Embed Size (px)

Citation preview

Enseigner la macroeconomie apres la crise

Steve Ambler, ESG UQAM, C.D. Howe, RCEA 1

septembre 2014

Les modeles keynesiens standard

I Secteurs: firmes, menages, gouvernement.

I Intermediation financiere: automatique.

I L’epargne des menages est canalisee vers les projetsd’investissement les plus productifs.

I 2007–2008: du sable dans l’engrenage du systeme financier.

I Les banques cessent de preter entre elles et l’intermedationfinancier devient inefficiente.

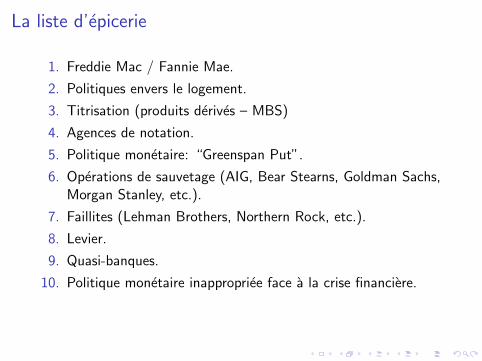

La liste d’epicerie

1. Freddie Mac / Fannie Mae.

2. Politiques envers le logement.

3. Titrisation (produits derives – MBS)

4. Agences de notation.

5. Politique monetaire: “Greenspan Put”.

6. Operations de sauvetage (AIG, Bear Stearns, Goldman Sachs,Morgan Stanley, etc.).

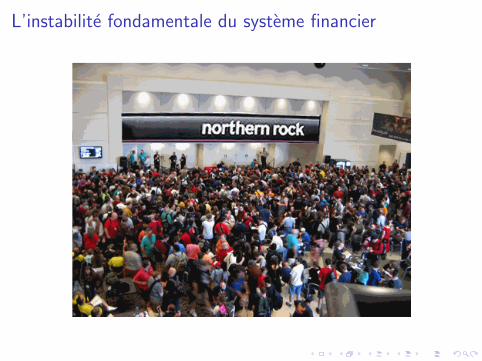

7. Faillites (Lehman Brothers, Northern Rock, etc.).

8. Levier.

9. Quasi-banques.

10. Politique monetaire inappropriee face a la crise financiere.

I Est-ce qu’il y a un ou deux themes unificateurs?

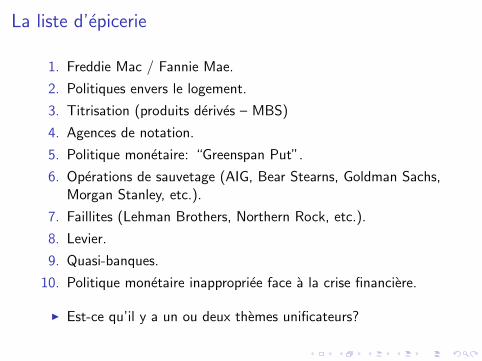

La liste d’epicerie

1. Freddie Mac / Fannie Mae.

2. Politiques envers le logement.

3. Titrisation (produits derives – MBS)

4. Agences de notation.

5. Politique monetaire: “Greenspan Put”.

6. Operations de sauvetage (AIG, Bear Stearns, Goldman Sachs,Morgan Stanley, etc.).

7. Faillites (Lehman Brothers, Northern Rock, etc.).

8. Levier.

9. Quasi-banques.

10. Politique monetaire inappropriee face a la crise financiere.

I Est-ce qu’il y a un ou deux themes unificateurs?

Sources

I Russell Roberts (2010), “Gambling with other People’sMoney: How Perverted Incentives Caused the FinancialCrisis.” Mercatus Centerhttp://mercatus.org/publication/gambling-other-peoples-money

I Gary Gorton (2010), Slapped by the Invisible Hand: ThePanic of 2007. Oxford University Press

I James Gwartney (2013), “The Public Choice Revolution in thePractice and Teaching of Economics.” Public Choice Societyhttp://publicchoicesociety.org/content/papers/

jamesgwartney-1119-2014-1622.pdf

I Congdon, Tim (2014), “What Were the Causes of the GreatRecession? The Mainstream Approach versus the MonetaryInterpretation.” World Economics 15, 1–32

L’instabilite fondamentale du systeme financier

Gorton

1. Paniques bancaire du 21e siecle.

2. Toujours une possibilite en presence de la transformation desecheances.

3. Possibilite d’equilibres multiples.

Risque moral

Roberts

1. Incitatifs pervers.

2. On fait moins attention aux risques lorsqu’on a confiance quec’est le contribuable qui va subir les pertes.

3. Captation reglementaire.

4. Equilibres multiples.

Theme unificateur parmi les themes unificateurs

Choix public

I Gwartney, 2013: “Rather than analyzing how both marketsand collective decision-making handle economic problems,mainstream economics continues to model government as if itwere an omniscient, benevolent social planner available toimpose ideal solutions . . .

I . . . the relevant choice is always between the real-worldoperation of markets and the real-world operation of thepolitical process.”

Choix public

I Gwartney, 2013: “Rather than analyzing how both marketsand collective decision-making handle economic problems,mainstream economics continues to model government as if itwere an omniscient, benevolent social planner available toimpose ideal solutions . . .

I . . . the relevant choice is always between the real-worldoperation of markets and the real-world operation of thepolitical process.”

Choix public

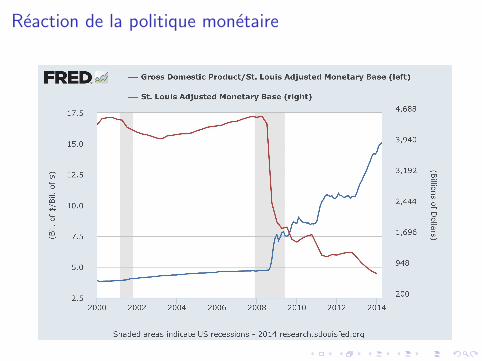

Reaction de la politique monetaire

I Panique financiere → demande de liquiditeI Deux reactions possibles par la Fed:

1. Fournir de la liquidite par des operations open market (solutionplus de marche);

2. Fournir des prets directement aux banques et auxquasi-banques (politique d’allouer directement le credit).

I La Fed est devenu un intermediaire financier tres important.

I L’importance de faire quelque chose, meme n’importe quoi.Bernanke: “There are no atheists in foxholes.”

I Par contre, la Fed n’a pas repondu suffisamment al’augmentation de la demande de monnaie.

Reaction de la politique monetaire