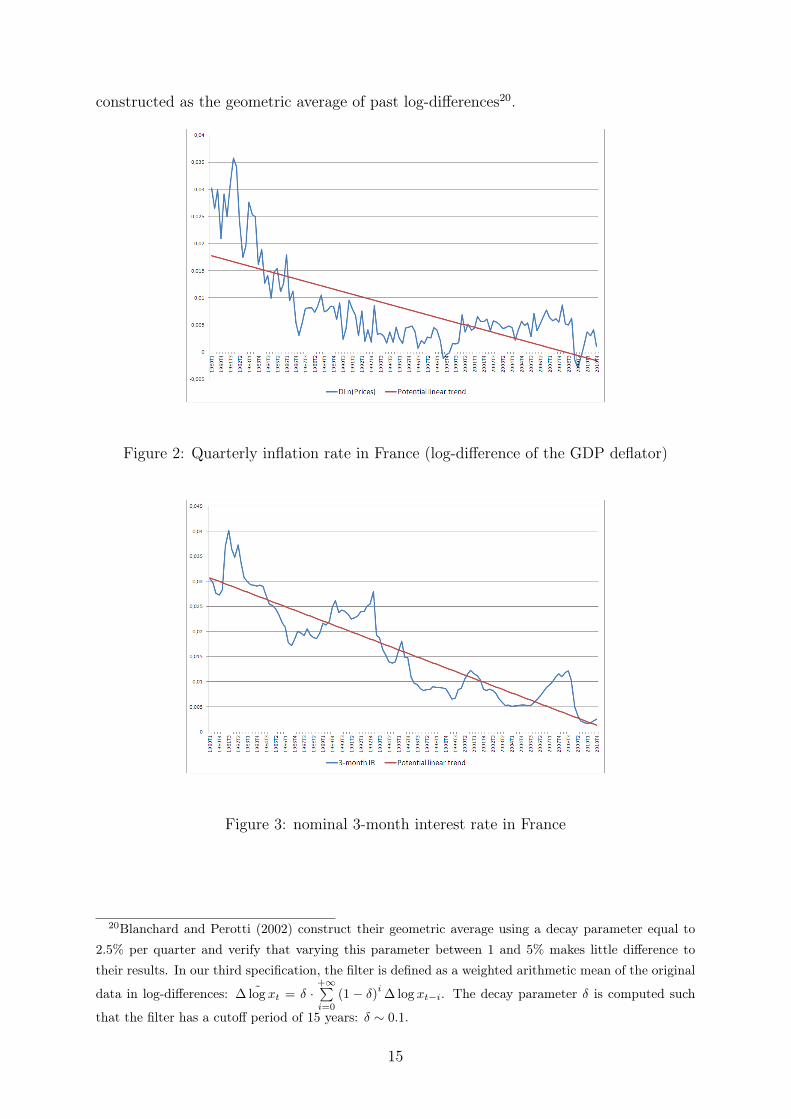

French data on the last 30 years are characterized by low-frequency evolutions that aredifficult to explain using only the 5 endogenous variables of the model. For instance,the inflation rate (log-difference of the GDP deflator) continuously decreased during the1980s (see figure 2). The second oil shock in 1979 and the counter-oil shock in 1985,but also decisions taken by the French government to achieve disinflation are exogenousevents, beyond the short term interest rate movements that we have in the model, thatmay explain why the inflation rate rose and fell in the 1980s.

Ignoring these exogenous events would most certainly bias the coefficients of our 5-variable model. Hence, three different data specifications will be considered in order todeal with these low-frequency evolutions:

• Specification 1: Our first data set consists in real government expenditures, realgovernment net receipts, real GDP, prices (GDP deflator) and the 3-month interestrate. All series are specified in log-level, except the 3-month interest rate whichis specified in level (% points). In order to take into account that prices (GDPdeflator) have an important low-frequency component (the inflation rate is steadilydecreasing, see figure 2 and appendix A), we allow for linear and quadratic trendsin each of the equations of the VAR. This specification is intended to be closestto the specifications in Auerbach and Gorodnichenko (2012) and Kirchner et al.(2010) and to the specification of usual monetary policy VARs.

• Specification 2: In order to apply a standard multivariate cointegration analysis onI(1) variables, we consider the previous data set with a single modification: pricesare replaced by price inflation. Hence, the cointegration analysis is done with thefirst three series (real government expenditures, real government net receipts andreal GDP) remaining specified in log-level, price inflation being defined as the log-difference of the GDP deflator and the 3-month interest rate remaining specifiedin level. In this way, all variables may be considered as I(1), even around a linear

13

deterministic trend (ADF or ERS tests).

In order to be consistent with our first specification, we allow for a linear determinis-tic trend in the cointegration space18. Both the trace and the maximum-eigenvaluecointegration test conclude to the existence of a single cointegration relation in thiscase19. Moreover, an LR test with a 5% level does not reject the joint hypothe-sis that real government expenditures, real government net receipts and real GDPmay be excluded from the cointegration relation and that this cointegration relationmay, itself, be excluded from the inflation equation. Hence, only price inflation, the3-month interest rate and the linear trend are linked together in the long run.

This multivariate cointegration analysis justifies a second data set with real gov-ernment expenditures, real government net receipts, real GDP and prices (GDPdeflator) specified in log-difference and the 3-month interest rate remaining in level.In this case, we allow for a linear trend in each of the equations of the VAR. Thisspecification allows taking into account the long run relation between inflation andthe 3-month interest rate. The fact that we are taking the log-difference of thefirst three variables (real government expenditures, real government net receiptsand real GDP) does not imply any loss of information since these variables may beexcluded from the cointegration relation.

• Specification 3: The third data set is identical to the second, but instead of allowingfor a linear trend in each of the equations of the VAR (which is equivalent topreviously regressing them on a linear trend), we pre-filter all data in subtractingto them a changing mean, constructed as the geometric average of their past.

Data specifications 1 and 3 are very close to those chosen by Blanchard and Per-otti (2002) who are also confronted to low-frequency movements on U.S. data (see pp.1339-1340 of their article). It leads them to present their results with two differentspecifications. In their first specification, all data (real government expenditures, realgovernment net receipts and real GDP) are specified in log-levels and they allow forlinear and quadratic trends in each of the equations of the VAR. In their second specifi-cation, all data are specified in log-differences from which they subtract a changing mean,

18This is case 4 decribed by Juselius (2006), p.100 of her book.19We rely on cointegration tests at a 10% level. This is consistent with Juselius (2006), p.145 of her

book: "[...] In small samples we often lack information to make a sharp distinction between unit roots,near unit roots and very stationary roots. In such cases, choosing the rank based on a small p-valuelike 0.05 is likely to exclusively pick up cointegration relations with relatively fast adjustment back toequilibrium. Unfortunately, the probability of excluding stationary relations characterized by slow, butnevertheless significant adjustments, is likely to be high, i.e. the probability of type 2 errors is generallyhigh for such relations. [...]"

14

constructed as the geometric average of past log-differences20.

Figure 2: Quarterly inflation rate in France (log-difference of the GDP deflator)

Figure 3: nominal 3-month interest rate in France

20Blanchard and Perotti (2002) construct their geometric average using a decay parameter equal to2.5% per quarter and verify that varying this parameter between 1 and 5% makes little difference totheir results. In our third specification, the filter is defined as a weighted arithmetic mean of the original

data in log-differences: ˜∆ log xt = δ ·+∞∑i=0

(1− δ)i ∆ log xt−i. The decay parameter δ is computed such

that the filter has a cutoff period of 15 years: δ ∼ 0.1.

15

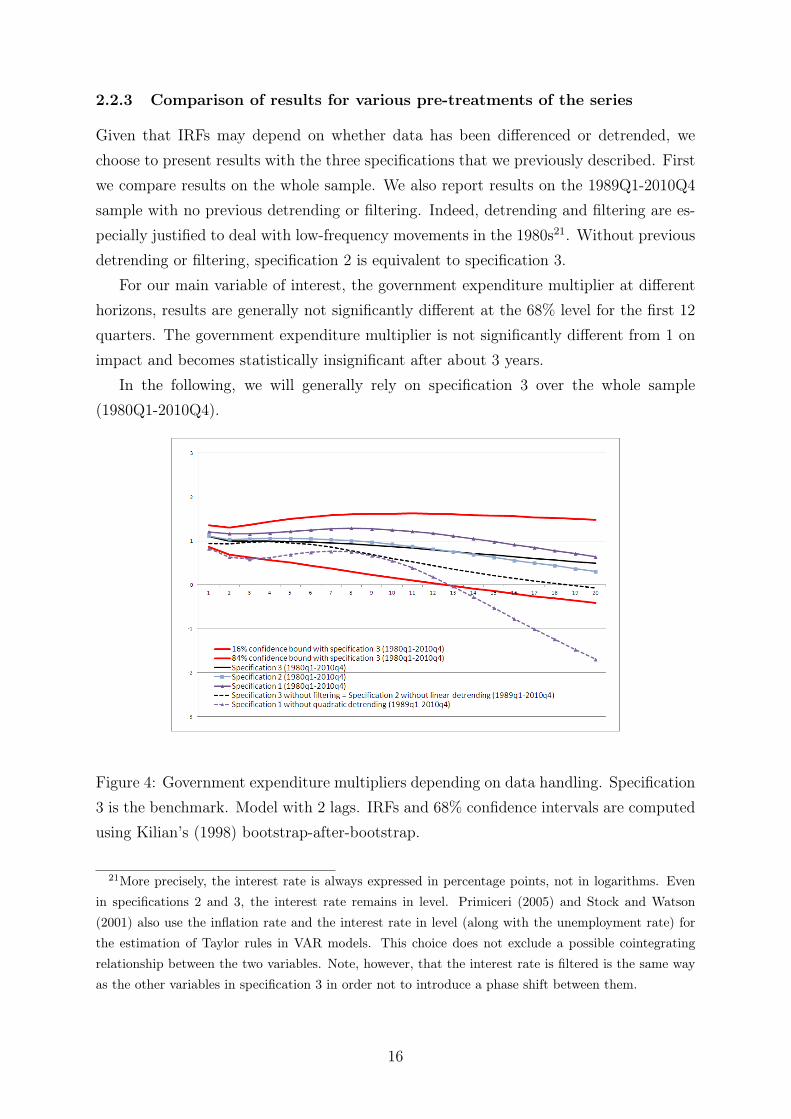

2.2.3 Comparison of results for various pre-treatments of the series

Given that IRFs may depend on whether data has been differenced or detrended, wechoose to present results with the three specifications that we previously described. Firstwe compare results on the whole sample. We also report results on the 1989Q1-2010Q4sample with no previous detrending or filtering. Indeed, detrending and filtering are es-pecially justified to deal with low-frequency movements in the 1980s21. Without previousdetrending or filtering, specification 2 is equivalent to specification 3.

For our main variable of interest, the government expenditure multiplier at differenthorizons, results are generally not significantly different at the 68% level for the first 12quarters. The government expenditure multiplier is not significantly different from 1 onimpact and becomes statistically insignificant after about 3 years.

In the following, we will generally rely on specification 3 over the whole sample(1980Q1-2010Q4).

Figure 4: Government expenditure multipliers depending on data handling. Specification3 is the benchmark. Model with 2 lags. IRFs and 68% confidence intervals are computedusing Kilian’s (1998) bootstrap-after-bootstrap.

21More precisely, the interest rate is always expressed in percentage points, not in logarithms. Evenin specifications 2 and 3, the interest rate remains in level. Primiceri (2005) and Stock and Watson(2001) also use the inflation rate and the interest rate in level (along with the unemployment rate) forthe estimation of Taylor rules in VAR models. This choice does not exclude a possible cointegratingrelationship between the two variables. Note, however, that the interest rate is filtered is the same wayas the other variables in specification 3 in order not to introduce a phase shift between them.

16

2.3 Different definitions of government expenditures

2.3.1 Government expenditures in goods and services, excluding the com-

pensation of civil servants

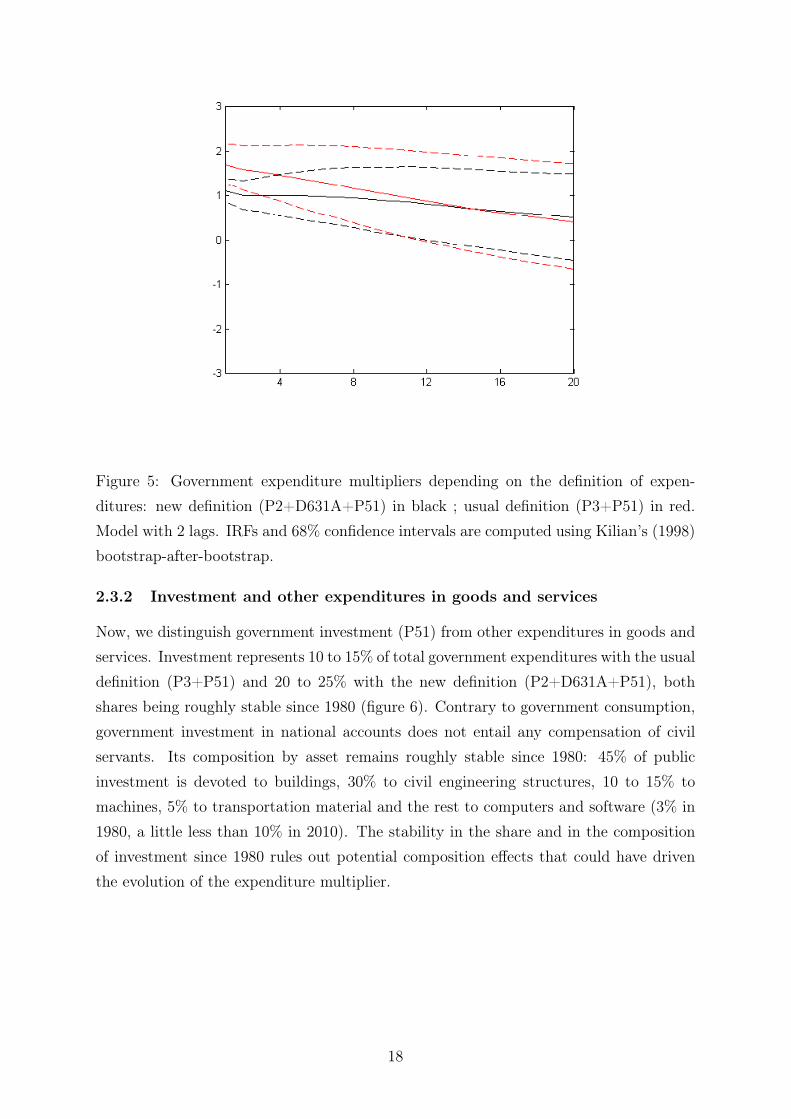

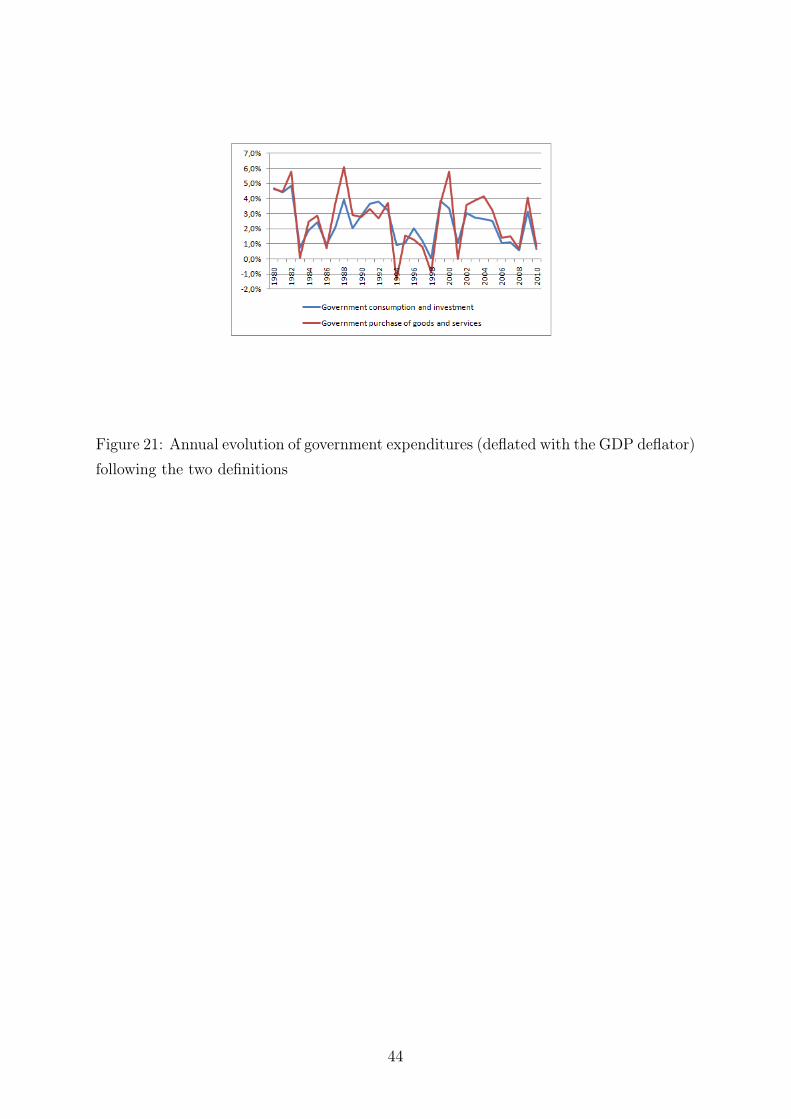

In order to compare our results with the previous literature, we first check what our mea-sure of government expenditures (excluding the compensation of civil servants) changesin comparison with the usual definition (sum of government consumption - P3 - andinvestment - P51 - in national accounts).

On the whole sample (1980Q1-2010Q4), the impact multiplier (i.e.: M1) is higher withthe usual definition of government expenditures (figure 5). The point estimate impactmultiplier equals 1.6 with the usual definition whereas it equals 1.1 with our measure ofexpenditures. This difference is not far from being statistically significant at the 68%level. For the United States, the non-defense spending multiplier found by Auerbach andGorodnichenko (2012) is 1.6 when they do not distinguish, like here, between expansionsand recessions22.

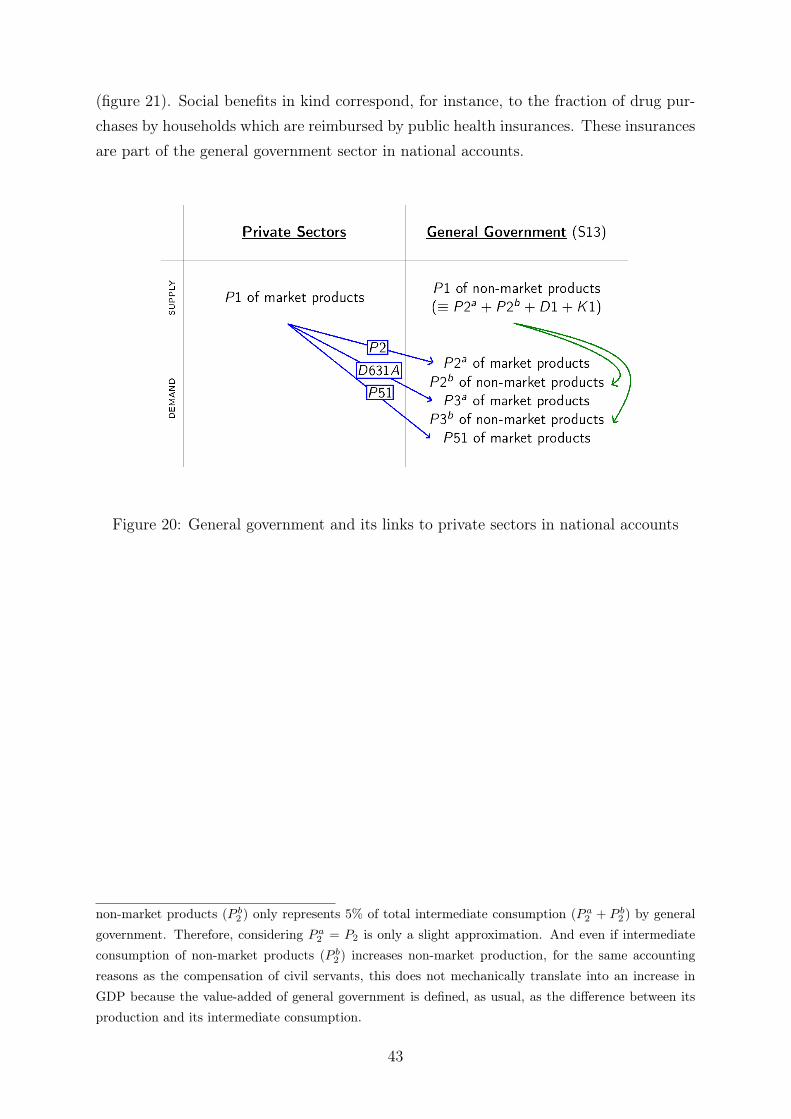

This difference between multipliers using different definitions of government expendi-tures can be linked to accounting conventions and to the fact that all expenditures arenot of the same kind. Indeed, following the 1993 System of National Accounts (1993SNA), non-market output by general government is estimated as the sum of intermediateconsumption, compensation of civil servants and consumption of fixed capital in the cor-responding sectors. This means that an exogenous increase in the compensation of civilservants mechanically leads to an increase in the value-added of non-market sectors, forstrictly accounting reasons (see Appendix B for details). Of course, one may also observea further increase in the value-added of market sectors due, for example, to an increase inthe private consumption of civil servants. We want to exclude the first (strictly account-ing) channel from our measure of the government expenditure multiplier. Moreover, thisallows us to consider more homogenous expenditures.

22They never exclude the compensation of civil servants from their definition of government spending.

17

Figure 5: Government expenditure multipliers depending on the definition of expen-ditures: new definition (P2+D631A+P51) in black ; usual definition (P3+P51) in red.Model with 2 lags. IRFs and 68% confidence intervals are computed using Kilian’s (1998)bootstrap-after-bootstrap.

2.3.2 Investment and other expenditures in goods and services

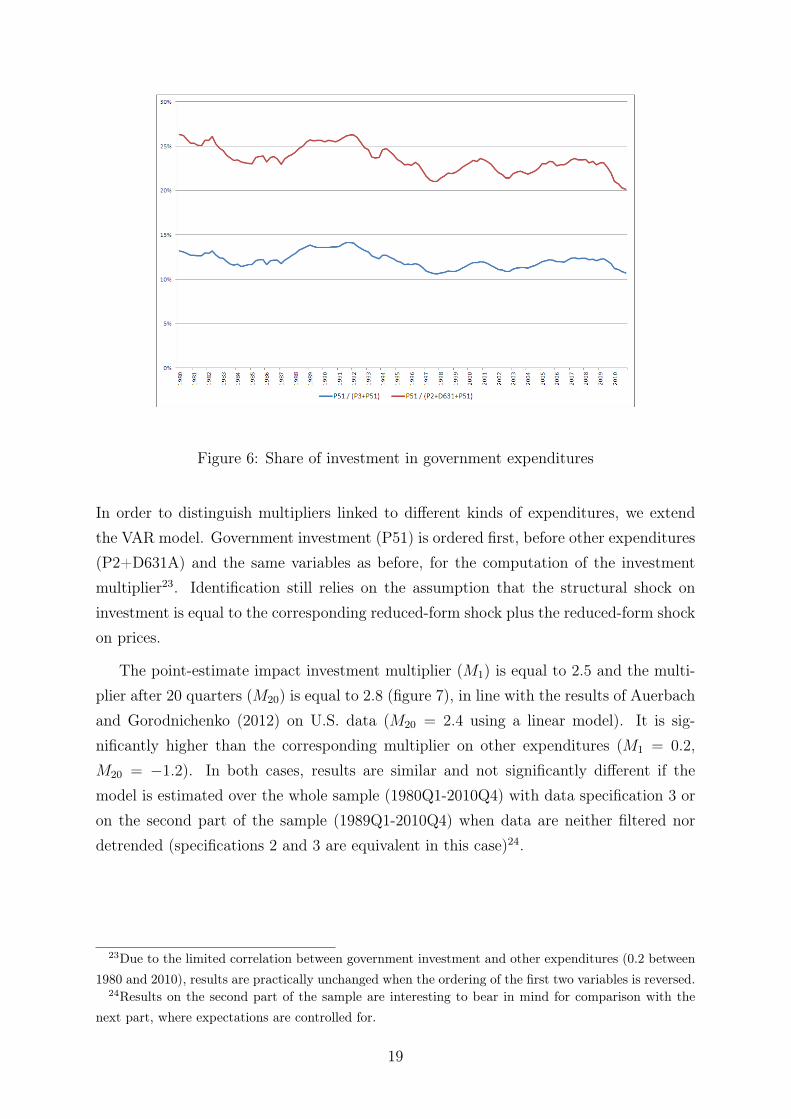

Now, we distinguish government investment (P51) from other expenditures in goods andservices. Investment represents 10 to 15% of total government expenditures with the usualdefinition (P3+P51) and 20 to 25% with the new definition (P2+D631A+P51), bothshares being roughly stable since 1980 (figure 6). Contrary to government consumption,government investment in national accounts does not entail any compensation of civilservants. Its composition by asset remains roughly stable since 1980: 45% of publicinvestment is devoted to buildings, 30% to civil engineering structures, 10 to 15% tomachines, 5% to transportation material and the rest to computers and software (3% in1980, a little less than 10% in 2010). The stability in the share and in the compositionof investment since 1980 rules out potential composition effects that could have driventhe evolution of the expenditure multiplier.

18

Figure 6: Share of investment in government expenditures

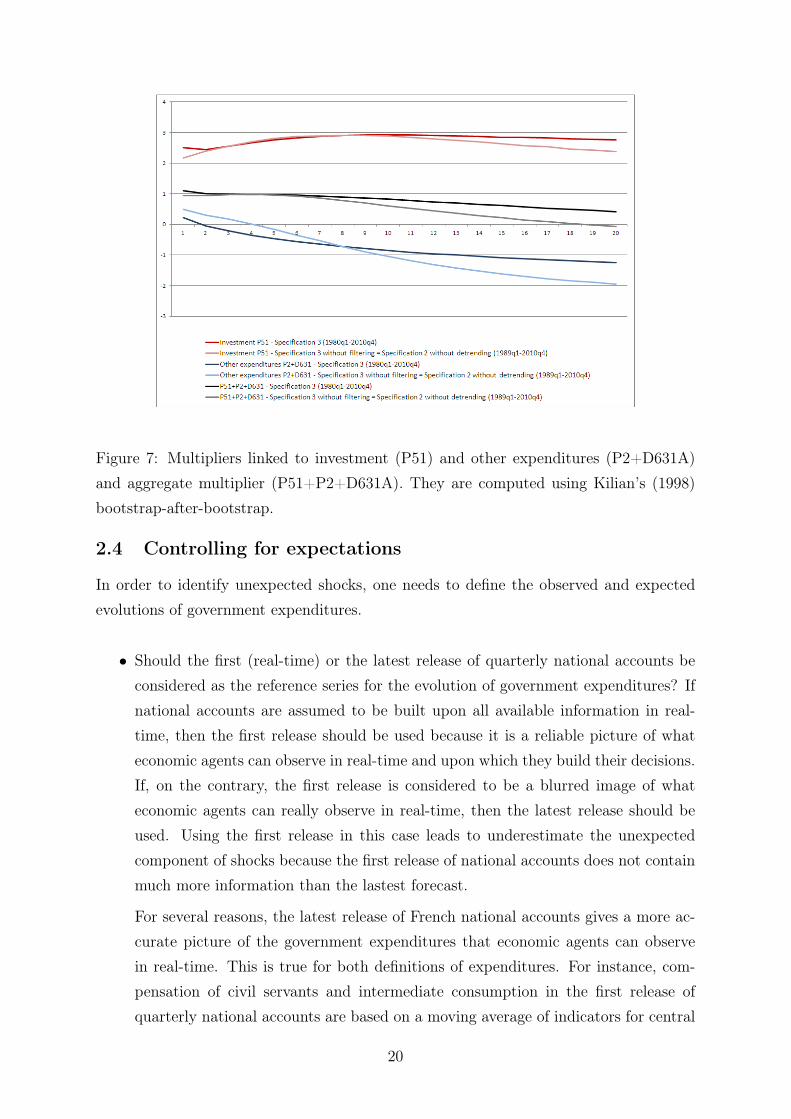

In order to distinguish multipliers linked to different kinds of expenditures, we extendthe VAR model. Government investment (P51) is ordered first, before other expenditures(P2+D631A) and the same variables as before, for the computation of the investmentmultiplier23. Identification still relies on the assumption that the structural shock oninvestment is equal to the corresponding reduced-form shock plus the reduced-form shockon prices.

The point-estimate impact investment multiplier (M1) is equal to 2.5 and the multi-plier after 20 quarters (M20) is equal to 2.8 (figure 7), in line with the results of Auerbachand Gorodnichenko (2012) on U.S. data (M20 = 2.4 using a linear model). It is sig-nificantly higher than the corresponding multiplier on other expenditures (M1 = 0.2,M20 = −1.2). In both cases, results are similar and not significantly different if themodel is estimated over the whole sample (1980Q1-2010Q4) with data specification 3 oron the second part of the sample (1989Q1-2010Q4) when data are neither filtered nordetrended (specifications 2 and 3 are equivalent in this case)24.

23Due to the limited correlation between government investment and other expenditures (0.2 between1980 and 2010), results are practically unchanged when the ordering of the first two variables is reversed.

24Results on the second part of the sample are interesting to bear in mind for comparison with thenext part, where expectations are controlled for.

19

Figure 7: Multipliers linked to investment (P51) and other expenditures (P2+D631A)and aggregate multiplier (P51+P2+D631A). They are computed using Kilian’s (1998)bootstrap-after-bootstrap.

2.4 Controlling for expectations

In order to identify unexpected shocks, one needs to define the observed and expectedevolutions of government expenditures.

• Should the first (real-time) or the latest release of quarterly national accounts beconsidered as the reference series for the evolution of government expenditures? Ifnational accounts are assumed to be built upon all available information in real-time, then the first release should be used because it is a reliable picture of whateconomic agents can observe in real-time and upon which they build their decisions.If, on the contrary, the first release is considered to be a blurred image of whateconomic agents can really observe in real-time, then the latest release should beused. Using the first release in this case leads to underestimate the unexpectedcomponent of shocks because the first release of national accounts does not containmuch more information than the lastest forecast.

For several reasons, the latest release of French national accounts gives a more ac-curate picture of the government expenditures that economic agents can observein real-time. This is true for both definitions of expenditures. For instance, com-pensation of civil servants and intermediate consumption in the first release ofquarterly national accounts are based on a moving average of indicators for central

20

government only because there is no reliable information for local administrationsavailable to national accountants at the time of the first release. Moreover, the de-composition of investment between firms and general government is conventional inthis first release. This is why we define unexpected shocks as the difference betweenthe latest release of quarterly national accounts and real-time forecasts made bythe forecasting department of the statistical institute.

• Another difficulty in the identification of unexpected shocks arises when accountingconcepts have changed between the release of the forecast and the release of nationalaccounts. In this case, using the latest release would lead to overestimate theunexpected component. The definition of government investment has remainedpractically unchanged since the 1980s25 but this is not the case for governmentconsumption26. Moreover, we do not have forecasts of government intermediateconsumption (P2) or social benefits in kind (D631A). Therefore, we only try tocontrol for expected government investment (P51) shocks.

• The latest forecast made by the forecasting department of the French statisticalinstitute (INSEE) before the first release of national accounts is used as an approx-imation of the expected evolution of government investment in France. The firstavailable forecast in our database is the forecast for 1989Q1.

• The correlation between forecasted investment growth and investment growth inthe latest release of national accounts lies between 0.2 and 0.3 and remains roughlystable on the available sample.

Following Ramey (2011a) and Auerbach and Gorodnichenko (2012), we expand theVAR model in order to control for expectations. The first three variables are nowgovernment investment forecasts, government investment itself and other expenditures(P2+D631A). The following four variables remain unchanged. The structural shock oninvestment is now a shock to the second variable. By construction, it is orthogonal togovernment investment forecasts27. Using this methodology, there is no evidence of an

25The only notable exception is the decision to treat software as an investment, rather than an in-termediate consumption, at the end of the 1990s. But at that time, this asset represented only 6% ofgovernment investment.

26Before the introduction of the 1993 SNA at the end of the 1990s, the definition of governmentconsumption was narrower. For instance, all the expenditures incurred on the market by the governmenton behalf of households were recorded as households’ consumption.

27We consider this methodology to be definitely superior to the one consisting in the inclusion govern-ment investment forecast errors as a first variable in the VAR instead of government investment forecasts.

21

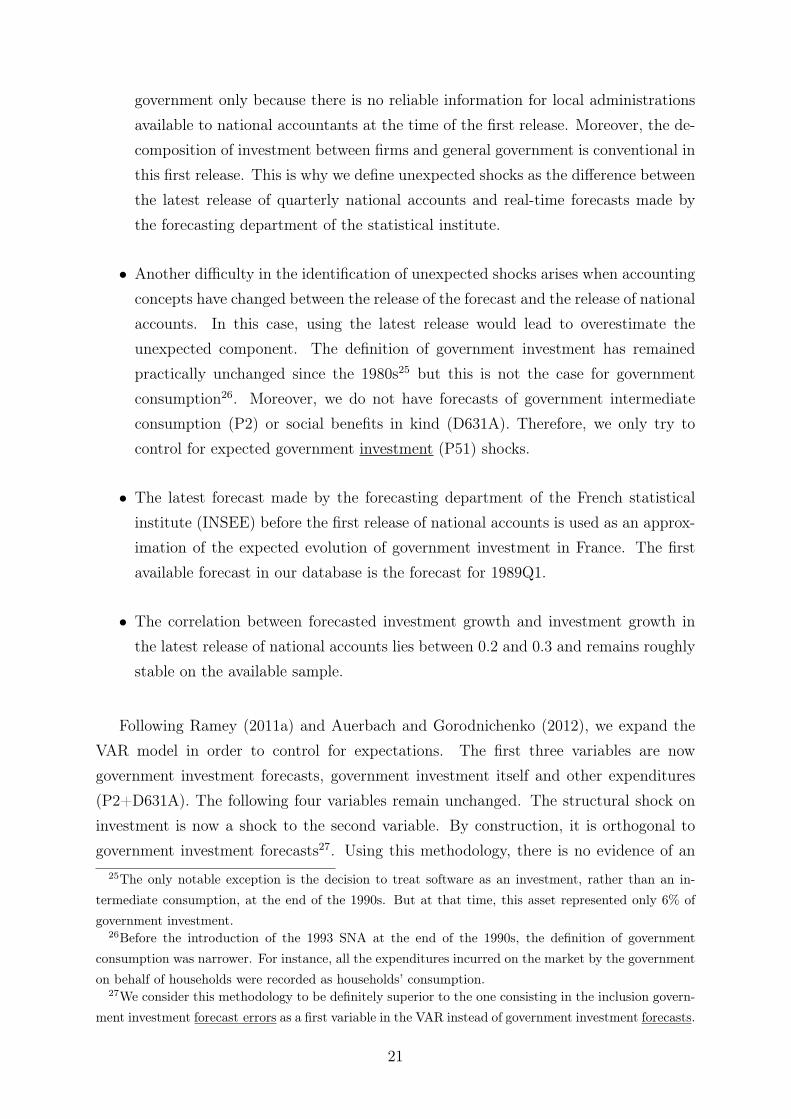

overlooked anticipation effect in the computation of the government investment multi-plier28 (figure 8).

Figure 8: Investment multipliers with or without control for expectations. Multipliers and68% confidence intervals are computed using Kilian’s (1998) bootstrap-after-bootstrap.

Indeed, if investment forecasts use all available information when they are made, investment forecasterrors can only be explained by news that arrived afterwards. Hence, investment and investment fore-cast errors are determined simultaneously and a regression of the former on the latter leads to a biasedcoefficient.

28This result for public investment is not necessarily surprising since half of this investment is devotedto buildings. The construction of buildings progresses at a regular pace and should be well forecastedusing lagged investment values, already included in the VAR model.

22

2.5 Different estimation samples

We now focus on results obtained with our measure of government expenditures on dif-ferent samples. Here are the main conclusions:

• The expenditure multiplier is slightly higher at each horizon in a sample includ-ing the Great Recession (1980Q1-2010Q4) than in a sample excluding it (1980Q1-2007Q2) but these differences are not statistically significant at the 68% level (fig-ure 9).

• Although it is not significant at the 68% level, the most important difference ontwo equal subsamples (1980-1995, 1995-2010) concerns the medium-run multiplier(horizon of 20 quarters, figure 10). It is larger when estimated over the first 15years (1980-1995). Nevertheless, the impact multipliers on the two subsamples arevery close to each other and not far from 1.

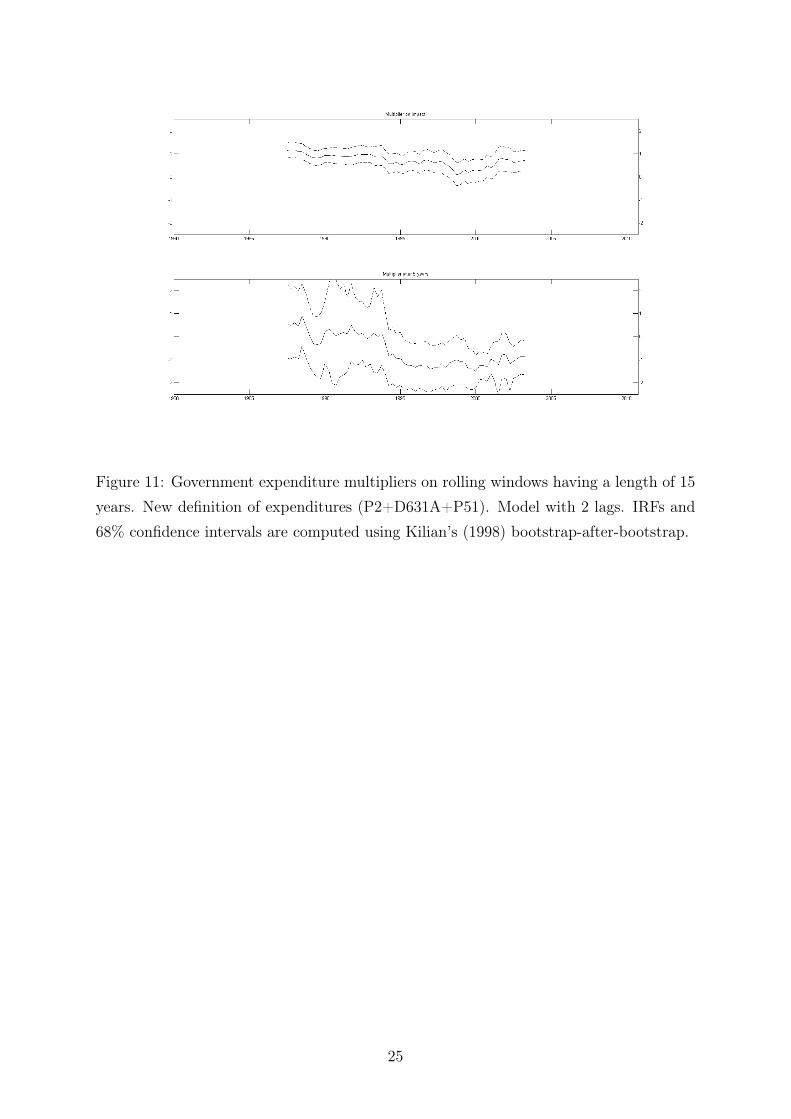

• We also estimate the SVAR model with constant parameter OLS on rolling windowswith a length of 15 years (figure 11). Beyond the decrease in the medium-runmultiplier (which is only marginally significant around 2000), it also indicates aslight and marginally significant decrease in the impact multiplier around 2000.Datation refers to the center of the rolling windows and, therefore, is far fromprecise. In the following, we compare these results with those from a Time-VaryingSVAR model.

23

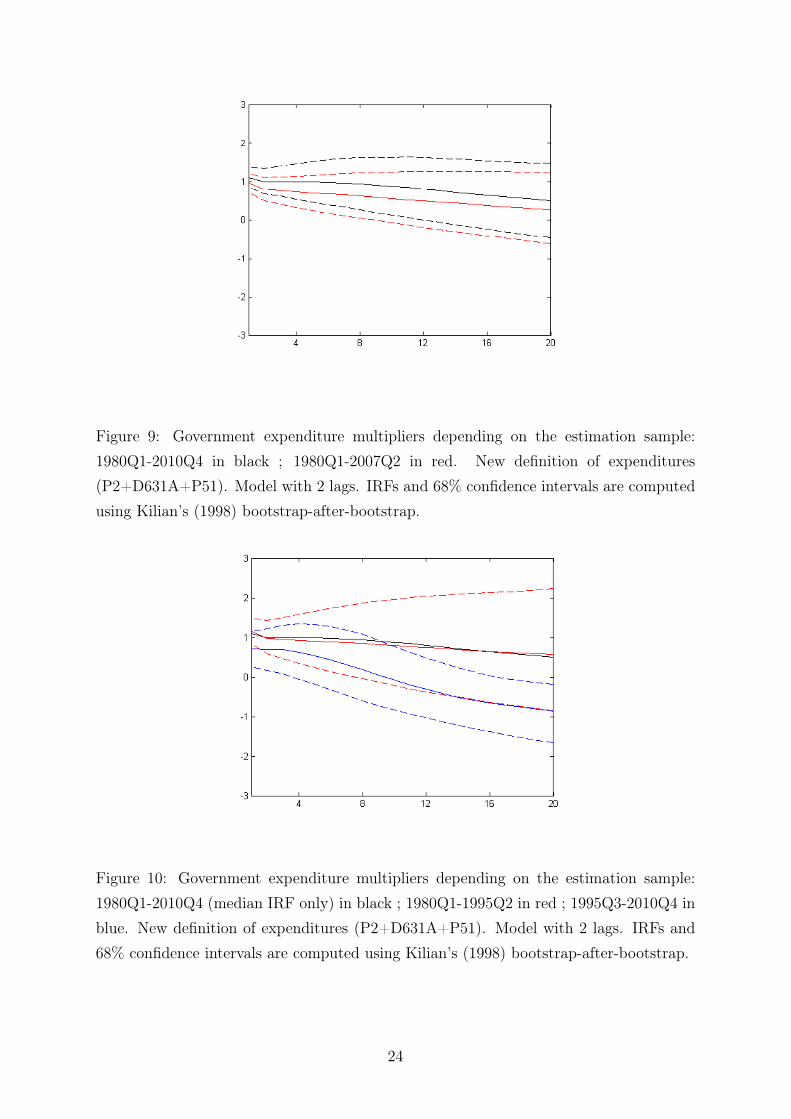

Figure 9: Government expenditure multipliers depending on the estimation sample:1980Q1-2010Q4 in black ; 1980Q1-2007Q2 in red. New definition of expenditures(P2+D631A+P51). Model with 2 lags. IRFs and 68% confidence intervals are computedusing Kilian’s (1998) bootstrap-after-bootstrap.

Figure 10: Government expenditure multipliers depending on the estimation sample:1980Q1-2010Q4 (median IRF only) in black ; 1980Q1-1995Q2 in red ; 1995Q3-2010Q4 inblue. New definition of expenditures (P2+D631A+P51). Model with 2 lags. IRFs and68% confidence intervals are computed using Kilian’s (1998) bootstrap-after-bootstrap.

24

Figure 11: Government expenditure multipliers on rolling windows having a length of 15years. New definition of expenditures (P2+D631A+P51). Model with 2 lags. IRFs and68% confidence intervals are computed using Kilian’s (1998) bootstrap-after-bootstrap.

25

3 Assessing the evolution of the expenditure multiplier

3.1 Econometric methodology

3.1.1 Description of the TV-SVAR model

The model that we consider is now a quarterly Time-Varying SVAR (TV-SVAR) with 5variables and l lags. The coefficients of the VAR and the variance covariance matrix ofthe error term are time-varying. This model can be written as:

yt =(I5 I5 ⊗ y′t−1 ... I5 ⊗ y′t−l

)· βt + A−1idtfA

−1t Σt · εt

= Zt · βt + A−1idtfA−1t Σt · εt

where εt ∼ NID(0, 1) are structural innovations and the (25l + 5)× 1 vector βt containscoefficients of constants and lags.

Matrices Aidtf , At and Σt have the following structure:

Aidtf =

1 0 0 1 0

0 1 0 0 0

0 0 1 0 0

0 0 0 1 0

0 0 0 0 1

, At =

1 0 0 0 0

α21,t 1 0 0 0

α31,t α32,t 1 0 0

α41,t α42,t α43,t 1 0

α51,t α52,t α53,t α54,t 1

,

Σt =

exp(h1,t2

)0 0 0 0

0 exp(h2,t2

)0 0 0

0 0 exp(h3,t2

)0 0

0 0 0 exp(h4,t2

)0

0 0 0 0 exp(h5,t2

)

The evolution of the time-varying parameters is described by the following state equa-

tions:

βt = βt−1 +K1t · υtαt = αt−1 +K2t · ζtht = ht−1 +K3t · ηt

The innovations εt, νt, ςt and ηt are assumed to be jointly normally distributed with the

26

following variance covariance matrix:

V = V ar

εt

υt

ζt

ηt

=

I5 0 . . . 0

0 Q. . . ...

... . . . S 0

0 · · · 0 W

These state equations are augmented with parameters Kit (i = 1, 2, 3) which can be

equal to 0 or 1. Depending on the value of Kit, state variables βt, αt and ht evolvebetween date t − 1 and date t or remain constant. When, for instance, K1t = 0, all thecomponents of the state vector βt remain unchanged between date t−1 and date t. Koopet al. (2009) introduced this specification into the TV-SVAR framework developed byPrimiceri (2005) in order to assess whether the monetary transmission mechanism in theUnited States changed and whether changes were gradual or abrupt.

3.1.2 Bayesian estimation strategy

Following Canova and Ciccarelli (2009), priors on α0, β0, h0, Q, S and W are specifiedusing OLS estimates on the 1980Q1-2007Q2 sample (i.e.: on a sample excluding theGreat Recession).

β0 ∼ N

(ˆ

βOLS, 4 ·ˆ

V

(ˆ

βOLS

))α0 ∼ N

(ˆαOLS, 4 ·

ˆ

V(

ˆαOLS

))h0 ∼ N

(2 · log

ˆσOLS, 4 ·

ˆ

V(

ˆσOLS

))

Q, S and W are diagonal matrices with diagonal elements qi, si and wi

qi ∼ IG

(k2q · νq ·

ˆ

Vi,i

(ˆ

βOLS

), νq

)si ∼ IG

(k2s · νs ·

ˆ

Vi,i

(ˆαOLS

), νs

)wi ∼ IG

(k2w · νw ·

ˆ

Vi,i

(ˆσOLS

), νw

)

ˆ

Vi,i

(ˆ

βOLS

),

ˆ

Vi,i

(ˆαOLS

)and

ˆ

Vi,i

(ˆσOLS

)correspond, respectively, to the diagonal

elements of matricesˆ

V

(ˆ

βOLS

),

ˆ

V(

ˆαOLS

)and

ˆ

V(

ˆσOLS

). The meaning of hyperpa-

rameters kq, ks, kw, νq, νs and νw will be clarified in the next section.

27

Finally, the Gibbs sampling algorithm is used to simulate the joint posterior distri-bution

p(β1..T , Q, α1..T , S, h1..T ,W,K1..T

1 , K1..T2 , K1..T

3 , s1..T |y1..T)

where x1..T corresponds to (x1, ..., xT ). The implementation of this algorithm is describedin Appendix D.

3.2 Results with the TV-SVAR model

3.2.1 Benchmark specification

We now estimate the TV-SVAR model presented above. In the definition of the Bayesianpriors, we have to set important hyperparameters governing time variation of the modelparameters.

• First, we have to set the hyperparameter p scaling the probability to observe ajump in the parameter values between date t − 1 and date t. In the benchmarkspecification, this hyperparameter is defined so that the mean probability to observea jump is 0.5 for the three classes of model parameters (autoregressive parameters,parameters of the impact matrix At and variances of the orthogonalized shocks).

• Second, we have to set the hyperparameters kq, ks and kw governing the variance ofparameter innovations. The econometric literature gives some guidance when thelaw of motion of parameters is a random walk with Gaussian innovations (i.e. whenthe probability of jump between two successive dates is equal to 1). Following Stockand Watson (1996), the choice of kq = 0.01 has become standard in the literature ontime-varying parameter regressions (Cogley and Sargent 2001, Cogley and Sargent2005, Primiceri 2005). It corresponds to a standard error of the innovations in therandom walk processes describing parameter evolutions equal to 1% of the standarderror of the OLS estimates. Here, taking into account that the probability p of jumpis not equal to 1 in our prior specification, we follow Koop et al. (2009) and we setthe benchmark values for kq, ks and kw at 0.01√

pwith p = 0.5.

• Third, hyperparameters νq, νs and νw corresponding to the tightness of the priorsscaling time variation are chosen so that these priors are proper and to avoid im-plausible behavior of the parameters. In practice, we set νs = νw = 1

2and νq = 5

2

in the benchmark specification29.29Remind that νq, νs and νw are homogenous to a number of points, to be compared with half the

size of the sample used for the estimation of the model, 1222 = 61 points here.

28

Recall that these choices direct but do not fully constrain time-variation a posteriori.Indeed, the weight given to priors in final (a posteriori) estimates declines with the sizeof the sample and asymptotically converges to 0.

With this benchmark specification, we find that posterior means for the transitionprobabilities are comprised between 0.35 and 0.75 (E(p1|y1...T ) = 0.5, E(p2|y1...T ) = 0.35

and E(p3|y1...T ) = 0.75). Thus, although our benchmark specification does not excluderare abrupt changes, our results are close to those of a TV-SVAR model à la Primiceri.Results indicate that time variation is mostly located in the variance of (reduced-form)shocks (figure 12) 30.

Two features are worth noticing:

• a gradual decrease of the variance of residuals in the price inflation equation sincethe beginning of the 1980s;

• a peak of volatility in 1992-1993 in the interest rate equation, corresponding to thecrisis of the European Monetary System (EMS)31. This means that the restrictivemonetary policy at that time is partly interpreted as an interest rate shock, withmore variance than usual, rather than only as a strengthening of the systematicmonetary response to business cycle conditions. It seems particularly useful in suchcases to estimate a model which is able to discriminate between heteroscedasticityand time-varying parameters.

However, there is only very limited variation over time of the impulse response func-tions (IRFs) to a government spending shock (see figure 13 showing government expen-diture multipliers on 20 quarters and at 4 different dates: 1980, 1990, 2000 and 2010).

30Notice that the algorithm advocated by DelNegro and Primiceri (2013) leads to smoother variancesthan the algorithm originally advocated by Primiceri (2005), see Appendix D.

31Since the beginning of the 1990s, France and the other members of the EMS had chosen to an-chor their currency to the Deutsche Mark. In practice, this meant that the French central bank wasconstrained to follow the German short term interest rate policy. Difficulties arose after the Germanreunification when the Bundesbank began to counteract the inflationary pressures following the choice ofa rate of exchange of 1:1 for conversion of East German money to Deutschmarks and the fiscal expansiondecided by the German government. Following the same monetary policy outside Germany with worsemacroeconomic conditions meant positive interest rate shocks. The size of these shocks rapidly increasedbecause other countries had to offer a growing spread relative to the German interest rate in order tomaintain a fixed parity with the Deutsche Mark. Some countries (UK, Italy, Spain) chose to leave theEMS at the end of 1992. France paid an interest rate spread of 200bp until the summer 1993 whenfluctuation bands inside the EMS were enlarged. The interest rate spread relative to Germany thendisappeared rapidly. For more details on the EMS crisis, see Muet (1994).

29

Figure 12: Posterior median of the standard deviation of shocks ; 16% and 84% confidencebounds. Benchmark specification.

Figure 13: Government spending multiplier for a shock initiated at different dates (1980,1990, 2000 and 2010). Benchmark specification.

3.2.2 Two alternative specifications where time variation is more favored by

the Bayesian priors

The hyperparameters governing time variation of the model parameters are now set toalternative values. We consider two alternative specifications:

30

• In the first specification, the probability p of observing a jump in parameter valuesbetween two successive dates is set at a prior mean value of 0.01 instead of 0.5.Consequently, the hyperparameters kQ, kS and kW are revised upwards (kQ = kS =

kW = 0.01√p). In this case, we set νs = νw = 1

2(unchanged) and νq = 20

2. This

specification is intended to be closer to the regime-switching VAR specificationadopted by Auerbach and Gorodnichenko (2012) but, contrary to them, we do notconstrain the regime switch to be influenced by business cycle conditions only. Welet the data decide for the timing and size of the jumps, only indicating that jumpsshould be rare and rather important a priori.

• In the second specification, the probability of observing a jump has a prior meanvalue of 0.5, as in the benchmark, but the hyperparameters kQ, kS and kW are setat a value of 0.1√

0.5instead of 0.01√

0.5in the benchmark specification. Consequently,

evolutions are assumed to be gradual but with a much higher amplitude than inthe benchmark. In this case, we set νs = νw = 1

2(unchanged) and νq = 50

2. This

prior specification is intended to really push the model towards time-variation butit can be considered as extreme given what is usually considered reasonable in theliterature (cf. Stock and Watson (1996)).

Examining the results of the first alternative specification shows that even when theBayesian priors are more in line with the Auerbach and Gorodnichenko (2012) specifica-tion, data information is strong enough to pull posterior transition probabilities upwardsfor the log-variances ht (E(p3|y1...T ) = 0.25, compared to a prior transition probabilityequal to 0.01). However, posterior transition probabilities for coefficients αt and βt re-main very close to the prior probabilities (E(p1|y1...T ) = 0.02, E(p2|y1...T ) = 0.01), whichmay indicate that data is less informative for these coefficients. All in all, IRFs, multi-pliers and evolutions of shock variances remain practically unchanged compared to thebenchmark specification (not shown).

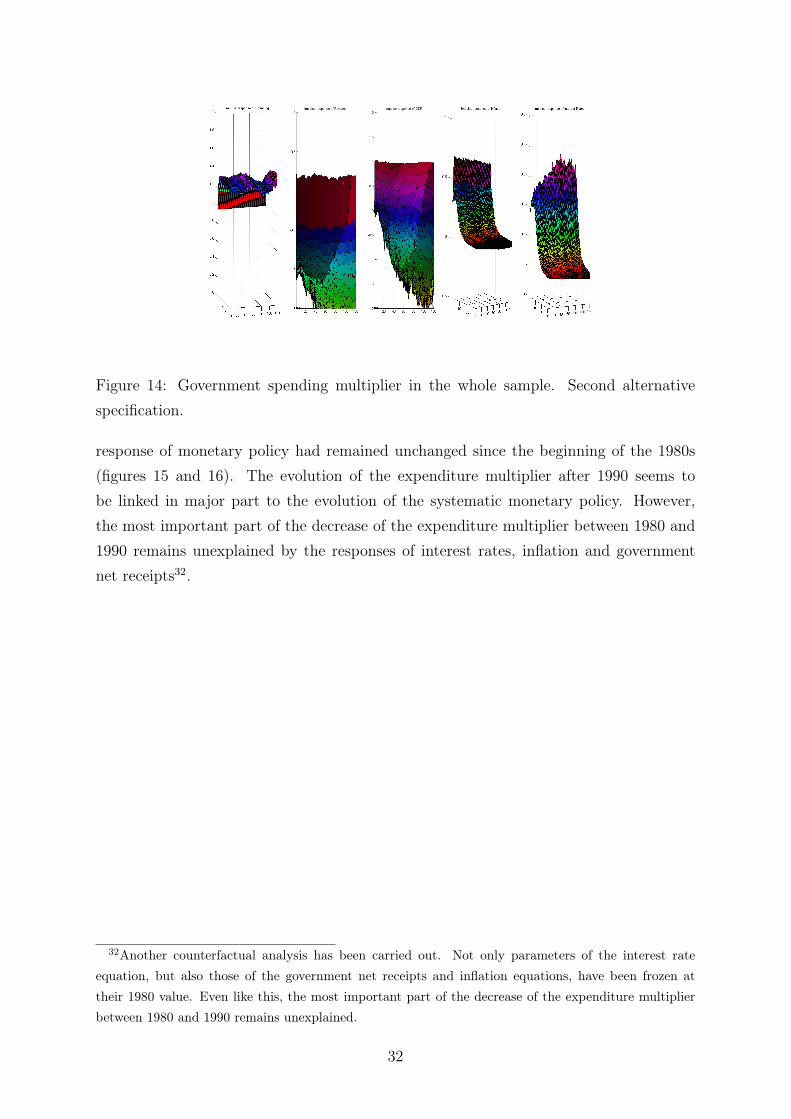

It is only with the second alternative specification that one may see an evolution inthe IRFs and in the expenditure multiplier. The most notable evolution is a decreasein the medium term multiplier between the beginning and the end of the sample. Thisis consistent with what we previously obtained relying on simple rolling windows OLSestimates. Another visible evolution in the IRFs concerns the systematic response ofmonetary policy: the upward adjustment of the short term interest rate following agovernment spending shock becomes more aggressive in the 1990s (figure 14). Thisevolution can probably be linked to the disinflation and exchange rate policy followed bythe French Central Bank at that time.

This visual inspection is confirmed if one compares the observed evolution of thegovernment expenditure multiplier with its counterfactual evolution if the systematic

31

Figure 14: Government spending multiplier in the whole sample. Second alternativespecification.

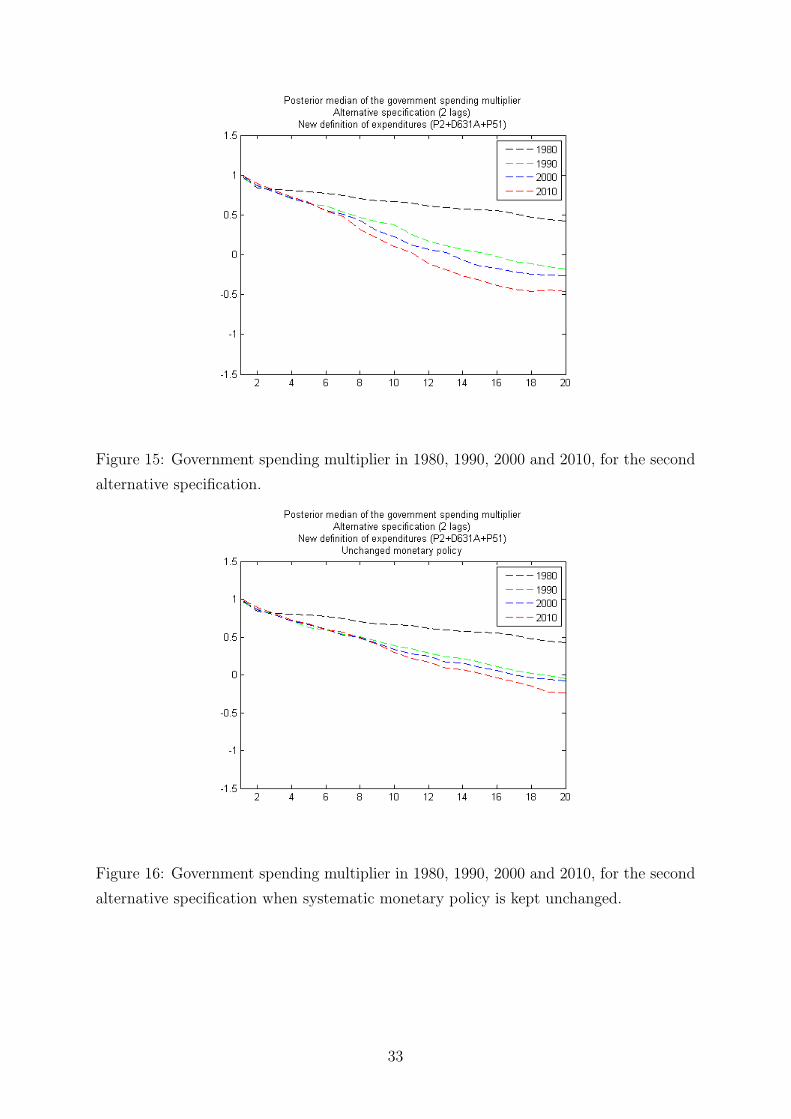

response of monetary policy had remained unchanged since the beginning of the 1980s(figures 15 and 16). The evolution of the expenditure multiplier after 1990 seems tobe linked in major part to the evolution of the systematic monetary policy. However,the most important part of the decrease of the expenditure multiplier between 1980 and1990 remains unexplained by the responses of interest rates, inflation and governmentnet receipts32.

32Another counterfactual analysis has been carried out. Not only parameters of the interest rateequation, but also those of the government net receipts and inflation equations, have been frozen attheir 1980 value. Even like this, the most important part of the decrease of the expenditure multiplierbetween 1980 and 1990 remains unexplained.

32

Figure 15: Government spending multiplier in 1980, 1990, 2000 and 2010, for the secondalternative specification.

Figure 16: Government spending multiplier in 1980, 1990, 2000 and 2010, for the secondalternative specification when systematic monetary policy is kept unchanged.

33

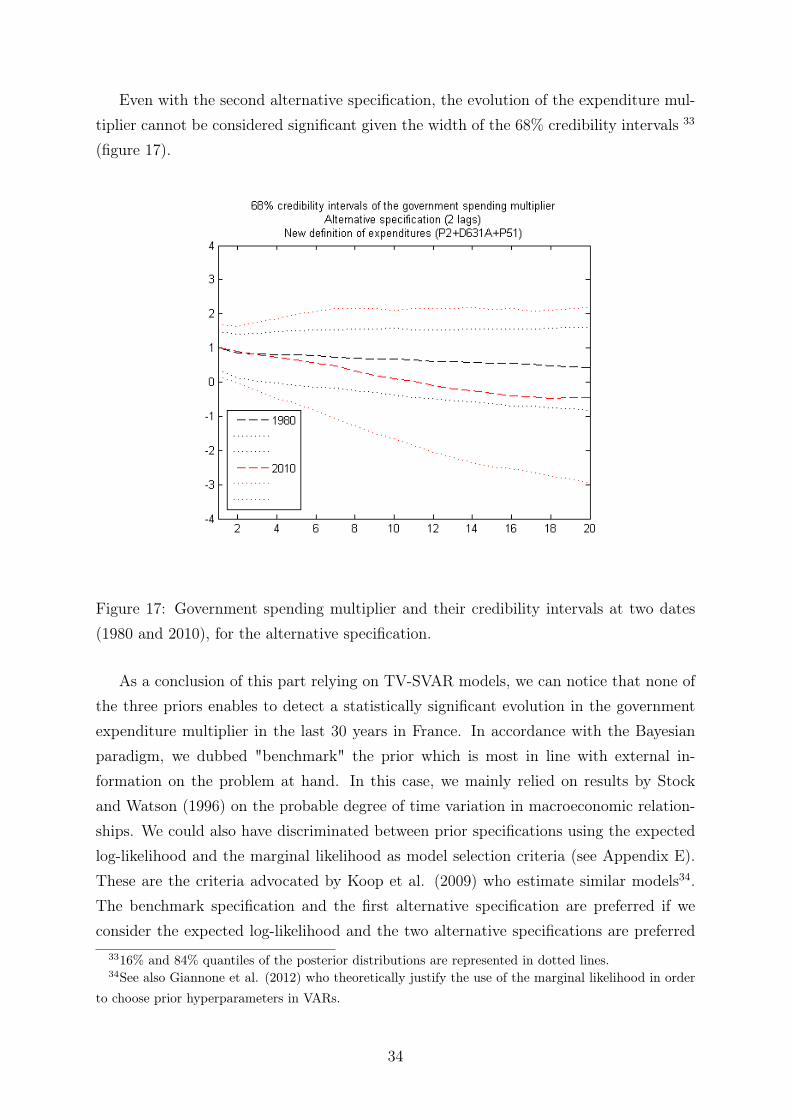

Even with the second alternative specification, the evolution of the expenditure mul-tiplier cannot be considered significant given the width of the 68% credibility intervals 33

(figure 17).

Figure 17: Government spending multiplier and their credibility intervals at two dates(1980 and 2010), for the alternative specification.

As a conclusion of this part relying on TV-SVAR models, we can notice that none ofthe three priors enables to detect a statistically significant evolution in the governmentexpenditure multiplier in the last 30 years in France. In accordance with the Bayesianparadigm, we dubbed "benchmark" the prior which is most in line with external in-formation on the problem at hand. In this case, we mainly relied on results by Stockand Watson (1996) on the probable degree of time variation in macroeconomic relation-ships. We could also have discriminated between prior specifications using the expectedlog-likelihood and the marginal likelihood as model selection criteria (see Appendix E).These are the criteria advocated by Koop et al. (2009) who estimate similar models34.The benchmark specification and the first alternative specification are preferred if weconsider the expected log-likelihood and the two alternative specifications are preferred

3316% and 84% quantiles of the posterior distributions are represented in dotted lines.34See also Giannone et al. (2012) who theoretically justify the use of the marginal likelihood in order

to choose prior hyperparameters in VARs.

34

if we consider the marginal likelihood. Nevertheless, this slight ambiguity resulting fromthe choice of model selection criteria does not affect the overall conclusion of the article.

4 Conclusion

Relying on OLS estimation of a SVAR model over the period 1980-2010, we find thatthe government expenditure multiplier is significant and not far from 1 on impact andbecomes statistically insignificant after about 3 years in France. This result is based ona careful exploitation of national accounts in order to use the most relevant definition ofgovernment expenditures (excluding the compensation of civil servants). We also carryout numerous robustness checks concerning assumptions about data stationarity, the roleof expectations and the choice of the sample.

We only rely on the Blanchard-Perotti identification scheme in order to identify struc-tural shocks on government expenditures on goods and services. Hence, we do not needto know the correct value of the elasticity of government net receipts relative to businesscycle conditions. We justify this partial identification scheme in appendix C.

Our second conclusion using a Time Varying-SVAR model is that the expendituremultiplier in France did not evolve significantly at any horizon since the beginning ofthe 1980s. The variance of shocks hitting the economy evolves a lot more than theautoregressive parameters of the model. Even in alternative specifications where theBayesian priors are pushed towards time-variation, the main evolution that we uncover isa (non significant) decrease of the medium term expenditure multiplier, partly linked to amore aggressive monetary policy since the 1990s. We do not find evidence of an increaseof the multiplier during every recession in France, contrary to the finding of Auerbachand Gorodnichenko (2012) for the United States. At least, business cycle conditions donot seem to be the main driver of the evolution of the expenditure multiplier in thelast 30 years in France. One possible explanation could be that the unemployment rate,generally considered as an indicator of slack, remained high in France since the middleof the 1980s. But if one thinks that the last 30 years of data only enable measuringthe government spending multiplier in bad times for France, the practical relevance ofconclusions reached on U.S. data regarding the evolution of the expenditure multiplierseems to be limited for the French economy.

35

References

Andrews, D. W. (1991). Heteroskedastic and Autocorrelation Consistent CovarianceMatrix Estimation. Econometrica 59, 817–858.

Auerbach, A. and Y. Gorodnichenko (2012). Measuring the Output Responses to FiscalPolicy. American Economic Journal: Economic Policy 4 (2), 1–27.

Barro, R. J. and C. J. Redlick (2009). Macroeconomic Effects from Government Pur-chases and Taxes. NBER Working Paper 15369.

Beetsma, R. and M. Giuliodori (2011). The Effects of Government Purchases Shocks:Review and Estimates for the EU. The Economic Journal 121, 4–32.

Bernanke, B. S. and M. Gertler (1995). Inside the Black Box: the Credit Channel ofMonetary Policy Transmission. Journal of Economic Perspectives 9 (4), 27–48.

Biau, O. and E. Girard (2005). Politique budgétaire et dynamique économique enFrance : l’approche VAR structurel. Economie et Prévision 169-171.

Blanchard, O. and R. Perotti (2002). An Empirical Characterization of the DynamicEffects of Changes in Government Spending and Taxes on Output. The QuarterlyJournal of Economics 117 (4), 1329–1368.

Bouthevillain, C. and G. Dufrénot (2011). Are the Effects of Fiscal Changes Different inTimes of Crisis and Non Crisis? The French Case. Revue d’économie politique 121,371–407.

Canova, F. and M. Ciccarelli (2009). Estimating Multicountry VAR Models. Interna-tional Economic Review 50 (3), 929–959.

Carlin, B. P. and T. A. Louis (2000). Bayes and Empirical Bayes Methods for DataAnalysis. Chapman and Hall .

Carter, C. K. and R. Kohn (1994). On Gibbs Sampling for State Space Models.Biometrika 81 (3), 541–553.

Christiano, L. J., M. Eichenbaum, and S. Rebelo (2011). When is the GovernmentSpending Multiplier Large? Journal of Political Economy 119 (1), 78–121.

Cogley, T. and T. J. Sargent (2001). Evolving Post-World War II U.S. Inflation Dy-namics. NBER Macroeconomics Annual 16, 331–373.

Cogley, T. and T. J. Sargent (2005). Drifts and Volatilities: Monetary Policies andOutcomes in the Post WWII U.S. Review of Economic Dynamics 8, 262–302.

Creel, J., E. Heyer, and M. Plane (2011). Petit précis de politique budgétaire par tousles temps. Les multiplicateurs budgétaires au cours du cycle. Revue de l’OFCE 116,

36

61–88.

DelNegro, M. and G. Primiceri (2013). Time-Varying Structural Vector Autoregres-sions and Monetary Policy: A Corrigendum. Federal Reserve Bank of New YorkStaff Reports No 619 .

Eichenbaum, M. and C. L. Evans (1995). Some Empirical Evidence on the Effectsof Shocks to Monetary Policy on Exchange Rates. Quarterly Journal of Eco-nomics 110 (4), 975–1009.

Forni, M. and L. Gambetti (2010). Fiscal Foresight and the Effects of GovernmentSpending. Mimeo.

Gelfand, A. E. and D. K. Dey (1994). Bayesian Model Choice: Asymptotics and ExactCalculations. Journal of the Royal Statistical Society - Series B 56 (3), 501–514.

Gerlach, R., C. Carter, and R. Kohn (2000). Efficient Bayesian Inference for DynamicMixture Models. Journal of the American Statistical Association 95 (451), 819–828.

Geweke, J. (1992). Evaluating the Accuracy of Sampling-Based Approaches to theCalculation of Posterior Moments. Bayesian Statistics - J.M. Bernardo, J. Berger,A.P. David, A.F.M. Smith eds., Oxford University Press , 169–193.

Geweke, J. (1998). Using Simulation Methods for Bayesian Econometric Models: In-ference, Development and Communication. Federal Reserve Bank of Minneapolis,Research Department Staff Report 249.

Giannone, D., M. Lenza, and G. E. Primiceri (2012). Prior Selection for Vector Au-toregressions. Working Paper .

Hall, R. E. (2009). By How Much Does GDP Rise If the Government Buys MoreOutput? Brookings Papers on Economic Activity Fall, 183–231.

Jorda, O. (2005). Estimation and Inference of Impulse Responses by Local Projections.American Economic Review 95 (1), 161–182.

Juselius, K. (2006). The Cointegrated VAR Model. Oxford University Press .

Justiniano, A. and G. E. Primiceri (2008). The Time-Varying Volatility of Macroeco-nomic Fluctuations. American Economic Review 98 (3), 604–641.

Kilian, L. (1998). Small Sample Confidence Intervals for Impulse Response Functions.The Review of Economics and Statistics 80 (2), 218–230.

Kilian, L. and P.-L. Chang (2000). How Accurate are Confidence Intervals for ImpulseResponses in Large VAR Models? Economics Letters 69, 299–307.

37

Kim, S., N. Shephard, and S. Chib (1998). Stochastic Volatility: Likelihood Inferencein Comparison with ARCH Models. The Review of Economic Studies 65 (3), 361–393.

Kirchner, M., J. Cimadomo, and S. Hauptmeier (2010). Transmission of GovernmentSpending Shocks in the Euro Area - Time Variation and Driving Forces. ECBWorking Paper 1219.

Koop, G., R. Leon-Gonzalez, and R. W. Strachan (2009). On the Evolution of MonetaryPolicy. Journal of Economic Dynamics and Control 33, 997–1017.

Muet, P.-A. (1994). La récession de 1993 réexaminée. Revue de l’OFCE 49, 103–123.

Owyang, M. T., V. A. Ramey, and S. Zubairy (2013). Are Government SpendingMultipliers Greater during Periods of Slack? Evidence from Twentieth-CenturyHistorical Data. American Economic Review 103 (3), 129–134.

Perotti, R. (2002). Estimating the Effects of Fiscal Policy in OECD Countries. ECBWorking Paper No 168 .

Perotti, R. (2007). In Search of the Transmission Mechanism of Fiscal Policy. NBERMacroeconomics Annual 22, 169–226.

Perotti, R. (2011). Expectations and Fiscal Policy: An Empirical Investigation.Mimeo.

Primiceri, G. (2005). Time Varying Structural Vector Autoregressions and MonetaryPolicy. The Review of Economic Studies 72 (3), 821–852.

Ramey, V. A. (2011a). A Reply to Roberto Perotti’s "Expectations and Fiscal Policy:An Empirical Investigation". Mimeo.

Ramey, V. A. (2011b). Identifying Government Spending Shocks: It’s All in the Tim-ing. The Quarterly Journal of Economics 126 (1), 1–50.

Sims, C. A. (1992). Interpreting the Macroeconomic Time Series Facts - The Effectsof Monetary Policy. European Economic Review 36, 975–1011.

Sims, C. A., J. H. Stock, and M. W. Watson (1990). Inference in Linear Time SeriesModels with Some Unit Roots. Econometrica 58 (1), 113–144.

Sims, E. R. (2009). Non-Invertibilities and Structural VARs. Mimeo.

Stock, J. H. and M. W. Watson (1996). Evidence on Structural Instability in Macroe-conomic Time Series Relations. Journal of Business and Economic Statistics 14 (1),11–30.

Stock, J. H. and M. W. Watson (2001). Vector Autoregressions. Journal of EconomicPerspectives 15 (4), 101–115.

38

Sutherland, A. (1997). Fiscal Crises and Aggregate Demand: Can High Public DebtReverse the Effects of Fiscal Policy. Journal of Public Economics 65, 147–162.

Woodford, M. (2011). Simple analytics of the government expenditure multiplier.American Economic Journal Macroeconomics 3 (1), 1–35.

39

A Data handling

A.1 Data in log-levels (except interest rate in % points) with

quadratic trends

Figure 18: Data in log-levels (specif. with prices) with quadratic trends

40

A.2 Data in log-differences (except interest rate in % points)

with linear trends

Figure 19: Data in log-levels (specif. with inflation) with linear trends

41

B Defining government expenditures using the SNA

The 1993 System of National Accounts (1993 SNA) is an international reference manualon national accounts35. It has been produced jointly by the OECD, the United NationsStatistical Division, the International Monetary Fund, the World Bank and the Com-mission of the European Communities. The 1995 European Accounting System (1995ESA) directly derives from the 1993 SNA: it is the reference manual for the elaborationof national accounts all over the European Union.

The sum of general government (S13)36 consumption (P3) and investment (i.e.: grossfixed capital formation, P51) is the most obvious definition of "government expenditures".In this case, net receipts are defined as the difference between the government financingcapacity (B9A) and these expenditures. Net receipts mainly include taxes, net of subsidiesand transfers.